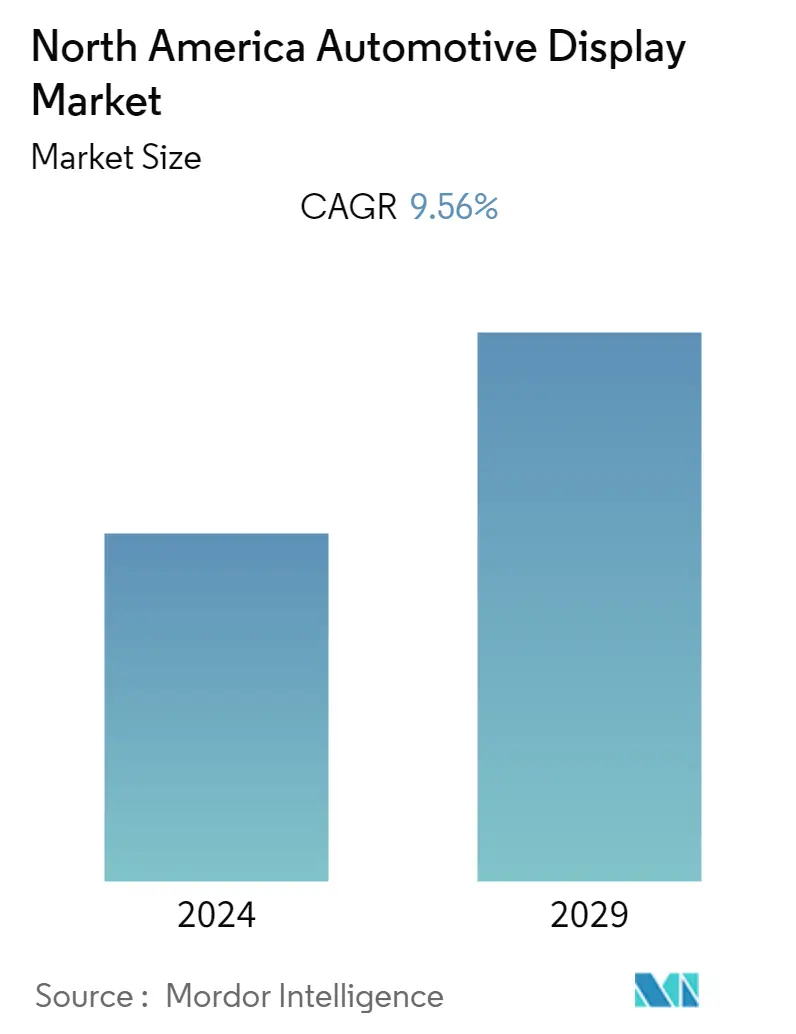

Market Size of North America Automotive Display Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 9.56 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Automotive Display Market Analysis

The North America Automotive Display Market was valued USD 4,969.10 million in 2021, and is expected to reach USD 8593.8 million registering CAGR of around 9.56% during the forecast period, 2022 - 2027.

Alhtough during Covid-19, demand for automotive displays witness a steep fall amid the reduce automotive sales and production across the United States and Canada. Considering the fact that, automotive display demand is deeply linked with automotive sales including passenger and commercial vehicles, Noth America showcased shrinking in demand during Q121 to Q421. Although after Q421, demand for automotive resumed globally and production houses in the United States also began at a faster pace.

Although, over the medium term, automotive sales in United States and Canada is showcasing prominent growth which is quite good sign for automotive display demand in the North America. With overall automotive navigation and connectivity characterizing the cars of this generation, automotive visualization technologies are becoming the most vital components of in-vehicle interactions. As a result, the incorporation of interactive displays has become a key feature of the vehicle manufacturing processes among a few prominent automakers like General Motors and Tesla.

In the last few years, the larger display in the vehicle interior system has improved tremendously. Many players have introduced their vehicles with big screens in the market. For intsnace, in 2021, S-Class from Mercedes packed with screens (the central unit will be a 12.8-inch OLED screen with haptic feedback). The new car has replaced a large number of physical buttons present in the past version with controls that are now in the screens all around the cabin. This screen, which has superior processing power, special pixels for extreme clarity, and compatibility with swipes, gestures, and voice commands, also has biometric security. Also, Mercedes owns the largest 56-inch-wide curved screen in its Mercedes-Benz Hypersceen.

Furthermore, the growing trend of connectivity in vehicles, augmented reality, with the increased integration of smartphones and tablets with in-vehicle entertainment and information systems, propel the demand for advanced display systems. Vehicle interiors are revolutionizing by providing the futuristic digital user experience in front of drivers. The number of displays in vehicles has been continuously increasing, as OEMs are always trying to stay ahead from their competitors to make their cars more attractive with advanced instrument clusters.

The region is one of the largest automotive markets worldwide, owing to its large-scale domestic production, with the major global players having their production plants in the United States. There are thirteen major car manufacturers in the United States. Considering these ongoing development in a factors, demand for automotive display is expected to witness a positive growth rate during the forecast period.

North America Automotive Display Industry Segmentation

The automotive display is a part of a vehicle's interior system. The display represents all the necessary information about the vehicle and is generally poisoned as head up, in the instrument cluster, and for infotainment purposes. These displays are sometimes highly automated to enhance the vehicle cockpit experiences. Furthermore, automotive displays come under several quality as high resolution, medium resolution, and low-resolution displays.

The North American automotive display market is segmented by vehicle type, product type, by display technology, sales channel, and by country. By Vehicle Type, the market has been segmented into passenger cars and commercial vehicles. By product type, the market has been segmented into center stack displays, instrument cluster displays, head-up displays, and rear seat entertainment displays.

By display technology, the market has been segmented into LCD, TFT-LCD, and OLED. By sales channel, the market has been segmented into OEM and Aftermarket and By country, the market has been segmented into the United States, Canada, and the Rest of North America. For each segment, the market sizing and forecasting are based on value (USD million).

| By Vehicle Type | |

| Passenger Cars | |

| Commercial Vehicles |

| By Technology Type | |

| LCD | |

| TFT-LCD | |

| OLED |

| By Product Type | |

| Center Stack Display | |

| Instrument Cluster Display | |

| Heads-up Display | |

| Rear Seat Entertainment System |

| By Sales Type | |

| OEM | |

| Aftermarket |

| By Country | |

| United States | |

| Canada | |

| Rest of North America |

North America Automotive Display Market Size Summary

The North American automotive display market is poised for significant growth, driven by the resurgence in automotive sales and the increasing integration of advanced display technologies in vehicles. The market, which experienced a downturn during the COVID-19 pandemic due to reduced automotive sales and production, has rebounded as production facilities in the United States ramped up operations. The demand for automotive displays is closely tied to the automotive industry's recovery, with a notable increase in the adoption of interactive displays and advanced visualization technologies by major automakers like General Motors and Tesla. These technologies are becoming essential for enhancing in-vehicle interactions, with larger displays and augmented reality features transforming vehicle interiors into futuristic digital environments.

The region's status as a leading automotive market, coupled with its technological sensitivity, positions it for robust growth in the automotive display sector. The increasing popularity of head-up displays (HUDs) and the integration of smartphones and tablets with in-vehicle systems are key trends propelling market expansion. Despite challenges such as semiconductor shortages and inflation, the market is witnessing a steady rise in demand, particularly for HUDs in SUVs and luxury vehicles. The presence of major global players and ongoing technological advancements, such as Visteon Corporation's TrueColor Image Enhancement technology, further bolster the market's growth prospects. As manufacturers continue to innovate and expand their market presence, the North American automotive display market is expected to experience a positive growth trajectory in the coming years.

North America Automotive Display Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.2 Market Restraints

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size in Value USD Million)

-

2.1 By Vehicle Type

-

2.1.1 Passenger Cars

-

2.1.2 Commercial Vehicles

-

-

2.2 By Technology Type

-

2.2.1 LCD

-

2.2.2 TFT-LCD

-

2.2.3 OLED

-

-

2.3 By Product Type

-

2.3.1 Center Stack Display

-

2.3.2 Instrument Cluster Display

-

2.3.3 Heads-up Display

-

2.3.4 Rear Seat Entertainment System

-

-

2.4 By Sales Type

-

2.4.1 OEM

-

2.4.2 Aftermarket

-

-

2.5 By Country

-

2.5.1 United States

-

2.5.2 Canada

-

2.5.3 Rest of North America

-

-

North America Automotive Display Market Size FAQs

What is the current North America Automotive Display Market size?

The North America Automotive Display Market is projected to register a CAGR of 9.56% during the forecast period (2024-2029)

Who are the key players in North America Automotive Display Market?

Robert Bosch GmbH, Continental AG, DENSO Corporation, Visteon Corporation and LG Electronics are the major companies operating in the North America Automotive Display Market.