Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

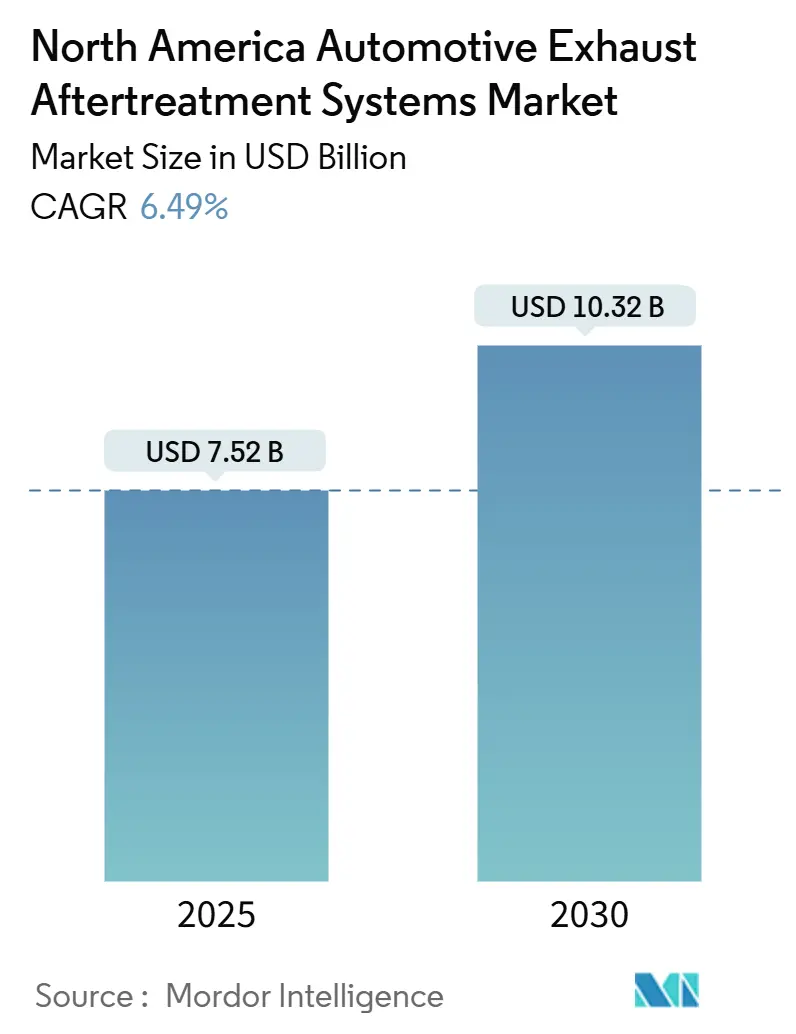

| Market Size (2025) | USD 7.52 Billion |

| Market Size (2030) | USD 10.32 Billion |

| Growth Rate (2025 - 2030) | 6.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Automotive Exhaust Aftertreatment Systems Market Analysis by Mordor Intelligence

The North America automotive exhaust aftertreatment systems market size stands at USD 7.52 billion in 2025 and is projected to reach USD 10.30 billion by 2030, translating into a 6.49% CAGR across the forecast window. Tightening EPA and CARB emission norms, the upcoming Phase-3 GHG limits for MY 2027+ heavy trucks, and rapid gasoline particulate filter (GPF) penetration in gasoline direct-injection (GDI) vehicles form the market’s regulatory backbone. Original-equipment manufacturers (OEMs) are investing in integrated single-can modules that combine selective catalytic reduction (SCR), diesel particulate filter (DPF), and diesel oxidation catalyst (DOC) functionality to control cost, simplify packaging, and accelerate multi-platform certification. Retrofit demand is rising as fleet operators exploit Averaging, Banking, and Trading provisions to monetize CO₂ credits, while suppliers explore nitrogen-free SCR reductants to curb ammonia slip and comply with urban air-quality mandates. Nearshoring into Mexico and the United States is re-shaping supply chains for ceramic substrates and precious-metal coated catalyst bricks, helping mitigate geopolitical risk and improve traceability.

Key Report Takeaways

- By product type, SCR systems held a 39.14% share of the North America automotive exhaust aftertreatment systems market in 2024, whereas DPF is forecast to advance at a 7.41% CAGR through 2030.

- By fuel type, diesel units accounted for 67.49% of the North America automotive exhaust aftertreatment systems market size in 2024, while gasoline aftertreatment is poised for 7.11% CAGR growth to 2030.

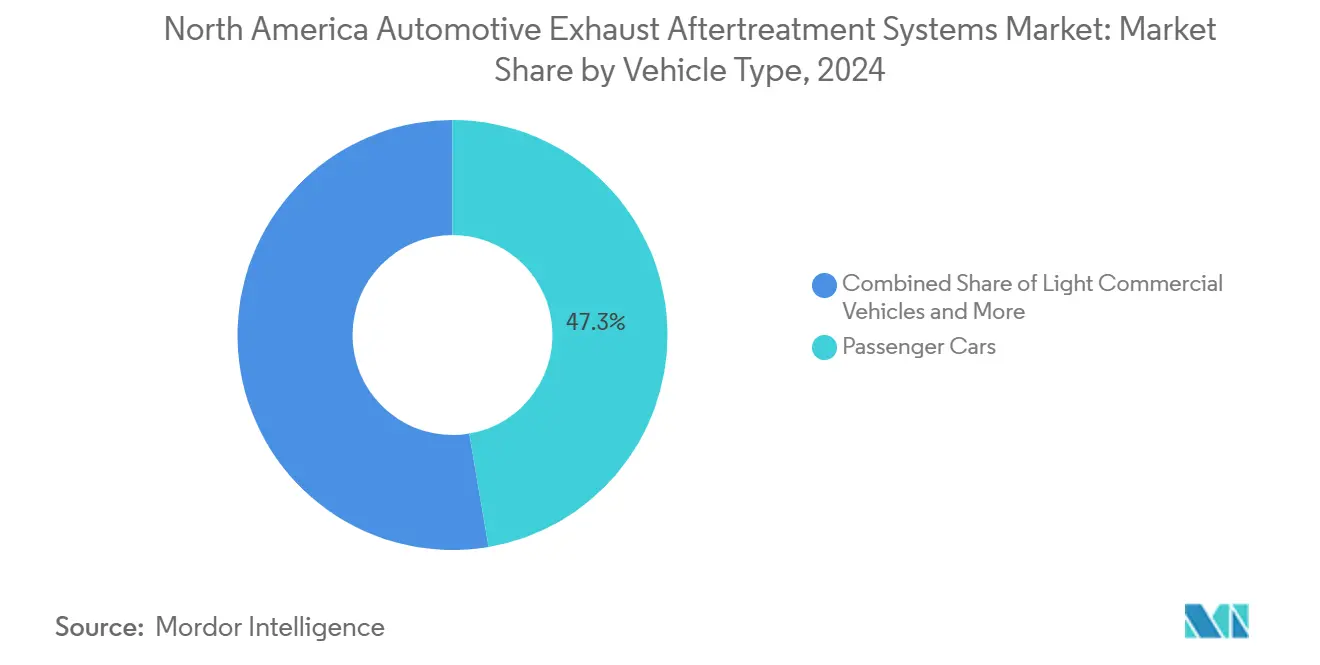

- By vehicle type, passenger cars commanded 47.32% of the North America automotive exhaust aftertreatment systems market share in 2024, but the light commercial vehicle (LCV) category is set to expand at a 7.34% CAGR during the same period.

- By end use, OEM installations represented 72.21% of the 2024 revenue base, whereas the aftermarket is projected to climb at a 6.98% CAGR on the back of mandatory retrofit cycles.

- By country, the United States captured a dominant 79.19% share of 2024 demand, while Canada is on track for the fastest 7.53% CAGR through 2030.

North America Automotive Exhaust Aftertreatment Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EPA and CARB Tier-III / HD Phase-2 Limits | +2.0% | United States, Canada | Short term (≤ 2 years) |

| Upcoming U.S. Phase-3 GHG Rule (MY 2027+) | +1.1% | United States | Medium term (2-4 years) |

| OEM Shift to Integrated After-Treatment Modules | +0.7% | North America | Medium term (2-4 years) |

| Accelerated Adoption of Gasoline Particulate Filters in GDI Cars | +0.6% | United States, Canada | Short term (≤ 2 years) |

| Fleet-Level CO₂ Credit Trading Driving Retrofits | +0.3% | United States | Medium term (2-4 years) |

| Emerging Nitrogen-Free SCR Reductants | +0.2% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EPA and CARB Tier-III / HD Phase-2 Emission Limits

The Federal Tier-III and California Air Resources Board (CARB) Omnibus rules have lowered the legal thresholds for NOx and particulate matter (PM), requiring every light- and heavy-duty platform to adopt SCR, DPF, and GPF hardware. Dual certification between federal and California programs has compressed launch schedules, prompting early adoption spikes for high-efficiency catalyst bricks. Suppliers are localizing wash-coat and substrate production to meet traceability requirements that accompany Greenhouse Gas (GHG) and Low-NOx certification. The regulatory clock is especially aggressive for heavy commercial engines because warranty and useful-life obligations now span longer mileage thresholds. Compliance activity also drives fleet-level telematics integration as operators track real-world emissions against lab-based certification benchmarks [1]“Omnibus Low-NOx Regulation,”, California Air Resources Board, arb.ca.gov.

Upcoming U.S. Phase-3 GHG Rule for MY 2027+ Heavy Trucks

Phase 3 GHG standards tighten CO₂ targets by roughly 18 g/ton-mile for Class 8 tractors, compelling the adoption of higher activity SCR catalysts, electrically heated DPF regeneration, and advanced thermal management strategies [2]“Heavy-Duty Phase 3 Greenhouse Gas Standards,”, Environmental Protection Agency, epa.gov. Averaging, Banking, and Trading provisions create a compliance market in which retrofitted legacy trucks can generate surplus credits. As a result, fleets weigh the cost of next-generation aftertreatment against the potential upside from credit monetization. OEM powertrain roadmaps now juggle near-term diesel optimization with longer-term zero-emission offerings. Component suppliers anticipate a surge in demand for thermal barrier coatings, compact urea tanks, and electrically driven dosing pumps for MY 2027 platforms.

OEM Shift Toward Integrated After-Treatment Modules

Vehicle-makers are replacing stacked, pipe-and-clamp assemblies with single-can modules that combine SCR, DPF, and DOC substrates. The redesign reduces under-floor volume, lowers system weight, and simplifies heat-management modeling, enabling OEMs to stay below platform mass targets even as battery-electric variants proliferate. Integration also boosts procurement leverage for tier-1 suppliers that co-design mounting brackets, sensors, and dosing control hardware with OEM engineering teams. Award decisions are increasingly based on the supplier’s simulation toolchain and additive manufacturing capability for rapid prototyping. As modular designs proliferate across passenger cars, LCVs, and vocational trucks, winning suppliers lock in multiyear volume commitments that stabilize unit cost trajectories.

Accelerated Adoption of Gasoline Particulate Filters in GDI Cars

Tight PM caps and emerging ultrafine particle oversight are accelerating the fitment of GPFs on mainstream sedans, crossovers, and pickup trucks that use high-pressure fuel injection. Recent field data show negligible back-pressure penalties after 100,000 miles, clearing a key durability hurdle. Platinum-group metal (PGM) demand is tilting toward palladium-rich washcoats due to cost advantages, yet new aluminum-oxide nanostructures are partially offsetting that dependency. OEM marketing teams spotlight particulate filters as “invisible” environmental upgrades, supporting showroom narratives around cleaner combustion. Suppliers report volume scale-up at Tennessee and Ontario manufacturing lines to keep pace with North American scheduling pull-ins.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Diesel LCV/PV Share (United States) | -1.2% | United States | Medium term (2-4 years) |

| High PGM Price Volatility | -0.8% | Global | Short term (≤ 2 years) |

| OEM Push for BEVs (Class 2b and Below) | -0.7% | United States, Canada | Long term (≥ 4 years) |

| U.S.–Mexico Substrate Supply Disruptions | -0.4% | United States, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Diesel LCV/PV Share in the United States

The diesel mix within light trucks and passenger vehicles has fallen below 3%, eroding a sizeable corner of the traditional aftertreatment installed base. Federal tax credits for battery-electric SUVs and state clean-truck rules incentivize fleets to retire diesel units early. OEM product planners have reduced diesel engine options for half-ton pickups, thereby shrinking future volumes for platinum-rich SCR bricks. Suppliers pivot toward gasoline GPF programs or charger-cooled exhaust systems for plug-in hybrids to backfill lost diesel demand. Tooling amortization for new diesel hardware now spans fewer units, putting pressure on margin outlooks[3]“Annual Energy Outlook 2024,”, U.S. Department of Energy, energy.gov.

High Platinum-Group Metal Price Volatility

Spot rhodium prices hovered around USD 4,750/oz in 2024, having spiked above USD 7,000/oz earlier that year, which pushed catalyst formulation costs sharply higher. Thin trading liquidity and concentrated mining supply in South Africa and Russia amplify price swings. Manufacturers hedge only a fraction of forward exposure, making quarterly earnings sensitive to market dislocations. Some suppliers test ruthenium-doped wash-coats, while others extend recycling cycles to recapture high-value metals from spent substrates. Price risk has rekindled interest in lean NOx traps, which reduce rhodium intensity, though adoption remains limited to the light-duty gasoline segment.

Segment Analysis

By Product Type: SCR Dominates While DPF Gains on Retrofit Momentum

SCR systems generated the single-largest revenue block, accounting for 39.14% of the North American automotive exhaust aftertreatment systems market in 2024. Tight NOx targets sustain adoption across diesel heavy-duty engines, mid-size gasoline pickups, and long-haul tractors. OEM calibration files increasingly depend on dual-dosing configurations that inject urea upstream and mid-stream to widen conversion efficiency at low temperatures. DPF volume expansion, forecasted at a 7.41% CAGR, primarily arises from mandated retrofits in refuse trucks, port drayage fleets, and municipal buses. Higher ash-capacity filter substrates, optimized regeneration algorithms, and corrosion-resistant metallic canning materials reinforce total cost-of-ownership economics. The integrated module trend blurs the boundaries between DOC and DPF layers, allowing suppliers to deliver tuned monolith stacks that shorten exhaust routing and shave 12–18 pounds of mass per vehicle. Through 2030, SCR remains the technological anchor for OEM compliance, but retrofit-driven DPF demand brings countercycle resilience, underpinning stable growth for the North America automotive exhaust aftertreatment systems market.

Second-tier products, such as EGR coolers and lean NOx traps, still serve legacy light-duty applications but now primarily act as assist technologies that smooth transient NOx spikes. Manufacturers refine catalyzed soot filters using engineering ceramics that can tolerate higher peak exotherms, thereby lowering regeneration fuel penalties. DOC maintains relevance as the first monolith in the can, igniting hydrocarbons to boost exhaust temperatures for passive DPF regeneration. Yet its standalone share erodes as combined catalyst coatings migrate onto the DPF brick, densifying functionality inside a unified volume. Suppliers that invest in wash-coat layering techniques claim measurable gains in light-off speed, enabling OEMs to hit step-function emission cuts locked into future rulemakings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fuel Type: Diesel Retains Scale but Gasoline Accelerates on GDI Proliferation

Diesel powertrains provided 67.49% of 2024 revenue for the North America automotive exhaust aftertreatment systems market, thanks to entrenched adoption in Class 4 to Class 8 trucks, vocational equipment, and off-road machinery. Current-generation diesel engines pair high-efficiency SCR cells with coated DPF substrates that harness advanced silicon-carbide channel designs, lowering pressure drop while preserving filtration efficiency. Upgraded turbocharger geometries sustain combustion temperatures conducive to low soot rates, further extending DPF service intervals. Conversely, gasoline aftertreatment units, spanning three-way catalysts (TWC) and GPF combinations, are on track for a robust 7.11% CAGR, powered by record GDI share in pickup, SUV, and crossover segments. OEMs overlay tight light-off targets with periodic active regeneration to protect filter porosity, a balancing act aided by precise injection mapping that limits fuel-borne soot precursors.

Hybrid powertrains, though small in unit share, carry elevated PGM loadings because frequent engine start-stop events demand rapid catalyst light-off. This subset preserves high value per vehicle for catalyst suppliers, partially offsetting diesel contraction in certain light-duty niches. Suppliers fine-tune high-porosity wash-coats and zero-gap brick matting to slash heat loss during coast-down phases, preserving efficiency through repeated thermal cycling. Looking ahead, escalating octane requirements for downsized turbocharged gasoline engines will tighten exhaust thermal budgets, reinforcing momentum behind advanced TWC-plus-GPF stacks across the regional fleet.

By Vehicle Type: Passenger Cars Anchor Revenue, LCVs Propel Future Upside

Passenger cars accounted for 47.32% of the 2024 turnover in the North American automotive exhaust aftertreatment systems market, leveraging their sheer parc scale and a high refresh cadence. Emission compliance strategies rely on compact, under-floor integrated cans that meet rigorous cold-start CO and NOx limits within the first 20 seconds of the cycle time. Luxury brands experiment with electrically heated catalysts that reduce light-off delays by up to 70%, although cost-benefit dynamics currently limit their adoption to premium trims. LCVs, covering vans and chassis-cabs up to 10,000 lb gross weight, clock a forecast-leading 7.34% CAGR. E-commerce activity and the expansion of last-mile delivery push this segment’s mileage accumulation well above average, accelerating DPF regeneration cycles and replacement frequency.

Heavy commercial vehicles remain the core showcase for high-capacity SCR filters and large-diameter DPF bricks. The advent of smart-dosing algorithms, which pair exhaust mass-flow sensors with adaptive urea shot timing, minimizes NH₃ slip during mountain climbs and urban idling. Bus and coach operators increasingly adopt low-pressure EGR coupled with insulated catalyst housings to maintain velocity in low-speed city grids. As metropolitan corridors consider zero-emission zones, retrofittable aftertreatment systems with verified performance credentials become a prerequisite for operating permits. Suppliers thus refine modular mounting brackets to cut retrofit downtime, enhancing value in the North America automotive exhaust aftertreatment systems market size for vehicle-type-specific solutions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End Use: OEM Installations Dominate, Aftermarket Gains on Compliance Retrofits

Factory installations accounted for 72.21% of the 2024 expenditure, reflecting the inextricable link between engine certification and integrated aftertreatment hardware. Platform life cycles lock suppliers into multi-year contracts, providing OEM channel orders with a relatively predictable margin. Hardware complexity has risen, however, requiring tier-1s to co-develop control software, urea tanks, and onboard diagnostics that meet OBD-II and HD-OBD protocols. The aftermarket, forecast to increase at a 6.98% CAGR, captures value from older fleet segments now subject to city-level low-emission zones and federal retrofit incentive schemes. Certified kits bundle mounting hardware, dosing controllers, and sensor arrays, all of which are audited under the EPA’s Verified Technologies list.

Independent distributors develop predictive maintenance packages that alert fleet managers when differential pressure readings indicate filter loading exceeds the threshold, prompting proactive DPF clean-and-bake or cartridge replacement. Data-centric offerings generate recurring revenue, softening the one-off nature of part sales. Insurance underwriters are increasingly mandating verified retrofit compliance before renewing coverage for specific urban freight routes, effectively turning emissions equipment into a quasi-regulatory requirement for operating in these areas. Collectively, OEM dominance preserves base volume, while aftermarket dynamism injects growth durability into the North American automotive exhaust aftertreatment systems market.

Geography Analysis

The United States remained the fulcrum of the North American automotive exhaust aftertreatment systems market in 2024, absorbing 79.19% of total demand amid vigorous enforcement by the Environmental Protection Agency and CARB. New engine launch programs across Detroit Three pickup platforms and multiple Class 8 powertrain refreshes amplified SCR and DPF procurement. Domestic substrate extrusion lines in the Midwest and Southeastern corridors gained investment priority, strengthening regional self-sufficiency and aligning with Buy-America content preferences. Federal Inflation Reduction Act incentives further tilt manufacturing footprints toward U.S. soil, buffering the market against future trade disruptions.

Canada is slated for the fastest 7.53% CAGR through 2030, primarily due to Ottawa's harmonization of light- and heavy-duty regulations with U.S. Tier III and Phase 3 frameworks. Provincial green-freight funding, coupled with an accelerated capital-cost allowance for clean-transport investments, shortens fleet payback periods on retrofit kits. Cross-border component flows diversify risk for Canadian assemblers as they source substrates from Quebec, coatings from Ontario, and steel cans from Michigan suppliers. This inter-provincial cross-pollination tightens lead times and injects resilience into the North American automotive exhaust aftertreatment systems market share.

Mexico’s strategic location under the USMCA pact positions it as a substrate and catalyst production hotbed that feeds U.S. assembly plants while tapping domestic light-truck growth. Low labor costs, competitive energy pricing, and buy-region compliance enable Mexican facilities to absorb volume surges with shorter notice than their Asian alternatives. Yet logistics hiccups at the Laredo and Otay Mesa crossings underscore the need for multi-route redundancy. Mexican investments in rail-served industrial parks and bonded warehouse capacity aim to alleviate such chokepoints, thereby enhancing the regional integration that supports broader market stability.

Competitive Landscape

Several multinationals—Tenneco, Cummins, Faurecia (formerly FORVIA), BorgWarner, Bosch, Johnson Matthey, Corning, and NGK—dominate the supplier landscape, collectively capturing the lion's share of OEM purchase orders. The trend of consolidation gained momentum with Deutz's acquisition of a significant stake in HJS Emission Technology, highlighting the industry's strategic emphasis on aftertreatment expertise. Platform modularity amplifies supplier bargaining power because a single-can design consolidates multiple functions into a single sourcing decision. Suppliers strengthen their moat through PGM recycling ventures; Heraeus Precious Metals’ 2024 purchase of McCol Metals increased regional rhodium and palladium recovery, buffering input volatility.

Technology differentiation hinges on wash-coat layering, porosity control, and corrosion-resistant cladding that extend useful life alongside stricter warranty mandates. Cummins pilots solid ammonia closed-loop systems aimed at class-8 tractors that idle extensively in port queues. At the same time, Johnson Matthey scales tri-metal catalyst formulations that flex between platinum, palladium, and rhodium in response to price swings. Partnerships, such as the Volvo Group–Westport Fuel Systems joint venture, which aims to commercialize high-pressure direct-injection (HPDI) fuel systems, illustrate how combustion and aftertreatment pathways intertwine when decarbonizing long-haul transport.

Digital monitoring emerges as a disruptive wedge. Start-ups integrate exhaust sensor streams with cloud analytics, flagging catalyst dehydration events before they trigger check-engine lights. Tier-1s embed Bluetooth-enabled differential-pressure sensors within replacement DPF cartridges, creating value-added subscription opportunities. As electrification accelerates, leading aftertreatment suppliers hedge their bets by investing in battery thermal-management components and hydrogen internal-combustion subsystems, positioning themselves for diversified revenue beyond 2030.

North America Automotive Exhaust Aftertreatment Systems Industry Leaders

-

Delphi Technologies

-

Tenneco Inc.

-

Cummins Inc.

-

Robert Bosch GmbH

-

Faurecia (FORVIA)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Volvo Trucks North America is set to apply for certification of a CARB-24 Omnibus-compliant engine, aiming to align with the California Air Resources Board’s 2024 emissions standards. The company anticipates the engine will soon be available for order. Engineered to achieve a 0.05g NOx rating, the new engine also boasts reduced particulate matter (PM) emissions. This development underscores Volvo's commitment to achieving zero emissions in heavy-duty transportation by 2040.

- February 2025: Isuzu has rolled out three new models in its ELF truck lineup in Mexico: the ELF 400, ELF 500, and ELF 600. These trucks feature the P700 cabin, designed to enhance aerodynamics and boost driver comfort. This revamped cabin not only optimizes space but also elevates the overall passenger experience by prioritizing functionality. Looking ahead, Isuzu plans to incorporate this advanced cabin design across its entire vehicle range. All three models meet stringent Euro VI standards and come equipped with an advanced aftertreatment system, including Selective Catalytic Reduction technology, to significantly cut down on harmful emissions.

North America Automotive Exhaust Aftertreatment Systems Market Report Scope

The North America automotive exhaust aftertreatment systems market report is segmented by product type (selective catalytic reduction, diesel particulate filter, and more), fuel type (gasoline and diesel), vehicle type (passenger cars, LCV, HCV, and buses and coaches), end use (OEM and aftermarket), and country. The market forecasts are provided in terms of value (USD).

By Product Type

| Selective Catalytic Reduction (SCR) |

| Diesel Particulate Filter (DPF) |

| Diesel Oxidation Catalyst (DOC) |

| Exhaust Gas Recirculation (EGR) |

By Fuel Type

| Diesel |

| Gasoline |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Buses & Coaches |

By End Use

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

By Country

| United States |

| Canada |

| Rest of North America |

| By Product Type | Selective Catalytic Reduction (SCR) |

| Diesel Particulate Filter (DPF) | |

| Diesel Oxidation Catalyst (DOC) | |

| Exhaust Gas Recirculation (EGR) | |

| By Fuel Type | Diesel |

| Gasoline | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Buses & Coaches | |

| By End Use | OEM (Original Equipment Manufacturer) |

| Aftermarket | |

| By Country | United States |

| Canada | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America automotive exhaust aftertreatment systems market?

The market is valued at USD 7.52 billion in 2025 and is projected to grow to USD 10.30 billion by 2030.

Which product segment holds the largest revenue share?

Selective catalytic reduction systems led with a 39.14% share in 2024.

Which vehicle category is expected to grow the fastest?

Light commercial vehicles should post the highest 7.34% CAGR through 2030.

Why are gasoline particulate filters gaining momentum?

Tightening PM rules for GDI engines and confirmed durability results are pushing mainstream OEM adoption.

How will PGM price volatility affect suppliers?

Fluctuating rhodium, palladium, and platinum prices inflate catalyst costs, prompting hedging, recycling, and formulation shifts.

Page last updated on: