| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.18 Billion |

| Market Size (2030) | USD 3.04 Billion |

| CAGR (2025 - 2030) | 6.84 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

North America Automotive LED Lighting Market Analysis

The North America Automotive LED Lighting Market size is estimated at 2.18 billion USD in 2025, and is expected to reach 3.04 billion USD by 2030, growing at a CAGR of 6.84% during the forecast period (2025-2030).

The North American automotive LED lighting industry is experiencing significant transformation driven by technological advancements and safety regulations. The increasing focus on vehicle safety has become paramount, evidenced by the concerning rise in motor vehicle deaths to approximately 46,000 in 2022, prompting manufacturers to enhance lighting solutions. Advanced lighting technologies, including adaptive driving beam systems and matrix LED headlights, are being rapidly adopted by manufacturers to improve visibility and reduce accident rates. The industry has also witnessed several innovative product launches, such as HELLA's introduction of FlatLight technology for daytime running lights and Nichia Corporation's development of high-definition light engines with more than 16,000 micro-LEDs for headlight applications.

The transition towards electric vehicles has emerged as a crucial factor reshaping the automotive LED lighting landscape. Alternative fuel vehicles, including hybrid and battery electric vehicles, captured 12.3% of all new vehicle sales in 2022, marking a significant 2.7% increase from the previous year. This shift has catalyzed substantial investments in manufacturing capabilities, exemplified by Ford's CAD 1.8 billion investment in its Oakville Assembly Complex in April 2023 to establish a high-volume EV manufacturing hub. The industry is witnessing a surge in technological integration, with manufacturers developing specialized LED lighting solutions optimized for electric vehicles' unique requirements and energy efficiency demands.

The automotive lighting sector is experiencing substantial industrial expansion through strategic investments and partnerships. In February 2023, BMW announced an $800 million investment in its San Luis Potosi plant, with EV production scheduled to commence from 2027. Similarly, Kia and Hyundai's partnership to build EVs in Mexico demonstrates the industry's commitment to regional manufacturing capabilities. These developments are accompanied by technological innovations, such as Oracle Lighting's launch of three new tail light models featuring a "Flush" style design for various vehicle applications in September 2023.

The regulatory landscape continues to shape industry dynamics, particularly through the United States-Mexico-Canada Agreement (USMCA). The agreement's requirement that 75% of vehicle content be produced in North America has significantly influenced manufacturing strategies and supply chain configurations. The automotive parts sector has shown remarkable growth, with Mexican automotive parts production for OEMs and aftermarket reaching a substantial value of USD 94.7 billion in 2021, with projections exceeding USD 101 billion. This growth is complemented by technological advancements in LED lighting, including the development of advanced driver assistance systems (ADAS) integrated lighting solutions and automotive smart lighting technologies that enhance both safety and efficiency.

North America Automotive LED Lighting Market Trends

The LED market is driven by investments by EVs and battery producers to increase automotive production

- The total automobile vehicle production in North America was 14.54 million units in 2022, and it is expected to reach 15.06 million units in 2023. One of the biggest manufacturing sectors in North America is the automotive sector. However, the COVID-19 pandemic caused two significant shocks to the region's automobile industry, which had a significant negative impact on production, sales, and foreign trade in 2020 and 2021. Thus, the disruption in the supply chain and production of automotive vehicles negatively affected the LED lighting business in the region.

- March saw an almost 31% year-over-year fall in the US light car production. Only one plant was operating for one week at the end of April, so there needed to be a higher level of light vehicle production. The auto industry also voiced concerns regarding its supply networks. ZF, a German supplier, has facilities in the United States and revealed plans to reduce its global employment by 10% by the end of May 2020. Several worldwide supply chain disruptions impacted manufacturing in the United States: Mercedes-Benz resumed its Vance, Alabama, facility on April 27; however, due to a scarcity of parts, production had to be briefly halted on May 15. This disruption created a downfall in semiconductors used in the automotive industry.

- Further, the demand for EVs is rapidly increasing in North America due to government initiatives. The Inflation Reduction Act was passed in August 2022, and between that time and March 2023, major EV and battery producers announced investments in North American EV supply chains worth at least USD 52 billion. Such initiatives in the interest of consumers and manufacturers will boost the LED lighting business in the region.

Government investments to drive the sales of electric vehicle and propel the growth of LED lighting

- Most of the EV sales in the North American region come from the US, Canada, and Mexico. In 2022, US BEV sales increased by 65% compared to 2021, and Tesla continues to dominate the EV market. In 2022, Mexico sales were only 0.5% of 1,090,000 total vehicle sales were fully electric, a percentage that falls well below other markets, such as China, Europe, and the United States. In Canada, during Q4 2022, battery electric vehicles (BEVs) alone had 27,754 new registrations, and plug-in hybrid electric vehicles (PHEVs) had 5,645 new registrations.

- To expand further, the US government issued a trillion-dollar infrastructure bill in 2021 that allocates USD 7.5 billion toward building 500,000 more public EV chargers by 2030 and also made investments in EV manufacturing by providing tax benefits of USD 7,500 for purchasing an EV assembled in the US. Also, Tesla, one of the significant players in EVs, committed to delivering around 3,500 of its US Supercharger stations and 4,000 Level 2 charging docks available to all brands of electric vehicles by the end of 2024.

- GM Canada invested more than USD 2 billion in Canada to transform manufacturing facilities in Ingersoll and Oshawa and expects electric vehicle production by the end of 2022. By 2030, Georgia, Kentucky, and Michigan are expected to dominate electric vehicle battery manufacturing in the United States. This EV battery manufacturing capacity will facilitate the production of 10 to 13 million batteries for all-electric vehicles per year, positioning the United States as a global EV competitor. Thus, the above instances lead to the development and production of new power stations because of the growing demand for EVs, which boosts the demand for automotive LEDs in the region.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Government initiatives to expand EV industry will boost the LED market.

- 62% of builders offer incentives to attract investment in commercial spaces further driving the growth.

- Financing options by banks to drive the growth of LED market

- Increasing headlight penetration by major manufacturers to drive the growth of the LED market

- Increasing government initiatives to promote the adoption of LED lights

- Increase in private-owned dwellings and government policy to drive the LED market

- Adoption of smart traffic monitoring systems and increasing government initiatives to drive the growth of LED lights

- Increasing subsidies for using energy-efficient equipment to drive the growth of LED lighting

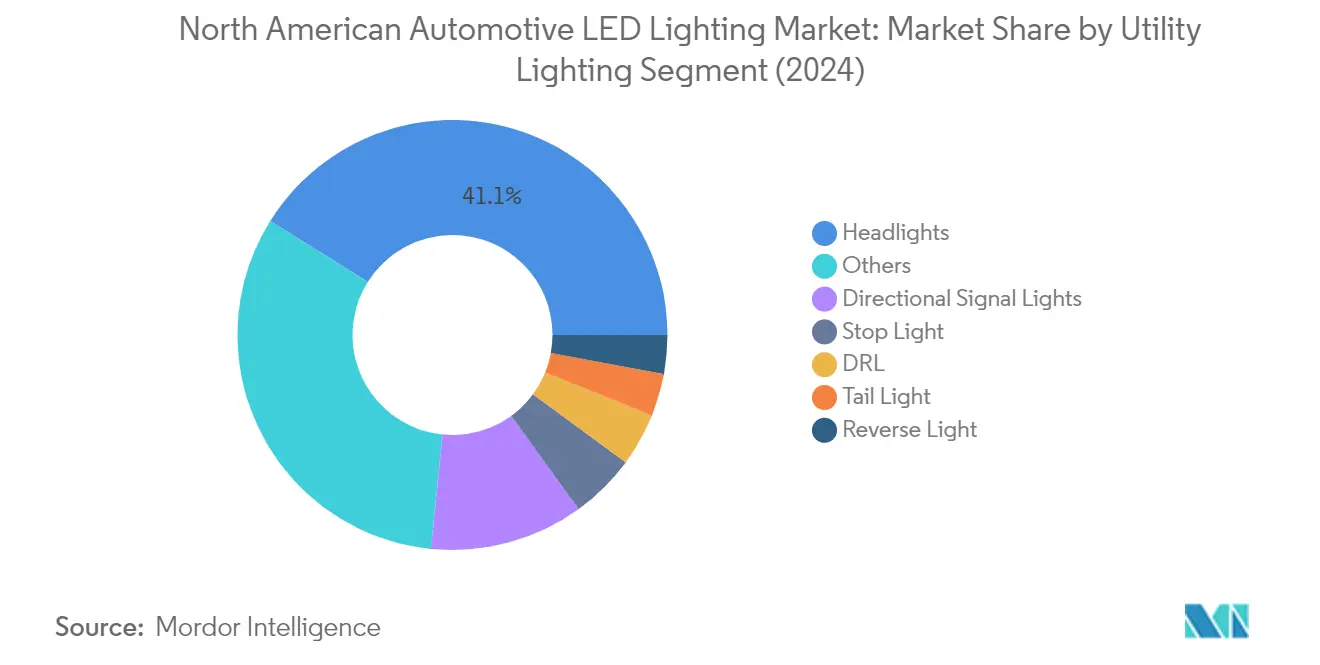

Segment Analysis: Automotive Utility Lighting

Headlights Segment in North American Automotive LED Lighting Market

The automotive headlights segment continues to dominate the North American automotive LED lighting market, commanding approximately 41% market share in 2024. This significant market position is driven by stringent safety regulations requiring LED headlights to comply with FMVSS-108 luminous intensity requirements, ensuring adequate roadway illumination while preventing glare from oncoming vehicles. The segment's growth is further bolstered by the increasing adoption of advanced technologies like Adaptive Driving Beam (ADB) systems and matrix LED headlights in premium and mid-range vehicles. Major automotive manufacturers are increasingly incorporating sophisticated LED headlight technologies, with companies like Toyota achieving around 90% LED penetration in headlights among their top-selling models.

Headlights Segment Growth in North American Automotive LED Lighting Market

The automotive LED headlight segment is experiencing robust growth, driven by technological advancements and increasing demand for enhanced safety features. The segment's expansion is supported by innovations such as high-definition light engines with more than 16,000 micro-LEDs for headlight applications. The growth is further accelerated by the rising adoption of electric vehicles across North America, with manufacturers incorporating advanced LED headlight systems as standard features. The integration of smart lighting technologies, including adaptive driving beam systems and matrix LED solutions, continues to drive innovation in this segment. Additionally, the development of slim-type headlight modules and the implementation of micro-lens array technology are creating new opportunities for market expansion.

Remaining Segments in Automotive Utility Lighting

The automotive utility lighting market encompasses several other crucial segments, including automotive turn signal lights, daytime running lights (DRL), stop lights, reverse lights, and tail lights. Directional signal lights represent a significant portion of the market, essential for vehicle safety and communication. Daytime running lights have gained prominence due to their role in improving vehicle visibility during daylight hours. Stop lights and tail lights continue to evolve with new LED technologies, offering enhanced visibility and safety features. Reverse lights, while representing a smaller segment, remain crucial for safe vehicle operation. These segments collectively contribute to the comprehensive lighting solutions required in modern vehicles, with each serving specific safety and functional purposes.

Segment Analysis: Automotive Vehicle Lighting

Passenger Cars Segment in North American Automotive LED Lighting Market

The passenger cars segment dominates the North American automotive LED lighting market, commanding approximately 89% market share in 2024. This substantial market position is driven by the increasing adoption of advanced LED lighting technologies across new passenger vehicle models. Major automotive manufacturers in the United States, Canada, and Mexico are incorporating sophisticated LED lighting systems as standard features in their passenger vehicles. The segment's growth is further bolstered by stringent safety regulations requiring advanced lighting solutions and the rising consumer demand for energy-efficient and aesthetically appealing lighting options. The rapid expansion of electric vehicle production in North America, supported by government incentives and infrastructure development, is also contributing significantly to the segment's dominance as EVs typically feature advanced LED lighting systems.

Two Wheelers Segment in North American Automotive LED Lighting Market

The two-wheelers segment is emerging as the fastest-growing category in the North American automotive LED lighting market, with a projected growth rate of approximately 7% from 2024 to 2029. This accelerated growth is primarily driven by the increasing adoption of LED lighting solutions in motorcycles and electric two-wheelers for enhanced visibility and safety. The segment is benefiting from the growing popularity of premium motorcycles that come equipped with advanced LED lighting systems. Additionally, the expansion of electric motorcycle manufacturing in North America, coupled with rising consumer interest in high-end two-wheeler models featuring sophisticated lighting solutions, is fueling this growth. The segment is also seeing increased demand for aftermarket LED lighting upgrades as motorcycle owners seek to enhance both the safety and aesthetics of their vehicles.

Remaining Segments in Automotive Vehicle Lighting

The commercial vehicles segment represents a significant portion of the North American automotive LED lighting market, though smaller than the passenger car segment. This segment encompasses a wide range of vehicles, including trucks, buses, and other commercial transportation vehicles. The adoption of LED lighting in commercial vehicles is driven by factors such as enhanced durability, improved visibility for safety, and lower maintenance requirements. Fleet operators are increasingly recognizing the long-term cost benefits of LED lighting solutions, particularly in terms of energy efficiency and reduced replacement frequency. The segment is also benefiting from the growing trend of electrification in commercial vehicles, with new electric trucks and buses incorporating advanced LED lighting systems as standard features.

North America Automotive LED Lighting Market Geography Segment Analysis

North America Automotive LED Lighting Market in the United States

The United States dominates the North American automotive LED lighting market, accounting for approximately 78% of the total market value in 2024. The country's leadership position is supported by its robust automotive manufacturing infrastructure and increasing adoption of electric vehicles. The U.S. automotive industry is experiencing a significant transformation, with major automakers expanding their EV production capabilities. The government's support through initiatives like the Inflation Reduction Act, which provides tax benefits of USD 7,500 for EVs assembled in the United States, has accelerated this transition. The country has also witnessed high adoption rates of advanced lighting technologies, particularly in premium vehicle segments. Ford and GM, which cumulatively account for a significant portion of sales, have been steadily increasing their LED penetration rates in headlights. The growing emphasis on vehicle safety and energy efficiency has led to increased implementation of advanced automotive lighting solutions across various vehicle categories, from passenger cars to commercial vehicles.

North America Automotive LED Lighting Market in Mexico

Mexico has emerged as a crucial hub for automotive LED lighting manufacturing and implementation, with a projected growth rate of approximately 7% from 2024 to 2029. The country's automotive sector has been experiencing remarkable expansion, driven by significant investments from global automotive manufacturers. Mexico's strategic position as the seventh-largest passenger vehicle manufacturer globally, producing approximately 3 million vehicles annually, has attracted substantial foreign investment in automotive lighting production. The country's automotive lighting industry benefits from its strong integration with the North American automotive supply chain and the advantages provided by the United States-Mexico-Canada Agreement (USMCA). Major automotive lighting manufacturers have established production facilities in Mexico, capitalizing on the country's skilled workforce and cost-competitive manufacturing environment. The growing domestic market, coupled with Mexico's position as a major export hub for vehicles and automotive components, continues to drive the demand for LED lighting solutions.

North America Automotive LED Lighting Market in Canada

Canada's automotive LED lighting market is characterized by its strong focus on innovation and sustainability. The country's automotive industry is heavily integrated with the U.S. market, with nearly 80% of cars produced being exported to U.S. roads. Canadian automotive manufacturers have been actively embracing LED lighting technology as part of their commitment to vehicle electrification and energy efficiency. The government's mandatory target for new light-duty cars to have zero emissions by 2035 has accelerated the adoption of advanced lighting technologies. The country's automotive sector benefits from significant research and development activities, particularly in Ontario's automotive cluster. Canadian manufacturers are increasingly focusing on premium vehicle segments, where advanced automotive lighting systems are standard features. The country's strong regulatory framework supporting vehicle safety and environmental protection continues to drive the adoption of LED lighting solutions across various vehicle categories.

North America Automotive LED Lighting Market in Other Countries

The remaining North American territories, including smaller markets in the Caribbean region, play a supporting role in the automotive LED lighting ecosystem. These markets primarily serve as distribution channels for automotive lighting products manufactured in the larger automotive hubs. While their manufacturing capacity might be limited, these regions contribute to the overall market through their aftermarket and replacement segments. The adoption of LED lighting in these markets is primarily driven by the import of vehicles from major manufacturing hubs like the U.S., Mexico, and Canada. The implementation of regional trade agreements and automotive standards influences the type and quality of LED lighting solutions in these markets. These territories often follow the technological trends and regulatory requirements set by the larger markets in the region, particularly in terms of safety standards and energy efficiency requirements.

North America Automotive LED Lighting Industry Overview

Top Companies in North America Automotive LED Lighting Market

The North American automotive LED lighting market is characterized by intense competition among major players who are actively pursuing innovation and expansion strategies. Companies are focusing on developing advanced technologies like chip-based headlamp matrix systems, micro-LED light engines, and adaptive driving beam applications to maintain their competitive edge. Strategic moves in the region primarily revolve around expanding production facilities, particularly near automotive manufacturing hubs, to strengthen supply chain capabilities and better serve key customers. Product development initiatives are largely centered on energy-efficient solutions, smart lighting systems, and integration with advanced driver assistance systems. Operational agility is demonstrated through investments in R&D centers, joint ventures with technology partners, and the establishment of innovation hubs across major markets like the United States, Mexico, and Canada.

Global Leaders Dominate Regional Market Dynamics

The competitive landscape is dominated by established global conglomerates with diverse automotive lighting portfolios, though specialized lighting manufacturers maintain significant market presence through technological expertise and focused innovation. Market consolidation is relatively high, with the top players controlling a substantial portion of the market share through their extensive distribution networks and long-standing relationships with automotive manufacturers. These companies leverage their global research capabilities and manufacturing footprint to serve the North American market while maintaining a strong local presence through strategic manufacturing facilities and technical centers.

The market exhibits a balanced mix of European, Asian, and North American players, each bringing unique strengths in terms of technology, manufacturing capabilities, and customer relationships. Merger and acquisition activities are primarily focused on acquiring technological capabilities, particularly in areas like smart automotive lighting solutions and electric vehicle-specific applications. Companies are increasingly forming strategic partnerships and joint ventures to combine complementary strengths and accelerate innovation in advanced lighting technologies.

Innovation and Integration Drive Future Success

Success in this market increasingly depends on companies' ability to integrate lighting solutions with broader automotive trends, particularly electrification and autonomous driving technologies. Market leaders are strengthening their positions by investing in next-generation lighting technologies, expanding their manufacturing footprint in strategic locations, and developing comprehensive product portfolios that address various vehicle segments. Companies are also focusing on building stronger relationships with electric vehicle manufacturers, as this segment presents significant growth opportunities.

For contenders looking to gain market share, specialization in niche applications and development of innovative, cost-effective solutions present viable strategies. The ability to offer customized solutions while maintaining cost competitiveness is becoming increasingly important as automotive manufacturers seek differentiation through lighting design. Regulatory requirements regarding vehicle safety and energy efficiency continue to shape product development strategies, while the growing trend toward vehicle customization creates opportunities for specialized lighting solutions. Success also depends on building robust supply chain networks and establishing strong relationships with tier-1 LED automotive suppliers.

North America Automotive LED Lighting Market Leaders

-

GRUPO ANTOLIN IRAUSA, S.A.

-

KOITO MANUFACTURING CO., LTD.

-

Marelli Holdings Co., Ltd.

-

OSRAM GmbH.

-

Stanley Electric Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

North America Automotive LED Lighting Market News

- March 2023: HELLA expanded Black Magic auxiliary headlamp series with 32 new lightbars. Range expansion includes 14 lightbars with ECE approval for on-road use and 18 light-bars for off-road applications

- January 2023: HELLA introduced FlatLight technology into series production as a daytime running light for the first time. The lighting concept is successfully transferred from the rear combination lamp to an application in the front area; series production starts in 2025.

- January 2023: Nichia Corporation and Infineon Technologies AG announced the joint development of a high-definition (HD) light engine with more than 16,000 micro-LEDs for headlight applications.

North America Automotive LED Lighting Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

-

4.11 Regulatory Framework

- 4.11.1 United States

- 4.12 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

-

5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

-

5.3 Country

- 5.3.1 United States

- 5.3.2 Rest of North America

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 ZKW Group

7. KEY STRATEGIC QUESTIONS FOR LED CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

North America Automotive LED Lighting Industry Segmentation

Daytime Running Lights (DRL), Directional Signal Lights, Headlights, Reverse Light, Stop Light, Tail Light, Others are covered as segments by Automotive Utility Lighting. 2 Wheelers, Commercial Vehicles, Passenger Cars are covered as segments by Automotive Vehicle Lighting. United States are covered as segments by Country.| Automotive Utility Lighting | Daytime Running Lights (DRL) |

| Directional Signal Lights | |

| Headlights | |

| Reverse Light | |

| Stop Light | |

| Tail Light | |

| Others | |

| Automotive Vehicle Lighting | 2 Wheelers |

| Commercial Vehicles | |

| Passenger Cars | |

| Country | United States |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

North America Automotive LED Lighting Market Research FAQs

How big is the North America Automotive LED Lighting Market?

The North America Automotive LED Lighting Market size is expected to reach USD 2.18 billion in 2025 and grow at a CAGR of 6.84% to reach USD 3.04 billion by 2030.

What is the current North America Automotive LED Lighting Market size?

In 2025, the North America Automotive LED Lighting Market size is expected to reach USD 2.18 billion.

Who are the key players in North America Automotive LED Lighting Market?

GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. are the major companies operating in the North America Automotive LED Lighting Market.

Which segment has the biggest share in the North America Automotive LED Lighting Market?

In the North America Automotive LED Lighting Market, the Headlights segment accounts for the largest share by automotive utility lighting.

Which country has the biggest share in the North America Automotive LED Lighting Market?

In 2025, United States accounts for the largest share by country in the North America Automotive LED Lighting Market.

What years does this North America Automotive LED Lighting Market cover, and what was the market size in 2025?

In 2025, the North America Automotive LED Lighting Market size was estimated at 2.18 billion. The report covers the North America Automotive LED Lighting Market historical market size for years: 2017, 2018, 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Automotive LED Lighting Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

North America Automotive LED Lighting Market Research

Mordor Intelligence offers a comprehensive analysis of the North America automotive LED lighting industry. We leverage decades of consulting expertise in the automotive sector. Our extensive research covers the complete spectrum of automotive lighting systems. This includes automotive interior LED lighting, automotive exterior LED lighting, and automotive LED headlights. The report provides detailed insights into various segments, such as automotive fog lights, automotive light bars, and vehicle mounted spotlights. It places particular emphasis on emerging technologies in automotive smart lighting solutions.

Stakeholders gain valuable insights through our detailed analysis of automotive LED suppliers and regional developments in automotive lighting North America. The report, available as an easy-to-download PDF, examines crucial segments including automotive ambient lighting, automotive LED lamps, and commercial vehicle LED lighting applications. Our research particularly benefits manufacturers, suppliers, and investors by providing detailed analysis of automotive interior LED lighting trends, automotive LED headlight innovations, and developments in vehicle LED lighting technologies. The comprehensive coverage extends to specialized segments such as motorcycle lighting and automotive turn signal lights. This ensures stakeholders have access to the most relevant market intelligence.