Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

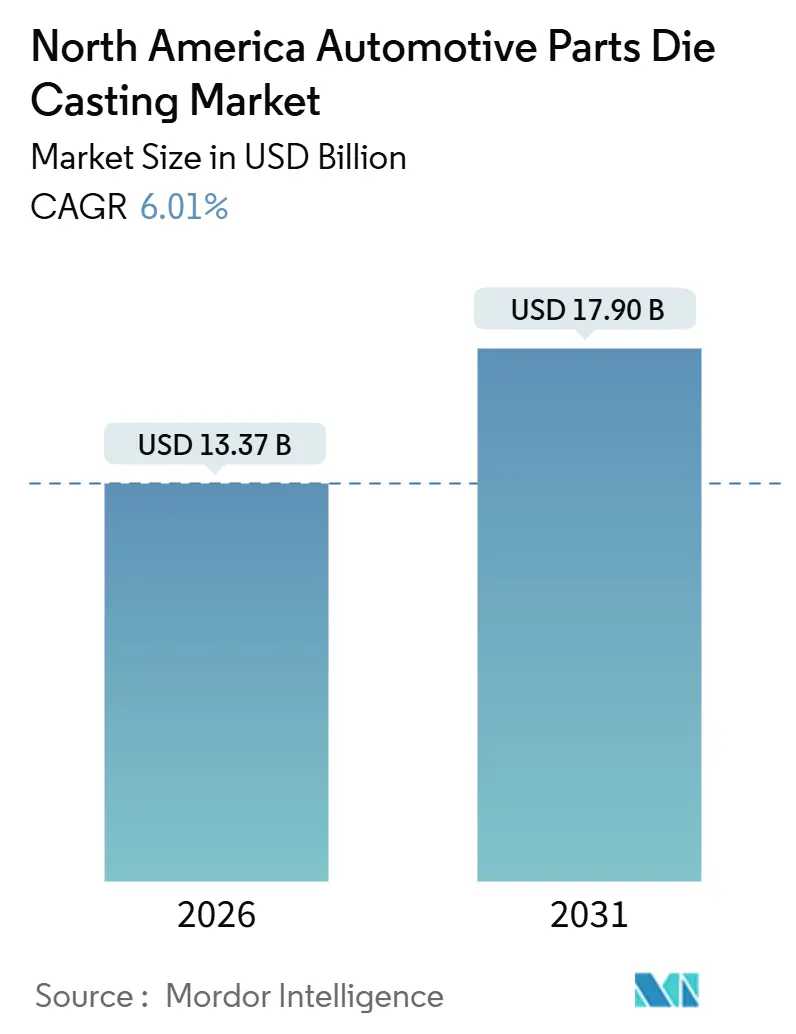

| Market Size (2026) | USD 13.37 Billion |

| Market Size (2031) | USD 17.90 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Parts Die Casting Market Analysis by Mordor Intelligence

The North America automotive parts die casting market size stands at USD 13.37 billion in 2026 and is forecast to reach USD 17.90 billion by 2031, translating into a 6.01% CAGR over 2026-2031. The growth path reflects tightening Corporate Average Fuel Economy (CAFE) targets, rapid electrification, and accelerated alloy substitution that favor aluminum and magnesium die-cast structural components [1]“Corporate Average Fuel Economy Standards 2027-2031,” NHTSA, nhtsa.gov. Foundries are scaling 4,000 to 6,100 ton press lines so that single-piece gigacastings can replace hundreds of welded stampings, cutting assembly time, and removing up to 18 kg from a body-in-white. As the share of electric vehicles (EVs) in light-vehicle sales grows, North America experiences a significant increase in battery-housing demand. While rising capital intensity and tighter emission limits from the Environmental Protection Agency (EPA) push for industry consolidation, numerous member firms of the North American Die Casting Association (NADCA) continue to fiercely compete. These firms focus on automation, porosity control, and near-net-shape machining, all in a bid to secure lucrative long-term contracts with original equipment manufacturers (OEMs).

Key Report Takeaways

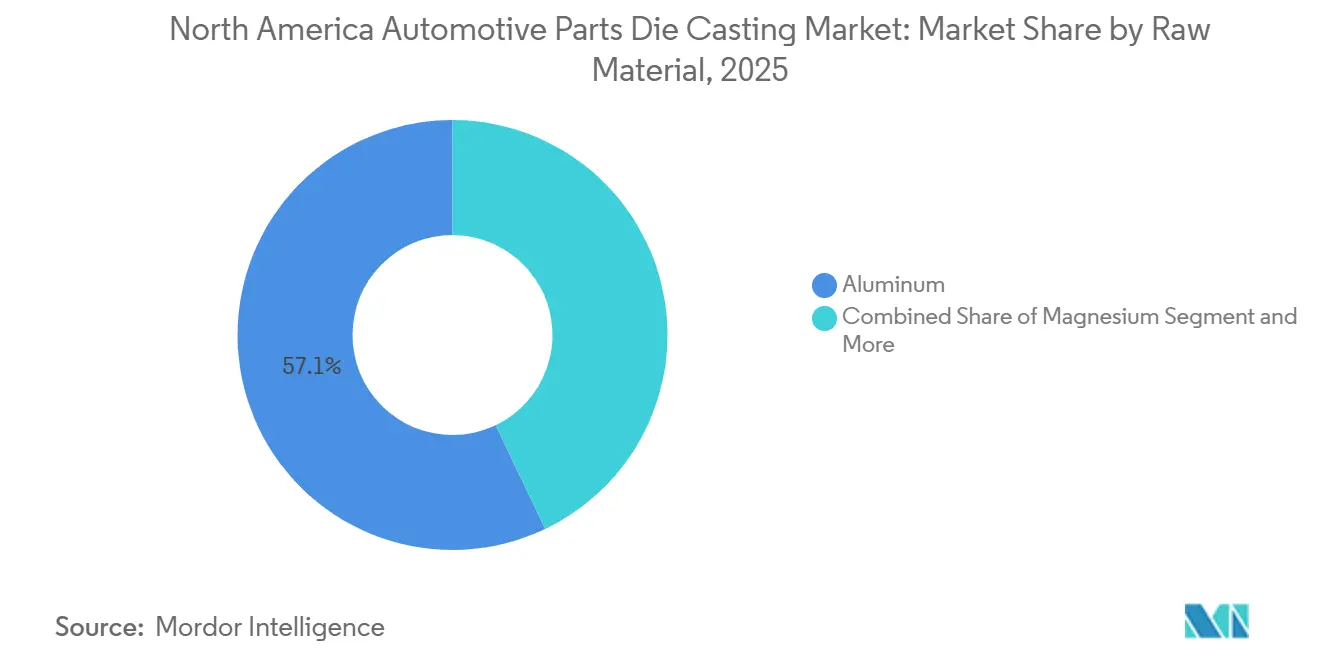

- By raw material, aluminum led with 57.12% of North America's automotive parts die casting market share in 2025, while magnesium is projected to expand at an 8.25% CAGR through 2031.

- By process, pressure die casting held 79.25% of the North America automotive parts die casting market size in 2025; vacuum die casting records the fastest forecast CAGR at 7.86% through 2031.

- By application, body parts commanded 51.33% revenue share in 2025, and electric-vehicle components are advancing at a 9.65% CAGR to 2031.

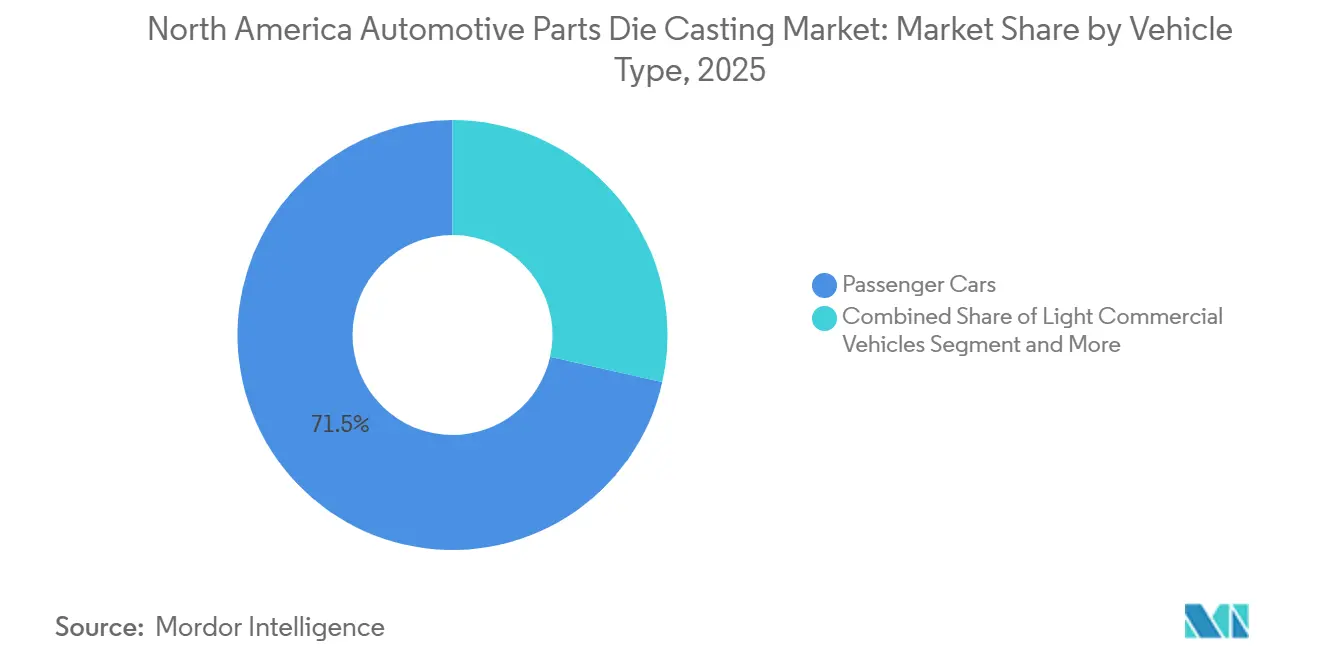

- By vehicle type, passenger cars captured 71.45% share of the North America automotive parts die casting market in 2025, while light commercial vehicles are set to grow at a 9.14% CAGR through 2031.

- By end-use industry, original equipment manufacturers (OEMs) absorbed 83.26% of demand in 2025, and the aftermarket is poised for a 7.21% CAGR on the back of an aging fleet.

- By country, the United States accounted for 74.18% of the North America automotive parts die casting market size in 2025; Canada represents the fastest-growing area with a 6.82% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automotive Parts Die Casting Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV Housing Demand | +1.8% | United States, Canada, Mexico | Short term (≤ 2 years) |

| HPDC Adoption by OEMs | +1.4% | United States, Canada | Medium term (2-4 years) |

| Strict Weight CAFE Rules | +1.2% | United States, Canada | Medium term (2-4 years) |

| USMCA Rule Near-Shoring | +0.9% | Mexico, United States, Canada | Short term (≤ 2 years) |

| Foundry Automation and Retrofits | +0.7% | United States, Canada | Long term (≥ 4 years) |

| High Recycled Feedstock Alloys | +0.5% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding EV Battery-Housing Demand

As electric vehicles (EVs) continue to gain traction in the automotive market, battery trays have become a key driver in the growth of the die-casting segment. Tesla's innovative gigacasting for its rear underbody streamlines production by consolidating numerous parts and eliminating welds, resulting in cost savings and improved manufacturing efficiency. General Motors is advancing its electric vehicle (EV) production capabilities by installing high-capacity presses to support the manufacturing of components for its electric pickups. Meanwhile, Linamar's advanced press technology is contributing to Tesla's production efforts, highlighting Canada's growing prominence as a hub for gigacasting. These one-piece castings not only optimize production processes but also enhance battery safety by significantly reducing water-leak risks for vehicles operating within high-voltage ranges.

HPDC Gigacasting Adoption by NA OEMs

In 2025, General Motors, Ford, and Tesla have secured significant multi-year contracts for structural gigacastings. Ford’s Ontario facility, operational since late 2025, is set to deliver aluminum front and rear subframes for multiple electric vehicle (EV) platforms, streamlining production by significantly reducing the number of components and welds per vehicle. Linamar’s Welland line highlights the substantial investments required in gigacasting technology [2]“Investor Presentation Q3 2025,” Linamar Corporation, linamar.com. Gigacast front modules have transformed body-shop efficiency, drastically reducing production time while also improving crash absorption performance.

Light-Weighting Regulations and CAFE Tightening

Stricter Corporate Average Fuel Economy (CAFE) rules for model years 2027-2031 mandate significantly higher fleet averages, compelling automakers to reduce vehicle weight substantially. By transitioning shock towers, hinge pillars, and seat frames from stamped steel to aluminum high-pressure die castings, automakers achieve notable weight reductions and avoid substantial costs associated with fuel-economy credit purchases. Ford’s F-150 Lightning and Mustang Mach-E benefited from a front subframe conversion, contributing meaningfully to each model’s overall weight-saving goal. The Environmental Protection Agency's (EPA's) greenhouse-gas limits align with Corporate Average Fuel Economy (CAFE), further intensifying compliance challenges[3]“GHG Emissions Standards for Light-Duty Vehicles,” EPA, epa.gov. Tier-1 suppliers highlight that increasing cast-aluminum content improves combined fuel economy, positioning die casting as a highly cost-effective compliance strategy.

OEM Near-Shoring Under USMCA Rules Boosts Regional Die-Casting Volumes

By 2027, the United States-Mexico-Canada Agreement (USMCA) mandates higher regional-value content, pushing automakers to prioritize domestic sourcing for castings. Ryobi's Irapuato expansion introduced additional large-tonnage presses and created new jobs, catering to Ford and GM's electric vehicle (EV) contracts. Pace Industries moved its headquarters to Detroit, significantly reducing prototype lead times. In a strategic move, Martinrea acquired a recycling facility in Mexico, ensuring a substantial portion of North American feedstock for its Saltillo plant, providing a buffer against tariffs. Near-shoring not only reduces logistics costs but also shortens lead times significantly.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum/Magnesium Price Volatility | -0.8% | North America | Short term (≤ 2 years) |

| Capex of 4,000-ton Press | -0.6% | United States, Canada | Long term (≥ 4 years) |

| Mg Supply Chain Risk | -0.5% | North America | Short term (≤ 2 years) |

| EPA and OSHA Emission Limits | -0.4% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aluminum/Magnesium Price Volatility

In 2025, aluminum prices experienced significant fluctuations, leading to margin compression due to delays in cost pass-through. Chinese export restrictions caused a sharp increase in magnesium prices, necessitating expensive alloy redesigns. This shift negatively impacted Linamar's casting margins. While rising aluminum prices can substantially increase the cost of producing a mid-size sedan, only a small proportion of die casters take the precaution of hedging prices.

Capex Intensity of 4,000-ton Press Lines

A high-pressure line represents a significant investment, while larger gigacasters demand considerably higher costs due to their advanced capabilities and scale. The tooling process for gigacasting dies is highly complex and time-intensive, which extends the timeline for achieving a return on investment compared to smaller and more conventional presses. This longer timeline highlights the challenges associated with adopting larger-scale technologies in the industry. Recognizing these challenges, private equity firms are increasingly stepping in to support modernization efforts. These investments aim to enhance the efficiency, productivity, and competitiveness of die casting operations, ensuring they remain viable and aligned with evolving industry demands.

Segment Analysis

By Raw Material: Aluminum Dominance Meets Magnesium Momentum

Aluminum alloys held 57.12% of the North American automotive parts die casting market share in 2025, riding on their balance of strength, thermal conductivity, and corrosion resistance. Magnesium is projected to outpace all materials at an 8.25% CAGR through 2031 thanks to its density advantage, despite a notable cost premium. Zinc claims a significant portion of output for door handles, buckles, and electronics, benefiting from die life that runs 10 times longer than aluminum. At Honda's Anna plant, aluminum boasts a high recycled content. This not only reduces lifecycle CO₂ emissions but also bolsters compliance with United States-Mexico-Canada Agreement (USMCA) sourcing regulations. Meanwhile, at Meridian's Strathroy site, magnesium recycling has made significant progress, marking a stride in overcoming oxidation challenges.

Demand trends are influenced by both thermal and electromagnetic requirements. Aluminum, with its superior conductivity, is essential for battery trays that manage heat effectively. On the other hand, magnesium's properties make it ideal for shielding inverters in advanced systems. Research funded by the Department of Energy (DOE) is pushing towards a future where scrap-fed alloys dominate, aiming for recycled aluminum that matches the properties of primary alloys. These developments not only solidify aluminum's leading position but also carve out a substantial niche for magnesium in ultra-light EV modules.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Process: Pressure Casting Leads, Vacuum Technology Gains

High-pressure die casting accounted for 79.25% of volume in 2025, driven by 60-90 second cycles and thin-wall repeatability for housings and brackets. Vacuum die casting is projected to log a 7.86% CAGR through 2031, fueled by suspension knuckles and control arms that demand porosity below 0.5% for T6 heat treatment. Gravity die casting holds a significant position for low-volume prototype blocks, while squeeze casting is increasingly being used for steering knuckles, replacing heavier iron components.

Choosing a process involves balancing cost, volume, and mechanical objectives. Ryobi’s innovative vacuum-valve system significantly reduces porosity, enabling welded A-pillars with impressive yield strength. Squeeze-cast engine mounts have demonstrated exceptional performance under heavy loads, proving their suitability for heavy-duty trucks. While High-Pressure Die Casting (HPDC) remains the preferred choice for thin-wall parts, both vacuum and squeeze methods are increasingly taking on structural roles, previously dominated by stampings, highlighting a diverse technological evolution in North America's automotive parts die casting landscape.

By Application: Body Parts Lead, EV Components Surge

Body structures commanded 51.33% of 2025 demand, led by shock towers, hinge pillars, and instrument-panel beams that yield significant weight savings over steel and help meet CAFE targets. EV components are set to post a 9.65% CAGR, the fastest among applications, as single-piece battery trays and motor housings will ramp up by 2031. Engine blocks and heads make up a notable share of value, but decline as ICE output will drop by 2031. Transmission housings split: multi-speed ICE cases fade while single-speed EV gearboxes climb.

Tesla's Gigacast rear underbodies streamline production by significantly reducing the number of parts, lowering costs, and improving manufacturing efficiency. Similarly, Ford and GM are transitioning from multiple welded parts to single aluminum castings, optimizing factory operations and enhancing space utilization. While the decline in ICE engines impacts certain components, the adoption of EV technologies, such as larger battery structures and advanced reducer housings, is driving an increase in casting content. These developments are fostering greater application diversification within North America's automotive parts die casting market.

By Vehicle Type: Passenger Cars Dominate, Light Commercials Accelerate

Passenger cars absorbed 71.45% of 2025 tonnage, averaging 85-120 kg of die castings per vehicle. Light commercial vehicles (LCVs) are forecast to log a 9.14% CAGR, topping all vehicle types, as e-commerce fleets electrify and specify 120-180 kg of aluminum castings per van to offset battery mass. Class 6-8 trucks hold a nominal share, mostly engine and transmission housings, but remain ICE-heavy through 2031.

Ford's E-Transit has replaced its previous welded steel battery tray with a lighter single-piece version, enhancing its payload capacity. BrightDrop's electric vans have adopted aluminum die-cast subframes, leading to a significant reduction in body-in-white mass. As the mix of passenger cars increasingly shifts toward SUVs, these vehicles require more cast content. Simultaneously, the electrification of light commercial vehicles (LCVs) is driving new growth opportunities in the North American automotive parts die casting market, independent of passenger car trends.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Use Industry: OEMs Command, Aftermarket Expands

OEMs controlled 83.26% of 2025 shipments, reflecting five- to seven-year contracts for engine blocks, transmission housings, and gigacast body structures. The aftermarket is expected to grow at a 7.21% CAGR, driven by the demand for replacement housings and steering knuckles in aging vehicles. Remanufacturing plays a significant role in the aftermarket, offering rebuilt parts at more affordable prices compared to new ones.

United States-Mexico-Canada Agreement (USMCA) rules encourage dealership channels to source North American castings for replacement parts, shielding domestic foundries from Asian imports. EVs complicate forecasts by removing engine blocks yet adding high-value battery-tray replacements for the housing alone. Thus, even as electrification reduces part counts, aftermarket revenue may evolve rather than vanish.

Geography Analysis

The United States captured 74.18% of regional value in 2025 on the back of several Michigan High-Pressure Die Casting (HPDC) foundries located within 150 miles of Detroit engineering centers. At GM’s Flint Metal Center, large-tonnage presses play a crucial role in producing significant volumes of Ultium trays annually, highlighting strong domestic demand for such projects. Larger plants in the United States, which are better equipped to meet stringent environmental compliance requirements, maintain a competitive edge due to their ability to invest in advanced filtration systems. The limited availability of domestic primary aluminum further emphasizes the importance of utilizing scrap-based alloys to meet production needs. Secondary production clusters in regions like Indiana, Ohio, and Tennessee are strategically positioned to support the operations of Japanese automotive manufacturers in North America.

Canada is projected to grow at a 6.82% CAGR, the fastest geography, buoyed by Linamar’s 6,100-ton Welland line that feeds Tesla Texas and represents a notable share of North American casting capacity. Technological upgrades in Canadian foundries have significantly improved operational efficiency, with government support playing a pivotal role in reducing the costs associated with automation. Quebec’s focus on magnesium production adds a layer of strategic flexibility to the region’s capabilities, although it remains exposed to potential supply chain disruptions from international markets.

Mexico, as a leader in near-shoring initiatives under the United States-Mexico-Canada Agreement (USMCA) framework, continues to benefit from its strategic position in North America. Recent expansions by key manufacturers have enhanced production capacity and created new employment opportunities. Additionally, the cost advantages offered by the Mexican labor market provide a competitive edge, enabling manufacturers to optimize production costs. Many remanufacturers leverage these advantages by routing components to Mexican facilities for processing before returning the finished products to distribution hubs in the United States, creating an efficient and cost-effective supply chain.

Competitive Landscape

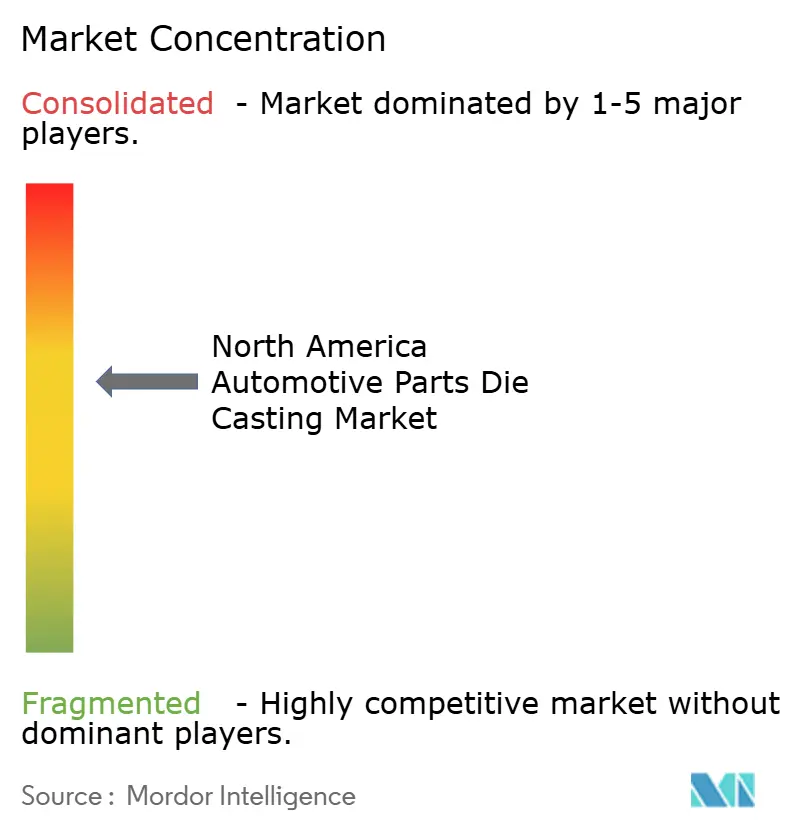

The top five suppliers—Nemak, Linamar, Martinrea, Pace Industries, and Ryobi—held a notable combined share in 2025, indicating moderate concentration within the North American automotive parts die casting market. Linamar’s gigacasting capability and Welland outlay illustrate the capital threshold for Tier-1 scale. Pace Industries moved its headquarters to Detroit in 2021 to shorten prototype loops to eight weeks and align with Ford and GM engineering. White-space openings lie in vacuum die casting for safety-critical structures, where fewer than 15 regional plants can hit porosity below 0.5%.

In the race of technology adoption, some companies sprint ahead while others lag. Ryobi's proactive inline inspection of cast-in inserts has effectively addressed issues related to product quality, ensuring greater reliability and customer satisfaction. Meanwhile, Martinrea has leveraged IoT-driven edge analytics to achieve notable improvements in operational efficiency and equipment performance over time, showcasing the transformative potential of advanced technologies in manufacturing processes.

Private equity firms are increasingly driving consolidation within the industry, with significant investments being directed toward modernizing operations and enhancing production capabilities. Architect Equity, for instance, has focused on revitalizing Gibbs Die Casting, aiming to capitalize on the benefits of advanced manufacturing upgrades. At the same time, rising compliance costs are creating challenges for smaller plants with limited capacities, prompting many to consider exiting the market. This ongoing trend is strengthening the mergers and acquisitions pipeline, enabling well-capitalized groups to expand their presence and secure a competitive edge in the market.

North America Automotive Parts Die Casting Industry Leaders

Nemak, S.A.B. de C.V.

Pace Industries, Inc.

Form Technologies (Dynacast)

Ryobi Die Casting

Linamar Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Linamar Corporation agreed to acquire select Aludyne North American assets for USD 300 million, expanding aluminum chassis and structural casting capacity.

- August 2025: Nemak struck a deal to buy GF Casting Solutions’ automotive arm, broadening its lightweight portfolio and European customer access.

North America Automotive Parts Die Casting Market Report Scope

The scope includes segmentation by raw material (aluminum, magnesium, zinc, and others), process (pressure die casting, gravity die casting, vacuum die casting, and squeeze die casting), application (engine components, transmission components, body parts, electric vehicle (EV) components, and others), vehicle type (passenger, light commercial vehicles, and medium and heavy commercial vehicles), and end-use (original equipment manufacturers (OEMs) and aftermarket). The analysis also covers country-level segmentation, including the United States, Canada, and the Rest of North America. Market size and growth forecasts are presented by value in USD.

By Raw Material

| Aluminum |

| Magnesium |

| Zinc |

| Others |

By Process

| Pressure Die Casting | High-Pressure |

| Low-Pressure | |

| Gravity Die Casting | |

| Vacuum Die Casting | |

| Squeeze Die Casting |

By Application

| Engine Components | Blocks |

| Cylinder Heads | |

| Transmission Components | Housings |

| Gear Cases | |

| Body Parts | Structural Frames |

| Brackets | |

| Electric Vehicle (EV) Components | Battery Housings |

| Motor Casings | |

| Others |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By End-Use Industry

| OEMs |

| Aftermarket |

By Country

| United States |

| Canada |

| Rest of North America |

| By Raw Material | Aluminum | |

| Magnesium | ||

| Zinc | ||

| Others | ||

| By Process | Pressure Die Casting | High-Pressure |

| Low-Pressure | ||

| Gravity Die Casting | ||

| Vacuum Die Casting | ||

| Squeeze Die Casting | ||

| By Application | Engine Components | Blocks |

| Cylinder Heads | ||

| Transmission Components | Housings | |

| Gear Cases | ||

| Body Parts | Structural Frames | |

| Brackets | ||

| Electric Vehicle (EV) Components | Battery Housings | |

| Motor Casings | ||

| Others | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By End-Use Industry | OEMs | |

| Aftermarket | ||

| By Country | United States | |

| Canada | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North American automotive parts die casting market?

The market is valued at USD 13.37 billion in 2026.

Which raw material is gaining share the quickest?

Magnesium castings will register an 8.25% CAGR through 2031, the fastest among all materials.

How will EPA rules affect small die-casting plants?

New MACT and dust-exposure standards add USD 3-5 million in compliance costs, pushing small foundries toward consolidation.

Which geography will be the fastest-growing market?

Canada is projected to grow at 6.82% CAGR through 2031, outpacing the United States and Mexico.