Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 6.23 Billion |

| Market Size (2030) | USD 8.31 Billion |

| Growth Rate (2025 - 2030) | 5.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Cereal Bar Market Analysis by Mordor Intelligence

The North America cereal bar market is projected to grow from USD 6.23 million in 2025 to USD 8.31 million by 2030, registering a compound annual growth rate (CAGR) of 5.93%. This growth is driven by increasing health consciousness among consumers, regulatory changes, and rapid product reformulations that are transforming cereal bars from being perceived as discretionary snacks to legitimate meal replacement options. The United States Food and Drug Administration's (FDA) updated definition of "healthy," which will take effect in February 2025, prioritizes recipes that incorporate whole-food ingredients while discouraging those with high levels of added sugars and sodium [1]Source: Federal Register, “Food Labeling: Nutrient Content Claims; Definition of Term 'Healthy’,” federalregister.gov. Retailers are responding by expanding shelf space for natural and organic products, prompting brands to seek certifications such as USDA Organic (United States Department of Agriculture Organic) and Non-GMO Project (Non-Genetically Modified Organism Project) verification. Furthermore, 71% of North American consumers now express a preference for obtaining protein from whole foods, which is driving the popularity of high-protein, low-sugar cereal bars in mainstream grocery stores. The growth of e-commerce and direct-to-consumer subscription models is also playing a significant role in accelerating the market by reducing customer acquisition costs and enabling the delivery of personalized nutrition bundles.

Key Report Takeaways

- By product type, energy and nutrition bars are projected to expand at a 7.43% CAGR through 2030, while granola and muesli bars held 44.32% of 2024 volume.

- By functional claim, organic formulations account for 22.68% of 2024 revenue and are forecast to grow at a 7.72% CAGR to 2030.

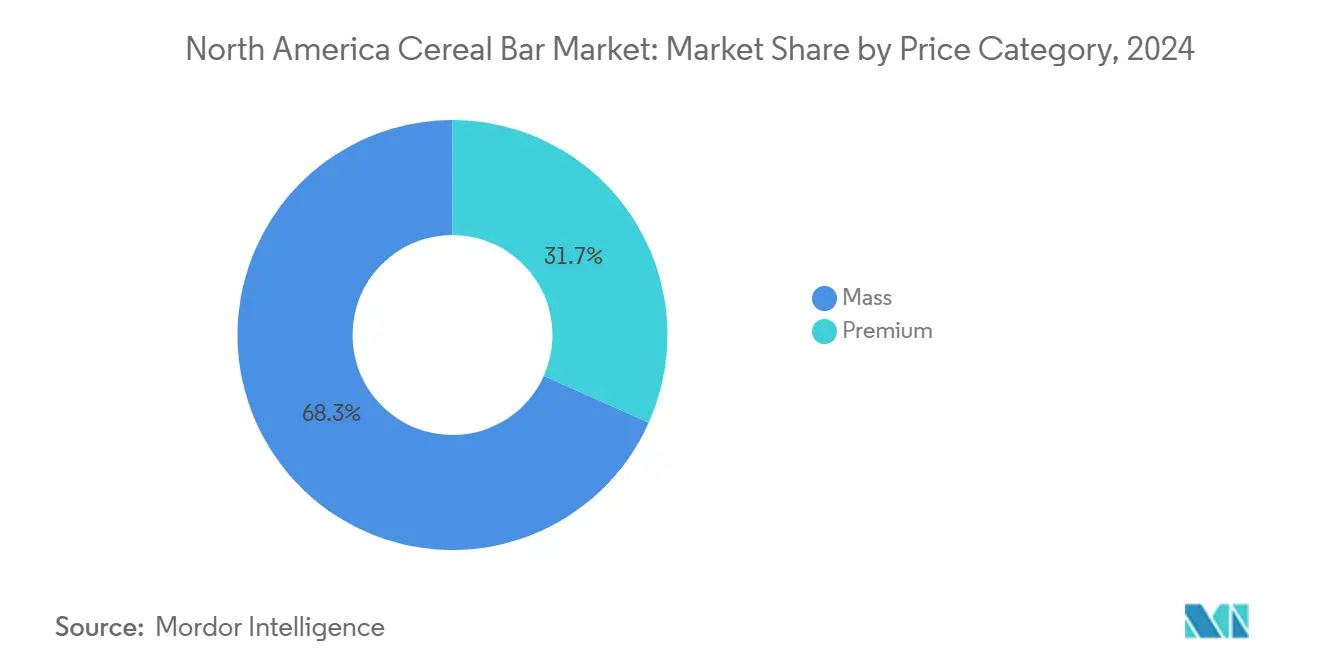

- By price category, mass-market SKUs captured 68.32% of 2024 sales; premium offerings are advancing at a 6.82% CAGR.

- By distribution, supermarkets and hypermarkets generated 39.92% of 2024 value, yet online channels are expanding at a 7.02% CAGR.

- By geography, the United States held 77.21% of 2024 volume; Mexico is the fastest-growing country at a 7.63% CAGR

North America Cereal Bar Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and focus on functional nutrition | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Expansion of clean label and non-GMO product offerings | +0.9% | United States, Canada | Short term (≤ 2 years) |

| Growth in plant-based and vegan product lines | +0.8% | United States, Canada | Medium term (2-4 years) |

| Increase in sports, fitness, and outdoor activity participation | +0.7% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Rise of gluten-free, allergy-friendly, and specialty diet formats | +0.6% | United States, Canada | Short term (≤ 2 years) |

| E-commerce and direct-to-consumer distribution growth | +1.1% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Health Consciousness and Focus on Functional Nutrition

North American consumers are increasingly perceiving cereal bars as functional nutrition products rather than indulgent snacks. This trend highlights a growing preference for products emphasizing protein content, gut-health ingredients, and micronutrient fortification over flavor. A significant portion of consumers believes that proper nutrition and regular physical activity can positively influence the aging process. Additionally, many consumers prefer obtaining protein from whole foods rather than relying on dietary supplements. This shift in preferences has driven demand for cereal bars that provide 10 to 15 grams of protein per serving, with ingredient lists that are simple and easy to recognize. Premium product offerings now incorporate prebiotic fibers, such as those sourced from watermelon, honeydew, and mango rinds, catering to health-conscious shoppers who prioritize gut health as a critical component of overall wellness.

Expansion of Clean Label and Non-GMO Product Offerings

Clean-label formulations, defined by short ingredient lists, easily recognizable components, and minimal processing, have evolved from being premium differentiators to becoming essential requirements for achieving mass-market distribution. The sales of organic snack bars have grown significantly, with numerous launches of organic bars recorded in recent years. This growth reflects the increasing allocation of shelf space by retailers to products certified as organic by the United States Department of Agriculture (USDA). Similarly, Non-Genetically Modified Organism (Non-GMO) Project Verification has emerged as a standard expectation for distribution within natural retail channels. Brands that do not carry the butterfly seal, which signifies Non-GMO Project Verification, face the risk of being removed from shelves at major retailers such as Whole Foods Market and Sprouts Farmers Market. At the same time, advancements in sweetener innovation continue to gain momentum. Alternatives such as stevia, monk fruit, tagatose, and allulose are increasingly replacing high-fructose corn syrup and cane sugar, addressing consumer demand for low-glycemic options that help avoid insulin spikes.

Growth in Plant-Based and Vegan Product Lines

Plant-based protein bars are gaining market share from whey-based formulations, driven by a growing number of North American consumers who perceive plant proteins as healthier alternatives to animal-derived options. Additionally, sustainability considerations are increasingly influencing consumer choices in packaged foods. Mondelez International's planned acquisition in June 2024 of a majority stake in Perfect Snacks—a refrigerated protein bar brand widely available in the United States—underscores the rising investment by major consumer packaged goods companies in chilled, plant-based formats. These formats address the textural limitations often associated with shelf-stable extrusion. However, refrigerated bars, while commanding a higher price premium compared to ambient products, require cold-chain logistics and have shorter shelf lives, restricting their distribution primarily to metropolitan markets with high turnover rates. Emerging brands such as Aloha and Health Warrior are incorporating ingredients like sunflower butter and pumpkin-seed protein into their formulations to eliminate tree-nut allergens while maintaining high protein content per bar. This approach enables access to school foodservice channels, where nut-free requirements are mandatory. According to the Good Food Institute, the United States plant-based food industry has experienced significant growth and evolution over the past decade. In 2024, plant-based foods accounted for 1.1% of total retail food and beverage dollar sales [2]Source: Good Food Institute, “U.S. retail market insights for the plant-based industry,” gfi.org.

Increase in Sports, Fitness, and Outdoor Activity Participation

Participation in endurance sports, CrossFit, and outdoor recreation is driving growth in the energy and nutrition bars market, extending its appeal beyond traditional gym-goers. Nutritional and health-focused bars, as defined by Circana, include protein bars, meal-replacement bars, and performance-nutrition products. These products experienced notable sales growth during the 52 weeks ending April 21, 2024, despite a decline in unit sales. This trend reflects a consumer shift toward premium, higher-protein options. To meet the needs of ultra-endurance athletes and military personnel, brands are introducing bars with calorie densities exceeding 250 calories per serving. For example, David Protein, a direct-to-consumer brand, reported strong sales in its first week by offering bars with 50% more calories from protein compared to competitors and leveraging endorsements from influencers such as Peter Attia and Andrew Huberman. Additionally, the segment's growth is supported by increased outdoor recreation, with retailers like Costco and Sam's Club featuring multi-packs of energy bars in end-cap displays, using bulk-purchase incentives to attract casual hikers and weekend adventurers.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory changes for labeling, health claims, and allergens | -0.4% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Consumer skepticism over processed food health benefits | -0.3% | United States, Canada | Medium term (2-4 years) |

| Challenges in scaling new formulations for mass production | -0.3% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Challenges in scaling new formulations for mass production | -0.2% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Changes for Labeling, Health Claims, and Allergens

The United States Food and Drug Administration (FDA)'s January 2025 proposal for a front-of-pack Nutrition Information box requires labels indicating Low, Medium, or High levels of saturated fat, sodium, and added sugars. Companies must comply within 3 to 4 years, with an estimated industry-wide cost of USD 333 million annually. Products displaying "High" added-sugar labels risk losing placement in health-and-wellness sections at major retailers such as Target, Walmart, and Kroger. This forces brands to undergo reformulation processes, which can reduce profit margins and delay product innovation. In Canada, the front-of-pack nutrition symbol, effective January 2026, requires bilingual packaging and warning symbols for products exceeding thresholds for saturated fat, sodium, or sugars. This adds compliance challenges for brands operating across North America. Similarly, Mexico's NOM-051 labeling regulation mandates black octagon warning labels for products with excessive levels of calories, sugars, saturated fat, trans fat, and sodium. This regulation triggered a wave of reformulations in 2024 as brands aimed to avoid the negative perception associated with multiple warning symbols. These overlapping regulatory requirements increase the complexity of stock-keeping units (SKUs). A single product may require three distinct label designs to meet the regulations in the United States, Canada, and Mexico. This raises packaging costs by 15% to 20% and extends time-to-market by 6 to 9 months. Smaller brands, which often lack dedicated regulatory affairs teams, face significant compliance challenges. As a result, there is growing consolidation pressure, with private-equity-backed platforms acquiring smaller brands to distribute legal and labeling costs across larger portfolios.

Consumer Skepticism Over Processed Food Health Benefits

In the United States, a significant portion of grocery purchases consists of ultra-processed foods (UPFs). Increasing evidence linking UPFs to obesity, type 2 diabetes, and cardiovascular disease is reducing consumer trust in packaged snacks marketed as healthy options. At the same time, only one-third of consumers fully trust organizations such as the Food and Drug Administration (FDA), Centers for Disease Control and Prevention (CDC), and World Health Organization (WHO), while 61% express distrust toward artificial dyes. Additionally, two-thirds of consumers are concerned about the use of seed oils—such as canola, soybean, and sunflower oils—which are widely used in bar formulations due to their affordability and high smoke points but are increasingly associated with inflammation and metabolic dysfunction, as highlighted in social media discussions. This skepticism is further heightened by the United States Department of Agriculture (USDA) Dietary Guidelines Advisory Committee's ongoing review of whether to classify UPFs as a distinct category in the 2025 guidelines. Such a classification could formalize the stigma surrounding UPFs and potentially lead to retailer de-listings of bars perceived as overly processed. This growing distrust underscores the need for bar manufacturers to adopt transparent sourcing practices and secure third-party certifications to rebuild consumer confidence.

Segment Analysis

By Product Type: Energy Bars Outpace Granola on Protein Innovation

Energy and nutrition bars are anticipated to grow at a compound annual growth rate (CAGR) of 7.43% through 2030, significantly outpacing the growth of granola/muesli bars. Granola/muesli bars are expected to account for 44.32% of the total volume in 2024, but their growth lags behind by 125 basis points. The faster growth of energy and nutrition bars can be attributed to advancements in product formulations, which now offer 15 grams of protein per serving while maintaining calorie counts below 200. These features cater to the needs of health-conscious consumers, particularly those focused on weight management and endurance activities, making these bars a preferred choice in the market.

In contrast, granola bars are encountering challenges due to the United States Food and Drug Administration's (FDA) updated definition of "healthy." The revised guidelines discourage the use of added sugars and saturated fats, which are integral to the honey-oat-nut clusters that define this subcategory. This regulatory change has created obstacles for granola bars, as manufacturers must now navigate these stricter standards while maintaining the appeal of their products. As a result, granola bars are facing increased pressure to adapt to evolving consumer preferences and regulatory requirements.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Functional Claim: Organic Bars Gain as Retailers Expand Natural Sets

Organic bars are anticipated to grow at a compound annual growth rate (CAGR) of 7.72% through 2030, surpassing the growth of conventional formulations. Conventional formulations accounted for 77.32% of the total volume in 2024, but organic bars are projected to outpace them by 179 basis points. This growth reflects the efforts of retailers to expand their natural and organic product offerings, driven by the 427 organic bar launches recorded between 2019 and 2023. Retailers such as Whole Foods Market and Sprouts Farmers Market have implemented policies requiring new stock-keeping units (SKUs) in the cereal-bar aisle to meet USDA (United States Department of Agriculture) Organic or Non-GMO (Genetically Modified Organism) Project Verification standards. These requirements effectively regulate access to the 10% share of the food market represented by natural products, a segment that is growing 38 times faster than conventional categories.

In March 2024, General Mills' Cascadian Farm introduced Organic Granola Bars, emphasizing their commitment to USDA Organic certification, non-GMO ingredients, and the exclusion of artificial additives. This strategic positioning allowed the product to secure placement in Kroger's Simple Truth organic set and Albertsons' O Organics planogram. By aligning with consumer demand for transparency and healthier options, Cascadian Farm has strengthened its presence in the rapidly growing organic food market, catering to the increasing preference for natural and sustainable products.

By Price Category: Premium Bars Scale on DTC and Specialty Retail

Premium bars are projected to grow at a compound annual growth rate (CAGR) of 6.82% through 2030, while mass-market offerings are expected to dominate, accounting for 68.32% of the market in 2024. This growth pattern reflects a shift in consumer preferences, as buyers increasingly prioritize products with unique attributes such as single-origin ingredients, upcycled components, and functional benefits. These benefits include adaptogens, which are believed to help the body manage stress, collagen for skin and joint health, and probiotics that support gut health. The willingness of consumers to pay a premium for these features underscores the growing demand for health-focused and sustainably sourced products in the market.

An example of this trend is David Protein, a direct-to-consumer (DTC) brand that achieved remarkable success by generating over USD 1 million in sales during its first week. The brand positioned its bars as offering 50% more calories from protein compared to competing stock-keeping units (SKUs), appealing to health-conscious consumers. David Protein scaled rapidly by employing influencer endorsements and focusing on product-led growth strategies. To further drive customer engagement, the company raised USD 10 million in seed funding and distributed 20,000 free samples to encourage product trials. This approach allowed the brand to bypass traditional retail slotting fees and significantly reduce customer acquisition costs, demonstrating an innovative and efficient path to market expansion.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: E-Commerce Gains as DTC Models Mature

Online retail channels are projected to grow at a compound annual growth rate (CAGR) of 7.02% through 2030, surpassing the growth of supermarkets and hypermarkets, which are expected to account for 39.92% of the total volume in 2024, by 110 basis points. This growth is primarily driven by the strong performance of food e-commerce, which has achieved a CAGR of 29.9%, and the increasing adoption of direct-to-consumer (DTC) subscription models. These models allow brands to reduce customer acquisition costs while offering personalized nutrition bundles tailored to individual preferences. For instance, brands like Aloha, which have achieved significant sales through platforms such as Amazon and their own websites, are now expanding into traditional retail channels. This approach mitigates risks associated with retail expansion and helps preserve the brand's equity and reputation in the market. Grocery e-commerce sales grew at the fastest rate of 26.4% annually over the past year, prior to 2024. Similar to offline grocery, grocery e-commerce is also highly consolidated, with both segments led by Walmart. Walmart's extensive network of outlets enables in-store pickup or quick delivery within reach of most United States consumers [3]Source: Government of Canada, "Distribution channel series – Grocery ecommerce market in the United States," agriculture.canada.ca.

While online channels are growing rapidly, supermarkets and hypermarkets remain the largest distribution channel, supported by impulse-purchase behavior and the cost benefits of multi-pack offerings. Retailers such as Walmart and Target are addressing consumer demand by allocating end-cap displays for protein bars and expanding refrigerated sections to include chilled formats like Perfect Snacks. Perfect Snacks, acquired by Mondelez in June 2024, is now available in over 27,000 retail locations across the United States, highlighting the increasing significance of chilled protein snack options in the market.

Geography Analysis

The United States emerged as the leading segment in North America's cereal bar market, commanding 77.21% of the region's volume in 2024. This dominance is attributed to its well-established retail networks, a mature sports-nutrition ecosystem, and a consumer base that is increasingly open to experimenting with functional product formats. Natural products, which currently represent approximately 10% of the U.S. food market, are growing at a rate 38 times faster than conventional categories. This rapid growth highlights the success of brands that prioritize clean labels, organic certifications, and allergen-free formulations. Additionally, the United States market is undergoing significant changes due to the U.S. Food and Drug Administration's (FDA) updated "healthy" definition, effective February 2025. This update introduces stricter requirements, including food-group equivalents and limits on added sugars, saturated fat, and sodium. Brands that fail to comply with these new standards risk losing placement in health-and-wellness sections at major retailers such as Target, Walmart, and Kroger.

Mexico stands out as the fastest-growing segment in the North American cereal bar market, with a projected compound annual growth rate (CAGR) of 7.63% through 2030. This growth is largely driven by the implementation of NOM-051 front-of-pack labeling regulations. These reforms require manufacturers to either reformulate high-sugar products or accept black octagon warning labels, which are designed to inform and deter health-conscious consumers. As a result, manufacturers are increasingly focusing on creating healthier product alternatives to align with consumer preferences and regulatory requirements. This regulatory shift has positioned Mexico as a key growth market within the region.

The rest of North America, which includes smaller Caribbean and Central American markets, remains in the early stages of development. Despite being nascent, these markets are gaining attention from United States and Canadian manufacturers. Companies are leveraging regional trade agreements and targeting rising disposable incomes in urban centers to expand their presence. While these markets currently represent a smaller share of the overall North American cereal bar market, they offer significant potential for growth as consumer demand for convenient and healthier snack options continues to rise.

Competitive Landscape

The North America cereal bar market demonstrates a moderate level of consolidation, with a limited number of multinational Consumer Packaged Goods (CPG) companies controlling the majority of market volume. Despite this dominance, there remains significant potential for smaller, emerging brands to carve out market share in premium and functional product niches. A notable development in this space is Mars' acquisition of Kellanova for USD 35.9 billion in August 2024. This acquisition has resulted in the creation of a snacking conglomerate that now encompasses well-known brands such as Nature Valley, Kashi, RXBar, KIND, and Clif Bar. These brands collectively cover a wide range of price points, functional benefits, and distribution channels. This strategic consolidation enables Mars to optimize its operations by spreading research and development (R&D) costs across multiple brands, negotiating advantageous slotting fees with retailers, and leveraging cross-brand promotional strategies to safeguard shelf space from private-label competitors.

Another significant move in the market is Mondelez International's acquisition of a majority stake in Perfect Snacks in June 2024. Perfect Snacks is a refrigerated protein-bar brand that is distributed across more than 27,000 retail locations in the United States. This acquisition underscores the growing interest of large CPG companies in refrigerated, plant-based product formats, which typically command a price premium of 30% to 40% compared to ambient stock-keeping units (SKUs). The move reflects a broader industry trend toward innovation in product formats that cater to evolving consumer preferences for healthier and more sustainable options.

Opportunities for growth in the cereal bar market are particularly evident in areas such as refrigerated bars, grain-free formulations, and the incorporation of upcycled ingredients. Emerging disruptors like Three Wishes are capitalizing on these trends by introducing innovative products such as grain-free granola bars, which are now available at Target. These bars are crafted using nuts and seeds, delivering 6 grams of protein and 3 grams of sugar per serving, while avoiding traditional ingredients like wheat, rice, corn, and oats. This formulation is specifically designed to appeal to health-conscious consumers, including those adhering to paleo and Whole30 diets, highlighting the potential for niche products to gain traction in a competitive market.

North America Cereal Bar Industry Leaders

-

General Mills Inc.

-

Kellanova

-

PepsiCo, Inc.

-

Mondelez International, Inc.

-

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Cerealto acquired a majority stake in Fresca Foods, establishing a strong U.S. manufacturing presence. This partnership accelerates Cerealto’s entry into the fast-growing North American snack bar market and expands capabilities in natural and organic snacking segments.

- November 2024: 1440 Foods acquired FITCRUNCH to strengthen its portfolio of protein-rich snack bars, expanding its position in North America's active nutrition segment and enhancing reach across retail channels with complementary product innovation capabilities.

- April 2024: Seven Sundays launched Real Cocoa Sunflower Cereal in US Costco stores, targeting health-conscious consumers. The product features grain-free, upcycled ingredients and plant protein, reflecting innovation and expansion within the North America cereal and snack market.

North America Cereal Bar Market Report Scope

Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

By Product Type

| Granola/Muesli Bars |

| Energy and Nutrition Bars |

| Others |

By Functional Claim

| Organic |

| Conventional |

By Price Category

| Mass |

| Premium |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Granola/Muesli Bars |

| Energy and Nutrition Bars | |

| Others | |

| By Functional Claim | Organic |

| Conventional | |

| By Price Category | Mass |

| Premium | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF