Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

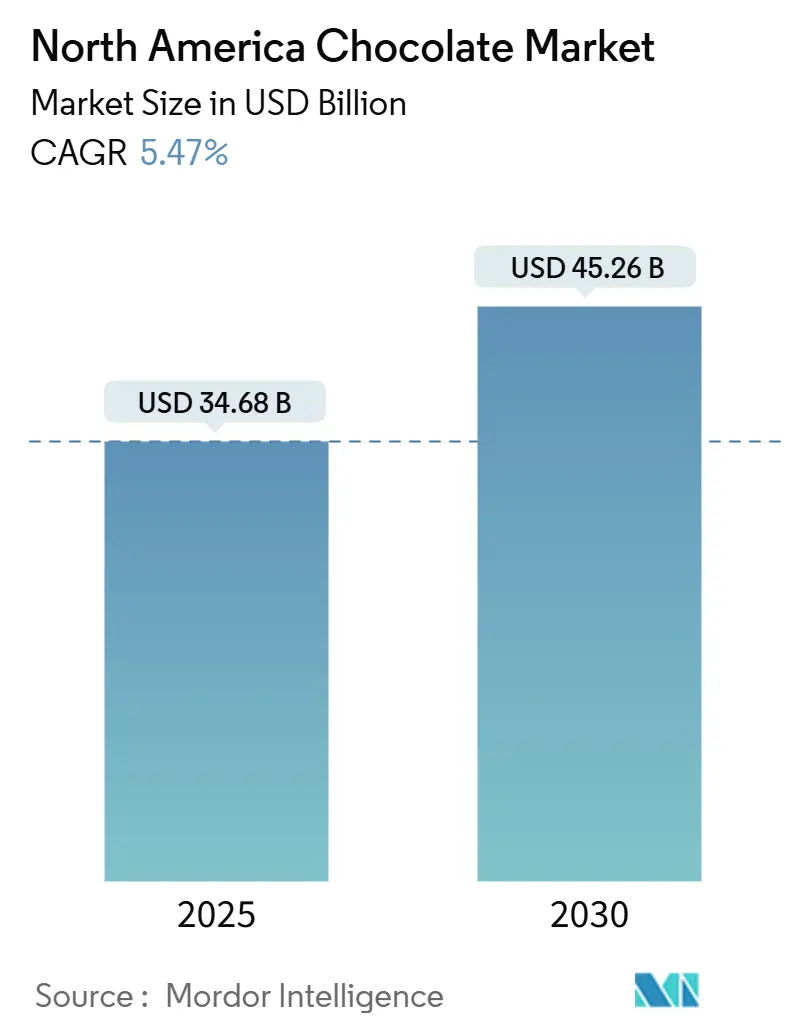

| Market Size (2025) | USD 34.68 Billion |

| Market Size (2030) | USD 45.26 Billion |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

| Fastest Growing Market | Supermarket/Hypermarket |

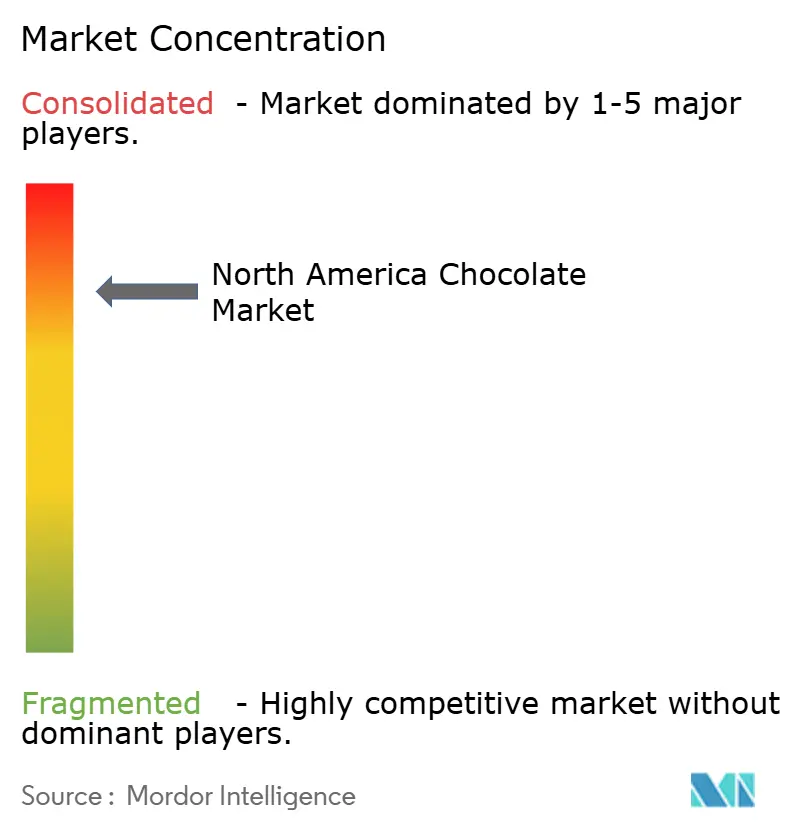

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Chocolate Market Analysis by Mordor Intelligence

The North America chocolate market size in North America is valued at USD 34.68 billion in 2025 and is projected to reach USD 45.26 billion by 2030, reflecting a 5.47% CAGR over the forecast period. Consumers are increasingly opting for premium bars, leading to an expansion in the market. Manufacturers are emphasizing single-origin transparency to appeal to ethically conscious buyers, while retailers are dedicating more shelf space to certified products, reflecting growing consumer demand for quality and sustainability. This momentum is further bolstered by rising disposable incomes, which enable consumers to spend more on premium offerings, innovations in plant-based alternatives catering to dietary preferences, and a notable increase in online subscription boxes that provide convenience and variety. Yet, challenges loom: volatile cocoa futures create uncertainty in raw material costs, stricter calorie guidelines from the FDA necessitate reformulations to meet regulatory standards, and mandates for sustainable packaging increase production expenses. These factors are putting pressure on profitability as producers find themselves at a crossroads, weighing the decision to pass on costs to consumers against the need to defend volume and market share. Meanwhile, competitive pressures mount as craft bean-to-bar labels, known for their artisanal appeal, push established players to enhance supply-chain visibility and adopt more experiential formats to stay relevant in a dynamic market.

