Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 15.11 Billion |

| Market Size (2031) | USD 23.65 Billion |

| Growth Rate (2026 - 2031) | 9.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aseptic Packaging Market Analysis by Mordor Intelligence

The North America aseptic packaging market is expected to grow from USD 13.82 billion in 2025 to USD 15.11 billion in 2026 and is forecast to reach USD 23.65 billion by 2031 at 9.36% CAGR over 2026-2031. Expansion is led by pharmaceutical biologics that require validated sterile containers, dairy processors intent on extending shelf life without refrigeration, and beverage brands aiming to curb cold-chain freight expenses across continental routes. Adoption further accelerates because inline AI sterility monitoring now verifies microbial integrity in real time, lowering recall risk for regulated drug and food plants. At the same time, material innovations especially fiber-based laminates and inert glass strengthen barrier performance while appeasing sustainability mandates. Competitive momentum therefore swings toward suppliers that bundle filling machinery, data analytics, and recycling partnerships into one integrated offer, adding a new digital layer to an already capital-intensive sector.

Key Report Takeaways

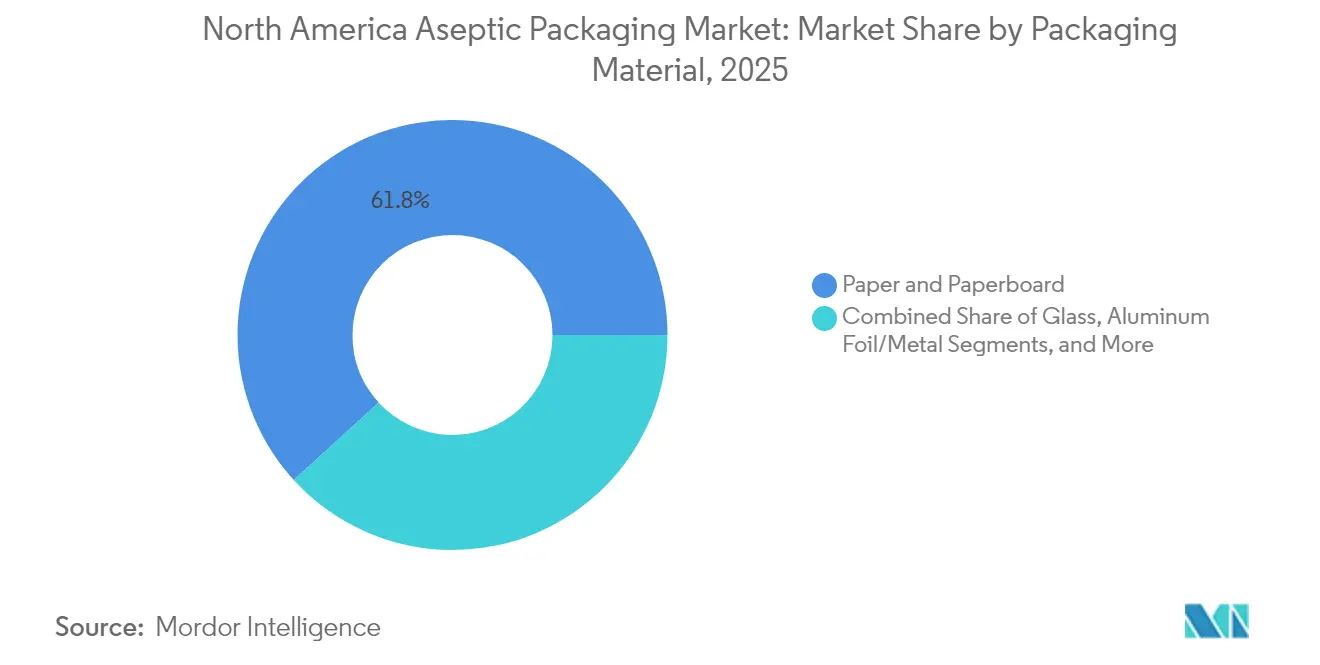

- By packaging material, paper and paperboard led with 61.78% revenue share in 2025; glass packaging is advancing at a 10.24% CAGR through 2031.

- By product type, cartons held 41.95% of the North America aseptic packaging market share in 2025, while vials and ampoules record the fastest 10.79% CAGR to 2031.

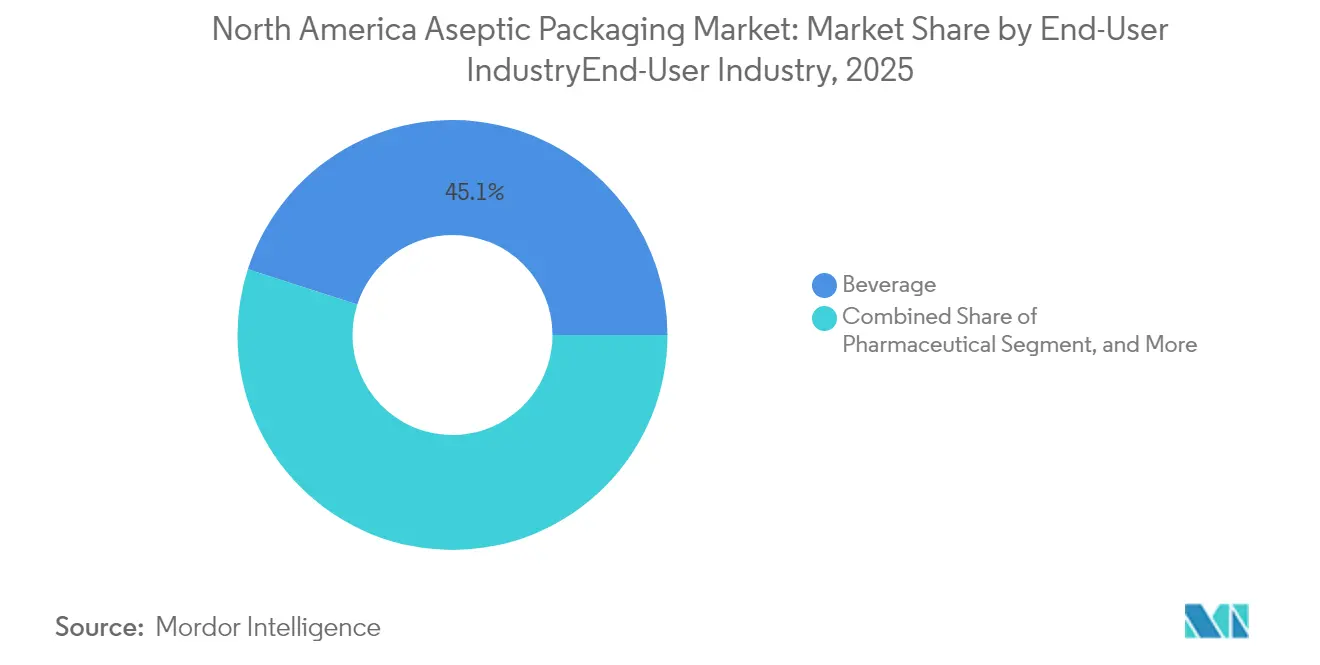

- By end-user industry, beverages commanded 45.05% of the North America aseptic packaging market size in 2025, and pharmaceuticals are moving forward at an 10.84% CAGR through 2031.

- By technology, aseptic liquid filling maintained 48.55% share in 2025; blow-fill-seal equipment is expanding at a 10.05% CAGR to 2031.

- The United States contributed 71.88% of regional revenue in 2025, whereas Mexico showed the strongest 11.23% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Aseptic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand to cut cold-chain logistics costs | +1.8% | North America, strongest in Mexico and rural U.S. | Medium term (2-4 years) |

| Preference for products with ≥12-month shelf life | +2.1% | U.S. and Canadian urban centers | Short term (≤2 years) |

| Sustainability push for paper-based and lightweight formats | +1.2% | North America and EU aligned regions | Long term (≥4 years) |

| Rapid expansion of aseptic capacity in U.S. dairy plants | +0.9% | Midwest and Southwest dairy corridors | Medium term (2-4 years) |

| Surge in biologics and RTU injectables needing sterile packs | +0.6% | U.S. hubs, Canadian biotech clusters | Long term (≥4 years) |

| AI-enabled inline sterility monitoring reducing recalls | +0.3% | U.S. and Canadian pharma centers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Demand to Cut Cold-Chain Logistics Costs

Temperature-controlled transport absorbs 15-25% of distribution budgets, so eliminating refrigeration quickly improves margins.[1] Foreign Agricultural Service, “Mexico: Dairy and Products Semi-Annual 2025,” fas.usda.gov Mexican milk imports, for instance, avoid USD 0.15-0.30 per liter in freight premiums when shipped ambient. Nestlé has earmarked USD 1 billion for aseptic lines in Mexico between 2025 and 2027 to exploit the savings. Rural U.S. counties with limited cold storage echo the calculus, while Canadian dairies rely on shelf-stable packs to reach remote northern communities where logistics costs often exceed product value. As diesel prices and driver shortages linger, the North America aseptic packaging market finds a durable advantage in cutting refrigerated miles.

Preference for Products with ≥12-Month Shelf Life

Bulk buying expanded during pandemic pantry stocking, and ambient-stable items now fetch 20-30% mark-ups in city markets. Tetra Pak surveys show 67% of households rank shelf life above brand loyalty. In pharma, SCHOTT Pharma’s USD 371 million North Carolina plant triples syringe output that holds room-temperature stability for 36 months. Urban shoppers equate longer life with convenience and emergency readiness, prompting beverage reformulations that withstand ambient warehousing. As a result, the North America aseptic packaging market gains momentum from both grocery aisles and hospital inventories.

Sustainability Push for Paper-Based and Lightweight Formats

California SB 54 stipulates 65% recycled content by 2032, intensifying demand for renewable substrates that preserve sterility. Smurfit WestRock aims for 100% recyclable packs by 2030, while Graphic Packaging allocates USD 200 million to fiber-barrier innovations. Although multilayer structures complicate recovery, consumer surveys suggest a 15-20% price tolerance for paper-centric options. Regulators and retailers now reward bio-based coatings that replace petroleum polymers, steering the North America aseptic packaging market toward circular design despite infrastructure gaps.

Rapid Expansion of Aseptic Capacity in U.S. Dairy Plants

Dairy processors spent USD 2.8 billion on upgrades in 2024, channeling 40% into aseptic lines that cut USD 0.12 per gallon in monthly cold storage charges. Midwest cooperatives deploy the technology to reclaim share from plant-based beverages, while Southwest facilities court Hispanic consumers familiar with shelf-stable formats. SIG Combibloc’s USD 35 million expansion in Querétaro supports cross-border dairy exports. Profit upside also stems from premium organic milk that earns 40-50% margins when sold ambient, reinforcing the North America aseptic packaging market trajectory.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex and long ROI for aseptic filling lines | -1.4% | North America, with strongest impact on mid-size manufacturers | Medium term (2-4 years) |

| Complex multi-material recycling infrastructure gaps | -0.8% | U.S. and Canadian waste management systems, limited Mexican infrastructure | Long term (≥ 4 years) |

| Contamination recalls eroding brand trust and margins | -0.7% | U.S. and Canadian markets with established recall systems, emerging in Mexico | Short term (≤ 2 years) |

| Rising polymer and paperboard prices squeezing converters | -0.5% | North America, with acute impact on multilayer composite manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex and Long ROI for Aseptic Filling Lines

Turnkey systems cost USD 10-50 million, and pharmaceutical validation adds another USD 2-5 million, extending payback to 7-10 years. Smaller processors struggle to finance such outlays, especially when technical talent commands 25-30% wage premiums. Leasing models seldom suit bespoke aseptic rigs, so mergers and private equity funding dominate expansion. Consolidation, therefore, rises even as demand surges, tempering the growth curve of the North America aseptic packaging market.

Complex Multi-Material Recycling Infrastructure Gaps

Less than 40% of multilayer cartons enter effective recovery streams versus 75% for single-material packs.[2]U.S. Environmental Protection Agency, “Materials, Waste and Recycling,” epa.gov Only one-third of North American material recovery facilities possess delamination equipment, and producer-funded upgrades add 3-5% to product cost in Canada. Even where pilot plants exist, separating aluminum foil from fiber remains energy-intensive. Until collection networks mature, legacy multilayer designs will face policy penalties that moderate long-run gains for the North America aseptic packaging market.

Segment Analysis

By Packaging Material : Paper Leads While Glass Gains Ground

Paperboard contributed 61.78% revenue in 2025, a testament to entrenched supply chains and consumer trust in renewable fibers. The segment also aligns with state recycled-content statutes, adding regulatory tailwind to the North America aseptic packaging market. Yet glass records a 10.24% CAGR through 2031, propelled by pharma’s need for chemical inertness. Innovations such as Corning Valor Glass solve historic delamination issues, while SCHOTT’s pre-sterilized vials shrink fill-finish steps. Plastics keep a foothold in flexibles, but single-use scrutiny caps upside. Aluminum foil remains essential for ultra-low oxygen transmission in sensitive biologics. Multilayer composites blend these attributes but confront recycling headwinds already outlined. Overall, material choice in the North America aseptic packaging industry depends on striking an equilibrium among sterility, sustainability, and cost targets.

The outlook shows glass emerging from niche status. Pharma manufacturers value its compatibility with lyophilized biologics and its immunity to extractables, justifying higher weight penalties. Conversely, beverage brands retain paper cartons for ambient juices, plant milks, and broths where fiber-based stories resonate with shoppers. Polymer barrels of regulatory pressure spur a gradual pivot toward bio-based coatings rather than outright abandonment. Collectively, these currents reinforce a diversified substrate mix that shields the North America aseptic packaging market from raw-material shocks.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type : Vials Accelerate Beyond Carton Mainstay

Cartons captured 41.95% of 2025 volume thanks to decades-old shelf-stable beverage lines and efficient pallet utilization. Nonetheless, vials and ampoules outpace all other formats at a 10.79% CAGR, buoyed by expanding biologic injections that need pristine primary packs. The segment benefits from ready-to-use configurations that arrive washed and depyrogenated, trimming drugmaker cycle times. Blow-fill-seal single-dose designs also attract vaccine programs that require needle-free workstreams. Consequently, pharmaceuticals tilt the North America aseptic packaging market toward container miniaturization and higher unit value.

Bottles serve premium cold brew coffees and nutritional shakes that justify heavier glass or PET. Pouches address soup and sauce brands needing flexible geometry at low gram weight. Meanwhile, in-line AI inspection embedded in new filling heads adds another layer of differentiation by slashing sterile failure rates. Every product family, therefore, jockeys for share via either convenience or compliance, making adaptive production platforms a strategic must for converters.

By End-User Industry : Pharmaceutical Upswing Outruns Beverage Stronghold

Beverages commanded 45.05% of turnover in 2025 and will retain numeric leadership because juice, dairy, and nutraceutical drinks remain pantry staples. However, pharmaceuticals exhibit the steeper 10.84% CAGR through 2031 as gene therapies, monoclonal antibodies, and long-acting injectables scale. Drug developers assign significant value to validated barriers, which elevates the average selling price per unit and pushes the North America aseptic packaging market toward a higher margin mix. West Pharmaceutical Services typifies this shift with expanded sterile component lines in Pennsylvania.

Food processors lean on ambient soups and hummus to reduce preservatives, while personal care entrants trial sterile sachets for probiotic cosmetics. Industrial chemical niches, such as aseptic pesticides, round out demand. Diverse application breadth helps cushion cyclical shocks, though capital spending cadence remains tied to pharma launch pipelines and dairy farm modernization efforts.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology : BFS Innovation Challenges Liquid Filling Dominance

Aseptic liquid systems still own 48.55% share because high-speed rotary fillers marry throughput with carton economies. Even so, blow-fill-seal rigs post a 10.05% CAGR thanks to built-in container molding that minimizes human touchpoints. ApiJect’s pre-filled injector exemplifies BFS versatility, courting mass immunization contracts. Form-fill-seal maintains relevance for flexibles in tomato products and baby food, whereas electron-beam sterilization debuts for heat-sensitive plant proteins.

Looking forward, digital twins simulate airflow and particle counts, shortening qualification timelines mandated by the FDA. Vendors bundling software, IoT sensors, and spare-parts service thus capture sticky revenue streams, reinforcing technological bifurcation inside the North America aseptic packaging market.

Geography Analysis

The United States held 71.88% revenue in 2025, anchored by pharmaceutical corridors in North Carolina, New Jersey, and California that prize proximity to syringe and vial suppliers. SCHOTT Pharma’s recent plant scale-up directly answers that geographic clustering. Dairy belts in Wisconsin and New York also widen aseptic adoption to bypass cold-chain surcharges when shipping coast-to-coast. FDA oversight supplies a stringent regulatory halo that U.S. converters leverage when exporting to Latin America and Europe, boosting order stability in the North America aseptic packaging market.

Canada delivers consistent gains under Health Canada GMP rules congruent with U.S. expectations.Toronto’s biotech corridor and Vancouver’s clean-tech hub fuel demand for small-batch sterile packs, while dairy co-ops rely on aseptic cartons to reach Yukon and Nunavut stores accessible only by seasonal roads. Regulatory reciprocity lowers documentation costs for suppliers, cementing cross-border equipment and material flows.

Mexico logs the swiftest 11.23% CAGR. Nestlé’s USD 1 billion rollout underscores the business case in rural provinces where refrigeration is scarce. National dairy self-sufficiency goals target 25% output growth by 2030, virtually guaranteeing carton volume ramps. COFEPRIS alignment with FDA norms unlocks technology transfers and lifts investor confidence. Consequently, Mexico evolves from an export-receiving node into an integrated production base supporting the wider North America aseptic packaging market.

Competitive Landscape

Industry structure skews toward mid-level concentration. Multinationals like Tetra Pak, SIG Combibloc, and SCHOTT Pharma pair material production with proprietary fillers, giving them scale economies and regulatory know-how. Capital barriers USD 10-50 million per line hinder new entrants and prompt roll-ups of niche converters unable to self-fund automation upgrades. Patent estates in blow-fill-seal and fiber-barrier laminates form further moats. The North America aseptic packaging market, therefore, rewards depth in validation services and real-time analytics more than commodity tonnage.

Yet white space remains. Sustainability regulations incentivize new recyclable laminates where incumbent intellectual property is thinner. AI quality assurance and closed-loop sensors attract start-ups backed by cloud providers who see industrial data as the next platform. Brands seeking carbon footprint cuts also trial refill-on-demand micro-factories that bypass centralized filling, posing a modest but visible threat to legacy line economics. For now, however, top suppliers preserve margin by bundling OEE dashboards, parts, and compliance audits into evergreen service contracts.

North America Aseptic Packaging Industry Leaders

Sealed Air Corporation

Schott AG

Tetra Pak International S.A.

Amcor plc

SIG Combibloc Group AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: SCHOTT Pharma completed its USD 371 million facility expansion in North Carolina, tripling syringe production capacity to address rising demand for ready-to-use sterile packaging across North America.

- December 2024: SIG Combibloc completed a USD 35 million capacity hike in Querétaro, adding 40% more aseptic carton volume.

- November 2024: Nestlé pledged USD 1 billion for ambient-stable foods in Mexico from 2025-2027.

- October 2024: SCHOTT Pharma, Gerresheimer, and Stevanato Group formed the Alliance for RTU to streamline injectable packaging.

North America Aseptic Packaging Market Report Scope

Aseptic packaging is a specific manufacturing process in which products such as food, pharmaceuticals, or other products are sterilized separately from the packaging. The sterilized contents are then inserted into the container in a sterile environment. This method primarily uses extremely high temperatures to maintain the freshness of the contents while ensuring that they are not contaminated with microorganisms.

North America Aseptic Packaging Market is Segmented by Product Type (Plastic Bottles, Prefillabe Syringes, Vials and Ampoules, Bags and Pouches, Cartons, Cups, and Glass Bottles), by End- User Type (Pharmaceutical, Beverage (Fruit-Based, Milk and Other Dairy Beverages, Ready-To-Drink, Other Beverage Industry Types), Food (Fruit-Based, Dairy Food, Processed Foods, Baby Foods, Soups and Broths, Other Food Industry Types)), and by Country (United States and Canada). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

By Packaging Material

| Paper and Paperboard |

| Plastics |

| Glass |

| Aluminum Foil/Metal |

| Multilayer Composites |

By Product Type

| Bottles |

| Cartons |

| Bags and Pouches |

| Vials and Ampoules |

| Other Product Types |

By End-User Industry

| Pharmaceutical | |

| Beverage | Fruit-based Drinks |

| Milk and Other Dairy Beverages | |

| Ready-to-Drink (RTD) | |

| Other Beverage Types | |

| Food | Fruit-based Foods |

| Dairy Food | |

| Processed Foods | |

| Soups and Broths | |

| Other Food Types | |

| Personal Care and Cosmetics | |

| Industrial | |

| Other End-User Industries |

By Technology

| Aseptic Liquid Packaging |

| Blow-Fill-Seal (BFS) |

| Form-Fill-Seal (FFS) |

| Electron-Beam Sterilization |

| Ultra-High-Temperature (UHT) / HTST |

By Country

| United States |

| Canada |

| Mexico |

| By Packaging Material | Paper and Paperboard | |

| Plastics | ||

| Glass | ||

| Aluminum Foil/Metal | ||

| Multilayer Composites | ||

| By Product Type | Bottles | |

| Cartons | ||

| Bags and Pouches | ||

| Vials and Ampoules | ||

| Other Product Types | ||

| By End-User Industry | Pharmaceutical | |

| Beverage | Fruit-based Drinks | |

| Milk and Other Dairy Beverages | ||

| Ready-to-Drink (RTD) | ||

| Other Beverage Types | ||

| Food | Fruit-based Foods | |

| Dairy Food | ||

| Processed Foods | ||

| Soups and Broths | ||

| Other Food Types | ||

| Personal Care and Cosmetics | ||

| Industrial | ||

| Other End-User Industries | ||

| By Technology | Aseptic Liquid Packaging | |

| Blow-Fill-Seal (BFS) | ||

| Form-Fill-Seal (FFS) | ||

| Electron-Beam Sterilization | ||

| Ultra-High-Temperature (UHT) / HTST | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America aseptic packaging market?

It is USD 15.11 billion in 2026, with a forecast to reach USD 23.65 billion in 2031 at a 9.36% CAGR.

Which end-user application is growing fastest?

Pharmaceuticals expand at an 10.84% CAGR through 2031 due to biologics and ready-to-use injectables.

Why are vials and ampoules gaining share?

Drugmakers prefer sterile, ready-to-use glass containers that minimize contamination and shorten fill-finish cycles.

How does aseptic packaging cut logistics costs?

Eliminating refrigeration removes USD 0.15-0.30 per liter in transport premiums, especially on cross-border dairy routes.

What is the biggest restraint to wider adoption?

High capital expenditure USD 10-50 million per line and long 7-10 year payback periods deter mid-size converters.

Which technology is growing quickest?

Blow-fill-seal equipment posts a 10.05% CAGR because it integrates container molding and filling in one sterile step.