Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

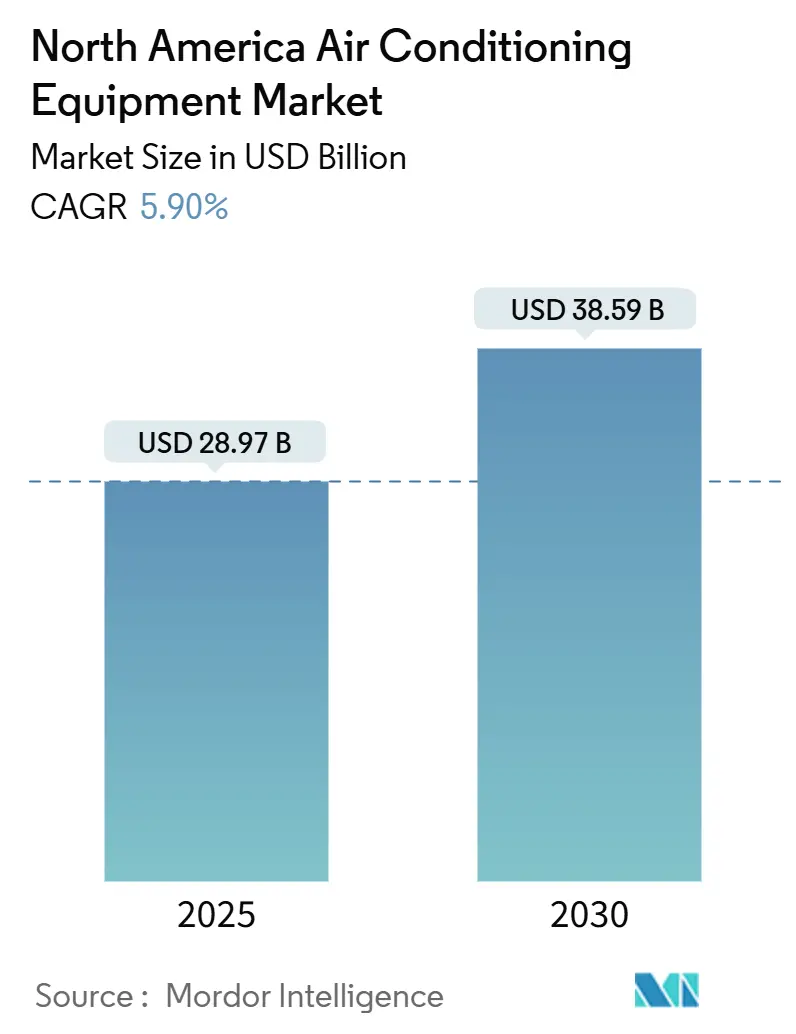

| Market Size (2025) | USD 28.97 Billion |

| Market Size (2030) | USD 38.59 Billion |

| Growth Rate (2025 - 2030) | 5.90% CAGR |

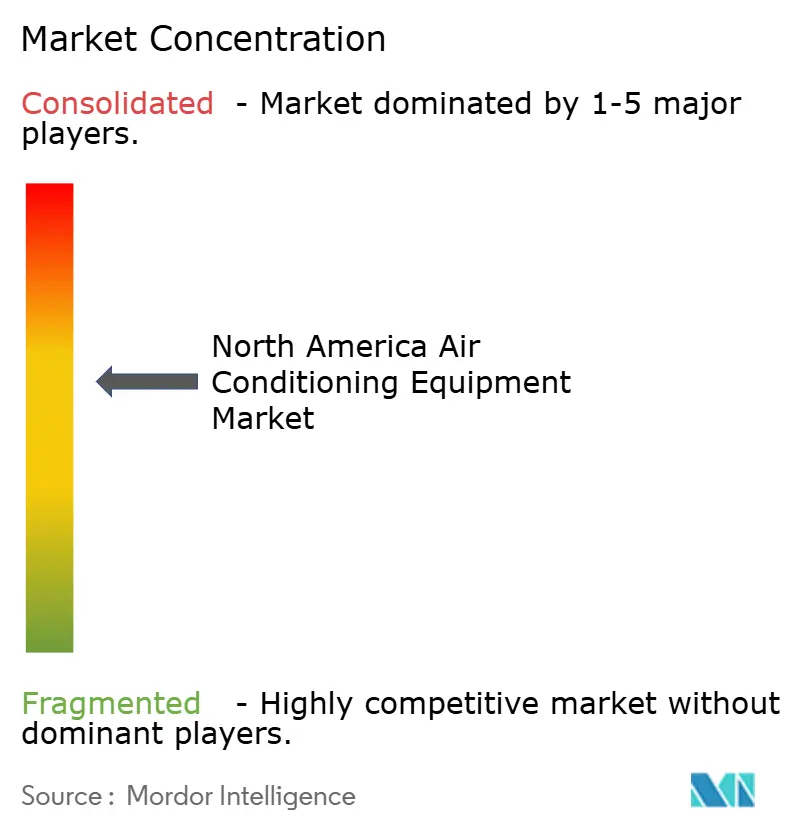

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Air Conditioning Equipment Market Analysis by Mordor Intelligence

The North America air conditioning equipment market size stood at USD 28.97 billion in 2025 and is forecast to reach USD 38.59 billion by 2030, advancing at a 5.9% CAGR over the period. Growing federal incentives, rapid smart‐home adoption, and rising extreme-heat events form a virtuous cycle that lifts replacement demand even as new construction ebbs in some geographies. OEMs that align product portfolios with A2L refrigerants and SEER2 requirements gain early-mover advantages because contractors increasingly bundle compliance, safety training, and connected-controls capabilities in a single sales proposition. Commercial building owners accelerate rooftop unit change-outs to capture energy savings and ventilation upgrades, while data-center operators deploy precision cooling that commands premium pricing. Supply shortages for skilled installers remain the primary speed bump, yet OEM investment in factory localization and technician training shields the North America air conditioning equipment market from prolonged disruption.

Key Report Takeaways

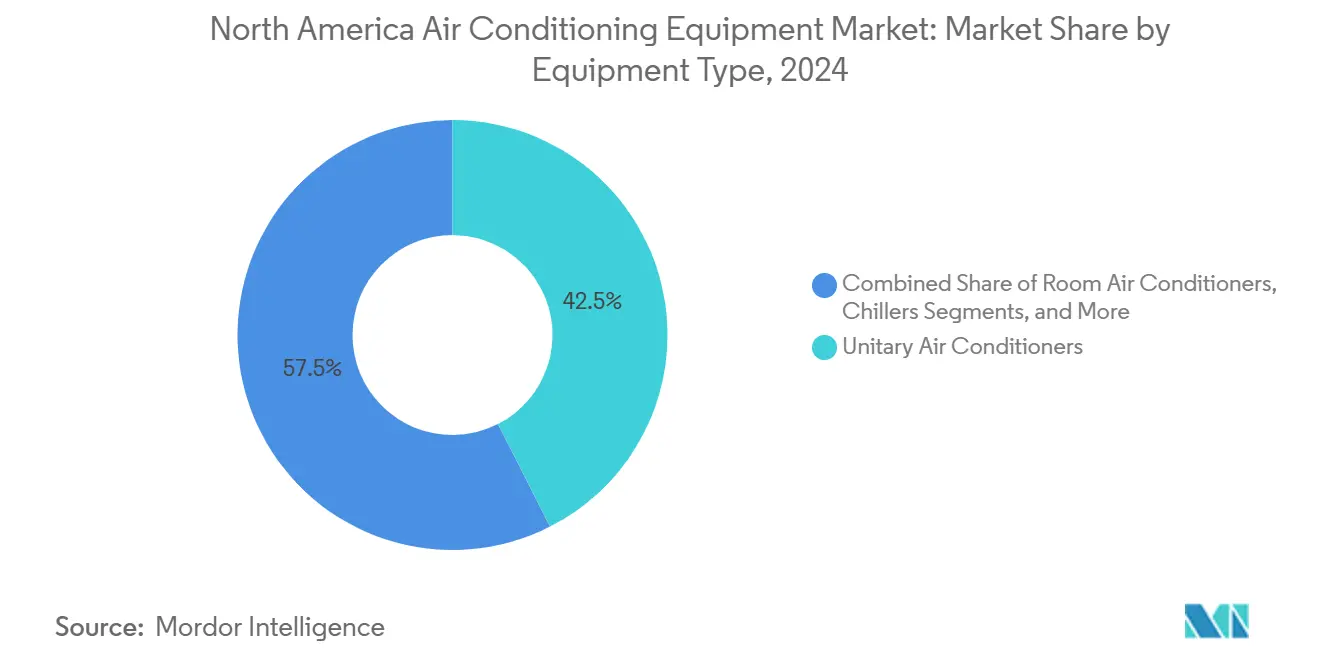

- By equipment type, unitary air conditioners led with 42.5% of the North America air conditioning equipment market share in 2024, while variable refrigerant flow systems are projected to log the fastest 7.3% CAGR through 2030.

- By Refrigerant type, R-410A led with 55.1% of the North America air conditioning equipment market share in 2024, while R-32 is set to expand at a 7.2% CAGR through 2030.

- By Capacity, 12,001–60,000 (1–5 Tons) led with a 50.5% of the North America air conditioning equipment market share in 2024, 12,001–60,000 (1–5 Tons) also led the segment with 7.0% CAGR through 2030.

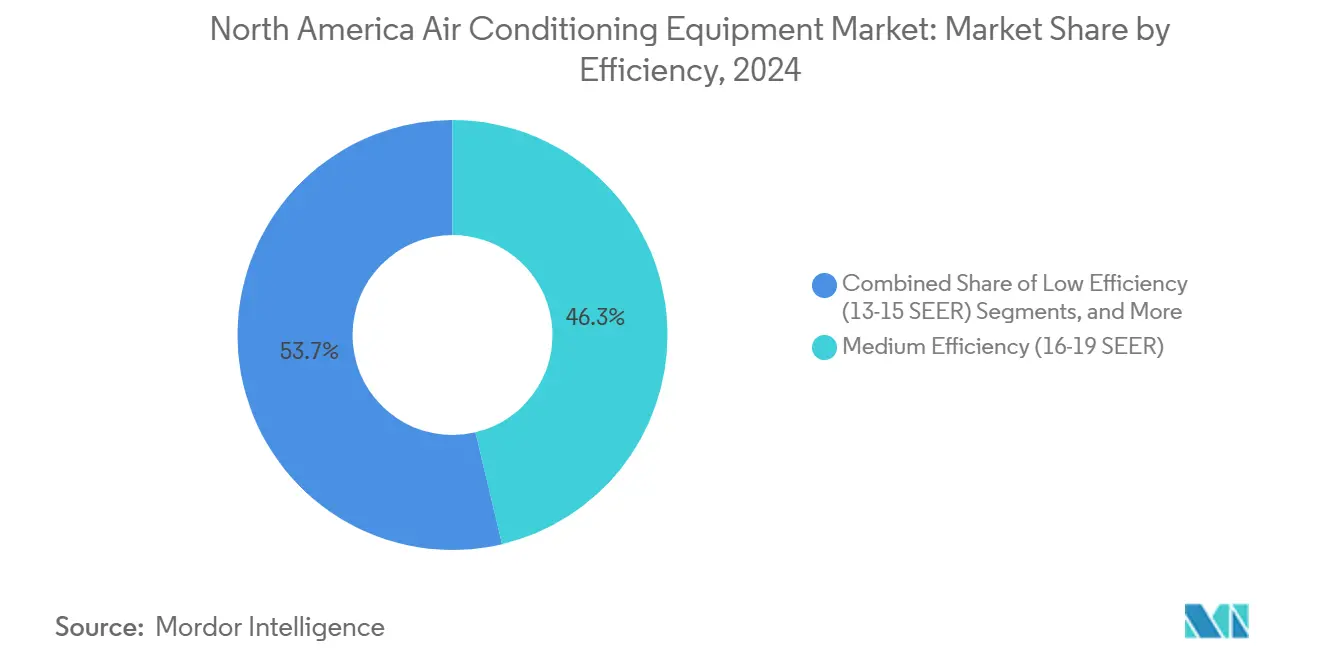

- By efficiency, the medium-efficiency segment held 46.3% of the North America air conditioning equipment market size in 2024, and the high-efficiency tier above 20 SEER is set to expand at a 6.6% CAGR to 2030.

- By end user, residential applications accounted for 58.0% of 2024 revenue; the industrial segment, propelled by data-center build-outs, will post the fastest 6.4% CAGR in the forecast window.

- By Installation type, replacement/retrofit accounted for 71.3% of 2024 revenue; the new construction, is set to expand at a 6.7% CAGR in the forecast window.

- By Sales channel, Direct (OEM-to-Contractor) accounted for 40.7% of 2024 revenue; the retail/e-commerce sector, is set to expand at a 6.5% CAGR in the forecast window.

- By country, the United States captured roughly 75% share in 2024; Canada is slated for a 6.5% CAGR through 2030 thanks to aligned efficiency codes and generous provincial rebates.

North America Air Conditioning Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tax-credit reinstatement and state-level rebate programs | +1.2% | United States, spillover to Canada | Medium term (2-4 years) |

| Replacement demand for aging rooftop units | +0.9% | Urban North America | Long term (≥ 4 years) |

| Rapid growth of smart-thermostat ecosystems | +0.7% | United States and Canada | Medium term (2-4 years) |

| Heat-pump incentives for reversible systems | +0.8% | Northern U.S. states and Canada | Long term (≥ 4 years) |

| Data-center cooling capacity additions | +0.6% | Virginia, Texas, California | Short term (≤ 2 years) |

| Extreme-heat events raising cooling-degree days | +0.5% | Southwestern North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tax-credit reinstatement and state-level rebate programs

Federal incentives under the Inflation Reduction Act grant households up to USD 2,000 in tax credits and as much as USD 8,000 in rebates for qualifying heat pumps, effectively erasing the price premium between entry-level and high-efficiency systems.[1]U.S. Department of the Treasury, “Heat Pumps Deliver Major Savings for American Families,” treasury.gov Contractors consequently up-sell 20 SEER-plus models that maximize rebates, while OEMs front-load inventory to high-population states such as California, New York, and Texas. Utility programs piggy-back on the federal architecture, stacking bill credits on top of tax relief and pulling forward replacement cycles. These overlapping incentives allocate demand toward the North America air conditioning equipment market segments that command higher margins and encourage factory re-tooling toward variable-speed compressors. Supply logistics tighten during midsummer peaks, but the policy certainty extending to 2032 provides OEMs with visibility to justify North American capacity expansions.

Replacement demand for aging rooftop units in commercial buildings

More than 15 million rooftop units cool roughly 60% of U.S. floor space, many now past optimum efficiency benchmarks. Building owners combine Section 179D tax deductions with paybacks from 5-15% energy savings to justify wholesale replacements rather than piecemeal repairs. COVID-19 drove a heightened focus on ventilation and filtration, pushing asset owners toward VRF and DOAS solutions that deliver better zone control and fresh-air ratios. As rooftop retrofits kick off, contractors integrate smart sensors for predictive maintenance, cementing long-term service agreements that anchor recurring revenue for OEM-affiliated service networks. The cascading effect boosts downstream demand for balance-of-system components such as economizers, ECM blower motors, and energy recovery ventilators.

Rapid growth of smart-thermostat and home-automation ecosystems

IoT-enabled thermostats allow grid-interactive pre-cooling strategies that shave peak loads by 13-28% in commercial buildings.[2]Stanford University, “Unlocking Demand Response in Commercial Buildings,” ssrn.com HVAC OEMs like Samsung embed proprietary software layers to secure recurring subscription income, while utilities compensate participants in demand-response programs. Predictive algorithms reduce service calls by flagging coil fouling and refrigerant losses, lengthening equipment life and lifting customer satisfaction scores. For consumers, the appeal extends beyond energy savings to indoor-air-quality visibility and voice-assistant integration, both of which now appear in more than 40% of premium models shipped in 2025. The North America air conditioning equipment market thus shifts from one-time equipment sales toward a hybrid hardware-as-a-service paradigm that favors scale players with cloud-engineering capabilities.

Heat-pump incentives shifting mix toward reversible systems

Cold-climate heat pumps that employ enhanced vapor injection maintain full heating output at −15 °F, enabling furnace displacement in the northern tier of states.[3]PR Newswire Asia, “GMCC & Welling Showcase at AHR Expo 2025,” prnasia.com Provincial rebates across Canada replicate U.S. tax credits, further tilting the installed base toward electrically driven solutions. OEMs deploy dual-fuel control logic that engages resistance coils only in extreme snaps, satisfying building-code electrification mandates without jeopardizing occupant comfort. The transition unlocks carbon savings, narrows gas-grid investments, and widens addressable demand for variable-speed compressors produced at Mitsubishi Electric’s new Kentucky facility.[4]Mitsubishi Electric, “Mitsubishi Electric to Establish Heat Pump Compressor Factory in the U.S.,” mitsubishielectric.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SEER2 and AWEF compliance cost pressures | −0.8% | United States and Canada | Short term (≤ 2 years) |

| Kigali Amendment phasedown of HFC refrigerants | −1.1% | Entire region | Medium term (2-4 years) |

| Electrical-grid congestion and demand-response penalties | −0.4% | Texas, California, Northeast | Medium term (2-4 years) |

| Skilled-labor shortages for HVAC installation | −0.6% | Rural and secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SEER2 and AWEF compliance cost pressures on OEM margins

DOE’s M1 procedure lowers nameplate ratings by roughly 4.1%, obliging manufacturers to re-engineer coils, fan-motor controls, and expansion valves. Component redesigns add USD 200-400 per residential unit, squeezing margins unless offset by price raises. Inventory segmentation across three DOE climate zones compounds working-capital needs, particularly painful for small regional brands. While leading OEMs amortize redesign costs across global platforms, smaller players risk exit or acquisition, intensifying consolidation within the North America air conditioning equipment market.

Kigali Amendment phasedown of HFC refrigerants

The AIM Act mandates an 85% reduction in HFC consumption by 2036, starting with a 40% production cut already in effect. OEMs migrate toward mildly flammable A2L refrigerants such as R-32 and R-454B, triggering the need for retooled compressors, thicker copper tubing, and onboard leak-detection electronics. Technicians must earn new certifications, with training costs escalating 20% for small contractors. Supply tightness for legacy R-410A inflates service prices, nudging hold-out consumers into early replacements yet creating short-term logistical headaches for distributors.

Segment Analysis

By Equipment Type: VRF Systems Accelerate Commercial Transformation

Unitary devices retained 42.5% of the North America air conditioning equipment market share in 2024, translating into a USD 12.3 billion slice of the overall North America air conditioning equipment market size. Commercial owners, however, pivot toward VRF architectures that expand at a 7.3% CAGR through 2030, seduced by 25-40% energy savings and precise zone control. VRF advantages compound as ASHRAE Standard 15 elevates ventilation requirements because decentralized indoor units allow individualized air treatment without oversizing central blowers. Mitsubishi Electric’s Kentucky compressor plant specifically targets variable-speed rotaries used in VRF, anchoring supply resilience during the A2L transition.

Second-order impacts ripple across the contractor base. Installers trained on brazing traditional split systems invest in specialized refrigerant recovery tools to handle R-32 VRF piping. OEMs incentivize early certification through warranty extensions, locking in brand loyalty. The ability to network VRF indoor units with building-automation platforms yields occupancy-based cooling schedules that trim operational expense, a convincing value proposition for property-management firms bidding on energy-performance contracts. These factors jointly reinforce VRF momentum inside the North America air conditioning equipment market even as unitary incumbents defend share through mid-tier price points and integrated smart-thermostat bundles.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Refrigerant Type: A2L Transition Reshapes Design Norms

Legacy R-410A systems still represented 55.1% of installed equipment in 2024, yet new-build permits already stipulate A2L designs in multiple jurisdictions, compressing the conversion timeline to just two cooling seasons. R-32 captures early VRF and ductless splits thanks to thermodynamic efficiencies that translate into 10% smaller heat-exchanger footprints, an advantage in height-constrained indoor units. R-454B rises in rooftop packaged units where drop-in viscosity profiles simplify coil scaling, allowing OEMs to minimize tooling expense during the changeover.

Safety code revisions, including UL 60335-2-40 4th Edition, mandate integrated leak sensors and automatic fan purge logic. The incremental bill of materials adds USD 300 per residential unit, but federal tax incentives offset half the premium for qualifying high-efficiency models. Distributors carry dual inventories through 2026 to service existing R-410A warranties, straining warehouse footprints and working capital, yet opening arbitrage margins for firms able to navigate mixed fleets. Insurance underwriters adjust liability clauses, nudging building owners to favor factory-sealed A2L equipment where risk scores improve.

By Capacity (BTU/hr): Mid-Range Systems Dominate Residential Demand

Systems between 12,001-60,000 BTU/hr encompass the canonical 2-4 ton split-system archetype and thus command nearly 50.5% of 2025 shipments. Larger commercial packaged units above 60,000 BTU/hr account for 26.2% of revenue but exhibit lumpy demand tied to cyclical construction patterns. Data-center chillers routinely exceed 500,000 BTU/hr yet appear under service contracts that smooth OEM revenue even in downturns. Rising cooling-degree days push homeowners to upsize capacities by 0.5 tons on average, but tighter building envelopes offset load growth. Variable-capacity inverters broaden viable ranges within a single chassis, reducing SKU proliferation for manufacturers and simplifying contractor stocking.

Climate variance within the region influences capacity mix; desert Southwest installs 5-ton units as standard, whereas maritime Northwest homes rely on 1-ton ductless splits for shoulder-season comfort. Heat-pump proliferation in Canada drives adoption of dual-stage 3-ton configurations optimized for heating dominance, an inversion of historical cooling-first load calculations. The result is a mosaic capacity curve that encourages flexible manufacturing lines capable of quick die-changeovers, a strategic advantage exploited by facilities in Monterrey and Maysville supplying the North America air conditioning equipment market.

By Efficiency (SEER Rating): High-Efficiency Tier Gains Velocity

Medium-efficiency (16-19 SEER) equipment retained 46.3% share in 2024 because price-sensitive mid-market consumers weigh first cost more heavily than lifetime operating expense. Yet high-efficiency models above 20 SEER register the fastest 6.6% CAGR, fueled by 30% federal tax credits and aggressive utility rebates pegged to ENERGY STAR 6.1 thresholds. Minimum-efficiency products shrink as SEER2 raises standards to what was previously considered mid-tier performance. OEMs invest in vapor-injection scroll compressors and redesigned coil geometries to recoup lost nameplate ratings under M1 testing, safeguarding price premiums.

Retailers such as Home Depot bundle smart thermostats and IAQ sensors with high-efficiency units, thereby amplifying perceived value while increasing the average transaction size. Over time, utility time-of-use pricing could elevate the elasticity difference between 18 SEER and 22 SEER models, propelling additional share shift toward the upper band. The North America air conditioning equipment market thus evolves into a barbell structure where ultrahigh-efficiency heat pumps coexist with cost-driven R-32 room ACs, leaving thin middle-tier volumes vulnerable.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Industrial Segment Emerges as Growth Leader

Residential sales deliver 58.0% of 2024 revenue, deriving stability from 12-15-year replacement cycles and ongoing suburban housing starts. Industrial applications expand at a 6.4% CAGR due to surging data-center and advanced-manufacturing investments, taking the North America air conditioning equipment market size for the industrial segment to an estimated USD 6.4 billion by 2030. Semiconductor fabs and battery plants require humidity and particulate control, pushing OEMs to integrate multi-stage filtration and desiccant wheels within package units. Cold-storage warehouses amplify refrigeration crossover, prompting OEMs to develop bi-temperature split systems that share components with standard comfort-cooling product lines.

Commercial buildings, offices, schools, and hospitals sustain 35% of revenue and gain incremental share through indoor-air-quality retrofits mandated by ASHRAE Std 241. VRF providers penetrate K-12 and higher-education campuses where phased renovations suit modular installation. Healthcare’s stringent infection-control standards fuel orders for high-MERV filters and UV-C sterilizers, elevating accessory attach rates and boosting overall margins.

By Installation Type: Replacement Dominates, New-Build Ups the Spec Bar

Replacements comprise roughly 71.3% of 2025 shipments, reflecting an aging installed base amid heightened energy-code stringency. Homeowners gravitate toward full-system overhauls rather than component swaps, especially when IAQ add-ons such as ERVs bundle seamlessly with new air handlers. Contractors exploit this trend to upsell duct upgrades and smart controls, fortifying recurring service coffers. New construction, while smaller in absolute volume, steers technological direction because builders select equipment early in project timelines, locking spec preferences for years. High-efficiency mandates in California Title 24 and Canada’s BC Step Code force builders to adopt 20 SEER-plus heat pumps in greenfield projects, influencing homeowner expectations region-wide.

Retro-commissioning in commercial settings represents a hybrid opportunity that blends replacement compressors with control-system recalibration, typically delivering 10-15% energy savings. Utilities fund measurement-and-verification studies, generating hard ROI figures that convince CFOs to green-light multi-site rollouts. As A2L refrigerant codes converge in 2025, building owners will time replacements to coincide with refrigerant changeovers, smoothing the demand curve for suppliers servicing the North America air conditioning equipment market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: Direct OEM-to-Contractor Path Gains Ground

E-commerce and factory-direct portals accelerate as OEMs chase margin and data visibility. Samsung’s acquisition of Quietside secures distribution for ductless lines, letting the brand control installer training and end-user engagement simultaneously. Large contractors appreciate reduced lead times and factory tech support, reciprocating with brand loyalty and exclusivity agreements. Distributors retain relevance for emergency inventory and credit financing; however, their share slips to an estimated 46% in 2025 from 53% five years earlier.

Retail big-box stores thrive at the DIY end of room-air-conditioner and PTAC categories but lose share in split-system kits now deemed too complex for self-install under A2L safety codes. Online marketplaces capture small parts and replacement filter sales, commoditizing low-value SKUs yet providing OEMs with data on consumption patterns that inform predictive inventory planning. The channel shake-up reshapes bargaining power within the North America air conditioning equipment market, rewarding brands that offer seamless digital configurators and real-time order tracking.

Geography Analysis

The United States anchors the North America air conditioning equipment market with an estimated USD 21.5 billion in 2025 revenue. Federal tax credits up to USD 2,000 for heat pumps tilt installations toward variable-speed technology, while Section 179D incentives catalyze rooftop unit replacements in office and retail complexes. SEER2 rules bifurcate inventories into three climate zones, complicating logistics yet boosting demand for high-end SKUs that clear mandated thresholds. Extreme-heat waves in Phoenix, Las Vegas, and Austin stretch grids, incentivizing utilities to offer demand-response payouts that embed smart-thermostat adoption into mainstream retrofit workflows.

Canada’s 2025 revenue approximates USD 4.3 billion, accelerated by provincial rebate programs that cover up to 30% of cold-climate heat-pump costs, effectively subsidizing the premium over baseline gas furnaces. CSA B52 alignment with U.S. efficiency standards simplifies cross-border OEM skus, allowing manufacturers to leverage economies of scale while meeting local frost-protection requirements. Quebec and Ontario collectively represent more than half of national demand, with multifamily construction in Toronto driving ductless deployments. Prairie provinces focus on hybrid dual-fuel systems where extended defrost cycles would otherwise hamper pure-electric performance.

Mexico contributes USD 2.9 billion in domestic sales while exporting significantly more under USMCA rules. Rising urbanization increases central-AC adoption in Monterrey and Mexico City; however, inverter mini-splits priced below USD 1,000 dominate volume. Government energy labelling educates consumers on lifetime operating costs, nudging share toward 18 SEER units. OEMs embed Wi-Fi modules to differentiate offerings, anticipating a future demand-response marketplace as Comisión Federal de Electricidad modernizes tariffs. The blend of local consumption growth and manufacturing expansion positions Mexico as both a demand node and supply linchpin within the North America air conditioning equipment market.

Competitive Landscape

Large incumbents consolidate share through vertical integration and technology alliances. Johnson Controls’ USD 8.1 billion divestiture of its residential portfolio to Bosch concentrates its focus on commercial and industrial segments, while Bosch gains immediate scale in North American retail and installer networks. Samsung Lennox capitalizes on SmartThings IoT assets to embed proprietary connectivity into ductless lines, differentiating on user experience rather than raw efficiency metrics.

Manufacturing localization gathers pace. Mitsubishi Electric’s USD 143.5 million Kentucky compressor plant comes online in 2027, cutting shipping lead times and currency risk. GMCC and Welling establishes a Dallas R&D hub to customize scroll compressors for U.S. voltage and humidity conditions, trimming design cycles and satisfying Buy-America provisions in federal procurement. Carrier teams with Google Cloud to deploy AI-powered energy-management analytics that overlay building automation, transforming the OEM-customer relationship into a continuous-optimization service.

Smaller regional brands confront higher compliance costs tied to SEER2 and A2L transitions. Some seek niche defensibility in coastal specialty dehumidifiers, while others pursue acquisition. Private-equity interest remains vibrant; Gamut Capital’s purchase of Airtron injects capital for geographic roll-outs and technician training aimed at capturing share amid the North America air conditioning equipment market’s service-centric pivot. Overall, the combined top-five share of 55% yields a moderate concentration profile that still allows room for innovation-led disruptors in controls and IAQ accessories.

North America Air Conditioning Equipment Industry Leaders

Daikin Industries Ltd

Carrier Corporation

Rheem Manufacturing Company

Trane Inc. (Trane Technologies PLC)

Johnson Controls International PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: GMCC & Welling announced a Dallas R&D center opening in Q3 2025 to tailor compressor designs for local codes.

- January 2025: Panasonic launched the OASYS residential central system in the United States, integrating mini-split, ERV, and DC fan modules to cut energy use by over 50%.

- December 2024: Mitsubishi Electric committed USD 143.5 million to retrofit its Kentucky plant for variable-speed compressor production, assisted by a USD 50 million DOE grant.

- August 2024: Gamut Capital agreed to acquire Airtron Heating and Air Conditioning from NRG Energy to accelerate multi-state expansion.

North America Air Conditioning Equipment Market Report Scope

The market is defined by the revenue accrued through the sale of AC equipment by various players in North America.

The North America Air Conditioning Equipment Market Report is Segmented by Equipment Type (Unitary Air Conditioners, Room Air Conditioners, Packaged Terminal Air Conditioners, Chillers, Variable Refrigerant Flow Systems), Refrigerant Type (R-410A, R-32, R-454B and R-466A), Capacity (less than 12,000, 12,001-60,000, More than 60,000), Efficiency (Low Efficiency (13-15 SEER), Medium Efficiency (16-19 SEER), High Efficiency (>20 SEER/SEER2 equivalent)), End User (Residential, Commercial, Industrial), Installation Type (New Construction, Replacement/Retrofit), Sales Channel (Direct (OEM-to-Contractor), Retail / E-commerce, Wholesalers / Distributors), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Equipment Type

| Unitary Air Conditioners | Ducted Split Systems |

| Ductless Mini-Splits | |

| Indoor Packaged and Rooftops | |

| Room Air Conditioners | |

| Packaged Terminal Air Conditioners | |

| Chillers | |

| Variable Refrigerant Flow (VRF) Systems |

By Refrigerant Type

| R-410A |

| R-32 |

| R-454B and R-466A (next-gen low-GWP) |

By Capacity (BTU/hr)

| <12,000 (less than < Ton) |

| 12,001-60,000 (1-5 Tons) |

| >60,000 (>5 Tons) |

By Efficiency (SEER Rating)

| Low Efficiency (13-15 SEER) |

| Medium Efficiency (16-19 SEER) |

| High Efficiency (>20 SEER/SEER2 equivalent) |

By End User

| Residential |

| Commercial |

| Industrial |

By Installation Type

| New Construction |

| Replacement / Retrofit |

By Sales Channel

| Direct (OEM-to-Contractor) |

| Retail / E-commerce |

| Wholesalers / Distributors |

By Country

| United States |

| Canada |

| Mexico |

| By Equipment Type | Unitary Air Conditioners | Ducted Split Systems |

| Ductless Mini-Splits | ||

| Indoor Packaged and Rooftops | ||

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| By Refrigerant Type | R-410A | |

| R-32 | ||

| R-454B and R-466A (next-gen low-GWP) | ||

| By Capacity (BTU/hr) | <12,000 (less than < Ton) | |

| 12,001-60,000 (1-5 Tons) | ||

| >60,000 (>5 Tons) | ||

| By Efficiency (SEER Rating) | Low Efficiency (13-15 SEER) | |

| Medium Efficiency (16-19 SEER) | ||

| High Efficiency (>20 SEER/SEER2 equivalent) | ||

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| By Installation Type | New Construction | |

| Replacement / Retrofit | ||

| By Sales Channel | Direct (OEM-to-Contractor) | |

| Retail / E-commerce | ||

| Wholesalers / Distributors | ||

| By Country | United States | |

| Canada | ||

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America air conditioning equipment market in 2025?

The market is valued at USD 28.97 billion in 2025 and is on track to reach USD 38.59 billion by 2030.

Which equipment category is growing the fastest?

Variable refrigerant flow systems expand at a 7.3% CAGR through 2030 thanks to energy savings and zoning flexibility.

What impact does the A2L refrigerant transition have on OEMs?

It necessitates redesigned coils, leak detection, and technician retraining, adding USD 300-600 per residential unit but positioning compliant models for future demand.

Why are high-efficiency heat pumps gaining traction in Canada?

Provincial rebates combined with federal tax credits narrow the initial cost gap with gas furnaces, while cold-climate technology maintains heating capacity at low temperatures.