Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

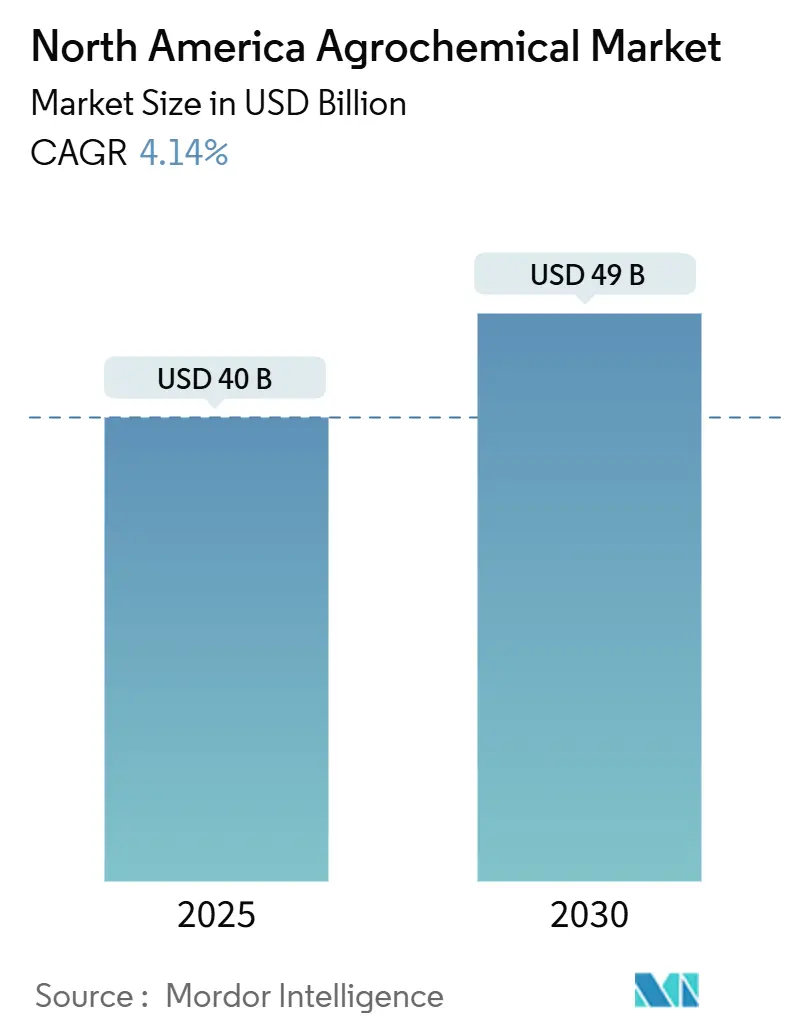

| Market Size (2025) | USD 40 Billion |

| Market Size (2030) | USD 49 Billion |

| Growth Rate (2025 - 2030) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Agrochemical Market Analysis by Mordor Intelligence

The North America agrochemical market size is valued at USD 40.0 billion in 2025 and is projected to reach USD 49.0 billion by 2030, registering a CAGR of 4.14%. The market exhibits stability while transforming through precision-application technologies, regulatory changes, and increased focus on input efficiency. Fertilizers represent the largest product segment, with precision spraying tools and digital agronomy platforms optimizing chemical application methods and timing, resulting in reduced volumes despite higher per-acre value. Market dynamics are influenced by supply chain adjustments due to tariffs and Environmental Protection Agency (EPA) regulations on endangered species protection, affecting both pricing and product selection. The demand for carbon-linked enhanced-efficiency fertilizers drives premium market segments. The industry undergoes channel destocking following the 2022-24 inventory accumulation, sustained investments in new action modes, and digital services indicate robust market fundamentals[1]U.S. Environmental Protection Agency, “EPA Updates Annual Pesticide Registration Maintenance Fee Materials for FY2025,” epa.gov.

Key Report Takeaways

- By product type, fertilizers led with 46.1% of the North America agrochemical market share in 2024, while adjuvants are projected to expand at a 6.3% CAGR through 2030.

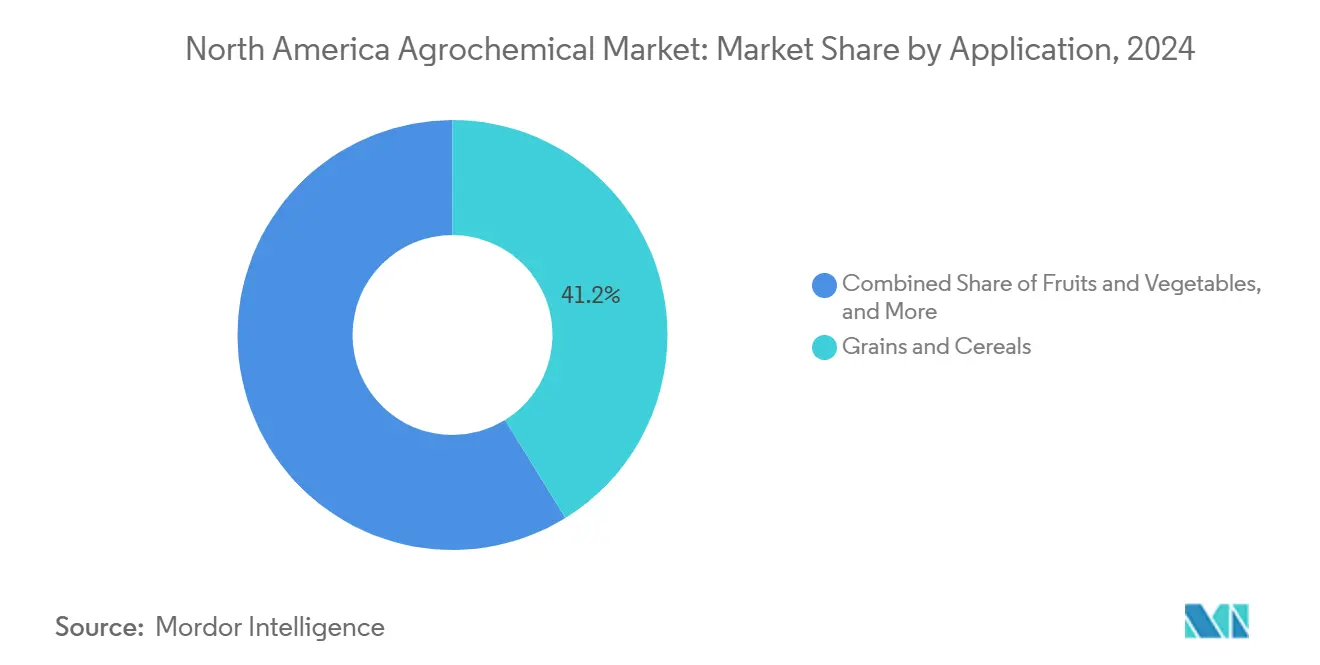

- By application, grains and cereals captured 41.2% of the North America agrochemical market size in 2024, while fruits and vegetables are advancing at a 5.4% CAGR through 2030.

- By geography, the United States held a 71.1% market share in 2024, whereas Mexico was projected to have the highest CAGR of 5.1% through 2030.

- Syngenta Group, Bayer AG, Corteva Agriscience, BASF SE, and FMC Corporation collectively account for around 60.0% of the market share in 2024.

North America Agrochemical Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for higher crop yields | +1.0% | United States Midwest and Canadian Prairies | Medium term (2-4 years) |

| Government agrochemicals purchase subsidy programs | +0.8% | United States and Mexico | Short term (≤ 2 years) |

| Precision farming driving optimized inputs | +0.9% | United States and Canada | Long term (≥ 4 years) |

| Rising pest resistance and demand for modified solutions | +0.6% | Herbicide-intensive regions | Medium term (2-4 years) |

| Carbon-credit linked enhanced-efficiency agrochemicals | +0.3% | United States and Canada | Long term (≥ 4 years) |

| Expansion of specialty micronutrient blends | +0.2% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Higher Crop Yields

The United States Department of Agriculture projects that corn productivity must increase by 1.2% annually to meet food demand by 2030. Field trials demonstrate that plant-growth regulators, specifically Ascend 2, increase corn yields by 3 bushels per acre. The combination of precision application techniques reduces nutrient losses while facilitating participation in carbon-credit programs. Agricultural producers across the Midwest United States and Canadian Prairies implement these yield-enhancing technologies, as incremental percentage improvements translate to substantial revenue increases. This market dynamic influences manufacturers to focus research and development on formulations that provide quantifiable yield improvements rather than maintaining existing productivity levels.

Government Agrochemicals Purchase Subsidy Programs

Government funding initiatives are reducing barriers to adopting modern agricultural inputs across North America. In 2024, the United States Department of Agriculture allocated USD 236 million to increase domestic fertilizer production, aiming to reduce price volatility and decrease import dependency. In Mexico, government programs support sustainable crop protection products, maintaining demand despite glyphosate limitations. Canadian provinces implement cost-sharing programs for precision agriculture technologies, including variable rate application equipment and soil testing services. These subsidies effectively reduce farmers' input costs and facilitate the adoption of advanced technologies by shortening the return on investment period for precision equipment and specialized agricultural chemicals.

Precision Farming Driving Optimized Inputs

Research demonstrates variable-rate sprayers reduce herbicide volumes by 42% while maintaining effectiveness. Precision AI's autonomous aerial systems treat 92 acres per hour at USD 2.85 per acre, influencing traditional ground-based providers and driving development of concentrated, low-drift formulations. FMC Corporation's 3RIVE 3D technology reduces water usage by 90% compared to conventional systems and covers 480 acres per fill, enhancing both operational efficiency and environmental impact. Application systems incorporating artificial intelligence and machine learning facilitate real-time pest detection and precise chemical application, with specialty crop farmers reporting annual cost savings of USD 40,000. This technological advancement is shifting the market toward high-value, digitally-enhanced products rather than volume-based sales.

Carbon-Credit Linked Enhanced-Efficiency Agrochemicals

Slow-release nitrogen fertilizers reduce nitrous-oxide emissions by 30-50%, enabling farmers to earn carbon credits that partially offset higher prices[2]Dallas Carpenter, “Enhanced Efficiency Nitrogen Fertilizers Useful Tool for Sustainable Nutrient Management,” Sask Wheat Development Commission, saskwheat.ca. Companies, including Nutrien, combine agronomic support with verification services, transforming input sales into outcome-based agreements. Adoption is highest in the United States and Canadian row-crop farming, where large-scale operations maximize environmental benefits. University of Saskatchewan research shows that polymer-coated products have different levels of effectiveness depending on application timing and environmental conditions, necessitating expert agronomic guidance to optimize both environmental and crop performance benefits. This trend continues as carbon credit programs develop and regulations strengthen, generating ongoing demand for enhanced efficiency products that provide measurable environmental improvements while maintaining agricultural productivity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Protection Agency (EPA) re-registration requirements | -0.9% | United States | Medium term (2-4 years) |

| Escalating research and development and registration costs | -0.7% | Global | Long term (≥ 4 years) |

| Consumer push for residue-free produce | -0.5% | North America specialty-crop belts | Medium term (2-4 years) |

| Biological solutions displacing conventional chemicals | -0.4% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Protection Agency (EPA) Re-Registration Requirements

The annual maintenance fees of USD 4,875 per product and enhanced ecological assessments increase compliance costs, affecting smaller registrants and leading to product withdrawals[3]Source: U.S. Environmental Protection Agency, “Pesticide Registration Maintenance Fee; Cancellation Order for Certain Pesticide Registrations,” epa.gov. The implementation of the Herbicide Strategy necessitates mitigation measures for over 900 endangered species, which include application restrictions and buffer zone requirements that impact product usage patterns. In October 2024, 131 Federal Insecticide, Fungicide, and Rodenticide Act section 3 registrations and 44 Federal Insecticide, Fungicide, and Rodenticide Act section 24(c) registrations were cancelled due to non-payment of maintenance fees. The Pesticide Registration Improvement Act of 2022 requires bilingual labeling, with Spanish translations for health and safety sections mandatory by 2025 for high-toxicity products and for all pesticide labels by 2030.

Consumer Push for Residue-Free Produce

The United States International Trade Commission's Global Economic Impact analysis reveals that varying maximum residue levels across markets disrupt trade and increase compliance costs for agricultural exporters. Specialty crop producers must manage different maximum residue limits in various countries, which increases testing expenses and requires shorter intervals between spraying. Studies indicate that 93% of no-till corn and soybean production uses chemical pesticides, with a substantial portion deemed hazardous to human health. Retailers have implemented protocols favoring reduced-risk pesticides and post-harvest washing due to residue concerns[4]U.S. International Trade Commission, “Global Economic Impact of Missing and Low Pesticide Maximum Residue Levels,” usitc.gov. These factors drive demand for low-persistence pesticides while limiting overall chemical usage.

Segment Analysis

By Product Type: Fertilizers Lead as Adjuvants Gain Speed

Fertilizers hold 46.1% of the North America agrochemical market share in 2024, maintaining their essential position in nutrient management across major corn, soybean, and wheat production areas. Enhanced-efficiency fertilizers, featuring controlled-release mechanisms, gain market share through their compatibility with carbon-credit programs and precision application equipment. Digital soil-mapping enables suppliers to offer customized blends, increasing revenue per metric ton despite stable overall volumes.

Adjuvants represent the fastest-growing segment in the North American agrochemical market, with a 6.3% CAGR through 2030. This growth stems from rising demand for spray-quality enhancers that minimize drift and improve foliar absorption. The growth correlates with increased adoption of drone and autonomous sprayer technologies, which require specialized surface-active agents due to lower carrier volumes. Despite their smaller market share, adjuvants achieve mid-single-digit CAGR, exceeding pesticides and fertilizers, as regulatory requirements emphasize improved spray deposition accuracy. Pesticides maintain their position as the second-largest product category, with herbicides predominant due to widespread herbicide-tolerant crop adoption and weed control needs. Plant growth regulators remain a specialized segment, with products like WinField United's Ascend 2 delivering corn yield increases of 3 bushels per acre, supporting premium pricing despite limited market reach.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Grains Dominate, Fruits and Vegetables Accelerate

Grains and cereals account for 41.2% of the North America agrochemical market size in 2024. This dominance stems from the adoption of genetic technology and high acreage concentration in the United States Corn Belt and the Canadian Prairies. Herbicide-tolerant traits form the foundation of chemical programs, while growers adopt pre-emergence residuals and post-emergence combinations to manage resistance. Large grain farms effectively implement precision nutrient and variable-rate lime applications, thereby supporting demand for fertilizers and liming products.

The fruits and vegetables segment grows at a 5.4% CAGR, driven by intensive management practices and adoption of premium chemistries to meet residue-free retail requirements. While the North America agrochemical market size for specialty crops remains smaller than grains, it generates higher revenue per acre. The segment's growth comes from investments in low Pre-Harvest Interval (PHI) fungicides, targeted miticides, and pollinator-safe insecticides. Pulses and oilseeds constitute a major application category, with soybean production relying on herbicide programs for weed control in no-till systems. The turf and ornamentals segment maintains premium pricing due to aesthetic requirements and specific pest challenges, as demonstrated by fluopyram's effectiveness against Pacific shoot-gall nematode in golf course applications.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States holds 71.1% of the North America agrochemical market share in 2024. The market growth through 2030 depends on the adoption of precision spraying technology, which reduces herbicide usage by 42% while maintaining effectiveness. Federal initiatives to increase domestic fertilizer production capacity combine agricultural input security with farm policy, ensuring a stable supply amid stricter regulations.

Mexico shows the highest growth rate at 5.1% CAGR through 2030. The country's agricultural exports to the United States now exceed Chinese volumes, driven by nearshoring of produce supply chains. The planned reduction in glyphosate usage drives farmers to adopt integrated weed management systems that combine mechanical methods and alternative chemical solutions. Government-funded loans and infrastructure development enhance cold-storage and logistics capabilities, which increase chemical demand through improved market access.

Canada maintains its market share through Prairie grain operations that utilize extensive variable-rate application systems. Research by the University of Saskatchewan demonstrates a 30-50% reduction in nitrous-oxide emissions when combining enhanced-efficiency fertilizers with zone-based application methods, providing both financial and environmental benefits. Provincial support through grants for soil mapping and drone monitoring strengthens these agricultural practices.

Competitive Landscape

Syngenta Group, Bayer AG, Corteva Agriscience, BASF SE, and FMC Corporation collectively held around 60.0% share of the North America agrochemical market in 2024, indicating moderate market concentration. Syngenta maintained its market leadership despite a 24% decline in regional crop-protection sales in 2024, primarily due to distributor inventory adjustments. The company's strong position is based on its robust development pipeline for fungicides and insecticides. In 2025, Bayer AG strengthened its market position by leveraging digital platforms to presell Vyconic soybeans with five-way tolerance, targeting fields affected by resistance for a 2027 launch. Corteva demonstrated financial resilience through its balanced revenue streams from crop protection products, achieving first-quarter 2025 earnings per share of USD 1.13, which exceeded market expectations.

FMC's 3RIVE 3D in-furrow application system demonstrates technological advancement in the sector, reducing water consumption by 90% and providing 480-acre coverage per fill. BASF's consideration of an initial public offering for its Agricultural Solutions division indicates potential changes in resource allocation and research development strategies. The market faces competition from agricultural technology companies such as Precision AI, whose autonomous aerial sprayers operate at costs below USD 2.85 per acre, challenging traditional application methods.

Companies are focusing on artificial intelligence for pest prediction, variable rate application systems for chemical optimization, and enhanced formulations that balance efficacy with environmental considerations. The industry demonstrates increased investment in digital platforms to improve agricultural decision-making and product performance.

North America Agrochemical Industry Leaders

Syngenta Group

Bayer AG

Corteva Agriscience

BASF SE

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: FMC Corporation, a global agricultural sciences company, established a strategic agreement with Corteva Agriscience to expand FMC's fluindapyr fungicide technology in the United States corn and soybean markets. The collaboration enables the United States growers to combat foliar diseases, including tar spot and southern rust, with this fungicide's active ingredient.

- June 2025: Ostara launched its phosphorus fertilizer, CG P2X, in Western Canada. The fertilizer, based on Crystal Green technology, provides a root-activated and seed-safe phosphorus source. CG P2X aims to reduce phosphorus tie-up in soils and improve nutrient efficiency in crop production.

- March 2025: 3Degrees, a global climate solutions provider and certified B Corporation, established the Low Carbon Fertilizer Alliance to reduce agricultural supply chain emissions for food, beverage, and apparel companies. CF Industries implemented an emissions reduction project at its Verdigris, Oklahoma, facility as part of its commitment to the alliance.

- March 2025: Bayer AG unveiled Vyconic soybeans tolerant to five herbicide modes of action, with commercial launch slated for 2027 pending regulatory clearance. Vyconic soybeans are the first in the industry to provide tolerance to five herbicides: dicamba, glufosinate, mesotrione, 2,4-D, and glyphosate.

North America Agrochemical Market Report Scope

According to the OECD, agrochemicals are commercially produced, usually chemical, bio-based compounds used in farming, such as fertilizers, pesticides, or soil conditioners.

The North American agrochemicals market is segmented by type (fertilizers, pesticides, adjuvants, and plant growth regulators), application (grains and cereals, pulses and oilseeds, fruits and vegetables, turfs and ornamentals, and other applications), and geography (United States, Canada, Mexico, and Rest of North America). The report offers market estimation and forecasts in value (USD) for all the above-mentioned segments.

By Product Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Turfs and Ornamentals |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Turfs and Ornamentals | ||

| Other Applications | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America agrochemical market in 2025?

It stands at USD 40.0 billion and is projected to reach USD 49.0 billion by 2030, implying a 4.14% CAGR over the forecast period.

Which product category currently generates the most revenue?

Fertilizers lead with 46.1% of 2024 sales, driven by both commodity NPK and rising enhanced-efficiency formulations.

What is the fastest-growing geographic segment through 2030?

Mexico is expanding at a 5.1% CAGR as nearshoring of produce supply chains and modernization programs boost input demand.

Which companies control the majority of regional sales?

Syngenta Group, Bayer AG, Corteva Agriscience, BASF SE, and FMC Corporation collectively hold around 60.0% of revenue, reflecting moderate concentration and ongoing innovation rivalry.