Key Report Takeaways

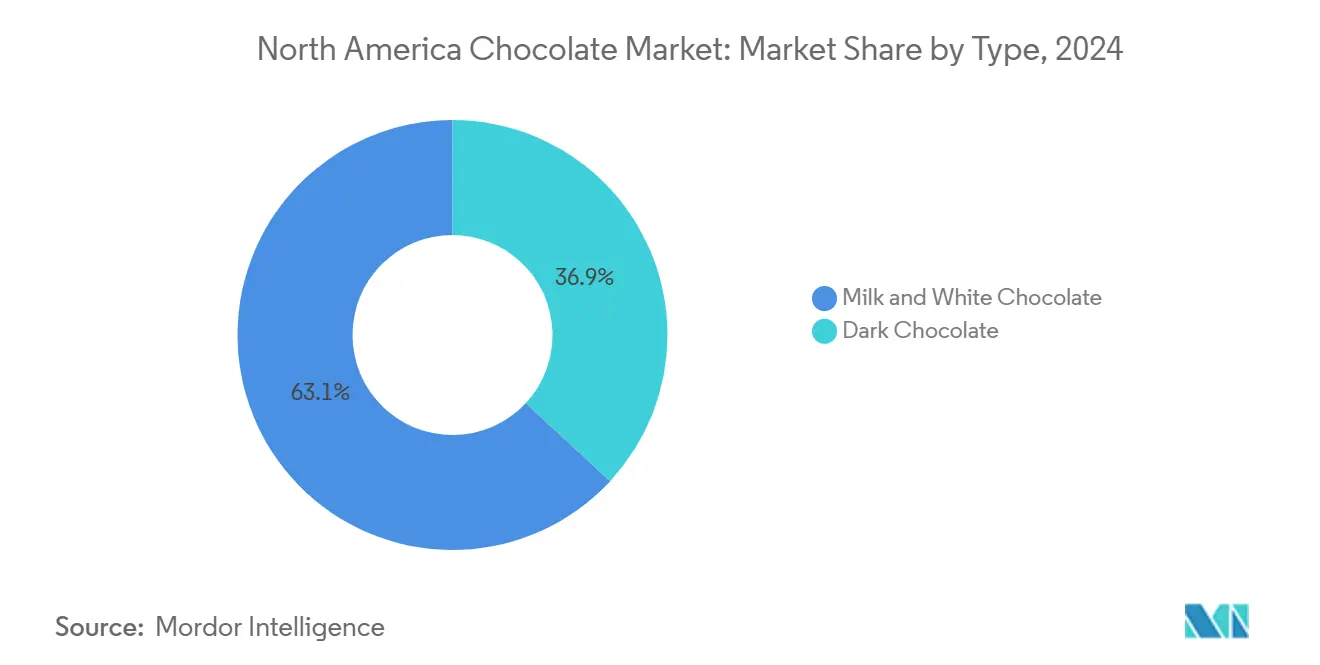

- By product type, milk and white varieties led with 63.10% of the dark chocolate market share in 2024, while dark chocolate is forecast to post the fastest 6.12% CAGR through 2030.

- By form, tablets captured 71.53% revenue share in 2024; pralines and truffles are projected to expand at a 7.41% CAGR between 2025-2030.

- By price range, the mass segment accounted for 57.15% of 2024 sales; premium offerings are set to grow at an 8.15% CAGR.

- By ingredient type, dairy-based products retained 59.13% share in 2024, whereas single-origin SKUs will accelerate at a 9.15% CAGR.

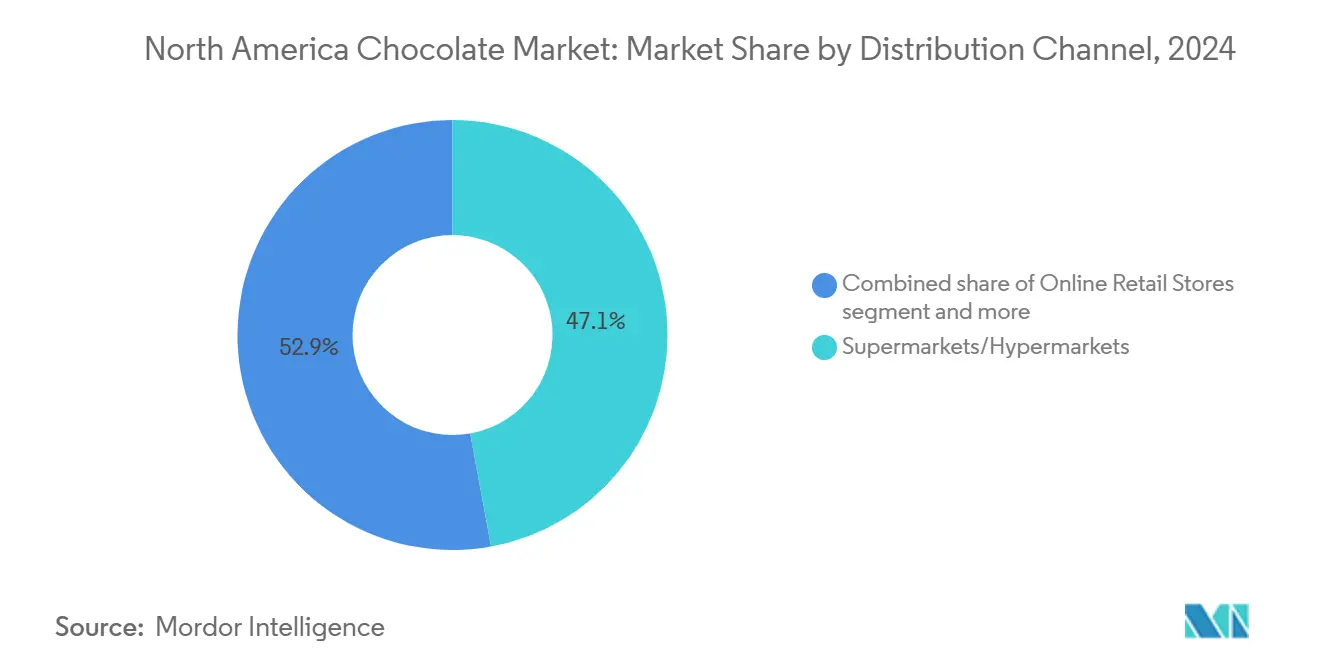

- By distribution channel, supermarkets controlled 47.14% of 2024 value; online retail is advancing at a 6.72% CAGR through 2030.

- Geographically, the United States generated 81.53% of regional revenue in 2024; Mexico represents the fastest-growing locale at a 6.51% CAGR.

North America Chocolate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium and dark chocolate | +0.9% | United States, Canada | Medium term (2-4 years) |

| Seasonal gifting culture and occasions | +0.7% | United States, Canada | Short term (≤ 2 years) |

| Flavour and format innovations | +0.8% | United States, Canada | Medium term (2-4 years) |

| Bean-to-bar craft transparency trend | +0.6% | United States, Canada | Long term (≥ 4 years) |

| Ethical-sourcing commitments by retailers | +0.5% | North America, driven by the United States and Canadian retailers sustainability mandates | Long term (≥ 4 years) |

| Increasing demand for plant-based and vegan chocolate | +0.7% | United States and Canada, with emerging interest in Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising demand for premium and dark chocolate

Health-conscious shoppers are gravitating towards premium SKUs, drawn by the allure of flavonoids, reduced sugar content, and the authenticity of single-origin products. Barry Callebaut's 2024 consumer survey revealed that 73% of buyers are on the hunt for novel taste experiences, while 53% place a premium on well-being cues. This dual focus sheds light on the growing trend of consumers 'trading up.' The trend is further propelled by Gen Z and Millennials, who are increasingly opting for plant-based milk alternatives. This shift is steering research and development efforts towards crafting oat- and almond-based ganaches. While affluent urban centers lead the charge in embracing these premium innovations, rural households continue to gravitate towards value multipacks. This dynamic landscape necessitates a strategy that balances premium innovation with affordability in mass channels.

Seasonal gifting culture and occasions

Holidays such as Valentine's Day, Easter, Halloween, and winter festivities play a pivotal role in driving the annual chocolate turnover in the region. These occasions, deeply intertwined with gifting traditions, see a notable surge in consumer demand. According to the National Confectioners Association, chocolate dominates the U.S. confectionery landscape, accounting for a substantial 56% share[1]Source: National Confectioners Association, "New NCA Report Reveals Latest Consumer Trends in Chocolate Consumption", candyusa.com . Leading the charge during these seasonal peaks are pralines and truffles. Their decorative packaging and artisanal nuances not only elevate their appeal but also allow them to command premium price points. Although late-season weather fluctuations and shifting holiday calendars can introduce sales unpredictability, e-commerce emerges as a stabilizing force. It enables gifting throughout the year, lessening the reliance on traditional retail outlets. Brands are broadening the gifting narrative beyond just holidays. By linking it to self-care moments, birthdays, and corporate events, they're not only evening out revenue fluctuations but also deepening consumer relationships and broadening their market presence.

Flavor and format innovations

Caramelized nuts, sea salt, and freeze-dried fruit elevate a standard commodity bar into a premium sensory delight by adding unique flavors and textures that appeal to discerning consumers. Indulgent-filled centers, like liquid caramel or fruit purée, enhance the experience further, while portion-controlled squares address the growing demand for calorie-conscious snacking options. Lindt's April 2024 launch of OatMilk truffles exemplifies the successful integration of dairy-free innovation with texture-driven allure, catering to evolving consumer preferences for plant-based indulgence. The challenge remains: how to automate artisanal methods at scale without compromising the craftsmanship and quality that justify premium pricing and maintain brand loyalty.

Bean-to-bar craft transparency trend

Bean-to-bar producers manage every step of the process, from sourcing ingredients to molding the final product, ensuring traceability that appeals to ethically conscious consumers. This approach not only guarantees quality but also provides transparency regarding the origins of ingredients, which is increasingly valued in the market. In 2024, Hershey announced it achieved 89% visibility in cocoa sourcing and aims for complete traceability by 2025, reflecting its commitment to ethical practices. While craft chocolate production is limited in volume, its impact is significant enough to compel multinational companies to bolster their partnerships with farmers, improve supply chain transparency, and disclose sourcing origins to meet growing consumer demand for accountability.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cocoa and sugar prices | -0.8% | North America | Short term (≤ 2 years) |

| Calorie-reduction health regulations | -0.6% | United States | Medium term (2-4 years) |

| Supply-chain fragility in West Africa | -0.7% | Global sourcing | Short term (≤ 2 years) |

| Sustainable-packaging cost burden | -0.5% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile cocoa and sugar prices

In late 2024, cocoa futures surged due to faltering yields in West Africa, driven by adverse weather conditions and pest infestations that impacted production. This, in turn, tightened U.S. exchange stocks by 11%, according to the International Cocoa Organization, creating supply constraints in the market[2]Source: International Cocoa Organization, "Cocoa Market Report for December 2024", icco.org. Concurrently, rising sugar costs, fueled by global inflation and supply chain disruptions, intensified the pressure on manufacturers. While private-label competitors maintained their prices, they capitalized on this strategy, drawing market share away from premium brands by appealing to cost-conscious consumers. Multinational corporations, equipped with advanced hedging techniques and direct contracts with farms, found a buffer against these market shifts, enabling them to manage risks more effectively. In contrast, smaller producers, lacking such financial flexibility and resources, felt the brunt of the market's pressures, heightening the push towards industry consolidation as they struggled to remain competitive.

Calorie-reduction health regulations

The FDA is tightening its grip on labeling and portion sizes, zeroing in on high-calorie and sugary items, with chocolate in its sights. Although the final rules are still under wraps, the agency's direction hints at stricter disclosure mandates and possible warning labels for products that overshoot calorie or added-sugar limits. This regulatory push is nudging manufacturers to either cut back on sugar, downsize portions, or bolster products with fiber and protein to sidestep negative perceptions. Yet, reducing sugar in chocolate isn't straightforward: using alternative sweeteners like stevia, erythritol, or allulose can lead to aftertastes or change the mouthfeel, which might not sit well with consumers. While moving from king-size chocolate bars to single, individually wrapped squares can help tackle calorie issues, it risks eating into profits if shoppers opt for fewer pieces. The weight of compliance isn't evenly distributed: bigger manufacturers have the resources for research and development and labeling changes, but smaller craft producers might struggle with the costs, potentially pushing the market towards further consolidation.

Segment Analysis

By Product Type: Health Narratives Propel Dark Chocolate

In 2024, milk and white chocolate command a dominant 63.10% share of the global chocolate market. Their stronghold stems from traditional preferences and their widespread application in baking, confectionery, and novelty items. These types of chocolate are often favored for their creamy texture and sweet flavor, making them a staple in various culinary applications. While brand loyalty and consumer recognition fortify their position, they face a noticeable slowdown amid rising health trends. In response, manufacturers are modernizing age-old recipes, reducing sugar content, and incorporating plant-based ingredients to cater to health-conscious consumers. Furthermore, innovations like ruby chocolate and dark-milk blends are ensuring brands remain appealing to consumers who desire variety but lean towards familiar flavors. These new offerings not only provide novelty but also help brands differentiate themselves in an increasingly competitive market.

Conversely, dark chocolate is rapidly gaining traction, with projections indicating a CAGR of 6.12% in the coming years. This growth is fueled by a consumer shift towards flavonoid-rich, lower-sugar options that align with wellness and premium indulgence. Dark chocolate is often perceived as a healthier alternative due to its higher cacao content and lower sugar levels, which appeal to health-conscious individuals. Bars boasting high cacao content benefit from a heightened appreciation for unique flavor profiles and origin-centric marketing. By emphasizing single-origin sourcing, dark chocolate draws parallels to the artisanal worlds of coffee and beer, boosting its allure. These narratives not only highlight the craftsmanship involved but also resonate with consumers seeking authenticity and exclusivity. As consumer tastes evolve, dark chocolate is set to secure an even larger share of the chocolate market's value sales, driven by its ability to cater to both health and premium indulgence trends.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Tablets Dominate, Truffles Surge

In 2024, tablets took the lead in the dark chocolate market, seizing a significant 71.53% share. Their triumph stems from a cost-effective molding process, versatile portion sizes, and a widespread retail footprint. As the cornerstone of the dark chocolate segment, tablets appeal to a broad consumer demographic, amplifying value through volume. Additionally, their ability to cater to both everyday consumption and premium offerings has made them a versatile choice for manufacturers. Moreover, the incorporation of premium inclusions, such as nuts, fruits, and exotic flavors, has elevated their price point, solidifying tablets' dominance in the market amidst shifting consumer preferences. With their inherent accessibility and versatility, producers increasingly rely on this segment for steady revenue in the dark chocolate landscape.

Conversely, the pralines and truffles segment, though smaller in volume, is rapidly emerging as the fastest-growing niche in dark chocolate, with a projected CAGR of 7.41%. This growth is largely fueled by seasonal gifting and the rising trend of experiential snacking, drawing in consumers seeking premium treats. Boxed chocolates, particularly those priced between USD 15-20, are becoming popular choices for both self-gifting and corporate presents, enhancing margins for the dark chocolate sector. The segment's appeal lies in its ability to offer a luxurious and personalized experience, often featuring intricate designs, unique packaging, and high-quality ingredients. With a strong focus on luxury and occasion-based consumption, this segment is establishing a notable and expanding footprint in the dark chocolate market.

By Price Range: Premium Gains Outpace Mass

In 2024, mass-priced dark chocolate SKUs held a commanding 57.15% share of market spending, ensuring volume stability by prioritizing everyday affordability for consumers. These mass lines, backed by strong brand loyalty and extensive omnichannel retail partnerships, skillfully navigate rising cocoa costs that threaten their value proposition. However, as consumers shift towards premium and specialty chocolate experiences, growth in this segment has slowed. To remain relevant, mass brands are rolling out selective premium extensions, such as organic and single-origin variants, countering commoditization and sparking heightened consumer interest. These premium extensions allow mass brands to tap into evolving consumer preferences for higher-quality and ethically sourced products while maintaining their competitive edge in the broader market.

Conversely, premium dark chocolate lines are on an upward trajectory, with an expected CAGR of 8.15%. This growth, outpacing mass lines, is driven by consumers' increasing appetite for limited-edition and ethically sourced products. With subscription services and specialty retail channels expanding, the premium segment is set for double-digit share gains, resonating with consumers who value authenticity, wellness, and exclusivity. These preferences not only validate higher price points but also enhance profit margins. Moreover, premium offerings are capitalizing on trends like single-origin storytelling, organic certification, and distinctive flavor infusions, reinforcing their strong growth prospects in the vast dark chocolate market. The focus on unique narratives and sustainable practices further strengthens the premium segment's appeal, enabling brands to build deeper connections with a discerning consumer base.Highlighting this trend, the National Confectioners Association revealed that 71% of mainstream consumers indulge in premium chocolate, underscoring that the allure of premiumization transcends elite demographics, resonating as an occasional treat across various income levels[3]Source: National Confectioners Association, "Getting to Know Chocolate Consumers 2024", candyusa.com.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ingredient Type: Single-Origin Surges as Dairy Holds Base

In 2024, dairy-based chocolate commands a market share of approximately 59.13%. Its creamy texture and familiar taste have solidified its top position, making it a preferred choice among consumers. Milk chocolate, known for its smoothness and comforting flavor, resonates with diverse age groups and regions, from children to older adults, and across both developed and emerging markets. This widespread appeal guarantees its continued prominence, even amidst changing trends and evolving consumer preferences. Furthermore, milk chocolate's association with the functional food movement, emphasizing its nutritional perks like calcium and protein, boosts its popularity among health-conscious consumers. Its adaptability across various sectors, from confectionery and bakery to beverages, reinforces its market dominance, as manufacturers continue to innovate and incorporate it into new product offerings.

Meanwhile, single-origin chocolate emerges as the market's bright spot, with a projected growth rate of 9.15% CAGR. By spotlighting terroir storytelling and establishing direct farmer connections, it carves a distinct niche in the competitive dark chocolate landscape. This premium segment capitalizes on consumers' heightened desire for authenticity, origin, and unique flavor experiences. Single-origin chocolate often highlights the specific regions where cocoa beans are sourced, offering consumers a deeper connection to the product and its origins. Plant-based chocolate, though still in its infancy, is charting its own growth path. Despite facing regulatory challenges, particularly around non-dairy "milk" labeling in the U.S., the segment thrives on innovation. It appeals to a growing demographic that values sustainability and dairy alternatives, bolstering its optimistic growth outlook. The increasing availability of plant-based chocolate in retail and online channels, coupled with its appeal to vegan and lactose-intolerant consumers, further drives its market potential.

By Distribution Channel: Supermarkets Lead, Online Accelerates

In 2024, supermarkets, with strategic placements near checkouts and enticing multi-pack promotions, effectively reached mainstream consumers, dominating the dark chocolate market with a turnover share of approximately 47.14%. These strategies not only encouraged impulse purchases but also catered to budget-conscious shoppers seeking value deals. Despite facing rising slotting fees, supermarkets, bolstered by their widespread accessibility and established consumer trust, played a pivotal role in driving volume sales. By offering a diverse range of products, from mainstream to premium dark chocolates, they catered to varying consumer preferences and cemented their position as the primary offline distribution channel. Their ability to stock both well-known brands and private-label options further enhanced their appeal to a broad consumer base.

Online retail, though currently holding a smaller market share, is witnessing a robust growth spurt, expanding at a CAGR of 6.72%. This growth is predominantly fueled by curated subscription boxes, direct-to-consumer brands, and algorithm-driven personalized shopping experiences, all of which navigate around the limitations of traditional shelf space. The convenience of home delivery, coupled with the ability to compare products and read reviews, has made online platforms increasingly attractive to consumers. Beyond being mere sales platforms, online avenues empower craft chocolatiers and niche producers to reach distant markets, overcoming geographical barriers. Consumers, in turn, enjoy access to premium, artisanal, and ethically sourced dark chocolate varieties, often unavailable in physical stores. This evolving online landscape is not only broadening the reach of dark chocolate distribution but also deepening consumer engagement, surpassing the limitations of traditional retail.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Chocolate Market in the United States

In 2024, the U.S. accounted for a commanding 81.53% of regional sales, driven by high per-capita consumption, deep supermarket penetration, and a strong gifting culture. The U.S. market's dominance highlights its role as a trendsetter in the region, where consumer preferences and regulatory changes often set the tone for neighboring markets. Consequently, shifts in FDA regulations send ripples throughout the dark chocolate market, influencing product formulations, labeling, and marketing strategies. Today's growth is more about premium offerings, plant-based options, and direct-to-consumer sales than just volume, reflecting evolving consumer priorities toward health, sustainability, and convenience.

Mexico is on the fast track, boasting a 6.51% CAGR, as urbanization and rising disposable incomes shift preferences from traditional drinking tablets to premium bars. This transition underscores a growing appetite for higher-quality products among Mexican consumers, driven by increased exposure to global trends and changing lifestyles. In response to this surging demand, multinationals are not only adopting bilingual packaging but also enhancing their cold-chain logistics to ensure product quality in a challenging climate. These investments are critical for maintaining competitiveness in a rapidly evolving market.

Canada's growth is steady but tempered, a reflection of its smaller population and established consumption patterns. While provincial labeling and bilingual packaging present logistical challenges, alignment with U.S. standards simplifies product introductions, enabling smoother cross-border trade. The Canadian market's maturity is characterized by a focus on niche segments, such as organic and fair-trade chocolate, which cater to its health-conscious and ethically driven consumers. Meanwhile, niches in the Caribbean and Central America, buoyed by tourism and selective imports, exert minimal influence on broader market forecasts. These regions rely heavily on seasonal demand and imported products, limiting their structural impact on the overall market dynamics.

Competitive Landscape

The exhibits moderate concentration with the presence of Mars, Hershey, Mondelez, Ferrero, Nestlé, and Lindt dominating the chocolate market. Leveraging global sourcing networks and a diverse brand portfolio, these industry giants can navigate cocoa price fluctuations effectively. They also channel significant investments into research and development, focusing on developing innovative sugar-reduced and plant-based products to meet growing health-conscious consumer demands. Their expansive scale not only offers a competitive advantage but also enables them to respond swiftly and efficiently to evolving consumer preferences, stringent regulatory requirements, and market dynamics.

Mondelez's interest in acquiring Hershey, highlighted in April 2025, signals a push for greater consolidation, albeit with potential antitrust challenges. Such a move reflects the broader trend of market leaders seeking to strengthen their foothold and expand their product offerings. On the other hand, bean-to-bar innovators like Theo, Askinosie, and Mast are carving out a niche, emphasizing traceability and compelling packaging narratives. These disruptors appeal to a growing segment of consumers who prioritize ethical sourcing and transparency. This has nudged larger players to highlight their farmer initiatives and advancements like satellite mapping, aiming to align with evolving consumer expectations.

Adoption of technology varies: established players harness AI for demand forecasting, blockchain for traceability, and automation in molding to streamline operations and enhance efficiency. In contrast, artisanal producers emphasize hand-tempering and small-batch roasting as hallmarks of authenticity, catering to consumers who value craftsmanship. Retailers are tightening ethical sourcing standards, and with extended producer responsibility fees on the horizon for packaging, a financial chasm may emerge between the well-resourced industry leaders and niche startups. This evolving landscape underscores the importance of innovation and adaptability for all market participants.

North America Chocolate Industry Leaders

-

Ferrero International SA

-

Mars Incorporated

-

Mondelēz International Inc.

-

Nestlé SA

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Ice Breakers has unveiled its innovative flavor-shifting gum, which boasts a unique technology that transitions from one flavor to another during chewing. This new product aims to enhance the consumer experience by offering a dynamic and engaging taste journey, setting it apart in the competitive gum market.

- November 2025: Mars Inc. has rolled out a new range of confectionery delights, featuring favorites like M&M's and Twix. Among the highlights, the Twix brand introduced its latest creation: the Twix Snowmen, a whimsical snowman-shaped bar that melds cookie, caramel, and creamy milk chocolate.

- October 2025: Zotter Chocolates has unveiled its latest creation: the Brains and Eggs chocolate bar, a unique addition to its product lineup that showcases the brand's innovative approach to chocolate-making.

- June 2025: Cacao Hunters brand has unveiled a premium line of chocolates, crafted from single-origin cacao. These chocolates are designed to offer a unique flavor profile that reflects the distinct characteristics of their origin. The brand emphasizes its commitment to ethics, asserting that all ingredients are responsibly and sustainably sourced.

North America Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single-origin |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Store |

| Online Retail |

| Others |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single-origin | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Store | |

| Online Retail | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF