North America Car Wash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.37 Billion |

| Market Size (2026) | USD 17.31 Billion |

| Market Size (2031) | USD 22.87 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

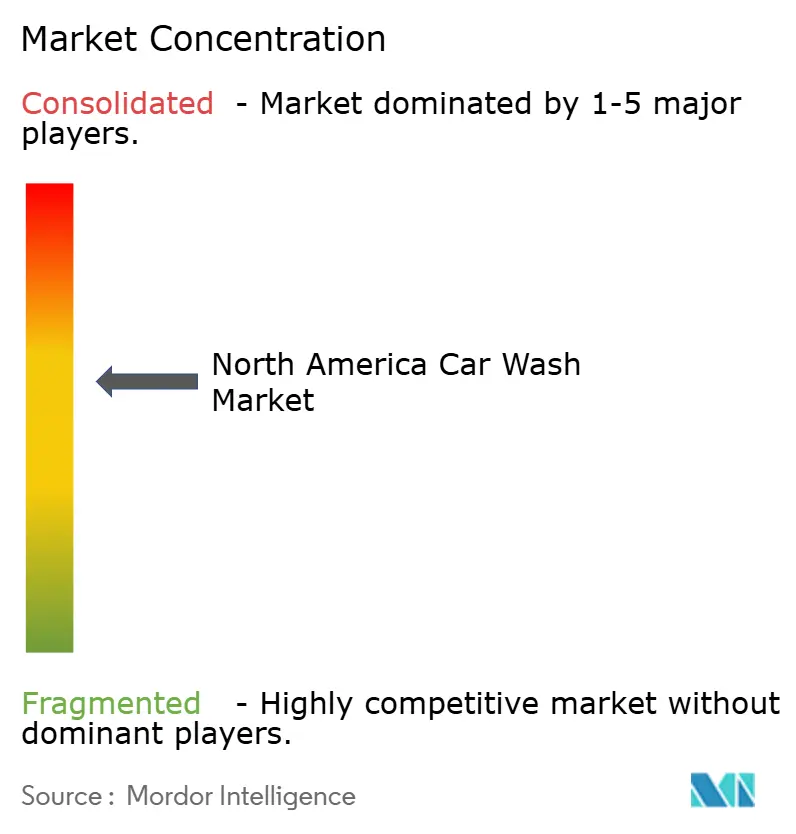

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Car Wash Market Analysis by Mordor Intelligence

The North America Car Wash Market size was valued at USD 16.37 billion in 2025 and estimated to grow from USD 17.31 billion in 2026 to reach USD 22.87 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). Rising vehicle ownership, the shift toward express tunnel formats, and the expansion of subscription programs collectively anchor this sturdy growth trajectory. Private-equity participation is recasting once-fragmented local businesses into scaled, technology-driven chains that capture recurring revenue and purchasing efficiencies. Operators now focus on throughput optimization rather than traditional service layering, which further tilts competitive dynamics in favor of large chains adopting license-plate recognition, advanced customer-relationship-management platforms, and water-recycling systems.

Key Report Takeaways

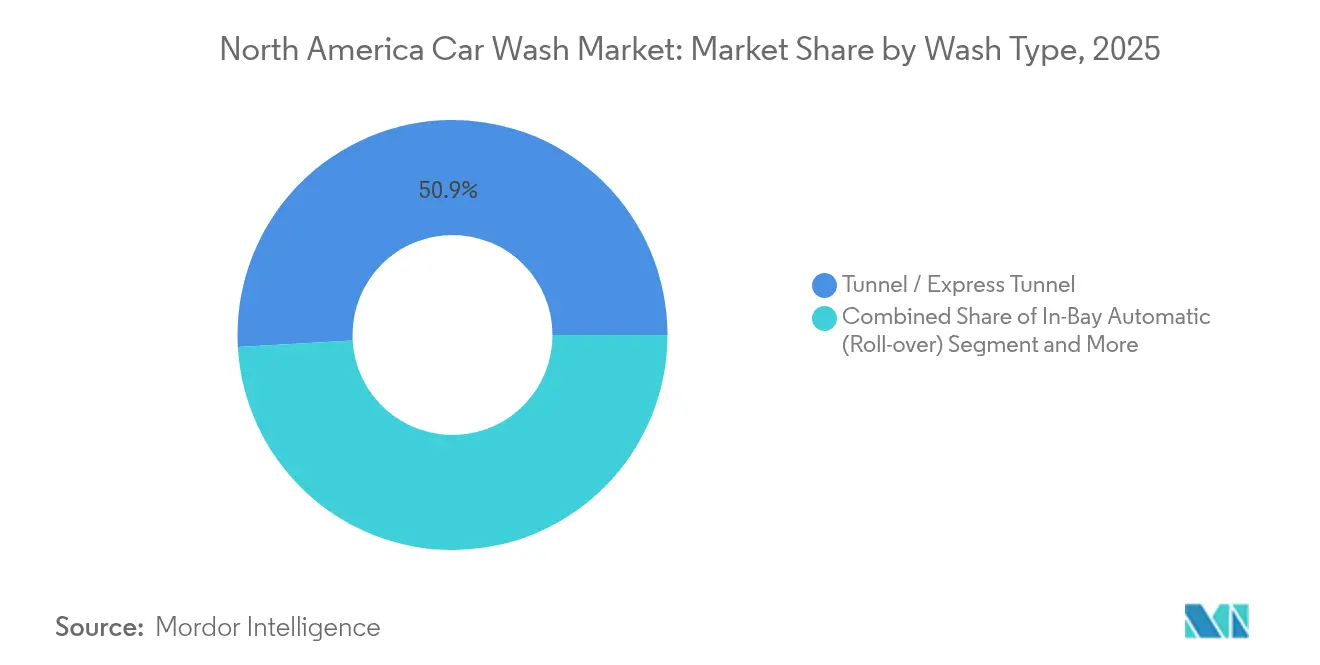

- By wash type, express tunnels led with 50.88% of the North America car wash market share in 2025; the segment is projected to expand at a 6.03% CAGR to 2031.

- By service model, express exterior services commanded 41.96% share of the North America car wash market size in 2025, whereas mobile and on-demand formats are forecast to grow at 6.18% CAGR through 2031.

- By mode of payment, cashless systems held 68.11% share of the North America car wash market size in 2025, while subscription memberships record the fastest 5.79% CAGR to 2031.

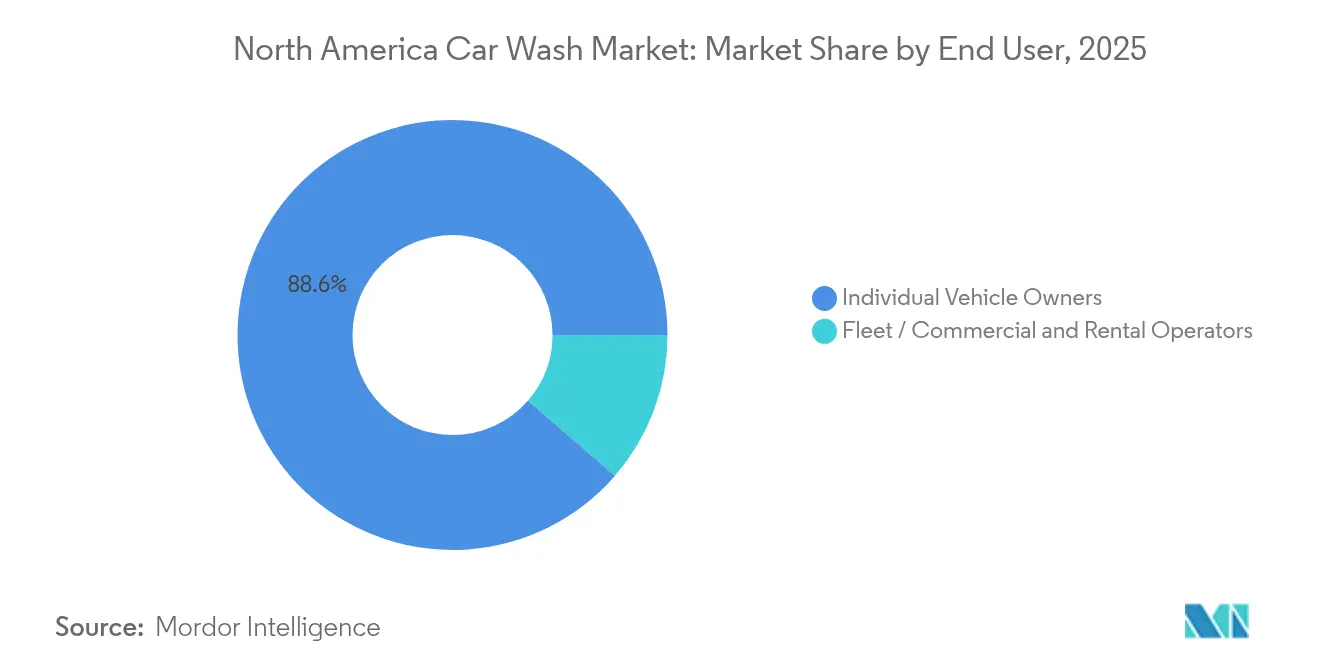

- By end user, individual vehicle owners accounted for 88.64% share of the North America car wash market size in 2025; fleet and commercial customers show the highest 5.65% CAGR through 2031.

- By location, stand-alone sites dominated with 64.93% of the North America car wash market share in 2025, yet convenience-store and shopping-center integrations are advancing at a 5.84% CAGR.

- By country, the United States retained 86.74% of the North America car wash market share in 2025, whereas Mexico is the fastest-growing geography at a 6.01% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North america contributes to a system defined not by any single geography but by the interaction of many. The global car wash market data by Mordor Intelligence represents that combined structure.

North America Car Wash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle ownership and ageing fleet | +1.8% | North America, with strongest impact in Mexico and suburban US markets | Long term (≥ 4 years) |

| Shift toward subscription programs | +1.5% | US and Canada, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Convenience-oriented consumer behaviour | +1.2% | Region, with premium impact in urban North American markets | Short term (≤ 2 years) |

| PE-backed express-tunnel | +0.9% | US primarily, with spillover to Canada | Medium term (2-4 years) |

| Water-recycling tech opens drought-prone metro markets | +0.6% | Western US states, particularly California and Arizona | Long term (≥ 4 years) |

| LPR-driven dynamic throughput and pricing optimisation | +0.4% | Technology-forward operators across North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Ownership and Ageing Fleet

Vehicle-park expansion and ageing fleets underpin consistent wash frequency across the North American car wash market. Mexico records the sharpest growth as near-shoring in automotive manufacturing enlarges middle-class vehicle ownership, while U.S. owners keep older cars on the road amid high new-car prices. Professional washes become more attractive because exterior treatments help preserve resale value in an ageing fleet. Corporate fleet managers increasingly outsource washing to multi-location chains offering tiered volume pricing per vehicle, thereby boosting commercial wash counts.[1]“Corporate Fleet Program,”, Brown Bear Car Wash, brownbear.com This durable demographic trend sustains premium service uptake and drives recurring revenue across metro and suburban corridors.

Shift Toward Subscription (Unlimited-Wash) Programs

Unlimited wash plans recast sporadic transactions into predictable monthly income for operators within the North America car wash market. Mister Car Wash’s Unlimited Wash Club surpassed 2.1 million members by Q4 2024, supplying three-quarters of its wash revenue. Technology vendors such as EverWash deliver mobile enrollment, license-plate recognition check-ins, and frictionless billing, all of which cut churn and improve lifetime value. Rinsed CRM lets chains like LUV Car Wash rescue dormant members through automated down-sell offers, saving more than 3,400 subscriptions and selling 12,000 digital memberships in one year.[2]“Case Study: LUV Car Wash,”, Rinsed, rinsed.com The model’s success hinges on balancing peak-hour traffic with infrastructure capacity so that service speed remains consistent throughout the day.

Convenience-Oriented Consumer Behaviour

Time-pressed consumers choose express tunnels that finish an exterior clean in under five minutes, reinforcing the express-format’s popularity in the North America car wash market. Location strategy evolves toward high-traffic corridors, fuel-station forecourts, and grocery-anchored plazas that capture daily errand patterns. Mobile wash operators respond to on-demand convenience, yet face water-discharge regulations that restrict scaling within dense downtown areas. Contactless payment, predictive queue management, and loyalty apps now set baseline expectations for urban customers.

PE-Backed Express-Tunnel Roll-ups Accelerate Footprint

Private-equity funds fuel rapid multi-state expansion across the North America car wash market. KKR’s USD 850 million backing of Quick Quack Car Wash financed new-build tunnels and unified technology stacks.[3]“Investment in Quick Quack Car Wash,”, KKR, kkr.com Consolidated chains gain purchasing leverage over chemicals and equipment, standardize operating procedures, and spread marketing costs over hundreds of sites. Yet municipal planning boards have begun to freeze permits in saturated regions such as Streetsboro, Ohio, where residents cite traffic and water-use concerns. Even so, distressed sales—ZIPS Car Wash filed for Chapter 11 under USD 654 million in debt in February 2025 —provide scaled buyers with attractive entry multiples for strategic infill.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter municipal water-use and discharge limits | -1.2% | Western US states and drought-prone metropolitan areas | Medium term (2-4 years) |

| High capital outlay for land and tunnel buildouts | -0.8% | Urban markets across North America with premium real estate costs | Long term (≥ 4 years) |

| Tariffs on imported cleaning chemicals inflate OPEX | -0.6% | North America, with particular impact on operators using Chinese suppliers | Short term (≤ 2 years) |

| Zoning moratoriums amid urban market saturation | -0.4% | Saturated metropolitan markets, particularly in Ohio, California, and Texas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Municipal Water-Use & Discharge Limits

California, Arizona, and other drought-prone jurisdictions mandate sophisticated reclamation and discharge protocols that raise construction and operating costs for the North America car wash market. The Environmental Protection Agency’s upcoming 2026 Multi-Sector General Permit introduces PFAS monitoring and stricter storm-water guidelines, requiring capital upgrades for compliant filtration and data reporting. Georgia’s statewide car-wash certification adds yearly inspections, amplifying administrative overhead. Small independents struggle to fund these upgrades, accelerating consolidation into better-capitalised platforms.

High Capital Outlay for Land & Tunnel Buildouts

Prime parcels along commuter arterials fetch premium valuations, pushing total express-tunnel development costs to USD 3–5 million per site across the North America car wash market. Extended permitting timelines, water-infrastructure reviews, and zoning hearings delay revenue commencement. Equipment prices remain elevated alongside steel and electronics input costs, though U.S. bonus-depreciation rules continue to soften net investment outlays for chains able to capitalise on accelerated write-offs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wash Type: Express Tunnels Drive Market Evolution

Express tunnels captured 50.88% of the North America car wash market in 2025, reflecting consumer appetite for quick, automated exterior cleaning. The format is on track for a 6.03% CAGR to 2031, the strongest among wash types. Operators leverage economies of scale in chemical procurement and centralised maintenance while using sensor-based platforms to optimise conveyor speeds.

Equipment suppliers such as Motor City Wash Works integrate IoT modules that push live operational data to cloud dashboards, shrinking downtime and supporting predictive parts replacement. These efficiencies reinforce express tunnel economics, enticing private equity to fund greenfield pipelines across suburban sub-markets. The North America car wash market share held by express tunnels is expected to keep rising as chains retrofit older bays into conveyorised formats.

By Service Model: Express Exterior Dominates, Mobile Gains Traction

Express exterior lanes delivered 41.96% of the North America car wash market in 2025. Low labor ratios and five-minute cycle times generate attractive unit margins. Meanwhile, mobile and on-demand apps represent the fastest 6.18% CAGR, albeit off a smaller base. Full-service interior-exterior packages remain a premium niche but suffer margin compression from wage inflation. Add-on detailing boosts ticket averages but requires departure from the high-throughput blueprint that defines express exterior operations.

Mobile operators tackle water-capture mandates by deploying containment mats and eco-certified soaps. Route-optimisation software lifts daily stops per crew, but the segment’s scalability still trails fixed-site networks. Even so, technology breakthroughs and rising urban parking fees make mobile a credible adjunct revenue line for chains seeking off-site exposure within the broader North America car wash market.

By Mode of Payment: Cashless Systems Enable Subscription Growth

Cashless transactions accounted for 68.11% of the North America car wash market in 2025, mirroring contactless habits ingrained during the pandemic. Digital wallets, near-field communication cards, and license-plate recognition let drivers roll through without stopping at kiosks, trimming queue times. Subscription membership revenue outpaced every other payment class at 5.79% CAGR. Chains track customer behaviour via point-of-sale integrations, enabling segmented promotions that nudge plan upgrades or retain users through downsell offers.

Cash use declines each year as operators trim armored-car pickups and tighten shrinkage controls. Nevertheless, kiosks preserve a small cash slot for legacy users in low-banking-access regions, maintaining universal service coverage across the North America car wash market size.

By End User: Fleet Operators Drive Commercial Growth

Individual drivers dominated 88.64% of 2025 volumes, yet fleet and commercial accounts represent the swiftest 5.65% CAGR through 2031. Rental firms, ride-hail fleets, and last-mile delivery vans need frequent cleans to protect brand image and resale values, fuelling negotiated-rate contracts for high-throughput chains.

Operators offer centralised invoicing, consolidated reporting, and regional service parity that single-site independents cannot match. This structural shift enlarges the commercial slice of the North America car wash market size and diversifies revenue streams beyond retail footfall peaks.

By Location: Convenience Store Integration Accelerates

Stand-alone tunnels preserved 64.93% dominance in 2025, yet convenience-store and shopping-centre co-locations notch a leading 5.84% CAGR. Retail petroleum chains add washes to lift non-fuel gross margin while bundling loyalty points that recycle customers back into the forecourt.

Canadian forecourt penetration illustrates the model’s stickiness and provides a blueprint for U.S. operators seeking white-space at existing fuel parcels. The North America car wash market share derived from co-located formats will expand as real-estate developers bundle fuel, food, and wash amenities on one edge-of-parking-lot pad.

Geography Analysis

The United States remains the anchor of the North America car wash market, accounting for 86.74% of 2025 revenue. Subscription penetration, express-tunnel conversions, and private-equity consolidation fortify operator economics across both Sun Belt and Rust Belt states. Markets such as California deliver majority of annual receipts but impose the strictest environmental regulations, compelling widespread adoption of reclaim systems that cut fresh-water draw by half. Urban saturation worries spur municipal moratoriums in locales like Streetsboro, Ohio, creating barriers to greenfield entrants while stabilising ticket counts for incumbents. Technology, particularly license-plate recognition and dynamic CRM workflows, has become table stakes in every major metro as chains compete on speed, consistency, and digital convenience.

Canada contributes steady growth underpinned by forecourt integration. Approximately 2,268 wash bays operate adjacent to 9,868 gas stations, a ratio now baked into new-build plans by chains such as Couche-Tard/Circle K. Mobile activation embedded in fuel pumps allows motorists to bundle a wash into the fueling session without approaching a pay kiosk, increasing impulse purchases. Loyalty tie-ins via Petro-Canada’s Petro-Points or Circle K’s Easy Rewards add stickiness, keeping throughput robust even in colder months when wash demand typically dips.

Mexico yields the highest growth runway within the North America car wash market, growing at a CAGR of 6.01% through 2031. Near-shoring inflows into Nuevo León and Coahuila have expanded the white-collar middle class, pushing suburban vehicle counts upward. Local chains remain fragmented, but U.S. operators recognise a scalable frontier market situated within trucking proximity to supply hubs. Regulatory navigation, especially water concessions and zoning, requires local partnerships or master franchise models. Nonetheless, the structural demand drivers of urbanisation, rising disposable incomes, and vehicle-ageing trends mirror the earlier U.S. narrative, implying a similar evolutionary arc in the decade ahead.

The car wash market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Middle East, and Asia Pacific.

Competitive Landscape

Moderate concentration characterises the North America car wash market, with the top six multilocation chains controlling a still-expanding slice of total sites. Whistle Express’s USD 385 million acquisition of Take 5 Car Wash propelled the combined chain to 530 sites across 23 states, instantly creating the largest express operator in the United States. ZIPS Car Wash’s Chapter 11 filing under USD 654 million of debt demonstrates the downside of over-leveraged location rolls, yet simultaneously unlocks acquisition channels for capital-rich sponsors that can absorb and rebrand foreclosed tunnels at discounted multiples.

Technology deployment determines day-to-day competitive edge. LUV Car Wash used Rinsed CRM to preserve more memberships and drive online sales, underscoring how data-driven retention tools sustain recurring revenue. Sensors, predictive maintenance, and water-reclaim units also drop operating expense per car by double-digit percentages, freeing cash to fund continued expansion.

White-space remains in suburban corridors devoid of express tunnels and in Mexico’s secondary metros where professional washing is still nascent. Chains sequencing openings favour cluster strategies that enable shared marketing, regional management leverage, and scale buying. However, zoning curbs and community resistance in already dense urban areas limit further build-out, steering capital toward conversion of distressed competitors rather than pure greenfield. Overall, the North America car wash market gravitates toward a hub-and-spoke web of regional strongholds dominated by handfuls of well-funded owner-operators.

North America Car Wash Industry Leaders

Zips Car Wash

International Car Wash Group (ICWG)

Autobell Car Wash

Quick Quack Car Wash

Super Star Car Wash

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tommy’s Express opened four new car-wash locations as part of its continuing expansion strategy, reinforcing growth momentum across competitive regional markets.

- April 2025: Whistle Express completed the USD 385 million acquisition of Take 5 Car Wash, becoming the largest express operator in the United States with more than 530 sites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North American car wash market as revenue earned from professional facilities, whether tunnel, in-bay automatic, self-service, or mobile, that clean and dry passenger and light commercial vehicles by mechanical or manual means. The value model captures ticket sales, prepaid packs, and recurring membership fees recorded at the wash site.

Scope Exclusions: Household driveway washing, dealer courtesy washes, heavy-duty fleet wash bays, and point-of-sale software revenues are kept outside our accounting frame to avoid double counting.

Segmentation Overview

- By Wash Type

- Tunnel / Express Tunnel

- In-Bay Automatic (Roll-over)

- Self-Service / Coin-Op

- By Service Model

- Express Exterior

- Full-Service / Interior-Exterior

- Mobile / On-Demand

- Detailing Add-on Packages

- By Mode of Payment

- Cash

- Cashless

- Subscription Membership (Unlimited Clubs)

- By End User

- Individual Vehicle Owners

- Fleet / Commercial & Rental Operators

- By Location

- Stand-alone Sites

- Gas / Fuel Stations

- Convenience Stores / Shopping Centers

- Others

- By Country

- United States

- Canada

- Mexico

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chain executives, equipment suppliers, chemical formulators, and regional owner-operators across the United States, Canada, and Mexico. These discussions clarified wash counts per site, average ticket uplifts from subscriptions, and regional construction pipelines, which sharpened assumptions harvested from desk work.

Desk Research

We began with publicly available datasets such as the International Carwash Association retail sales tracker, U.S. Census Bureau County Business Patterns on NAICS 811192 outlets, and Bureau of Transportation Statistics vehicle-parc figures, which help size the demand pool. Regulatory insights were gathered from the U.S. Environmental Protection Agency's water-recycling guidelines and Canadian provincial discharge norms. Company filings, investor decks, and major trade magazines added color on pricing shifts and site rollouts. Select paid repositories, including D&B Hoovers for chain financials and Dow Jones Factiva for deal news, offered cross-checks on operator revenue. This list is illustrative; many additional sources fed our desk analysis.

Market-Sizing & Forecasting

A top-down reconstruction converts vehicle stock and average annual wash frequency into a dollar universe, applying region-specific average spend per wash. Results are corroborated through sampled bottom-up roll-ups of leading chains and independent sites, which are then adjusted for the estimated share of cash transactions not reported in company accounts. Key variables feeding the model include vehicle population growth, professional-wash penetration, site density expansion, subscription membership ratio, typical ticket inflation, and macro factors such as disposable income. Forecasts rely on multivariate regression blended with scenario analysis around water-use regulation and consolidation pace, while gaps in bottom-up estimates are bridged with calibrated operator benchmarks.

Data Validation & Update Cycle

Outputs pass variance checks against third-party indicators before a senior reviewer signs off. We refresh every twelve months and trigger interim revisions if material events, large M&A, regulatory shifts, or fuel-station network closures, alter baseline drivers.

Why Mordor's North America Car Wash Baseline Commands Reliability

Published figures often diverge because firms pick contrasting regional mixes, include ancillary software or chemical sales, or carry forward older exchange rates. Mordor Intelligence fixes a clear facility-level boundary, applies live macro and micro inputs, and revisits assumptions yearly, which keeps our totals consistent yet current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.37 Bn (2025) | Mordor Intelligence | - |

| USD 17.20 Bn (2024) | Regional Consultancy A | Includes driveway detailing add-ons and counts Puerto Rico, inflating base year |

| USD 15.00 Bn (2024) | Industry Association B | Omits mobile washes and membership income, creating a conservative bias |

Differences above show how scope stretch or contraction moves the needle, while Mordor's disciplined boundary and timely refresh give decision-makers a dependable, transparent starting point.

Key Questions Answered in the Report

What is the current size of the North America car wash market?

The market is valued at USD 17.31 billion in 2026 and is forecast to reach USD 22.87 billion by 2031.

Which wash type holds the largest share?

Express tunnel formats led with 50.88% share in 2025 and are projected to grow at a 6.03% CAGR.

How fast are subscription programs growing?

Membership-based payment plans are advancing at a 5.79% CAGR, converting episodic demand into recurring revenue.

Which country shows the fastest growth?

Mexico is the fastest-growing geography, expanding at a 6.01% CAGR on rising vehicle ownership and manufacturing investment.

What are the primary restraints to market growth?

Stricter water-use regulations, high land and equipment costs, tariff-driven chemical price increases, and zoning moratoriums in saturated metros collectively dampen industry expansion.

Why are private-equity firms investing heavily in the sector?

Recurring revenue, defensive demand, and the ability to scale technology and purchasing efficiencies make professional car washing attractive to institutional capital.

Page last updated on: