North America Alfalfa Market Analysis by Mordor Intelligence

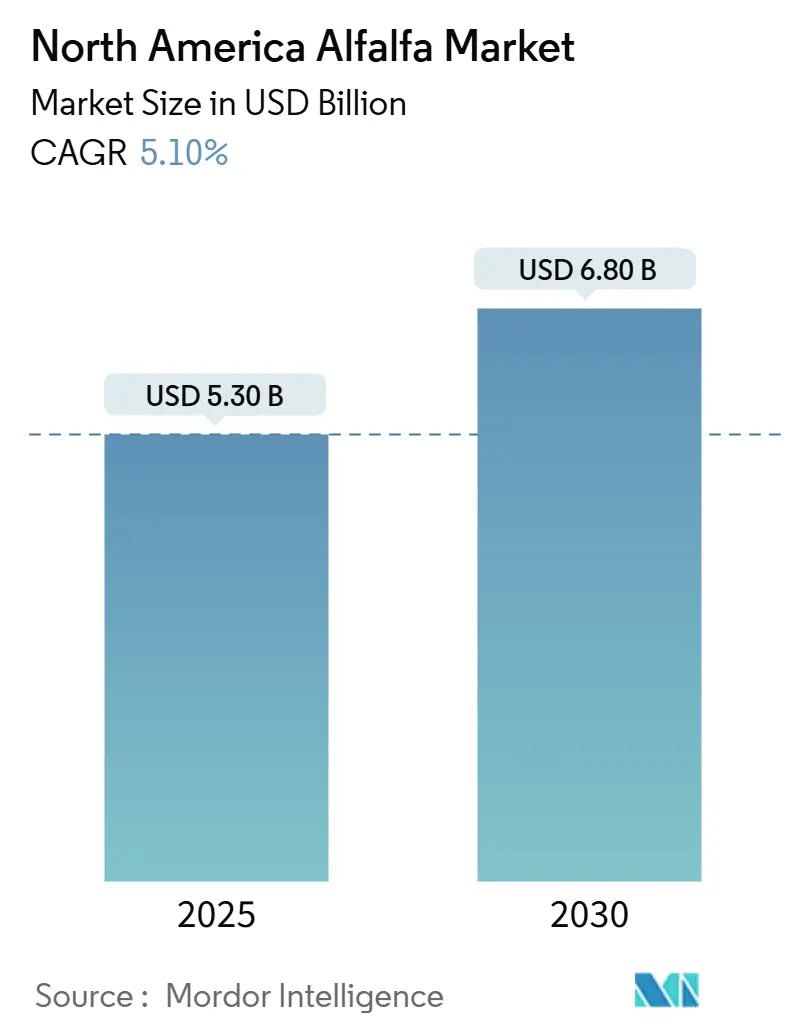

The North America alfalfa market size is valued at USD 5.3 billion in 2025 and is projected to reach USD 6.8 billion by 2030, advancing at a 5.10% compound annual growth rate (CAGR). Expanding dairy herd productivity, water-saving irrigation upgrades, and faster container port turnarounds along the United States' West Coast are widening demand–supply gaps that favor premium forage pricing. Elevated protein inclusion rates in dairy rations, the steady rise of organic and non-genetically modified organisms (GMOs) forage, and the renewed release of acreage from the Conservation Reserve Program (CRP) are supporting volume growth, even as currency strength and climate volatility introduce periodic shocks. Export flows continue to define competitive positioning within the North American alfalfa market, with Saudi Arabia, the United Arab Emirates, and Japan helping to offset the softness stemming from China’s dairy pullback. Against this backdrop, investments in precision irrigation and traceability systems are emerging as clear differentiators for growers and exporters determined to protect their margins in an environment of tightening groundwater regulations.

Key Report Takeaways

- By geography, the United States accounted for 85.0% of the North America alfalfa market share in 2024 for consumption, while Canada’s consumption is forecast to expand at a 6.9% CAGR between 2025 and 2030.

North America Alfalfa Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated dairy-sector protein demand | +1.2% | North America, with spillover to export markets in Middle East and Asia | Medium term (2-4 years) |

| Growing preference for non-GMO and organic forage | +0.6% | United States and Canada, limited adoption in Mexico | Long term (≥ 4 years) |

| Precision-irrigation reducing water use | +0.7% | Western United States (California, Idaho, Montana), emerging in Canada | Medium term (2-4 years) |

| United States west-coast export infrastructure upgrades | +0.8% | United States west coast, benefiting Middle East and Asian importers | Short term (≤ 2 years) |

| CRP (Conservation Reserve Program) expirations freeing western hay acres | +0.5% | United States Great Plains and Intermountain West | Medium term (2-4 years) |

| Saudi and United Arab Emirates forage-crop water bans boosting imports | +0.9% | Middle East (Saudi Arabia, UAE), sourcing from North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Dairy-Sector Protein Demand

Demand for digestible protein in dairy rations continues to anchor the North America alfalfa market. The United States dairy herd totaled 9.349 million head in January 2025, and federal projections show milk output climbing 9.1% through 2034[1]Source: United States Department of Agriculture Economic Research Service, “Dairy Cattle,” ers.usda.gov. Larger, higher-output herds require consistent supplies of neutral detergent fiber and protein-rich forage, both of which are supplied by premium alfalfa. In Canada, quota adjustments in Ontario and Quebec are triggering incremental forage demand, while Mexico’s 2.5 million-head herd is boosting imports of United States hay to improve milk solids. A price retreat to USD 195 per metric ton in April 2024 from USD 288 per metric ton a year earlier improved feed economics, encouraging higher inclusion rates. As land availability restricts local production in several dairy basins, alfalfa remains the preferred high-protein roughage, locking in long-term structural demand for the North America alfalfa market.

Growing Preference for Non-GMO and Organic Forage

Retailers reward dairies that source certified organic or non-genetically modified organism feed, a trend that adds value-added acreage despite a three-year transition burden. The 2021 Agricultural Census listed 238,000 acres of organic hay and haylage, a figure now estimated to be higher, given new conversions[2]Source: United States Department of Agriculture National Agricultural Statistics Service, “Milk Production,” nass.usda.gov. Organic alfalfa fetches 20–40% price premiums, offsetting lower yields and stricter weed-management costs. Canadian processors in British Columbia and Quebec are locking in multiyear contracts to secure compliant forage, and exporters report heightened interest from Japanese buyers. Although Mexico’s certification infrastructure remains nascent, premium pricing opportunities continue to drive acreage shifts in the United States' upper Midwest and Northeast. The trend supports margin expansion and helps differentiate shipments in the North American alfalfa market, although total organic volume still represents a modest share of the aggregate supply.

Precision-Irrigation Reducing Water Use

Sensor-driven irrigation systems are trimming water application by 10–15%, a crucial gain as aquifer depletion tightens allocations. Subsurface drip lines placed 30–45 centimeters deep in California’s Imperial and Central Valleys maximize root-zone moisture while curbing evaporation[3]Source: University of California Cooperative Extension, “Alfalfa Irrigation Management,” ucanr.edu. Soil-moisture probes and variable-rate pivots in Idaho and Montana mirror these savings. Install costs can exceed USD 1,500 per acre, yet rising water prices and Sustainable Groundwater Management Act mandates are strengthening return-on-investment calculations. Adoption unevenness persists, but field evidence of yield stability is encouraging broader uptake. Improved efficiency unlocks marginal acreage and stabilizes tonnage, directly underpinning growth projections for the North America alfalfa market.

United States West-Coast Export Infrastructure Upgrades

Container-handling expansions at the Ports of Los Angeles, Long Beach, Oakland, Seattle, and Tacoma have slashed dwell times, boosting compressed-hay throughput for Asian and Middle Eastern destinations. Ocean freight from the Pacific Northwest to Japan averaged USD 30.5 per metric ton in 2024, compared to USD 55.5 per metric ton from Gulf ports, reinforcing a geographic cost advantage. With Saudi Arabia and the United Arab Emirates scaling up imports, infrastructure gains are easing bottlenecks that once capped growth, solidifying the export channel’s contribution to the North America alfalfa market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chinese milk-price slump curbing import pull | -1.0% | China, with ripple effects on United States and Canadian export volumes | Medium term (2-4 years) |

| Strong United States dollar pressuring export margins | -0.8% | United States exporters, affecting competitiveness in Japan, South Korea, and other Asian markets | Short term (≤ 2 years) |

| Climate-induced yield volatility | -0.6% | Western United States (California, Idaho, Montana), sporadic impacts in Canada | Long term (≥ 4 years) |

| Growing availability of low-cost feed substitutes | -0.7% | North America, particularly in cost-sensitive dairy and beef operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong United States Dollar Pressuring Export Margins

The United States Dollar Index (DXY) hovered near 105–106 in 2024, widening landed-cost disparities for Japanese and South Korean buyers. Japan’s purchases dropped to 85% of their five-year average, with the yen’s weakness prompting government incentives for local forage cultivation. Competing supply from Australia and Canada, whose currencies had depreciated against the US dollar, intensified price competition. Unless interest-rate trends reverse, currency headwinds will continue to compress exporter margins in the North America alfalfa market.

Climate-Induced Yield Volatility

After the severe 2022–2023 drought, 2024 moisture improvements lifted on-farm stocks by 6%, yet temperature spikes and wildfire risks in California, Idaho, and Montana underline ongoing production fragility. Episodic weather shocks contribute to unpredictable supply swings, exposing growers and exporters locked into fixed-price contracts to margin erosion. The resulting uncertainty dampens investment appetite and injects risk into otherwise favorable growth projections for the North America alfalfa market.

Geography Analysis

The United States captured 85.0% of the consumption for the North America alfalfa market size, underlining its role as both the region’s largest producer and buyer, with dairy and beef operations absorbing nearly 52 million metric tons of hay. The United States dominates supply and demand, leveraging irrigated acreage in California, Idaho, Montana, and South Dakota. Improved 2024 moisture lifted stocks and moderated local prices, yet climate volatility remains a shadow risk. Precision irrigation uptake in California’s Imperial Valley and Idaho’s Snake River Plain is reducing water use by up to 15%, easing regulatory compliance under the Sustainable Groundwater Management Act and preserving yield stability critical to the North American alfalfa market.

Canada’s 6.9% CAGR underscores a clear export tilt, with prairie province producers capitalizing on currency softness and lower Pacific freight to gain footing in Asian markets. Larger farm sizes and mechanized operations enhance quality control, aligning shipments with the specifications of Japan and South Korea. Shorter growing seasons and limited irrigation constrain upside volumes; yet, consistent quality allows Canadian exporters to capture premium niches within the North American alfalfa market.

Mexico’s expanding middle-class appetite for dairy proteins raises alfalfa demand as herds cluster in Jalisco, Coahuila, Durango, and Chihuahua. Domestic supply lags due to scarce water, fragmented landholdings, and capital limitations. Rail network congestion forces importers to evaluate new logistics strategies, including container shipments from west-coast United States ports. Price sensitivity leads many Mexican dairies to shift toward lower-grade hay or feed substitutes during alfalfa price spikes, but protein requirements keep a baseline import flow, reinforcing Mexico’s strategic importance to the North America alfalfa market.

Recent Industry Developments

- January 2025: The United States Department of Agriculture extended the authority of the Conservation Reserve Program until September 30, 2025. This maintains the 27 million-acre enrollment cap and supports grassland conservation with limited haying and grazing.

- November 2024: The University of Minnesota Extension reported that 2025 blister-beetle populations were 30 percent above 10-year averages, attributed to consecutive mild winters that improved overwintering survival. This suggests that contamination risk will persist in alfalfa hay through the forecast period, absent significant climate shifts.

- October 2024: The Bureau of Reclamation announced mandatory Colorado River Lower Basin water reductions of 1.033 million acre-feet, effective 2025. Arizona, Nevada, and California will absorb cuts based on priority rights, impacting alfalfa acreage in the Imperial Valley and Yuma, where the crop uses 32% of the basin's water and 62% of agricultural diversions. The policy is anticipated to idle 50,000 to 75,000 acres of alfalfa over two years, thereby tightening the supply and supporting prices.

North America Alfalfa Market Report Scope

The North America Alfalfa Market Report is Segmented by Geography (United States, Canada, and Mexico). The Study Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| United States |

| Canada |

| Mexico |

| By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America alfalfa market?

The market is valued at USD 5.3 billion in 2025 and is forecast to climb to USD 6.8 billion by 2030.

Which country leads consumption within North America?

The United States holds 85.0% of total regional consumption, driven by its large dairy and beef industries.

Why is Canada the fastest-growing geography in this sector?

Canada’s 6.9% CAGR is tied to expanding dairy herds under supply management and competitive export pricing to Asia.

How are precision-irrigation technologies influencing alfalfa production?

Subsurface drip and sensor-based scheduling cut water use by up to 15%, stabilizing yields and freeing acreage.

Which factors currently restrain export growth?

A strong United States dollar, lower Chinese dairy margins, and rising feed substitutes are compressing exporter margins.

Page last updated on: