North America Agriculture Adjuvants Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

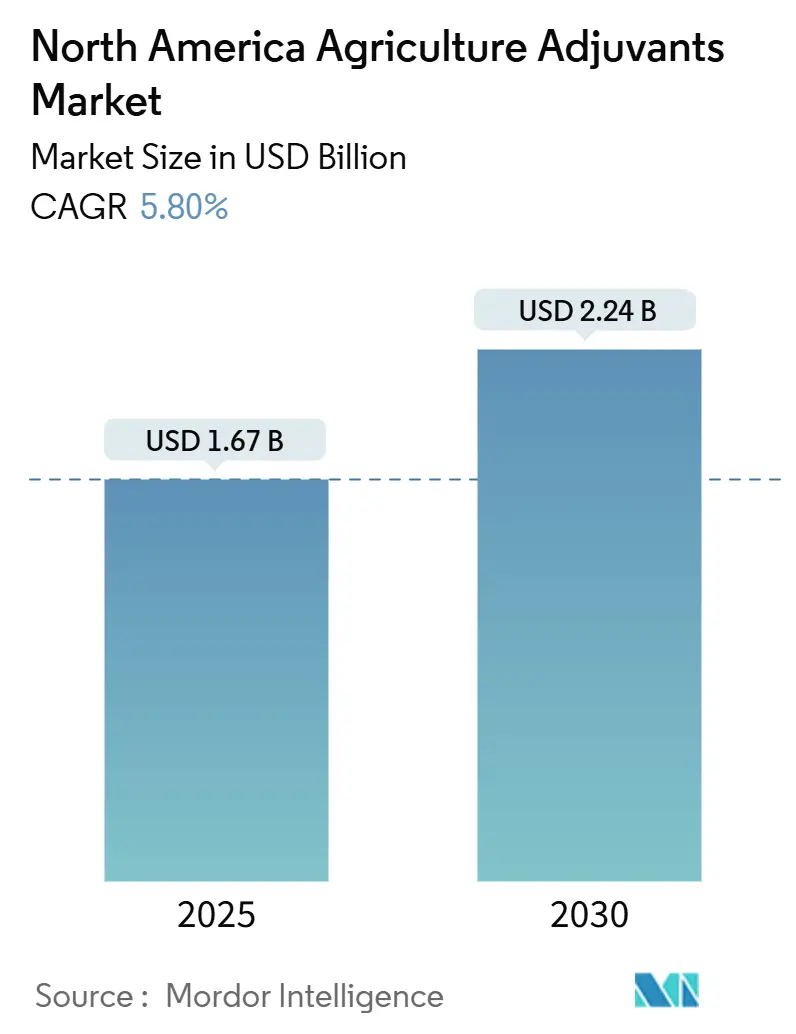

| Market Size (2025) | USD 1.67 Billion |

| Market Size (2030) | USD 2.24 Billion |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Agriculture Adjuvants Market Analysis by Mordor Intelligence

The North America agriculture adjuvants market size reached USD 1.67 billion in 2025 and will rise to USD 2.24 billion by 2030, reflecting a 5.80% CAGR. This momentum is driven less by volume gains and more by the economics of modern crop protection as herbicide-resistant weeds now span 120 million acres in the United States, forcing growers to optimize every spray pass. Activator adjuvants remain dominant, but utility adjuvants are accelerating because precision-spraying platforms require drift-control and deposition chemistries that legacy surfactants cannot deliver. Parallel regulatory and sustainability pressures from the Environmental Protection Agency (EPA) drift-mitigation rules, which took effect in 2024, and carbon-credit programs rewarding input efficiency are reshaping procurement priorities toward branded, traceable, and biologically compatible solutions.

