Market Overview

| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 332.4 Million |

| Market Size (2030) | USD 414.7 Million |

| Growth Rate (2025 - 2030) | 4.53% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Alfalfa Seed Market Analysis

The North America Alfalfa Seed Market size is estimated at 332.4 million USD in 2025, and is expected to reach 414.7 million USD by 2030, growing at a CAGR of 4.53% during the forecast period (2025-2030).

The North American alfalfa seed industry is experiencing significant transformation driven by evolving agricultural practices and technological advancements. The sector has established itself as a crucial component of the broader agricultural landscape, with alfalfa accounting for 15.7% of the total forage seed market in 2022. This prominence is largely attributed to the increasing integration of advanced breeding techniques and the growing adoption of precision farming methods. The industry has witnessed substantial investments in research and development, particularly in developing varieties with enhanced nutritional profiles and improved stress tolerance. Agricultural technology companies are increasingly focusing on developing innovative solutions to optimize alfalfa seed production and improve crop yields.

The livestock and dairy sectors continue to be the primary demand drivers for alfalfa seeds, with the crop serving as a vital source of protein-rich feed. In Canada, alfalfa constitutes approximately 60% of the beef cattle diet and 40% of the dairy cattle diet, highlighting its significance in animal nutrition. The industry has seen notable government support, exemplified by the Canadian government's USD 2.6 million investment in 2022 to equip alfalfa growers with advanced technologies. This investment reflects the growing recognition of alfalfa's importance in sustainable agriculture and its role in supporting the livestock industry's growth.

The export market has emerged as a significant growth avenue for the North American alfalfa seed industry. The United States has established itself as a major exporter of alfalfa hay, with export values reaching USD 55.5 million in 2022 to key markets including Saudi Arabia, Mexico, Algeria, Argentina, and Libya. This international trade expansion has encouraged seed producers to develop varieties that meet diverse climatic conditions and quality standards. The industry has also witnessed increased collaboration between seed companies and agricultural research institutions to develop varieties that can withstand various environmental stresses while maintaining optimal nutritional content.

Technological innovation and sustainable farming practices are reshaping the industry landscape. The cultivation area under alfalfa reached 11.5 million hectares in 2022, reflecting the sector's robust growth and adaptation to modern agricultural demands. Seed companies are increasingly focusing on developing varieties with wider adaptability traits, which accounted for 75.7% of the transgenic alfalfa seed market in 2022. This trend indicates a growing emphasis on creating resilient varieties that can thrive across different geographical regions and weather conditions. The industry is also witnessing increased adoption of digital farming technologies and precision agriculture techniques to optimize seed production and improve crop management efficiency.

North America Alfalfa Seed Market Trends

Rising cattle populations, growing demand from the processed forage industry and government support, are leading to an increase in the cultivation area

- Alfalfa is one of the major crops cultivated in countries such as the United States and Canada due to the high demand from the feed processing industry to feed livestock, especially cattle. To meet this high demand for alfalfa-based feed, the area cultivated for alfalfa was 11.5 million hectares in 2022, which increased by 5.5% during 2017-2022. The crop accounted for 30% of the area used for the cultivation of forage crops in the region in 2022.

- With an increase of 1.9% from 2017 to 2022 in North America's ruminant population, the number of buffaloes and cattle rose from 155.1 million to 158.6 million during the same period, which led to an increase in the demand for alfalfa and the area harvested in the region. Alfalfa is largely cultivated in Canada, with an area of 5 million ha in 2022, and the country had a regional area share of 93% in the same year. The area under alfalfa cultivation increased by 33% during 2017-2022 due to the increasing investments and support from the Canadian government to increase the production of feed for the livestock industry. The area cultivated increased by 1.4% in the United States during 2021-2022 due to increased demand for high protein in animal feed and its important role in biological nitrogen fixation and improving the soil content.

- Due to the increasing livestock population and rising demand for dairy products, the cultivation area has been increasing. Government support and its important role in a high-protein diet for animals are the factors that may increase the area under cultivation for alfalfa during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

The adoption of disease-resistant, insect-resistant, and drought-resistant alfalfa seeds for high yield during adverse climatic conditions is rising

- Alfalfa is a major forage crop cultivated in North America. The high-demand traits of alfalfa are disease resistance, insect resistance, and wider adaptability for improving the quality of the feed/silage for the livestock industry. Wider adaptability was the largest trait adopted by growers as there have been changes in weather conditions and demand for high yields with early maturity. Furthermore, other traits such as increasing protein content, growing throughout the seasons, and reducing lignin content are expected to gain popularity in the future, increasing forage quality.

- Popular traits of Alfalfa include disease resistance to wilts and root rots, wider adaptability to different seasons and soil conditions, drought tolerance, and resistance to insects and nematodes. For instance, major companies offering and marketing the traits of alfalfa varieties are Ampac Seed Company (Attention II), KWS SAAT SE & Co. KGaG (HarvXtra, Standfast), Bayer Crop Science (Roundup-Ready), Syngenta AG (NEXGROW), and DLF (Fortune) for resistance to diseases such as Colletotrichum trifolii and Verticillium wilt.

- Drought tolerance is the second-most popular trait among growers, as states such as Nebraska, Kansas, Oklahoma, Texas, New Mexico, and Oregon have been experiencing severe drought since 2022. About 12% of the land in these states was experiencing extreme drought in 2023. Therefore, the drought-tolerant trait is expected to gain popularity during the forecast period.

- Factors such as the increased demand for improving animal feed and a large number of benefits such as resistance to diseases and increasing yield are expected to drive the market's growth in the region.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Hybrid breeding dominates the market due to better yields and nutritional content

Segment Analysis: By Breeding Technology

Hybrids Segment in North America Alfalfa Seed Market

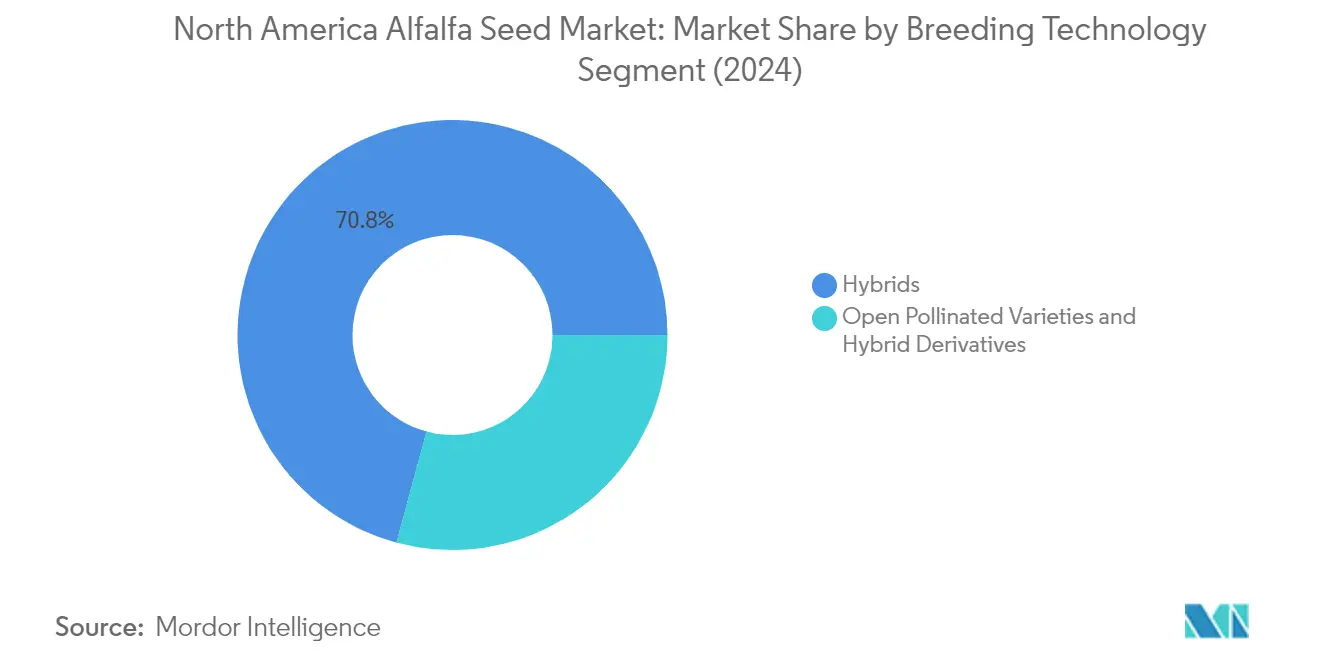

The hybrid alfalfa seed segment dominates the North American alfalfa seed market, accounting for approximately 71% of the market value in 2024. This significant market share is driven by the high adoption of both transgenic and non-transgenic hybrid varieties by farmers across the region. The segment's dominance can be attributed to hybrids' superior characteristics, including higher yields, better disease resistance, and wider adaptability to different climatic conditions. Non-transgenic hybrid alfalfa seed particularly holds a strong position in Canada, where farmers are increasingly adopting these varieties to provide chemical-free feed to cattle. Additionally, the segment is experiencing the fastest growth in the market, projected to grow at around 5% through 2029, driven by continuous innovation in breeding technologies and increasing demand for high-protein animal feed from the expanding dairy industries in regions like Idaho, New Mexico, and California.

Remaining Segments in Breeding Technology

The open pollinated varieties (OPV) and hybrid derivatives segment represents a significant portion of the North American alfalfa seed market, serving as an important alternative to hybrid varieties. This segment is particularly strong in Canada, where it maintains a substantial presence due to the affordability of OPVs and their advantage in restoring soil vigor through nitrogen fixation, making them an excellent choice for rotational cropping systems. The segment continues to maintain its relevance in the market due to growing demand for organic alfalfa seed from the dairy industry and increasing concerns about animal health with GM feeds cultivated from transgenic hybrids. Mexico's alfalfa seed market has shown particular interest in OPVs, driven by efforts to reduce dependence on imported hybrids and potential restrictions on GMO cultivation.

North America Alfalfa Seed Market Geography Segment Analysis

North America Alfalfa Seed Market in Canada

Canada dominates the North American alfalfa seed market, commanding approximately 68% of the total market value in 2024. The country's leadership position is primarily attributed to its extensive agricultural infrastructure and favorable weather conditions for alfalfa cultivation. The major alfalfa-producing regions include Saskatchewan, Manitoba, and Alberta, where optimal soil conditions and climate patterns support robust seed production. The government's proactive approach in supporting alfalfa cultivation through various initiatives and technological advancements has significantly strengthened the country's position. Canadian farmers have increasingly adopted advanced farming techniques and high-quality seed varieties, particularly focusing on varieties that offer superior winter survival rates. The country's strong focus on research and development in alfalfa breeding has resulted in varieties specifically adapted to local growing conditions. Additionally, the integration of sustainable farming practices and the growing emphasis on organic alfalfa seed production methods have further enhanced Canada's competitive advantage in the alfalfa seed market.

North America Alfalfa Seed Market in United States

The United States is positioned as the most dynamic market in the North American alfalfa seed sector, with projections indicating a robust growth rate of approximately 6% from 2024 to 2029. The country's alfalfa seed market is characterized by its strong emphasis on technological innovation and advanced breeding techniques. The adoption of genetically modified varieties and the integration of precision agriculture practices have revolutionized alfalfa seed production in the country. American farmers have shown increasing preference for high-yielding hybrid varieties that offer enhanced disease resistance and improved forage quality. The country's robust research infrastructure, supported by both public and private institutions, continues to drive innovation in seed development. The strong linkage between research institutions and commercial seed producers has facilitated rapid commercialization of new varieties. Furthermore, the growing focus on sustainable agriculture and environmental stewardship has led to the development of drought-resistant and climate-resilient alfalfa varieties, positioning the United States at the forefront of agricultural innovation.

North America Alfalfa Seed Market in Mexico

Mexico has established itself as a significant player in the North American alfalfa seed market, with major production concentrated in states like Chihuahua, Hidalgo, Guanajuato, Durango, and Baja California. The country's diverse climatic conditions and agricultural landscapes provide unique advantages for alfalfa seed production. Mexican farmers have increasingly adopted modern farming techniques and improved seed varieties to enhance productivity and quality. The country's agricultural sector has shown remarkable resilience and adaptability, particularly in addressing challenges related to water management and soil conditions. The integration of traditional farming knowledge with modern agricultural practices has created a unique approach to alfalfa cultivation. Mexico's strategic geographical location and trade relationships have facilitated both domestic market growth and export opportunities. The country's focus on developing region-specific varieties adapted to local conditions has strengthened its position in the market. Additionally, the growing awareness among farmers about optimal harvest cycles and improved cultivation practices has contributed to the market's development.

North America Alfalfa Seed Market in Other Countries

The remaining North American countries, including Costa Rica, Cuba, Panama, Guatemala, and Nicaragua, collectively represent an emerging segment in the alfalfa seed market. These countries are characterized by their diverse agricultural practices and varying climatic conditions, which influence alfalfa seed production and consumption patterns. The agricultural sectors in these nations are gradually modernizing, with increasing adoption of improved farming techniques and better-quality seed varieties. Local farmers are showing growing interest in alfalfa cultivation, particularly due to its importance in livestock feed production. The development of region-specific cultivation practices and the adaptation of seed varieties to local conditions have been key focus areas. These countries are also benefiting from knowledge transfer and technological assistance from more established markets in the region. The increasing awareness about the benefits of quality alfalfa seeds and improved agricultural practices continues to drive market development in these nations. Furthermore, the growing emphasis on sustainable agriculture and food security has created new opportunities for market expansion in these countries.

Get Analysis on Important Geographic Markets

Download PDF

North America Alfalfa Seed Industry Overview

Top Companies in North America Alfalfa Seed Market

The North American alfalfa seed market features several established players focusing on continuous innovation and strategic expansion. Companies are actively investing in research and development to create new seed varieties with enhanced traits such as disease resistance, drought tolerance, and wider adaptability. Product development efforts are particularly concentrated on creating hybrid alfalfa seed and transgenic varieties that offer higher yields and better nutritional content for livestock feed. Strategic partnerships and collaborations with research institutions and universities have become increasingly common to accelerate innovation in breeding technologies. Companies are also expanding their distribution networks and strengthening their market presence through mergers and acquisitions, particularly targeting smaller regional players with established grower relationships. The industry has seen significant investment in biotechnology and advanced breeding techniques, with major players maintaining dedicated research facilities across different geographical locations to develop region-specific varieties.

Consolidated Market Led By Global Players

The North American alfalfa seed market demonstrates a fairly consolidated structure dominated by large multinational agricultural companies with diverse product portfolios. These major players possess significant advantages through their established research capabilities, extensive distribution networks, and strong brand recognition in the agricultural sector. The market features a mix of global agricultural conglomerates and specialized seed companies, with the larger players leveraging their integrated operations from breeding to distribution. The competitive landscape is characterized by high barriers to entry due to the substantial investments required in research and development, regulatory compliance, and establishment of seed production infrastructure.

The market has witnessed considerable merger and acquisition activity, particularly involving larger companies acquiring smaller regional players to expand their geographical presence and product offerings. These strategic moves have further consolidated the market position of leading players while providing them access to local expertise and established grower networks. Companies are increasingly focusing on vertical integration strategies to maintain better control over their supply chains and ensure consistent product quality. The presence of regional players remains significant in specific geographical areas where they maintain strong relationships with local farmers and understand specific regional requirements.

Innovation and Adaptation Drive Market Success

Success in the North American alfalfa seed market increasingly depends on companies' ability to develop innovative products that address specific regional challenges and changing climate conditions. Market leaders are strengthening their positions by investing in advanced breeding technologies, expanding their trait portfolios, and developing varieties that offer improved performance under various environmental conditions. Companies need to maintain strong relationships with farmers through comprehensive technical support and education programs while ensuring efficient distribution networks. The ability to navigate complex regulatory requirements for new variety approvals, particularly for transgenic seeds, has become a crucial factor for maintaining market competitiveness.

For emerging players and market contenders, success lies in identifying and serving specific market niches or geographical regions where larger players may have limited presence. Companies can gain ground by focusing on specialized varieties adapted to local conditions or by offering superior customer service and technical support to farmers. Building strong relationships with research institutions and participating in collaborative breeding programs can help smaller players access advanced technologies and develop competitive products. The increasing focus on sustainable agriculture and organic farming also presents opportunities for companies to develop specialized seed varieties catering to these growing market segments. Additionally, companies need to maintain flexibility in their operations to respond to changing weather patterns and evolving farmer preferences while ensuring compliance with regional regulatory requirements.

North America Alfalfa Seed Market Leaders

-

Bayer AG

-

Corteva Agriscience

-

DLF

-

KWS SAAT SE & Co. KGaA

-

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

North America Alfalfa Seed Market News

- December 2022: S&W Seed acquired DuPont’s Pioneer Alfalfa seed business for USD 42 million. As part of the acquisition, S&W will acquire more than 15 DuPont Pioneer alfalfa seed varieties in the market today and more than 60 varieties in the development pipeline.

- October 2021: Bayer launched an organic vegetable seeds portfolio, enabling greater access to certified organic markets in Canada, the United States, Mexico, Spain, and Italy. The initial product offering focused on key crops for the greenhouse and glasshouse markets.

- November 2020: S&W Seed Company entered an agreement with Calyxt Inc., headquartered in Roseville, to identify a novel, proprietary trait for improved forage quality in commercial alfalfa seed production.

Free With This Report

We provide a complimentary and exhaustive set of data points on regional and country-level metrics that present the fundamental structure of the industry. Presented in the form of 90+ free charts, the section covers difficult-to-find data from various regions regarding the area under cultivation for different crops within the scope

List of Tables & Figures

- Figure 1:

- AREA UNDER CULTIVATION OF ALFALFA, HECTARE, NORTH AMERICA, 2017-2022

- Figure 2:

- VALUE SHARE OF MAJOR ALFALFA TRAITS, %, NORTH AMERICA, 2022

- Figure 3:

- VALUE SHARE OF ALFALFA BREEDING TECHNIQUES, %, NORTH AMERICA, 2022

- Figure 4:

- VOLUME OF ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 5:

- VALUE OF ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 6:

- VOLUME OF ALFALFA SEED BY BREEDING TECHNOLOGY CATEGORIES, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 7:

- VALUE OF ALFALFA SEED BY BREEDING TECHNOLOGY CATEGORIES, USD, NORTH AMERICA, 2017 - 2030

- Figure 8:

- VOLUME SHARE OF ALFALFA SEED BY BREEDING TECHNOLOGY CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 9:

- VALUE SHARE OF ALFALFA SEED BY BREEDING TECHNOLOGY CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 10:

- VOLUME OF ALFALFA SEED BY HYBRIDS CATEGORIES, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 11:

- VALUE OF ALFALFA SEED BY HYBRIDS CATEGORIES, USD, NORTH AMERICA, 2017 - 2030

- Figure 12:

- VOLUME SHARE OF ALFALFA SEED BY HYBRIDS CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 13:

- VALUE SHARE OF ALFALFA SEED BY HYBRIDS CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 14:

- VOLUME OF NON-TRANSGENIC HYBRIDS ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 15:

- VALUE OF NON-TRANSGENIC HYBRIDS ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 16:

- VALUE SHARE OF NON-TRANSGENIC HYBRIDS ALFALFA SEED BY COUNTRY, %, NORTH AMERICA, 2023 AND 2030

- Figure 17:

- VOLUME OF ALFALFA SEED BY TRANSGENIC HYBRIDS CATEGORIES, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 18:

- VALUE OF ALFALFA SEED BY TRANSGENIC HYBRIDS CATEGORIES, USD, NORTH AMERICA, 2017 - 2030

- Figure 19:

- VOLUME SHARE OF ALFALFA SEED BY TRANSGENIC HYBRIDS CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 20:

- VALUE SHARE OF ALFALFA SEED BY TRANSGENIC HYBRIDS CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 21:

- VOLUME OF HERBICIDE TOLERANT HYBRIDS ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 22:

- VALUE OF HERBICIDE TOLERANT HYBRIDS ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 23:

- VALUE SHARE OF HERBICIDE TOLERANT HYBRIDS ALFALFA SEED BY COUNTRY, %, NORTH AMERICA, 2023 AND 2030

- Figure 24:

- VOLUME OF OTHER TRAITS ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 25:

- VALUE OF OTHER TRAITS ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 26:

- VALUE SHARE OF OTHER TRAITS ALFALFA SEED BY COUNTRY, %, NORTH AMERICA, 2023 AND 2030

- Figure 27:

- VOLUME OF OPEN POLLINATED VARIETIES & HYBRID DERIVATIVES ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 28:

- VALUE OF OPEN POLLINATED VARIETIES & HYBRID DERIVATIVES ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 29:

- VALUE SHARE OF OPEN POLLINATED VARIETIES & HYBRID DERIVATIVES ALFALFA SEED BY COUNTRY, %, NORTH AMERICA, 2023 AND 2030

- Figure 30:

- VOLUME OF ALFALFA SEED BY COUNTRY, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 31:

- VALUE OF ALFALFA SEED BY COUNTRY, USD, NORTH AMERICA, 2017 - 2030

- Figure 32:

- VOLUME SHARE OF ALFALFA SEED BY COUNTRY, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 33:

- VALUE SHARE OF ALFALFA SEED BY COUNTRY, %, NORTH AMERICA, 2017 VS 2023 VS 2030

- Figure 34:

- VOLUME OF CANADA ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 35:

- VALUE OF CANADA ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 36:

- VALUE SHARE OF CANADA ALFALFA SEED BY BREEDING TECHNOLOGY, %, NORTH AMERICA, 2023 AND 2030

- Figure 37:

- VOLUME OF MEXICO ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 38:

- VALUE OF MEXICO ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 39:

- VALUE SHARE OF MEXICO ALFALFA SEED BY BREEDING TECHNOLOGY, %, NORTH AMERICA, 2023 AND 2030

- Figure 40:

- VOLUME OF UNITED STATES ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 41:

- VALUE OF UNITED STATES ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 42:

- VALUE SHARE OF UNITED STATES ALFALFA SEED BY BREEDING TECHNOLOGY, %, NORTH AMERICA, 2023 AND 2030

- Figure 43:

- VOLUME OF REST OF NORTH AMERICA ALFALFA SEED, METRIC TON, NORTH AMERICA, 2017 - 2030

- Figure 44:

- VALUE OF REST OF NORTH AMERICA ALFALFA SEED, USD, NORTH AMERICA, 2017 - 2030

- Figure 45:

- VALUE SHARE OF REST OF NORTH AMERICA ALFALFA SEED BY BREEDING TECHNOLOGY, %, NORTH AMERICA, 2023 AND 2030

- Figure 46:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, COUNT, NORTH AMERICA, 2017-2023

- Figure 47:

- MOST ADOPTED STRATEGIES, COUNT, NORTH AMERICA, 2017-2023

- Figure 48:

- VALUE SHARE OF MAJOR PLAYERS, %, NORTH AMERICA

North America Alfalfa Seed Industry Segmentation

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Canada, Mexico, United States are covered as segments by Country.| Breeding Technology | Hybrids | Non-Transgenic Hybrids | ||

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |||

| Other Traits | ||||

| Open Pollinated Varieties & Hybrid Derivatives | ||||

| Country | Canada | |||

| Mexico | ||||

| United States | ||||

| Rest of North America | ||||

Breeding Technology

| Hybrids | Non-Transgenic Hybrids | ||

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Other Traits | |||

| Open Pollinated Varieties & Hybrid Derivatives | |||

Country

| Canada |

| Mexico |

| United States |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF