Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

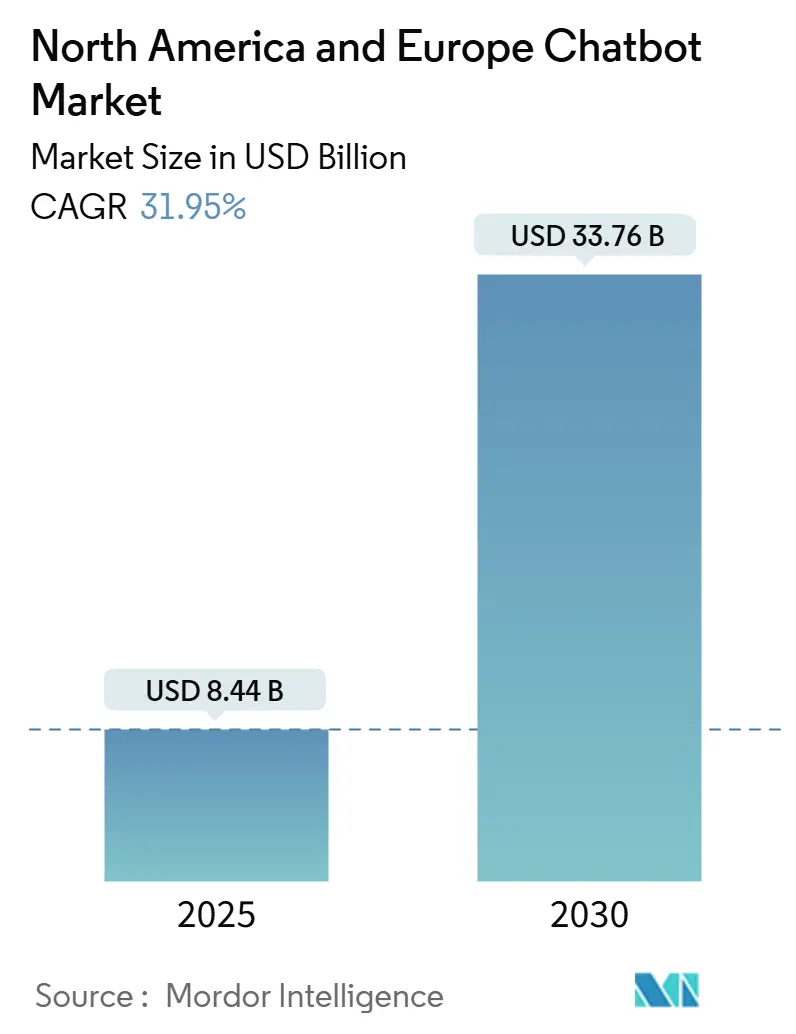

| Market Size (2025) | USD 8.44 Billion |

| Market Size (2030) | USD 33.76 Billion |

| Growth Rate (2025 - 2030) | 31.95% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America And Europe Chatbot Market Analysis by Mordor Intelligence

The North America and Europe Chatbot Market size is estimated at USD 8.44 billion in 2025, and is expected to reach USD 33.76 billion by 2030, at a CAGR of 31.95% during the forecast period (2025-2030). A steep decline in large-language-model (LLM) inference costs, coupled with omnichannel service mandates from enterprises, is pushing conversational AI from experimental pilots into enterprise-grade production environments. Large buyers are replacing agent-centric contact centers with AI-native platforms that operate 24/7, handle multilingual queries, and reduce operating expenses by up to 50%. Regulatory nudges in insurance and healthcare accelerate adoption by leveraging automated triage, claims, and compliance workflows, thereby reducing human error and enhancing audit trails. Cloud deployment dominates because infrastructure-agnostic delivery shortens implementation from months to weeks, while hybrid and sovereign-cloud designs meet data-residency mandates in Europe. Competitive dynamics favor hyperscale providers that bundle conversational AI into broader contracts, yet open-source frameworks sustain differentiated positions for vendors focused on regulated verticals.

Key Report Takeaways

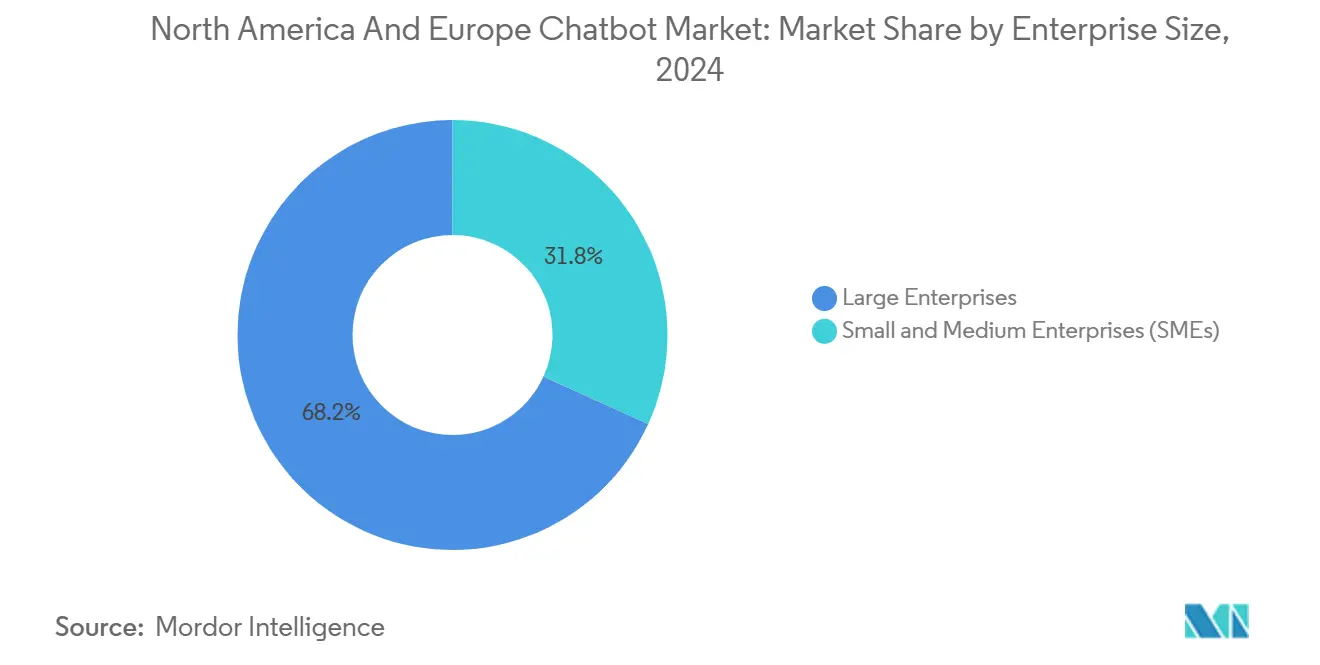

- By enterprise size, large enterprises commanded 68.20% of the North America and Europe chatbot market in 2024, while small and medium enterprises are projected to grow at a 32.45% CAGR to 2030.

- By end-user vertical, the BFSI segment led with 27.60% of the North America and European chatbot market in 2024, while the healthcare segment is forecast to advance at a 33.12% CAGR through 2030.

- By architecture, rule-based/NLU chatbots captured 55.12% of the North America and European chatbot market in 2024, whereas generative AI chatbots are expected to expand at a 33.41% CAGR through 2030.

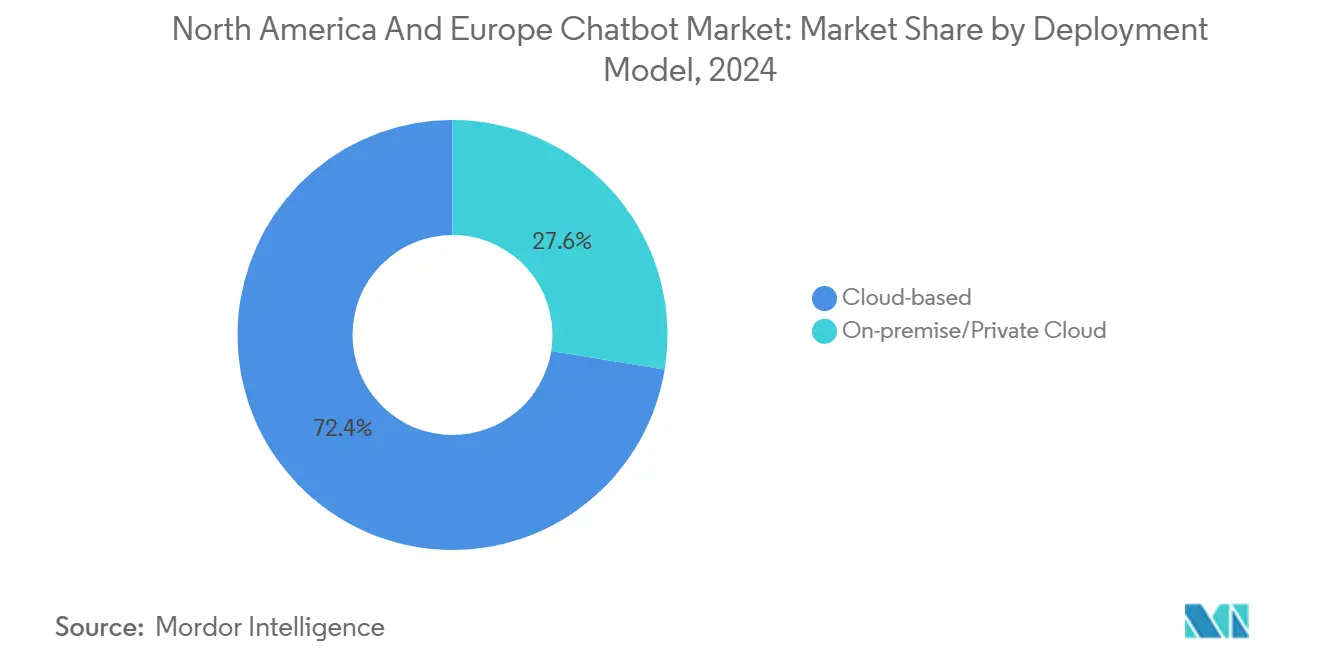

- By deployment model, cloud-based models accounted for 72.43% of the North America and European chatbot market in 2024 and are projected to rise at a 34.12% CAGR through 2030.

- By communication channel, web and mobile apps held 43.79% of the North America and European chatbot market in 2024, whereas voice assistants and IVR integrations are the fastest-growing sub-segment, with a 33.98% CAGR to 2030.

- By geography, North America retained 61.80% of the North America and European chatbot market in 2024, while Europe is pacing ahead with a 32.87% CAGR through 2030.

North America And Europe Chatbot Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Native Customer-Experience Platforms Adoption Surge | +8.2% | Global, with North America leading enterprise rollouts | Medium term (2-4 years) |

| Rapid LLM Cost Declines Broaden SME Access | +7.5% | Global, particularly benefiting European SMEs and Canadian mid-market firms | Short term (≤ 2 years) |

| Omnichannel CX Mandates from Fortune-1000 Majors | +6.8% | North America and Europe, concentrated in BFSI and retail sectors | Medium term (2-4 years) |

| Insurance-Sector Regulatory Nudges for Digital Servicing | +3.2% | North America (state-level mandates) and Europe (Solvency II digital-service requirements) | Long term (≥ 4 years) |

| Growing Preference for Voice-First Interfaces | +4.1% | North America (automotive, smart-home), Europe (multilingual IVR upgrades) | Medium term (2-4 years) |

| Context-Aware Chatbots for Healthcare Triage | +5.7% | Global, with U.S. hospital systems and European national health services leading pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Native Customer-Experience Platforms Adoption Surge

Enterprises are exiting siloed, license-heavy suites in favor of unified orchestration layers that integrate chat, voice, and live agents into a single interface. Vodafone rolled out Microsoft Azure-based chatbots across 14 European markets in 2024, deflecting 68% of Tier 1 queries and saving millions in contact center labor. [1]Microsoft, “Investor Relations,” microsoft.com Best Buy embedded a generative assistant in its mobile app during the 2024 holiday period and saw a 22% uplift in product-discovery conversions. Standardized connectors, pre-trained industry packs, and ISO 27001 certifications now ship out of the box, cutting deployment from nine months to six weeks and expanding the chatbot market among compliance-oriented verticals.

Rapid LLM Cost Declines Broaden SME Access

Token-level inference costs for high-performing LLMs have decreased roughly tenfold each year since 2023, owing to the optimization of transformers and the development of custom silicon. Databricks documented an 80% bill reduction after moving from GPT-4 to the open-weight Llama 3.3 model in early 2025. [2]Databricks, “Cutting LLM Costs by 80%,” databricks.com Canadian SMEs, buoyed by federal grants, doubled the deployment rate of chatbots in 2024 compared to their US peers. European small businesses leverage regional providers, such as OVHcloud, to obtain GDPR-compliant hosting at 40% lower costs than hyperscale alternatives. No-code platforms with templated flows now serve more than 2 million SME users, demonstrating that cost barriers to entry are nearing zero for mainstream verticals.

Omnichannel CX Mandates from Fortune-1000 Majors

Board-level mandates necessitate a single conversation thread across web chat, mobile, social messaging, and voice channels. UPS integrated chatbots into its app and WhatsApp Business in 2024, cutting call-center package inquiries by 41%. [3]UPS, “Investor Presentation Q3 2024,” ups.com Target connected voice-enabled chat with Google Assistant and Amazon Alexa, attributing 8% of Q4 2024 online grocery revenue to smart-speaker transactions. PCI-DSS obligations still apply when payment data flows through bots, prompting enterprises to wrap card-handling dialog in tokenization layers.

Growing Preference for Voice-First Interfaces

Voice-assistant and IVR traffic is predicted to outpace text channels, reflecting the growing demand for hands-free convenience and accessibility. Mercedes-Benz outfitted its 2024 models with a generative MBUX assistant for in-vehicle navigation and climate control. The US hospital pilots at Cleveland Clinic cut emergency-department walk-ins by 18% through phone-based symptom collection bots. Edge-based speech processing keeps data local and reduces latency, a critical factor in Germany and France, where data-sovereignty rules restrict outbound traffic. Noise and accent variance remain technical challenges, but sub-200 millisecond response targets are now feasible on-device for major languages.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy-by-Design Obligations (GDPR/CPRA) | -3.8% | Europe (GDPR) and California (CPRA), with spillover to other U.S. states adopting similar laws | Medium term (2-4 years) |

| High Switching Costs for Brown-Field IT Landscapes | -2.6% | Global, particularly acute in North American enterprises with legacy CRM and ERP systems | Long term (≥ 4 years) |

| LLM Hallucination Risk in Regulated Verticals | -4.2% | North America and Europe, concentrated in BFSI, healthcare, and insurance sectors | Short term (≤ 2 years) |

| Scarcity of Domain-Specific Training Datasets | -2.1% | Global, with greater impact in niche verticals (industrial, specialty insurance, legal) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy-by-Design Obligations (GDPR/CPRA)

GDPR fines exceeded EUR 2.1 billion in 2024, with several sanctions tied to inadequate consent procedures for chatbots. Compliance requirements, such as explicit user permission and the right to deletion, as well as local data processing, are driving European buyers toward private or sovereign clouds, which can increase infrastructure costs by up to 40%. California’s CPRA expands the definition of sensitive data, restricting the functionality of bots used in healthcare and banking unless encryption or tokenization is implemented. Vendors that bundle ISO 27701 privacy certifications into contracts gain an edge with risk-averse clients.

LLM Hallucination Risk in Regulated Verticals

Air Canada’s obligation to honor a chatbot’s inaccurate bereavement fare in 2024 established a legal precedent that brands own the output of their AI. US banking regulators now require pre-deployment validation of chatbot answers, which can extend project timelines by up to six months. The FDA guidance classifies symptom triage bots under Class II medical device rules when they influence treatment decisions, triggering premarket filings and clinical evaluations. Retrieval-augmented generation and human-in-the-loop overrides mitigate risk but erode some cost savings that initially justified automation.

Segment Analysis

By Enterprise Size: SMEs Narrow the Gap While Large Enterprises Retain Scale Advantage

Large enterprises generated 68.20% of their revenue in 2024 through multi-year transformation budgets and hybrid architectures that blend rule-based flows for compliance with generative AI for open-ended queries. However, SMEs are expected to register a 32.45% CAGR over the forecast period. SMEs already account for roughly one-third of conversational AI revenue, despite resource constraints, underscoring pent-up demand.

Canada disbursed CAD 87 million (USD 64 million) in 2024, and Germany’s Digital Now program earmarked EUR 120 million (USD 130 million) for SMB digitization. The chatbot market size for SMEs is poised to climb sharply as cloud subscriptions eliminate hardware capital outlays. However, SME churn remains higher because integrating bots with legacy point-of-sale or inventory software can be complex. European SMEs also navigate GDPR without large compliance teams, although sovereign-cloud vendors now bundle privacy toolkits to ease the burden.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Vertical: Healthcare Surges Ahead of BFSI in Growth

The BFSI segment led revenue growth at 27.60% in 2024, leveraging chatbots for fraud alerts, balance checks, and claim status updates to reduce call-center volume. Bank of America’s Erica surpassed 2 billion chats in 2024, handling bill payments and spending insights for retail clients. Yet, healthcare is forecast to grow faster, at a 33.12% CAGR, propelled by context-aware bots that triage symptoms and manage chronic disease reminders. Mayo Clinic reported a 29% drop in nurse triage calls after deploying a generative assistant in 2024.

Retail segment, where Sephora’s bot contributed 11% of online sales by guiding product discovery. The IT, telecom, travel, and hospitality segments round out the landscape, utilizing bots for network troubleshooting or making booking changes. Marriott’s WhatsApp concierge handled 3.8 million guest inquiries in 2024, with 82% of room-service orders placed via chat. Compliance frameworks such as HIPAA and PCI-DSS elevate barriers to entry, but they also protect incumbent vendors that achieve certification.

By Architecture: Generative AI Moves from Novelty to Necessity

Rule-based and NLU bots accounted for 55.12% of deployments in 2024, as compliance teams trust deterministic flows that guarantee every answer appears on an audit report. Still, generative-AI bots will grow at a 33.41% CAGR as retrieval-augmented grounding reduces hallucinations to below the 2% error threshold tolerated by most regulators. Customers accept a cent-per-query premium when the bot can troubleshoot a router or explain an insurance rider in plain English, rather than sending them to a PDF link.

Hybrid routing has become the house standard. Zendesk logs show 54% of enterprise clients funnel password resets to a USD 0.001 rule-based script while offloading product-comparison questions to a generative model that costs 30-50 times more per turn but closes sales that would otherwise stall. Industry consortia are easing data bottlenecks by pooling sanitized chat logs, an approach that finally provides niche sectors, such as industrial valves and marine insurance, with the corpus they need to train domain-aware models without triggering antitrust concerns in Brussels.

By Deployment Model: Cloud Thrives, Sovereign Variants Gain Political Tailwind

Cloud deployments accounted for 72.43% of 2024 spending, as CIOs prefer elastic usage meters and quarterly feature drops that are released without change-freeze windows. For retailers, this enables rapid scaling of operations during the holiday season and subsequent downsizing in January, with costs incurred only for the queries processed. European banks, on the other hand, adhere to strict data sovereignty requirements. For example, Deutsche Bank utilizes IBM Watson on a private cloud hosted in Germany, ensuring compliance with BaFin regulations while leveraging IBM’s natural language processing capabilities for German idioms and regulatory terminology. Furthermore, sovereign cloud providers like OVHcloud and IONOS prominently display their “GDPR native” certifications, which resonate strongly with procurement teams compared to traditional presentations on data encryption.

The hybrid model offers a balanced approach between these two paradigms. For instance, Red Hat OpenShift enables hospitals to route data inference to the public cloud while retaining chat logs on-premises to meet HIPAA compliance requirements. This approach reduces GPU costs while maintaining data privacy. However, cloud solutions are not universally optimal. Parcel-tracking bots, which handle millions of daily calls, sometimes revert to on-premises systems when egress fees exceed the costs of server depreciation. This highlights the adaptability of deployment models as pricing structures evolve.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Communication Channel: Voice Interfaces Surge as Web and Mobile Mature

In 2024, web and mobile apps led communication-channel revenue with 43.79%, driven by dominance in e-commerce, banking, and SaaS platforms. Their interfaces simplify workflows, such as bookings and product configurations. Social media and messaging platforms, including WhatsApp Business and Telegram, captured 28% of revenue due to asynchronous communication. Gupshup processed 10 billion monthly messages in 2024, primarily on WhatsApp, serving retail, banking, and healthcare in North America and Europe. Voice assistants and IVR integrations are projected to grow at a 33.98% CAGR through 2030 as enterprises adopt AI-driven speech recognition.

In-product widgets and SDKs enable SaaS vendors to embed chatbots, thereby reducing context switching and improving user retention. Drift’s platform generated 1.2 million qualified leads in 2024 by engaging website visitors in real time. Fragmented communication channels complicate integration, requiring consistent flows, branding, and data synchronization across platforms. Omnichannel orchestration platforms, such as Zendesk and Genesys, address these challenges but increase costs with the addition of more channels. Voice channels often face issues such as accent variability, noise, and limited language support, particularly in multilingual European markets. Edge-based speech processing offers solutions to address latency and privacy concerns, but lags behind server-side models in accuracy.

Geography Analysis

North America retained 61.80% of 2024 revenue, as US Fortune 500 budgets converged with a deep venture capital pool that funds every layer, from foundational models to no-code builders. California, New York, and Texas house the lion’s share of install bases, owing to tech headquarters, dense retail footprints, and healthcare networks willing to beta-test AI triage. Privacy laws, such as CPRA, do sting, but the same rules also push companies toward bots that automate consent capture far better than human agents reading scripts. Canada punches above its weight; federal grants totalling CAD 87 million bankrolled SME chatbots, and Toronto’s Ada Support raised USD 130 million to sell no-code bots to SaaS help desks across the continent.

Europe, although smaller today, is catching up at a 32.87% CAGR because GDPR fines have made manual data handling expensive and nudged enterprises toward privacy-by-design automation. London’s fintech player, Barclays’ virtual assistant, deflected 64% of 2024 call volume, freeing staff for mortgage advice that lifts fee income. Germany's manufacturing sector couples with AI-driven after-sales service; Mercedes-Benz pipes spare-parts queries into the same generative engine that powers in-car voice, anchoring the chatbot market size to both hard goods and software. France relies on sovereign clouds for every workload involving citizen data, sidelining U.S. hyperscalers in segments such as energy utilities and municipal services.

Southern and Eastern Europe are later adopters, but show a sharp inflection as EU Recovery and Resilience funds earmark digital spending. Italy digitized public-sector portals in 2024, enabling citizens to query their pension status via chat instead of waiting in line at municipal counters, a shift that reduced wait times and scored political points ahead of regional elections. Nordic nations steer the voice boom; near-universal smartphone penetration and long winter commutes make hands-free services attractive, so banks in Sweden now route loan-balance questions through Alexa skills in Swedish and English. Across the continent, sovereign-cloud mandates and multilingual requirements are driving vendors to invest in localized inference stacks and broader language models, indicating that by 2028, Europe could command up to 45% of the combined revenue.

Competitive Landscape

The chatbot market in North America and Europe resembles a spectrum. Hyperscalers like Microsoft, Google, and IBM dominate one end by bundling conversational AI into enterprise solutions. Microsoft’s Copilot Studio, included in Microsoft 365 E5, expands its user base and secures customer loyalty. Google integrates Dialogflow tokens into Vertex AI, offering volume discounts, while IBM secures compliance-driven deals by utilizing industry-specific libraries in banking and healthcare.

Open-source and niche players focus on specialization. Rasa offers European banks a Git-based pipeline to ensure data sovereignty in accordance with the GDPR. Cognigy, backed by USD 100 million, targets telecom and airline self-service with legacy IVR integration kits. Nuance leads the healthcare dictation market with Dragon Medical, processing 2.7 billion voice interactions and holding FDA-approved credentials.

Startups occupy the other end, exploring edge inference and multimodal chat. Ada enables e-commerce merchants to deploy Shopify-native bots within a day, while Personetics helps banks automate savings using behavioral science. In 2024, Google, Microsoft, and IBM filed 47, 39, and 28 multimodal chatbot patents, respectively, focusing on the integration of text, voice, and image. With the top five vendors holding a significant market share, low switching costs drive competition and rapid innovation.

North America And Europe Chatbot Industry Leaders

Microsoft Corporation

IBM Corporation

Google LLC (Alphabet Inc.)

Zendesk, Inc.

Nuance Communications, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Microsoft expanded Azure AI Foundry with sector-specific chatbot templates that cut deployment from 12 weeks to four and embed HIPAA, PCI-DSS, and GDPR controls.

- June 2024: Cognigy closed a USD 100 million Series C round led by Insight Partners to scale its conversational-AI platform across banking, insurance, and telecom sectors.

- March 2024: Zendesk acquired Ultimate.ai for USD 140 million, adding multilingual generative-chatbot capability across 109 languages and strengthening its European footprint.

North America And Europe Chatbot Market Report Scope

The North America and Europe Chatbot Market Report is Segmented by Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-user Vertical (Retail, BFSI, Healthcare, IT and Telecom, Travel and Hospitality, Other Verticals), Architecture (Rule-based/NLU Chatbots, Generative-AI Chatbots, Hybrid Architectures), Deployment Model (Cloud-based, On-premise/Private Cloud), Communication Channel (Web and Mobile Apps, Social-Media/Messaging Apps, Voice Assistants and IVR, In-product Widgets/SDKs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Vertical

| Retail |

| BFSI |

| Healthcare |

| IT and Telecom |

| Travel and Hospitality |

| Other Verticals |

By Architecture

| Rule-Based/NLU Chatbots |

| Generative-AI Chatbots |

| Hybrid Architectures |

By Deployment Model

| Cloud-based |

| On-Premise/Private Cloud |

By Communication Channel

| Web and Mobile Apps |

| Social-Media/Messaging Apps |

| Voice Assistants and IVR |

| In-Product Widgets/SDKs |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe |

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Vertical | Retail | |

| BFSI | ||

| Healthcare | ||

| IT and Telecom | ||

| Travel and Hospitality | ||

| Other Verticals | ||

| By Architecture | Rule-Based/NLU Chatbots | |

| Generative-AI Chatbots | ||

| Hybrid Architectures | ||

| By Deployment Model | Cloud-based | |

| On-Premise/Private Cloud | ||

| By Communication Channel | Web and Mobile Apps | |

| Social-Media/Messaging Apps | ||

| Voice Assistants and IVR | ||

| In-Product Widgets/SDKs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is the North America and Europe chatbot market expected to grow?

The region is projected to post a 31.95% CAGR between 2025 and 2030, taking value from USD 8.44 billion to USD 33.76 billion.

Which enterprise segment is expanding the quickest?

Small and medium enterprises lead growth with a forecast 32.45% CAGR through 2030, aided by no-code platforms and falling LLM costs.

Which vertical shows the highest future growth?

Healthcare is set to rise at 33.12% CAGR as context-aware triage and chronic-disease monitoring drive adoption in hospitals and clinics.

What deployment model dominates current spending?

Cloud-based deployment captured 72.43% of 2024 revenue due to its elasticity and quicker time to value, though sovereign clouds are rising in Europe.

Why are voice-first interfaces gaining traction?

Voice assistants and IVR bots offer hands-free convenience, meet accessibility standards, and are forecast to grow at 33.98% CAGR through 2030.

What is the main regulatory hurdle in Europe?

GDPR’s data-privacy-by-design mandate increases infrastructure costs by up to 40% when chatbots process personal data, pushing many firms toward private or sovereign clouds.