Key Report Takeaways

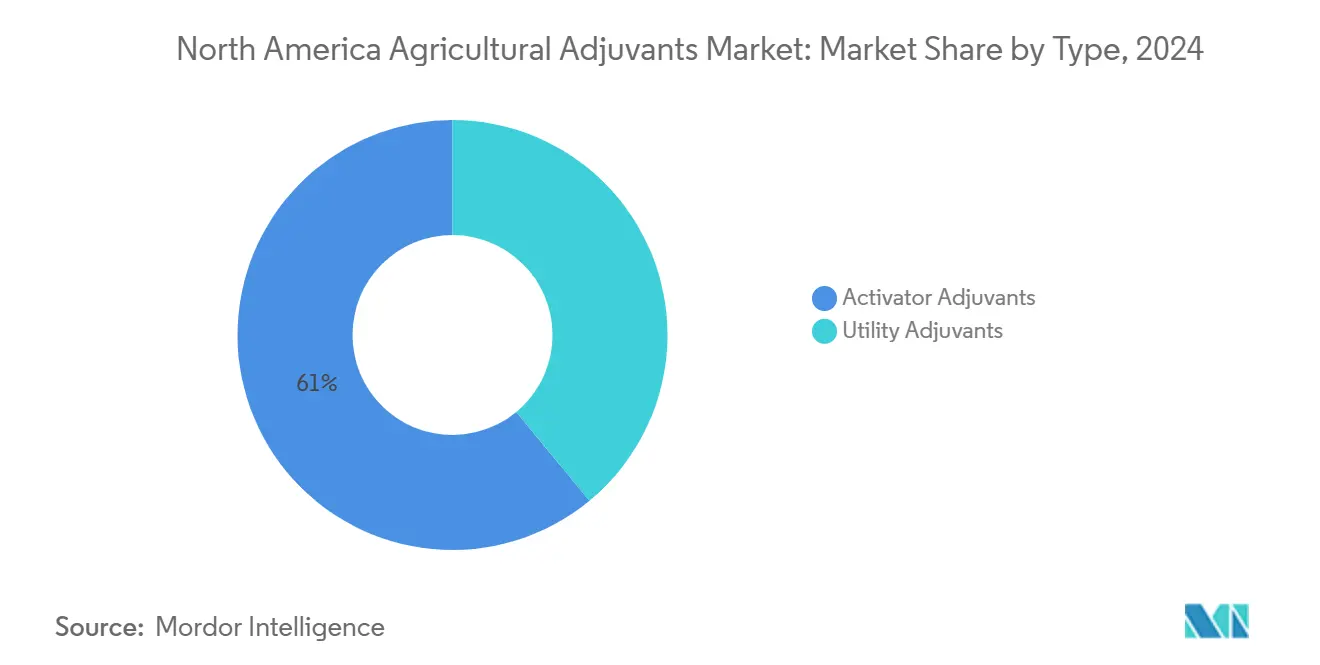

- By type, activator adjuvants accounted for 61.0% of the North America agriculture adjuvants market share in 2024, while utility adjuvants are on track to expand at a 9.8% CAGR through 2030.

- By application, herbicide adjuvants led with 48.5% of the North America agriculture adjuvants market share in 2024, whereas insecticide adjuvants are forecast to post an 8.9% CAGR to 2030.

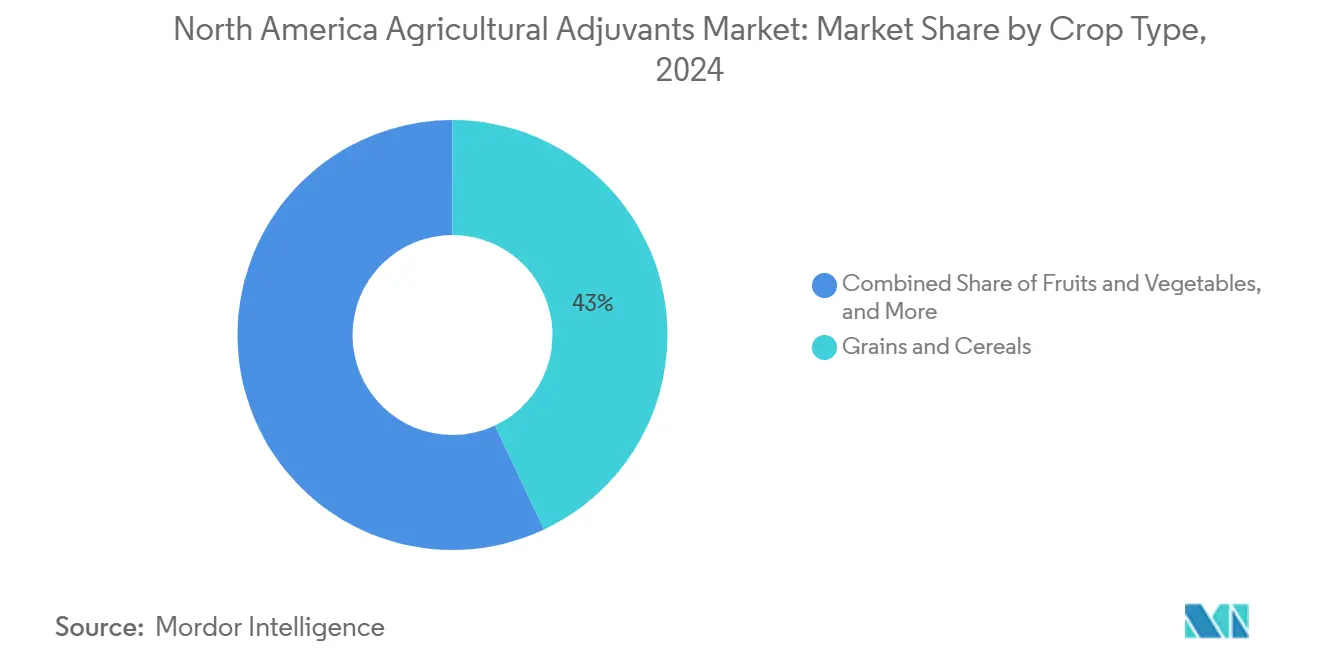

- By crop type, grains and cereals held 43.0% of the North America agriculture adjuvants market share in 2024, and fruits and vegetables will advance at a 7.5% CAGR to 2030.

- By geography, the United States captured 72.0% of the North America agriculture adjuvants market share in 2024, and Mexico is projected to grow at a 7.7% CAGR to 2030.

North America Agriculture Adjuvants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing use of natural and sustainable adjuvants | +0.9% | United States and Canada, with early organic-certified adoption in California, and Ontario | Medium term (2-4 years) |

| Growing demand for crop-protection chemicals | +1.2% | United States (Midwest corn-soy belt) and Mexico (emerging commercial farms) | Short term (≤ 2 years) |

| Higher investment in adjuvant R&D by multinationals | +0.7% | Global, with innovation hubs in United States (Delaware, New Jersey) and Canada (Alberta) | Long term (≥ 4 years) |

| Expansion of precision-spraying technologies | +1.4% | United States (Great Plains, Corn Belt), Canada (Prairie Provinces), and Mexico (Sinaloa, Sonora) | Medium term (2-4 years) |

| Carbon-credit incentives for input-efficiency products | +0.6% | United States (United States Department of Agriculture (USDA) Climate-Smart Commodities states), and Canada (federal carbon pricing zones) | Long term (≥ 4 years) |

| Surfactant blends optimized for biologicals | +1.0% | United States (California, Florida specialty crops), and Canada (Quebec, Ontario vegetable zones) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Use of Natural and Sustainable Adjuvants

Organic acreage in the United States grew 12% year on year to 5.6 million acres in 2024, opening more shelf space for OMRI-listed adjuvants that comply with National Organic Program rules [1]Source: U.S. Department of Agriculture, “Organic Farming Data,” USDA.gov. Methyl soyate and ethyl lactate are now displacing petroleum-based crop-oil concentrates in many herbicide programs as retailers extend sustainability scorecards to their supply partners. Croda’s rapeseed-derived surfactant line, launched in 2024, illustrates how renewable feedstocks can satisfy both volatile-organic-compound limits and grower preference for lower-risk inputs. California’s stringent Volatile Organic Compound (VOC) rules accelerate this trend because low adjuvants preserve air-quality compliance without compromising efficacy. Carbon-intensity metrics embedded in food-processor supply contracts amplify demand by rewarding input suppliers that can document Scope 3 reductions.

Growing Demand for Crop-Protection Chemicals

Palmer amaranth and waterhemp resistance to glyphosate triggered a 25% surge in herbicide treatments per acre in Midwestern corn and soybean systems since 2020, elevating adjuvant usage to maintain coverage without raising active-ingredient loads. Mexico mirrors this trajectory: federal subsidies now offset up to 50% of herbicide and adjuvant costs for commercial farms in Sinaloa and Sonora under the Fertilizantes para el Bienestar program. Insecticide adjuvants are also climbing as pyrethroid resistance spreads in corn rootworm and soybean aphid populations, spurring interest in chemistries that enhance cuticle penetration and rainfastness. Almond and grape growers deploy premium adjuvants to enhance fungicide canopy coverage, thereby extending spray intervals and reducing labor bottlenecks during peak season as growers stack modes of action, adjuvants that buffer pH, and manage water hardness, becoming indispensable to avoid antagonism in complex tank mixes.

Higher Investment in Adjuvant R&D by Multinationals

Corteva allocated USD 2.1 billion to R&D in 2024, directing a sizable share to proprietary adjuvant systems that enhance the performance ceiling of its flagship herbicides [2]Source: Corteva Agriscience, “2024 R&D Highlights,” Corteva.com. BASF paired its Revysol fungicide relaunch with co-developed adjuvants that confer faster rainfastness and systemic movement, underscoring a shift toward bundled chemistry solutions. Stepan broke ground on a USD 50 million surfactant plant in Illinois to secure domestic intermediates amid geopolitical uncertainty. Patent filings for adjuvant formulations increased 18% in 2024, with a focus on drift-reduction polymers and biocompatible surfactants, signaling that intellectual property has become a moat in what was once a commodity space. Companies with toxicology datasets that meet the EPA’s revised inert-ingredient guidance are better positioned to list new products faster, thereby raising competitive hurdles for smaller formulators.

Expansion of Precision-Spraying Technologies

John Deere’s See and Spray Ultimate covered 1.2 million acres in 2024, trimming herbicide volumes by up to 76% in Nebraska corn trials but only when paired with adjuvants that stabilize droplets at lower carrier volumes. Drift-control polymers and deposition aids are crucial for maintaining finely atomized sprays within target zones, particularly in regulatory districts that now require coarse droplets to protect endangered species habitats. Mexico’s drip-irrigation subsidy program accelerates the uptake of precision sprayers in water-limited regions, thereby multiplying demand for utility adjuvants that optimize low-volume applications. In Canada, Prairie growers integrate precision spraying with VR nitrogen and seeding, creating complex tank mixes that require high-tolerance compatibility agents.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Protection Agency and regulatory guidelines | -0.8% | United States (European Space Agency (ESA) counties, drift-prone zones), Canada (Pest Management Regulatory Agency (PMRA) registration delays) | Short term (≤ 2 years) |

| Low grower awareness in specialty-crop pockets | -0.4% | United States (Southeast vegetables, Pacific Northwest tree fruits), Mexico (smallholder zones) | Medium term (2-4 years) |

| Volatility in tall-oil and methyl-soyate feedstocks | -0.6% | United States and Canada (bio-based adjuvant manufacturers), Mexico (import-dependent formulators) | Short term (≤ 2 years) |

| Increasing scrutiny of wetting agents | -0.5% | United States (Pest Management Regulatory Agency (PMRA)-sensitive watersheds), Canada (Great Lakes basin) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Protection Agency and Regulatory Guidelines

The Environmental Protection Agency's (EPA’s) 2024 Herbicide Strategy requires applicators in 1,500 counties designated under the Endangered Species Act to log adjuvant selection and weather parameters, prompting small operators to adopt new record-keeping systems or face compliance penalties. Coarser droplet mandates now cover 40% of the United States cropland, which can reduce efficacy on small-seeded weeds and may lead to repeat treatments if unsuitable adjuvants are used. Canada’s Pest Management Regulatory Agency added aquatic-toxicity data requirements for every surfactant component, extending registration timelines and raising costs for new entrants. Mexico tightened import permits on nonylphenol ethoxylate blends, forcing distributors either to reformulate or exit. As hurdles rise, suppliers with Environmental Protection Agency (EPA) registrations gain a market advantage because growers prefer traceable products that simplify audits.

Low Grower Awareness in Specialty-Crop Pockets

Extension surveys indicate that fewer than 40% of vegetable growers in Pennsylvania and North Carolina adjust adjuvant picks for water hardness or pH, leaving untapped efficacy gains. Retail agronomists often prioritize high-volume row-crop clients, resulting in limited technical advice for tree-fruit and wine-grape producers in the Pacific Northwest. Mexico’s smallholder sector, which cultivates 60% of the farmland, receives minimal adjuvant education because public programs focus mainly on seeds and fertilizers. Price-driven purchasing of generic adjuvants dominates these areas, leading to the potential overapplication of active ingredients. Digital agronomy tools from Farmers Business Network offer field-specific recommendations, but they remain concentrated among larger growers with strong broadband access.

Segment Analysis

By Type: Utility Adjuvants Gain Momentum in Precision Spraying

Activator adjuvants accounted for 61.0% of the revenue in 2024, as non-ionic surfactants and crop-oil concentrates remained core to post-emergence herbicide programs in corn and soybeans. Oil-based blends that include methyl soyate offer enhanced penetration and rainfastness, explaining their continued presence even as bio-based alternatives emerge. Utility adjuvants, however, are forecast to rise 9.8% annually to 2030, lifting the North America agriculture adjuvants market size for this category well above USD 900 million by the period end. Drift-control polymers and deposition aids form the backbone of this surge because precision sprayers triple the active-ingredient concentration in the tank, which increases the risk of clogging without specialized additives [3]Source: John Deere, “Precision Ag Technology,” Deere.com.

Water conditioners are another high-growth pocket, given evidence that untreated hard-water conditions can slash glyphosate efficacy by as much as 30%. Compatibility agents round out the story as biologicals move mainstream, making it a non-negotiable requirement for growers who want single-pass applications, preventing flocculation when mixing microbes and synthetics. Momentum in these utility segments means the North America agriculture adjuvants market share for activators is expected to slide modestly even as absolute activator revenue rises.

Note: Segment shares of all individual segments available upon report purchase

By Application: Insecticide Adjuvants Accelerate under Resistance Pressure

Herbicide adjuvants generated 48.5% of the revenue in 2024, reflecting the entrenched reliance on weed management across 320 million acres of United States cropland. Nevertheless, insecticide adjuvants are projected to increase 8.9% annually through 2030, expanding their share of the North America agriculture adjuvants market size as pyrethroid resistance forces growers to seek better cuticle penetration tools. Demand is especially strong in corn rootworm hotspots where improving residual control can trim rescue-treatment costs.

Fungicide adjuvants continue to expand in high-value fruits and vegetables because canopy density makes thorough coverage critical. BASF SE’s drift-reduction additives coupled with Revysol illustrate how integrated offerings reshape buying dynamics. Other applications, namely plant-growth regulators and foliar nutrients, contribute steady but smaller revenue streams, with performance heavily tied to adjuvants that reduce phytotoxicity in stress-sensitive crops.

By Crop Type: Fruits and Vegetables Justify Premium Price Points

Grains and cereals dominated the market with 43.0% revenue in 2024, as herbicide programs are non-optional across vast corn and soybean acreage. By contrast, fruits and vegetables are forecast to grow at a rate of 7.5% per year to 2030, increasing the North America agriculture adjuvants market share for high-value specialty crops, as premium inputs pay for themselves through reduced disease losses. Almond and wine-grape estates in California alone spend more than USD 200 million annually on adjuvants that help maximize the length of fungicide intervals.

Oilseeds such as canola depend on adjuvants that improve herbicide selectivity, and Canada’s 22 million-acre canola belt ensures a baseline of demand even under flat acreage projections. Turf and ornamental use remains a niche market but carries premium pricing because end users value aesthetics and low-odor formulations, contributing incremental dollar volume despite small tonnage.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United States generated 72.0% of 2024 revenue, reflecting its expansive cropland, high adjuvant penetration rates, and tight linkage between chemical suppliers and digital agronomy platforms. The North America agriculture adjuvants market size in the United States will still grow, albeit at a slower pace than in Mexico, as saturation effects begin to take hold. Farmer Business Network’s direct-to-grower channel pressures distributor margins and places a premium on technical service rather than simple product availability.

Mexico is projected to grow at a 7.7% CAGR through 2030, driven by government subsidy programs that reimburse the purchase of precision equipment and encourage the use of biologically compatible adjuvants across smallholder cooperatives. Commercial vegetable operations in Sinaloa and Sonora adopt integrated weed management strategies that mirror best practices in the United States, driving increases in herbicide adjuvant usage for crops where per-acre revenue justifies premium additives.

Canada remains a steady but slower grower, with Prairie provinces accounting for 80% of national adjuvant demand. Cool, short-season conditions make rainfastness particularly important. Hence, activator adjuvants that accelerate foliar uptake continue to command loyalty. Federal carbon pricing of CAD 80 (USD 59) per metric ton incentivizes input-efficiency gains that bolster utility-adjuvant volumes, especially those that enable lower carrier rates in precision spraying scenarios

Competitive Landscape

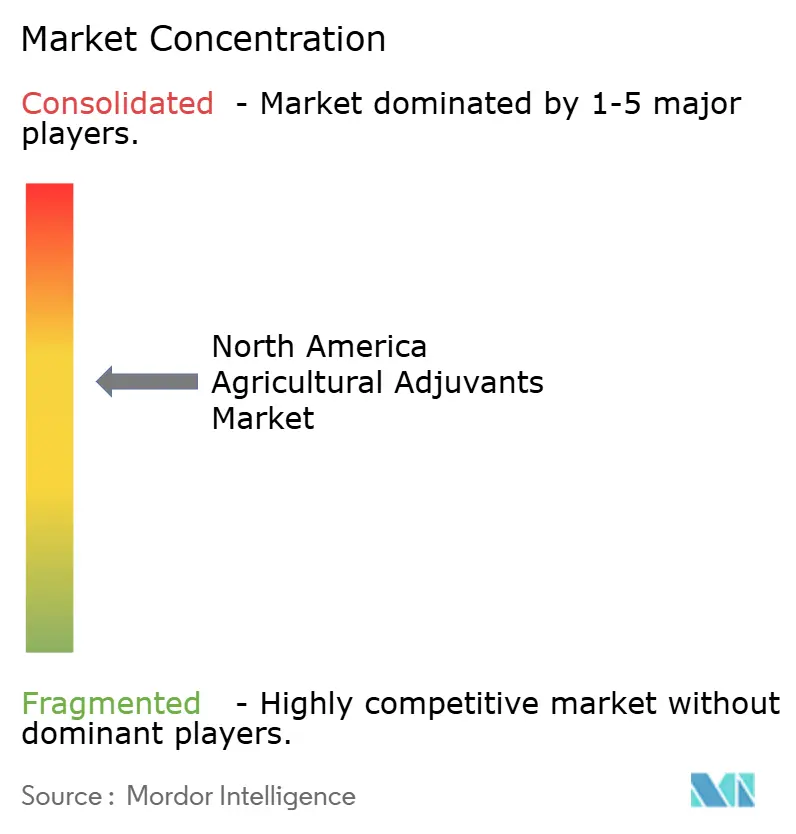

The North America agriculture adjuvants market remains moderately concentrated, with the five largest suppliers, Corteva Agriscience, Stepan Company, Croda International PLC, Helena Agri-Enterprises, and Land O’Lakes Inc. Each multinational pairs in-house chemistry with distribution scale, allowing them to bundle adjuvants alongside proprietary herbicides and fungicides and lock in grower loyalty. Mid-tier formulators hold the remaining share and compete mostly on price in commodity surfactants, although regulatory expertise and local agronomic support create defensible niches. Patent activity around drift-reduction polymers, biocompatible surfactants, and pH buffers rose 18% in 2024, signaling that intellectual property is becoming a barrier for late entrants.

Strategic investments underscore how leaders seek differentiation. Corteva Agriscience earmarked USD 150 million to expand its Johnston facility and add biologicals-compatible adjuvant capacity that supports its Utrisha foliar line, tightening vertical integration from active ingredient to final spray mix. BASF SE rolled out a new drift-reduction series co-developed with Revysol fungicide, providing specialty-crop growers with a turnkey solution that meets EPA coarse-droplet rules without compromising efficacy. Croda International PLC acquired Solus Biotech for USD 85 million, gaining surfactant know-how that accelerates growth in organic-certified and microbial-safe formulations. Stepan’s USD 50 million Illinois plant secures domestic feedstocks for bio-based surfactants, hedging geopolitical risk tied to import supplies.

Disruptive models are emerging in parallel. Farmers Business Network bypasses traditional retail by bundling adjuvants with data subscriptions that generate field-specific recommendations, compressing distributor margins while sharpening price transparency. Equipment makers such as Deere & Company partner with adjuvant formulators to co-design chemistries that prevent nozzle clogging in precision sprayers, raising the engineering bar for independent blenders. Innovation white space also lies in PFAS-free wetting agents and OMRI-listed blends, areas where smaller specialists can scale fast before multinationals react. As EPA drift and inert-ingredient rules tighten, growers prefer branded, fully registered formulations that simplify audits, a trend likely to extend the advantage of suppliers with deep regulatory portfolios.

North America Agriculture Adjuvants Industry Leaders

-

Corteva Agriscience

-

Land O’Lakes Inc.

-

Stepan Company

-

Croda International PLC

-

Helena Agri-Enterprises

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Corteva Agriscience announced a USD 150 million expansion of its formulation facility in Johnston, Iowa, adding capacity for biologicals-compatible adjuvants designed to work with its Utrisha foliar biofungicide line. This expansion reflects the company's strategic pivot toward integrated crop protection solutions that bundle active ingredients with performance-enhancing additives.

- December 2024: BASF SE launched a new line of drift-reduction adjuvants co-developed with its Revysol fungicide platform, targeting specialty-crop growers in California and Florida who face stringent spray-drift regulations under EPA's 2024 Herbicide Strategy.

- November 2024: Croda International plc completed the acquisition of Solus Biotech for USD 85 million, gaining formulation expertise in biologicals-compatible surfactants and expanding its portfolio of OMRI-listed adjuvants for organic-certified production systems.

North America Agriculture Adjuvants Market Report Scope

Adjuvants are materials added to crop protection products or agrochemicals to enhance the efficacy of active ingredients and improve the overall performance of the product. North American Agriculture Adjuvants Market is Segmented by Type (Activator Adjuvants and Utility Adjuvants) Application (Herbicide Adjuvants, Insecticide Adjuvants, Fungicide Adjuvants, and Others) Crop Application (Crop based and Non Crop based), and Geography (United States, Mexico, Canada and Rest of North America). The report offers the market size and forecasts in terms of value (USD) for all the above segments.

| Activator Adjuvants | Surfactants |

| Oil Adjuvants | |

| Utility Adjuvants |

| Herbicide Adjuvants |

| Insecticide Adjuvants |

| Fungicide Adjuvants |

| Other Applications |

| Crops Based | Grains and Cereals |

| Fruits and Vegetables | |

| Oil Seeds | |

| Other Applications | |

| Non-Crops Based | Turf and Ornamental Grass |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Activator Adjuvants | Surfactants |

| Oil Adjuvants | ||

| Utility Adjuvants | ||

| By Application | Herbicide Adjuvants | |

| Insecticide Adjuvants | ||

| Fungicide Adjuvants | ||

| Other Applications | ||

| By Crop Type | Crops Based | Grains and Cereals |

| Fruits and Vegetables | ||

| Oil Seeds | ||

| Other Applications | ||

| Non-Crops Based | Turf and Ornamental Grass | |

| Others | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large is the North America agriculture adjuvants market in 2025?

It stands at USD 1.67 billion and is forecast to reach USD 2.24 billion by 2030.

What CAGR is projected for adjuvant sales through 2030?

The market is projected to expand at a 5.8% CAGR over the forecast period.

Which adjuvant type is growing fastest?

Utility adjuvants, including drift-control and deposition aids, are set to climb 9.8% annually as precision spraying scales up.

Why are insecticide adjuvants gaining traction?

Rising pyrethroid resistance increases demand for additives that improve cuticle penetration and residual activity.

How will carbon-credit programs influence adjuvant adoption?

USDA and private-sector carbon markets financially reward growers who pair adjuvants with precision equipment to cut chemical rates, accelerating uptake.

What regulatory changes most affect adjuvant choices?

EPA drift-mitigation rules and PFAS scrutiny push growers toward coarse-droplet, PFAS-free, and EPA-registered formulations.

Page last updated on: