Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

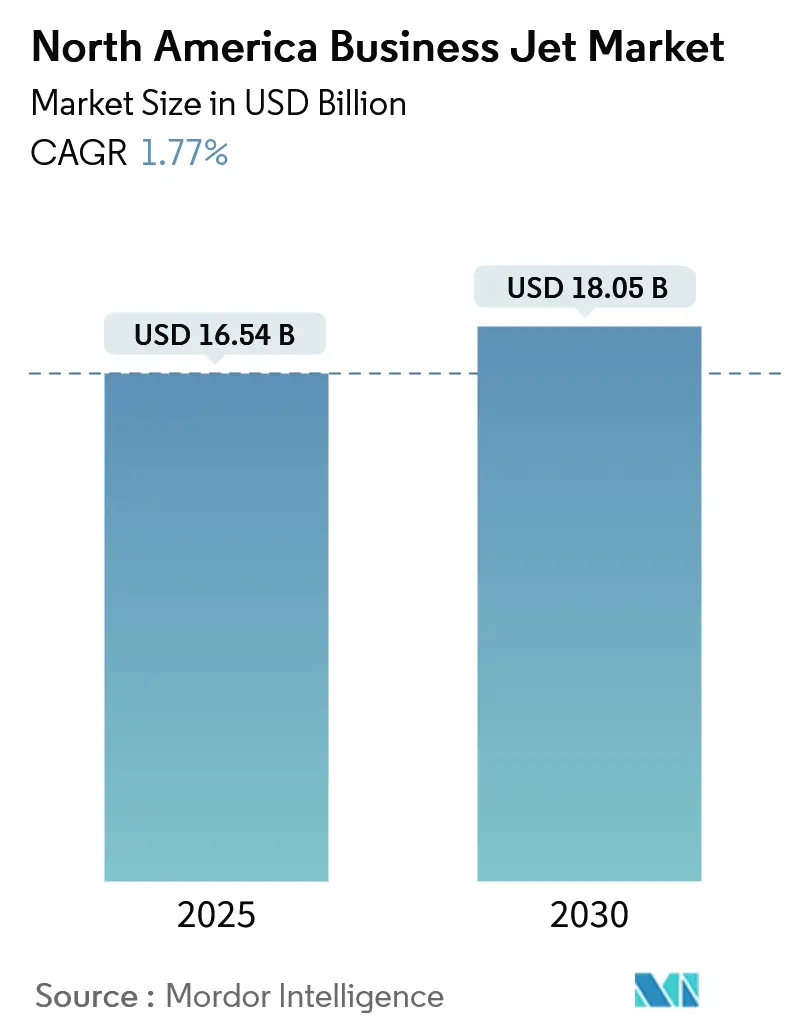

| Market Size (2025) | USD 16.54 Billion |

| Market Size (2030) | USD 18.05 Billion |

| Growth Rate (2025 - 2030) | 1.77% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Business Jet Market Analysis by Mordor Intelligence

The North America business jets market size reached USD 16.54 billion in 2025 and is projected to climb to USD 18.06 billion by 2030, reflecting a 1.77% CAGR over the forecast period. The growth trajectory highlights a maturing ecosystem in which corporate and individual buyers are focusing less on raw fleet expansion and more on productivity gains, cabin connectivity upgrades, and sustainability features. Large-cabin platforms gain momentum because ultra-high-net-worth travelers increasingly view nonstop intercontinental capability as essential infrastructure. Meanwhile, flexible access models fractional shares, jet cards, and app-based charter, capture incremental demand by lowering entry barriers and outsourcing operational complexity. OEMs respond with higher-thrust engines, lower-emission avionics suites, and line-fit satellite communications (Satcom) options. Yet, production flow remains constrained by supply-chain constraints and an acute pilot shortage, which tightens delivery slots. As a result, OEM orderbooks remain full through at least 2028, preserving pricing discipline even as secondary-market values moderate.

Key Report Takeaways

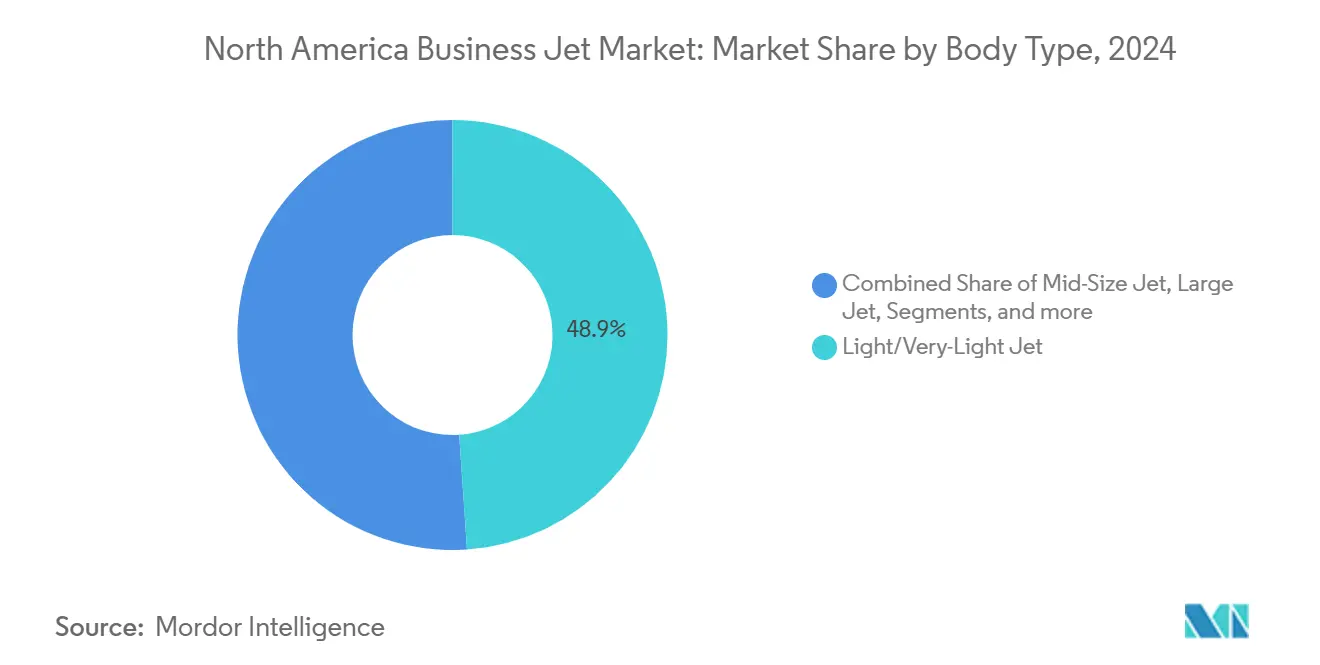

- By body type, light and very-light jets accounted for 58.12% of the North America business jets market share in 2024, while the large-jet class is advancing at a 4.12% CAGR through 2030.

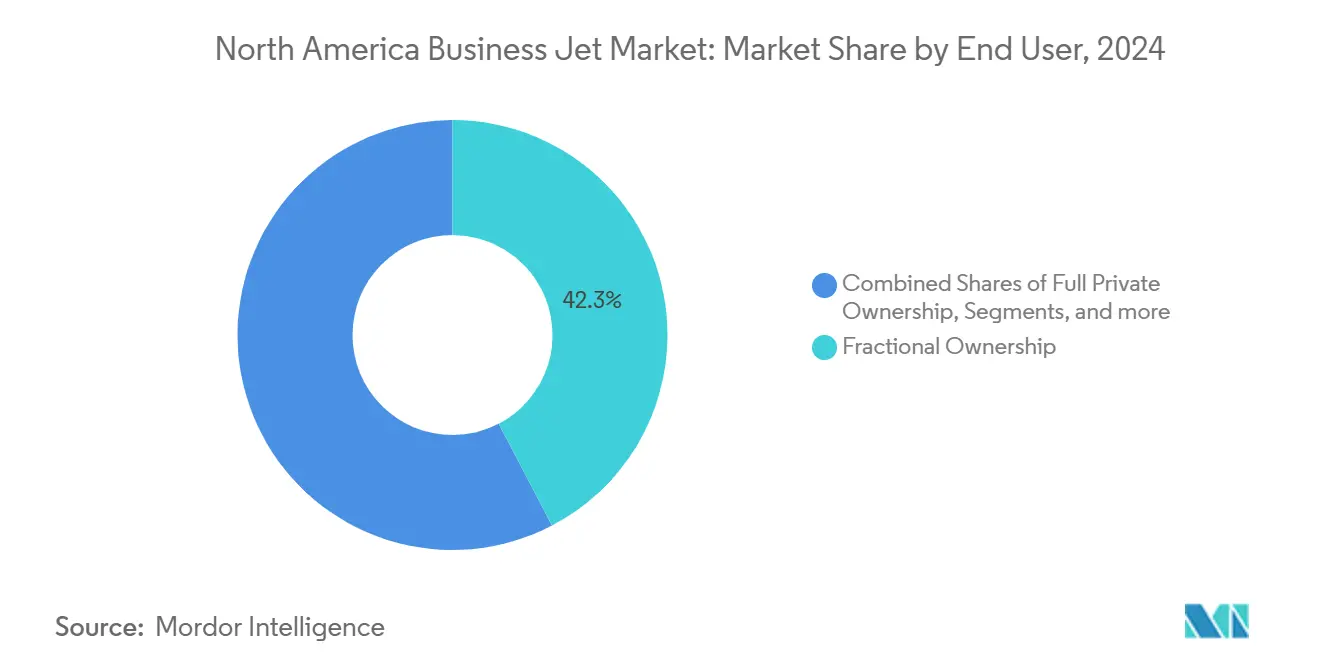

- By end user, fractional ownership is expected to hold a 42.34% revenue share in 2024; charter and air-taxi operators are projected to post the fastest expansion at a 4.92% CAGR through 2030.

- By ownership model, new aircraft purchases accounted for 41.45% of the North American business jet market size in 2024. In contrast, jet cards and membership programs are expected to grow at a rate of 3.56% per year over the same horizon.

- By geography, the United States led the North America business jets market with a 69.22% share in 2024, and Canada is estimated to deliver the highest regional CAGR of 3.44% through 2030.

North America Business Jet Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in high-net-worth population | +0.8% | United States, Canada core markets | Long term (≥ 4 years) |

| Corporate profitability and time-efficiency needs | +0.6% | North America, concentrated in major business hubs | Medium term (2–4 years) |

| Expansion of fractional ownership programs | +0.4% | United States dominance, expanding to Canada | Medium term (2–4 years) |

| OEM backlog-driven upgrade cycle | +0.3% | North America manufacturing and delivery centers | Short term (≤ 2 years) |

| Sustainability-driven fleet renewal | +0.2% | Regulatory focus in US and Canada | Long term (≥ 4 years) |

| Advanced connectivity and cabin digitalization demand | +0.1% | Global, with North America leading adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in High-Net-Worth Population

The swelling ranks of millionaires and billionaires across the United States and Canada elevate private aviation from discretionary luxury to mission-critical mobility. Newly minted wealth holders often bypass turboprops and step directly into midsize or large-cabin jets, a behavior that underpins the 4.12% CAGR logged by the premium segment. [1]Nick Copley, “Current Trends in Business Aircraft Sales,” SherpaReport, sherpareport.com

Geographic wealth concentration amplifies demand out of New York, Los Angeles, Toronto, and Houston, where schedules and security considerations render commercial networks impractical. Structured ownership vehicles, family offices, and LLCs treat aircraft expenses as deductible operating costs, providing a tax-efficient hedge against time loss. The same demographic also fuels the 42.34% stake already held by fractional programs, suggesting a pivot toward professionally managed access over outright title transfer.[2]Nick Copley, “Current Trends in Business Aircraft Sales,” SherpaReport, sherpareport.comProlonged macro-economic resilience points to sustained order flow for cabin classes offering sleeping berths, conference layouts, and nonstop Europe-to-West-Coast range.

Corporate Profitability and Time-Efficiency Needs

For boards and leadership teams, trip-time reductions translate directly to revenue-per-executive-hour metrics. A single-day roadshow that covers Boston, Chicago, and Dallas with no overnight hotel stays and minimal downtime often justifies a charter invoice that appears steep when viewed in isolation. [3]Donna M. Airoldi, “Wheels Up to Acquire New Fleet, Offer Satellite-Based Wi-Fi,” Business Travel News, businesstravelnews.comDistributed workforce models, born in the post-pandemic era, expand flight legs as management shuttles between hub offices and remote employees. Public company filings are increasingly citing mobility productivity as a line item, revealing how private lifts become a strategic enabler rather than a perk. [4]Jeremy Kariuki, “Wheels Up Transitioning Fleet to Phenom 300s, Challenger 300s,” Aviation Week, aviationweek.comThe 4.92% CAGR expected for charter and air-taxi operators confirms that many CFOs now prefer variable-cost access over balance-sheet aircraft assets. This choice preserves liquidity while ensuring service levels comparable to those of owned fleets.

Expansion of Fractional Ownership Programs

Fractional pioneers such as NetJets and Flexjet report record-high block-hour utilization, driven by guaranteed aircraft availability clauses that de-risk mission planning. Program upgrades, including Wi-Fi refreshes and SAF access, push share renewal rates above 90%, which elucidatesand why fractional models captured a 42.34% share of the North America business jets market in 2024. Beyond cost spreading, fractional structures offload regulatory compliance, maintenance oversight, and crew scheduling pain points that intimidate first-time buyers. Recently unveiled 30-hour entry tiers target mid-management travelers whose trip profiles cannot justify full shares but exceed jet-card minimums. Cross-border service expansions into Canadian markets further widen the funnel of potential buyers, clarifying and mitigating the Americanaitigated Americaricaican, reinforcing medium-term CAGR tailwinds for the segment.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and operating costs | -0.4% | North America, particularly affecting mid-market segments | Medium term (2–4 years) |

| Pilot shortage and training bottlenecks | -0.3% | United States and Canada, acute in regional markets | Short term (≤2 years) |

| Stringent emission and noise regulations | -0.2% | United States and Canada, with FAA and Transport Canada oversight | Long term (≥4 years) |

| Cabin interior supply-chain delays | -0.2% | Global supply chains affecting North American deliveries | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

OEM Backlog-Driven Upgrade Cycle

Aggregate OEM backlogs in excess of USD 50 billion keep orderbooks filled through the decade, even as producers expand final-assembly footprints in Dallas, Savannah, and Montreal. Longer lead times incentivize existing owners to initiate trade-ins sooner, as they fear facing multi-year waits if they delay upgrades. In parallel, large-fleet operators scour the pre-owned market, sometimes purchasing entire Phenom 300 or Challenger fleets to secure availability. The scarcity effect enables airframers to sustain pricing power and invest in incremental improvements, from laminar-flow winglets to predictive-maintenance software, without jeopardizing their margin structures. In the short term, this backlog dynamic adds 0.3% to CAGR forecasts; however,rt-term, this backlog dynamic adds 0.3% to CAGR forecasts, though the benefit diminishes after 2027 if supply chains stabilize.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and operating costs | -0.4% | North America, particularly affecting mid-market segments | Medium term (2–4 years) |

| Stringent emission and noise regulations | -0.2% | United States and Canada, with FAA and Transport Canada oversight | Long term (≥4 years) |

| Cabin interior supply-chain delays | -0.2% | Global supply chains affecting North American deliveries | Short term (≤2 years) |

| Pilot shortage and training bottlenecks | -0.3% | United States and Canada, acute in regional markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Operating Costs

Escalating sticker prices, driven by the cost of composite materials and avionics R&D amortization, erode affordability for first-time owners. Even as depreciation schedules remain favorable, capital-budgeting committees are hesitant to approve eight-figure outlays that compete with core business investments. Operating expenses follow a similar upward trend, driven by fuel volatility, rising insurance premiums, and labor shortages in maintenance trades. This cost burden explains why fractional shares and charter hours outpace wholly owned additions; they convert fixed costs into variable ones, aligning expense with utilization. Pre-owned shopping offers relief yet introduces uncertainty about future regulatory compliance and upgrade capital, tempering enthusiasm among cash-flow-sensitive buyers.

Pilot Shortage and Training Bottlenecks

Regional airlines are hiring aggressively, pulling flight-deck talent from business aviation pools and intensifying compensation battles. Recurrent-training centers book out months in advance, and simulator slots fetch premium rates that smaller charter firms cannot absorb. The shortage grounds aircraft that are otherwise airworthy, capping charter-hour growth even when customer demand is present. FAA oversight, heightened following recent runway incursions, adds to the administrative workload that further strains the limited cockpit personnel. Unless accelerated ab-initio pipelines or military-to-civilian bridges gain scale, the sector risks leaving revenue unrealized amid a persistent pilot gap.

Segment Analysis

By Body Type: Large jets drive premium growth

Large-cabin variants opened 2025 with the strongest upward trajectory, reflected in a 4.12% CAGR outlook through 2030. Although light and very-light jets held 58.12% of the North America business jets market share in 2024, the long-range category captures disproportionate value as buyers prioritize nonstop routes linking New York or Toronto to the Middle East and Pacific Rim. The Global 8000’s 8,000 nautical-mile promise and Mach 0.94 cruise speed epitomize how OEMs woo this clientele. Range, cabin volume, and high-speed connectivity dominate purchase criteria, softening price elasticity.

In contrast, midsize platforms offer balanced economics for corporate shuttles that rarely exceed five-hour legs, maintaining steady yet unremarkable demand. Light-jet momentum stems from fractional fleets standardizing around 8-passenger cabins that fit 5,000-foot runway envelopes, thereby allowing access to secondary airports. Very-light types face substitution pressure from high-speed turboprops on sub-500-mile sectors. Ultimately, the North American business jets market rewards airframers that can cascade innovations, such as fly-by-wire and predictive health monitoring, from flagships into smaller classes without cost blow-through.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Charter operators accelerate growth

Charter and air-taxi providers are forecast to expand 4.92% annually, eclipsing the broader North America business jets market’s 1.77% pace. Flexible, pay-as-you-fly economics resonate with corporations that value travel agility but eschew asset ownership. The model also serves high-net-worth individuals whose trip volume falls short of fractional share thresholds. Heavy app adoption, transparent pricing algorithms, and guaranteed recovery clauses collectively boost consumer confidence, converting first-time flyers at a brisk clip.

Fractional ownership, with a mature 42.34% share, continues to capture upsell revenue through larger-share upgrades and fleet-renewal assessments. Full private ownership remains the domain of ultra-wealthy families and governments requiring 99% asset availability. Training organizations and academic institutions hold niche fleets optimized for flight-instruction cycles rather than passenger amenities, contributing marginal volume but essential pilot throughput. Together, these patterns illustrate a spectrum of consumption models that the North American business jet industry must service with tailored maintenance, financing, and digital booking solutions.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ownership Model: Jet cards gain momentum

New-aircraft purchases represented 41.45% of the North America business jets market size in 2024, yet growth moderates as buyers confront long delivery queues. Jet cards and membership programs, expected to grow at a 3.56% CAGR, appeal to travelers who demand fixed-hour pricing, guaranteed aircraft class, and minimal contractual complexity. Operators differentiate by bundling carbon-offset packages, ground-transfer credits, and loyalty reciprocities with luxury hotel brands.

Pre-owned acquisitions spike whenever OEM slot scarcity intensifies, though buyers now scrutinize upgrade-path availability to ensure compliance with 2028–2030 avionics mandates. Fractional shares compete directly with high-tier jet cards, incentivizing providers to experiment with shorter-term lease options that offer membership-like flexibility. The blurring of boundaries prompts financiers to create hybrid products, such as asset-backed revolving credit lines pegged to fractional-share liquidity events, reflecting how capital markets adapt to evolving user preferences across the North American business jet market.

Geography Analysis

The United States accounted for 69.22% of the North American business jets market size in 2024, supported by over 5,000 public-use airports, robust FBO networks, and a corporate culture that values time efficiency. Tax regimes allow accelerated depreciation of Part 91 assets, incentivizing fleet renewals at predictable cadences. OEM service expansion, including a 770,000-square-foot Toronto-adjacent facility for Global models, further entrenches regional dominance by shortening maintenance downtime for the US-registered tails.

Canada, forecasted to grow at a 3.44% CAGR through 2030, benefits from resource-driven prosperity that necessitates rapid, all-weather access to remote mining and energy sites. Transport Canada’s close regulatory alignment with the FAA eases cross-border crew qualification and aircraft certification, thereby encouraging dual bases of operation. The North American business jets market share attributable to Canadian operators should therefore inch upward as newly affluent sectors, such as technology entrepreneurs in Vancouver and private-equity partners in Calgary, join the legacy oil-and-gas clientele.

Mexico is emerging as a manufacturing and MRO hub thanks to a USD 370 million Gulfstream investment that adds 1,500 skilled jobs and embeds supply-chain resilience south of the border. Domestic charter demand remains modest but is climbing steadily as near-shoring drives executive travel between the US headquarters and Mexican production lines. Airframers benefit from maquiladora cost structures, positioning the country as both a cost-effective assembly site and a growing consumption market. Infrastructure upgrades at Toluca and Monterrey airports further strengthen the tri-national network underpinning the broader North America business jets market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Moderate concentration defines the playing field: the top five OEMs account for the majority of cumulative deliveries and hold order books. Gulfstream leads in backlog depth, Bombardier in ultra-long-range innovation, and Textron Aviation in breadth of cabin classes, while up-and-coming entrants explore hybrid-electric demonstrators. Product differentiation centers on SAF compatibility, cabin digitalization, and dispatch reliability metrics, which can reach 99.9% when supported by predictive maintenance analytics.

Service ecosystems increasingly determine buyer loyalty. OEM-branded MROs offer subscription-based support packages that cap direct operating cost variability for owners and fleet managers. Meanwhile, charter aggregators invest in proprietary booking engines that leverage AI to optimize aircraft positioning, thereby cutting empty-leg mileage and carbon footprints. Connectivity providers such as Gogo and Viasat cultivate captive upgrade paths by embedding modular antenna bays during final assembly, ensuring a steady stream of retrofit business throughout the aircraft's life cycle.

Regulatory compliance emerges as a competitive lever. Operators that proactively align with forthcoming FAA Part 5 SMS mandates secure premium insurance quotes and corporate contract wins. Conversely, small charter outfits lacking training infrastructure face rising audit costs and attrition to larger brands. This dynamic supports ongoing consolidation, evidenced by Wheels Up’s fleet acquisition spree and Vista Global’s pan-regional basing strategy. The resultant scale advantages sustain pricing discipline, underpinning stable residual-value curves across the North America business jets market.

North America Business Jet Industry Leaders

-

Textron Inc.

-

General Dynamics Corporation (Gulfstream)

-

Bombardier Inc.

-

Embraer S.A

-

Dassault Aviation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Embraer achieved a significant milestone by surpassing 2,000 business jet deliveries. The milestone aircraft, a Praetor 500, was delivered to a corporate flight department during a ceremony held at Embraer’s state-of-the-art Global Customer Center in Melbourne, Florida.

- June 2025: Bombardier announced a major firm order for 50 of its high-performance Challenger and Global aircraft, accompanied by a groundbreaking service agreement. The combined value of the aircraft and service agreements is USD 1.7 billion, with deliveries scheduled to commence in 2027.

- October 2023: Textron Aviation announced that it entered a purchase agreement with Fly Alliance for up to 20 Cessna Citation business jets, with options for 16 additional aircraft. Fly Alliance is expected to use the aircraft for its luxury private jet charter operations.

North America Business Jet Market Report Scope

Large Jet, Light Jet, Mid-Size Jet are covered as segments by Body Type. Canada, Mexico, United States are covered as segments by Country.

By Body Type

| Large Jet |

| Mid-Size Jet |

| Light/Very-Light Jet |

By End User

| Individual Owners |

| Businesses and Corporate Entities |

| Charter/Air-Taxi Operators |

| Training and Academic Institutions |

| Government and Special-Mission Operators |

By Ownership Model

| New Aircraft Purchase |

| Pre-Owned Purchase |

| Fractional Shares |

| Jet Cards/Membership |

By Geography

| US |

| Canada |

| Mexico |

| By Body Type | Large Jet |

| Mid-Size Jet | |

| Light/Very-Light Jet | |

| By End User | Individual Owners |

| Businesses and Corporate Entities | |

| Charter/Air-Taxi Operators | |

| Training and Academic Institutions | |

| Government and Special-Mission Operators | |

| By Ownership Model | New Aircraft Purchase |

| Pre-Owned Purchase | |

| Fractional Shares | |

| Jet Cards/Membership | |

| By Geography | US |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Market Definition

- Aircraft Type - General Aviation includes aircraft used for corporate aviation, business aviation and other aerial works.

- Sub-Aircraft Type - Business Jets which are private jets and are designed to carry small groups of people and are used for various roles are included in this study.

- Body Type - Light Jets, Mid-Size Jets, and Large Jets according to their ability to carry passengers and flying distance ranges have been included under this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF