Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

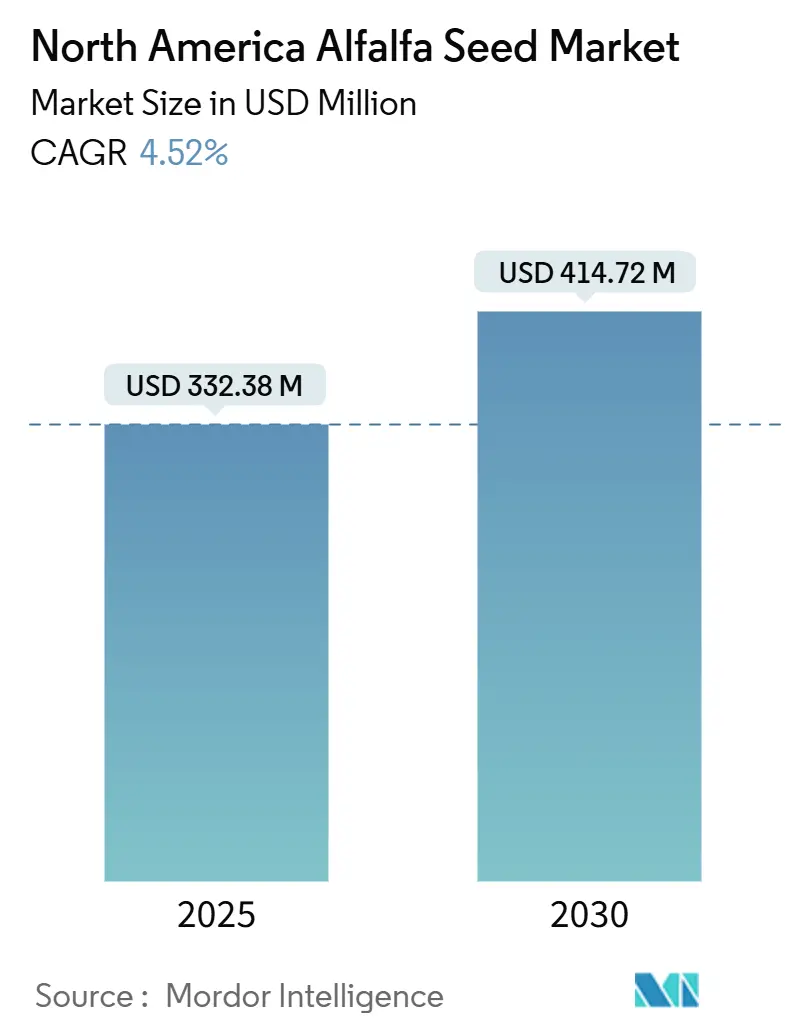

| Market Size (2025) | USD 332.38 Million |

| Market Size (2030) | USD 414.72 Million |

| Growth Rate (2025 - 2030) | 4.52% CAGR |

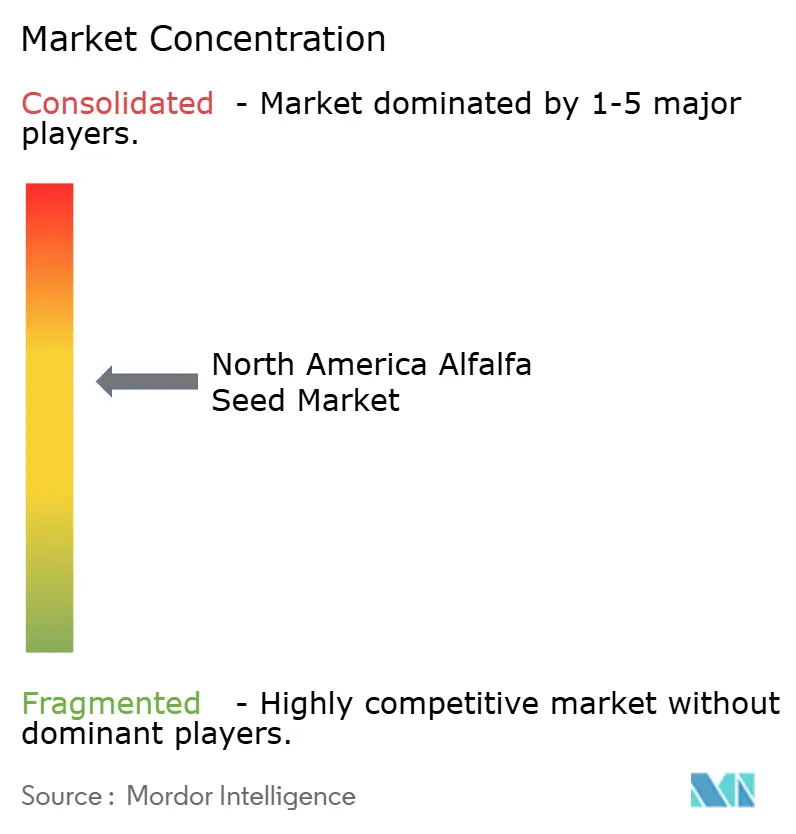

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Alfalfa Seed Market Analysis by Mordor Intelligence

The North America alfalfa seed market size stands at USD 332.38 million in 2025 and is projected to reach USD 414.72 million by 2030, registering a 4.52% CAGR. Strong dairy‐sector demand, rapid adoption of biotechnology traits, and climate resilience incentives underpin this expansion. Hybrid varieties increasingly dominate varietal choices as producers seek higher yields, stress tolerance, and streamlined crop management. Government programs that subsidize water-efficient genetics accelerate uptake in drought-prone areas, while precision agriculture tools optimize seeding rates and reduce input costs. Trade linkages among the United States, Canada, and Mexico foster a unified marketplace that rewards certified seed with documented trait performance.

Key Report Takeaways

- By breeding technology, hybrid varieties captured 70.8% of the North America alfalfa seed market share in 2024; while the same segment is projected to advance at a 5.03% CAGR through 2030.

- By country, Canada accounted for 68.0% of the North America alfalfa seed market size in 2024, while the United States is forecast to grow at a 6.16% CAGR through 2030.

North America Alfalfa Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust dairy-sector demand sustains seed replacement cycle | +1.2% | United States and Canada | Medium term (2-4 years) |

| Regulatory fast-tracking of biotech low-lignin traits | +0.8% | United States and Canada | Short term (≤ 2 years) |

| Climate-resilience programs subsidizing salt- and drought-tolerant varieties | +0.6% | Western United States and Prairie Provinces | Long term (≥ 4 years) |

| Precision-ag adoption boosting optimal seeding-rate prescriptions | +0.4% | North America | Medium term (2-4 years) |

| Soil-carbon credit schemes rewarding alfalfa rotations | +0.3% | United States and Canada | Long term (≥ 4 years) |

| U.S.–Mexico hay-export bio-security norms raising certified-seed use | +0.2% | United States and Mexico border regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Dairy-Sector Demand Sustains Seed Replacement Cycle

Milk production gains keep the North America alfalfa seed market on a predictable replacement schedule, as forage quality directly affects feed conversion ratios and profitability. High-protein content positions alfalfa as an essential component of total mixed rations, so producers prioritize certified seed with proven digestibility and stand life. Research at the University of California, Davis confirms alfalfa as the highest protein-yielding crop per acre in the United States[1]Source: UC Davis Department of Plant Sciences, “Alfalfa Field Day Research Highlights,” ucdavis.edu. Consolidation among dairy farms favors operations that evaluate genetic value rigorously, which supports premium pricing for hybrids that deliver consistent forage characteristics. The standard four-to-six-year replacement period assures recurrent demand cycles that seed companies can forecast accurately. This stability encourages ongoing breeding investment and rapid varietal turnover that keeps performance standards rising.

Regulatory Fast-Tracking of Biotech Low-Lignin Traits

United States Department of Agriculture (USDA), Animal and Plant Health Inspection Service (APHIS) streamlined approval processes shorten commercialization timelines for low-lignin events such as J101, J163, and KK179, enabling seed companies to capture early-mover advantages[2]Source: National Institute of Food and Agriculture, “Generation of Alfalfa Plants with Optimized Lignin Biosynthesis,” usda.gov. Faster approvals cut regulatory costs and improve return on R&D, which accelerates trait stacking strategies that combine herbicide tolerance with enhanced digestibility. These innovations reduce enteric methane emissions, aligning with corporate sustainability targets across dairy supply chains. The result is a premium segment within the North America alfalfa seed market where producers pay for proven feed efficiency and environmental benefits. Swift regulatory pathways also spur competitive pressure as firms rush to launch second-generation traits that push digestibility gains beyond current benchmarks.

Climate-Resilience Programs Subsidizing Salt- and Drought-Tolerant Varieties

Federal and state incentives lower the cost barrier for adopting varieties that maintain yield under moisture stress, thereby broadening the addressable acreage for improved genetics. The USDA Water-Saving Commodities Program earmarked USD 400 million for irrigation-efficiency projects that list drought-tolerant seed as an eligible practice. Prairie Provinces add matching funds for salt-tolerant lines that thrive in secondary salinization zones. Universities such as New Mexico State are developing deeper-rooted cultivars that enter protective dormancy in extended dry spells, a feature that appeals to western hay producers facing water-allocation cuts. Subsidies encourage growers to shift capital toward premium seed while shortening payback periods, which sustains demand even during commodity-price downturns.

Precision-Ag Adoption Boosting Optimal Seeding-Rate Prescriptions

Variable-rate technology lets producers tailor seeding density to soil variability, cutting wastage and improving stand uniformity. Government Accountability Office (GAO) data show that adoption of seeding rate VRT (Variable Rate Technology) climbed to 25.3% of planted acres by 2023[3]Source: U.S. Government Accountability Office, “Precision Agriculture Benefits and Challenges,” gao.gov. Satellite and Unmanned Aerial Vehicle (UAV) imagery guide zone mapping that supports prescription maps for alfalfa establishment. Seed firms bundle agronomic services with variety packages to demonstrate superior returns, reinforcing customer loyalty. As sensor costs fall, smaller farms now access analytics once reserved for large enterprises, widening the market for premium genetics calibrated to precision management.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seed-trait royalty inflation is squeezing grower ROI (Return on Investment) | -0.9% | North America | Short term (≤ 2 years) |

| Tight Western US irrigation quotas are limiting acreage | -0.7% | Western United States | Medium term (2-4 years) |

| Adventitious-presence tolerance tightening for non-GMO hay exports | -0.4% | United States and Canada | Short term (≤ 2 years) |

| Pollinator-shortage risk in Pacific Northwest seed valleys | -0.3% | Pacific Northwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seed-Trait Royalty Inflation Squeezing Grower ROI

Layered royalty structures for stacked traits drive seed prices beyond the comfort zone of cost-sensitive operators. Smaller farms with limited bargaining power struggle to pass higher costs downstream, especially when milk prices soften. Some growers downgrade to open-pollinated lines despite lower yield potential, thereby curbing revenue growth for technology providers. Seed companies respond with volume discounts and multi-year loyalty programs, yet price perceptions remain a headwind in the near term.

Tight Western-US Irrigation Quotas Limiting Acreage

Allocation cuts across districts in California, Arizona, and Idaho, force producers to fallow alfalfa stands or adopt partial-season deficit irrigation. Research in Idaho finds patchy crop water productivity, implying yield penalties if water is rationed uniformly. Alfalfa converts water to biomass efficiently, but in quota regimes, higher-value cash crops such as almonds often displace forage. This acreage squeeze dampens expansion prospects for the North America alfalfa seed market in water-scarce zones. Adoption of drought-tolerant genetics mitigates some losses but cannot fully offset land reallocation to more profitable crops.

Segment Analysis

By Breeding Technology: Hybrids Extend Performance Gap

Hybrid varieties held 70.8% of the North America alfalfa seed market share in 2024, while the same segment is projected to advance at a 5.03% CAGR through 2030. These gains reflect superior heterosis that translates into higher yields, improved pest tolerance, and longer stand life. The North America alfalfa seed market continued trait stacking, promising to raise value capture per acre. Seed developers complement genetic advances with vigor-rating indices that simplify variety selection for consultants and nutritionists.

Open-pollinated varieties and hybrid derivatives still serve cost-conscious segments and organic farms, yet growth remains modest. Their combined share of the North America alfalfa seed market size is forecast to drop below by 2030 as producers weigh the opportunity cost of lower biomass against rising land and water expenses. Even within this tier, improved lines incorporate marker-assisted selections that narrow the yield gap with full hybrids. The landscape, therefore, tilts toward technology-rich products that reward R&D investment and strengthen intellectual-property defenses.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Canada commanded 68.0% of the North America alfalfa seed market size in 2024, supported by Prairie Provinces with ideal seed-production climates. Cooperative networks streamline distribution, while the Canadian Food Inspection Agency maintains transparent variety registration that nurtures innovation. Producers in Alberta and Saskatchewan favor persistent varieties that endure severe winters, further entrenching certified seed demand.

The United States records the fastest expansion at a 6.16% CAGR through 2030 as climate resilience programs and precision agriculture investments unlock fresh demand. In the United States, geographic diversity yields contrasting market drivers. The Upper Midwest and Northeast enjoy abundant rainfall and proximity to large dairies, encouraging rapid turnover to low-lignin hybrids that amplify milk yields per ton of dry matter. Western states contend with irrigation quotas, sharpening interest in varieties bred for deficit regimes that maintain forage value under stress.

Mexico’s contribution to the North America alfalfa seed market is rising as livestock intensification lifts demand for high-protein forage. SENASICA’s updated phytosanitary code streamlines import permits for certified seed, while domestic multiplication under contract with United States and Canadian breeders builds local capacity. Northern states such as Chihuahua and Coahuila allocate irrigated acreage to seed crops that supply both domestic dairies and export hay presses. Exchange-rate shifts intermittently influence procurement, yet integrated supply chains mitigate volatility through multi-year contracts that lock in volumes and pricing.

Competitive Landscape

The market remains moderately fragmented. Leading firms maintain multiregional germplasm pools that speed up adaptive breeding and reduce time to market. Bayer recently reorganized field teams in Illinois and Wisconsin to deliver localized technical support, increasing customer retention in those high-volume territories. Smaller breeders thrive by specializing in drought-resilient and non-GMO lines that serve niche export contracts or organic dairies.

Strategic partnerships between seed companies and precision agriculture platforms embed seeding prescriptions into monitor displays, positioning preferred varieties as default options. Collaborations with input dealers expand reach into secondary regions where direct sales teams are thin. Licensing agreements for proprietary traits spread R&D costs across multiple brand portfolios, although royalty stacking drives the pricing controversy mentioned earlier.

Mergers and acquisitions target germplasm libraries rather than physical assets, reflecting the high value placed on intellectual property. The moderate concentration leaves room for start-ups anchored around Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR-based) gene editing, which promises targeted improvements without transgene status. The resulting competitive tension drives continuous variety refresh cycles that benefit growers through steady performance gains.

North America Alfalfa Seed Industry Leaders

Bayer AG

Corteva Agriscience

DLF

KWS SAAT SE & Co. KGaA

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2024: USDA Farm Service Agency launched the USD 400 million Water-Saving Commodities Program, providing grants to irrigation districts for water conservation practices that include incentives for drought-tolerant crop varieties. The program's estimated 50,000 acre-feet of water savings across 250,000 acres creates market opportunities for water-efficient alfalfa genetics.

- May 2024: Michigan State University launched a USD 5 million Agricultural Climate Resiliency Program with four projects addressing climate adaptation in plant agriculture, including field crop climate-resilient systems research that encompasses forage production optimization.

North America Alfalfa Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Canada, Mexico, United States are covered as segments by Country.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Country

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Country | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF