Market Trends of North America Aircraft MRO Industry

Military Aviation Segment is Projected to Significant Growth During the Forecast Period

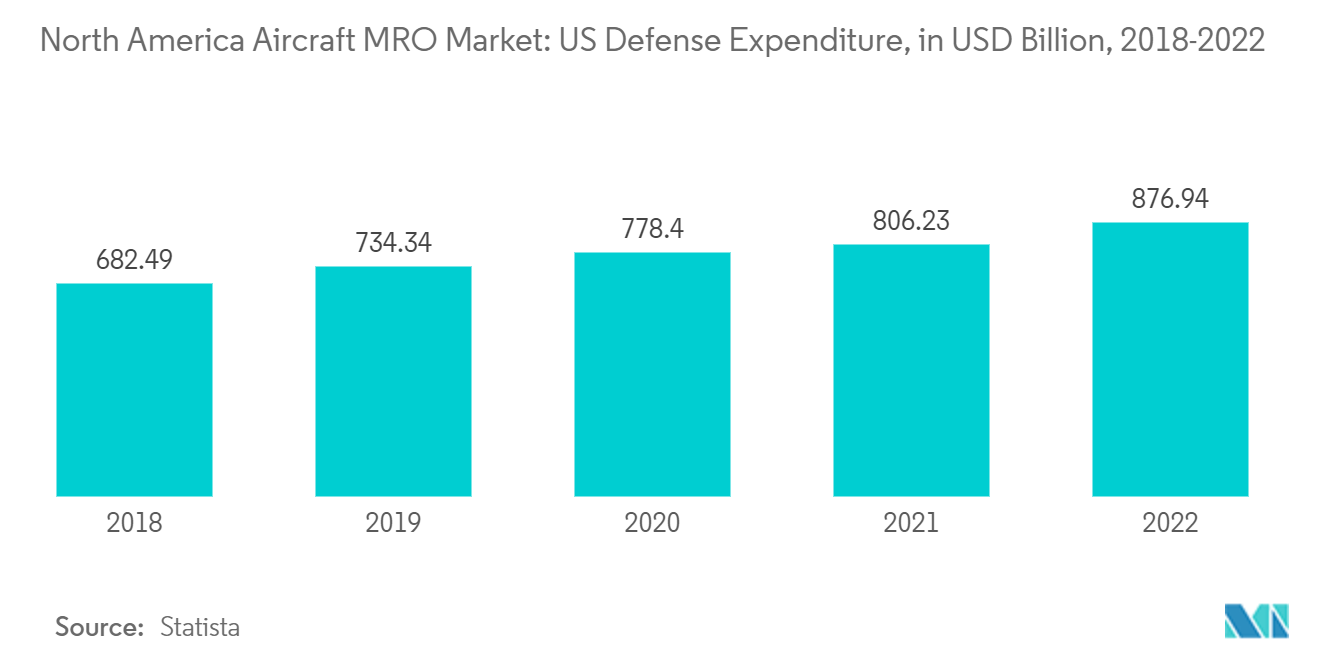

The military aviation segment will showcase remarkable growth during the forecast period. The growth is attributed to the increasing defense expenditure, rising procurement of next-generation military aircraft, and growing aircraft modernization programs from the US Air Force. The US Air Force’s logistics enterprise is building its first artificial intelligence-driven data system, called the Basing & Logistics Analytics Data Environment (BLADE). BLADE gathers information from more than 300 Air Force and broader Defense Department data sources. The US Air Force has expanded its artificial intelligence (AI)-powered predictive maintenance tools, called Condition-Based Maintenance Plus, to 16 of its aircraft fleets. Furthermore, Canada is also struggling with the aging fleet of its CF-18 fighter aircraft, which has reached the age of more than 33 years. A few aircraft in the Royal Canadian Air Force are too old to be upgraded with the latest equipment to comply with the latest air traffic and aviation rules. Also, In April 2023, GE Aerospace signed an agreement with Lockheed Martin Corporation to support avionics and electrical power systems on the F-35 military aircraft. Under the four-year agreement, the company will provide MRO services for GE Aerospace systems on the F-35 Lightning II aircraft. The company will service the F-35 systems at its repair and maintenance locations in California, Georgia, and Utah. Thus, growing procurement of fighter jets and rising expenditure on military aircraft modernization programs drive the growth of the market during the forecast period.

The United States is Estimated to Dominate the Market During the Forecast Period

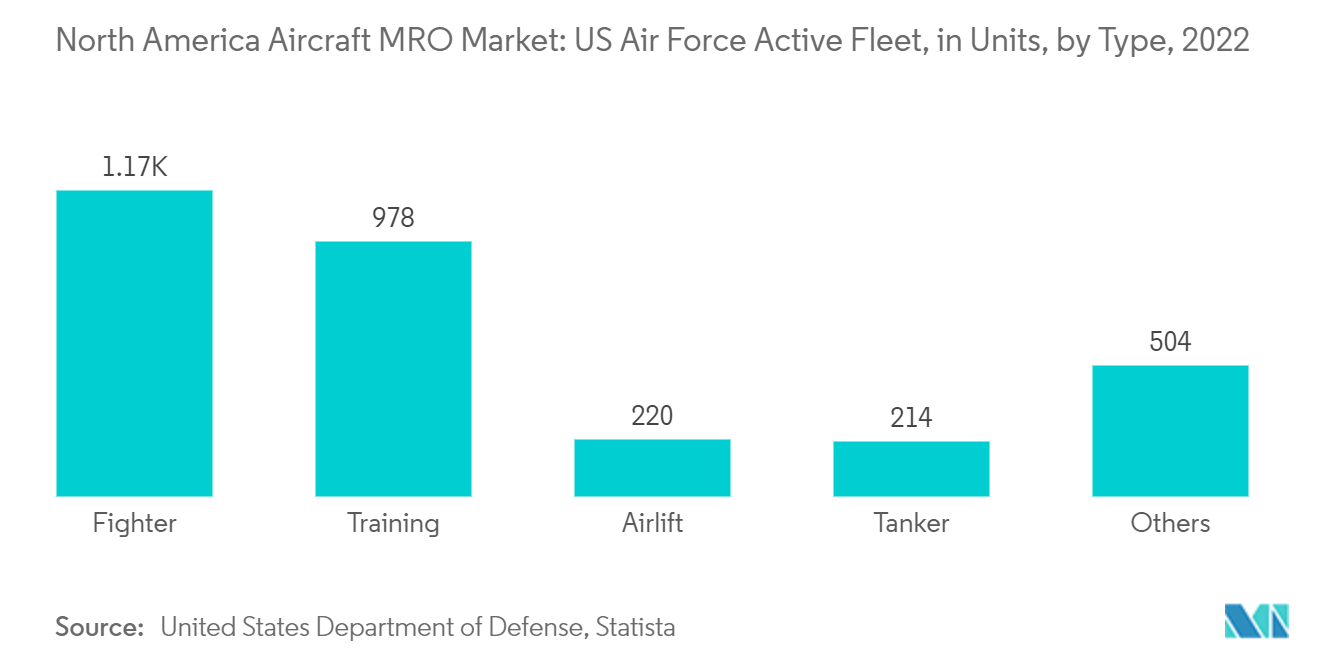

The US held the highest shares in the market and will continue its domination during the forecast period. The growth is due to the presence of the highest commercial and military aircraft fleet, the largest number of airports, and a large number of MRO service providers. The United States is the leading producer of commercial, defense, and general aviation aircraft. The increase in spending on aircraft development is further propelling the growth of the aircraft and aircraft MRO markets. The major driving factor for the MRO in this country is the significant demand to upgrade such a vast fleet with the latest technologies and systems. The US Department of Defense (DoD) plans to spend USD 61.1 billion on aircraft and related systems in 2024. The DoD plans to buy a diverse mix of 270 aircraft, ranging from nearly USD 700 million B-21 stealth bombers for the USAF to twin-engine King Air 200-derived trainers for the US Navy. The US DoD budget requests for FY2022 and FY2023 depot maintenance reached USD 32.6 and USD 35.1 billion, respectively. According to DoD, the FY2023 budget request would fund 50% of total executable Army depot maintenance requirements, 85% of Air Force requirements, 80% of Marine Corps requirements, 71% of Navy requirements, and 83% of Space Force requirements. The majority of the MRO expenditure is on the nation’s large fleet of multi-role aircraft, transport aircraft, and surveillance aircraft that require high maintenance on engines and airframes, along with field and component maintenance services. Thus, the increase in several aircraft acquisitions and the growing presence of aircraft engine MRO service providers within the United States will lead to a positive outlook and significant market growth during the forecast period.