Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

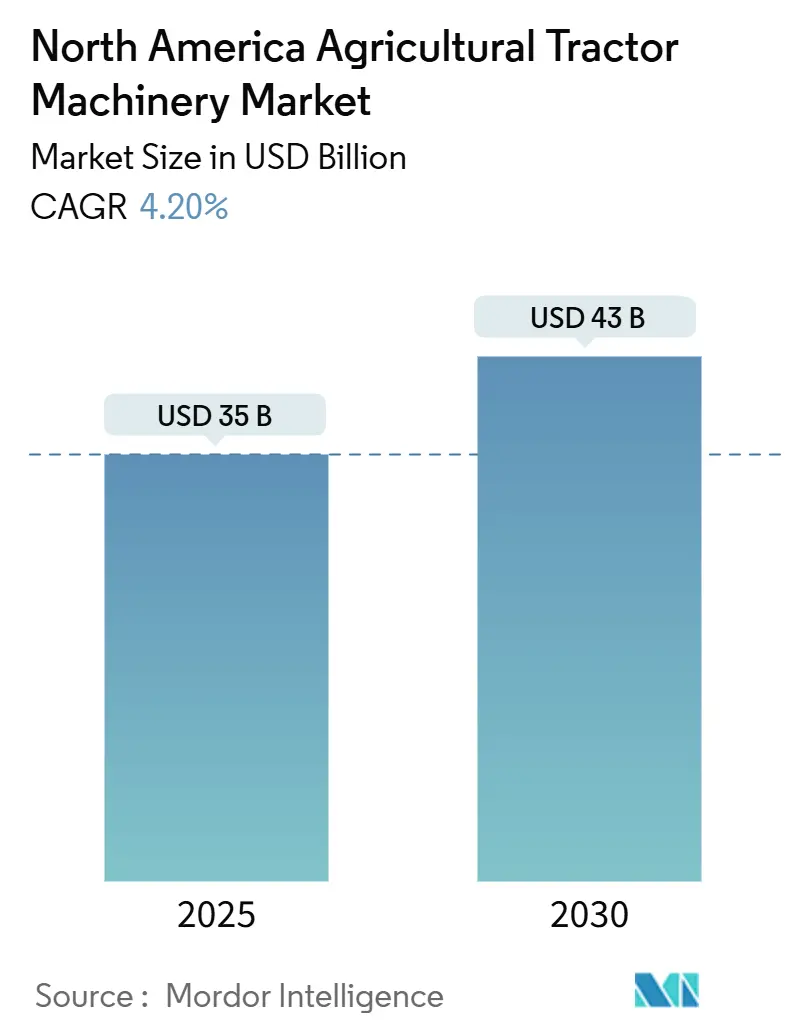

| Market Size (2025) | USD 35 Billion |

| Market Size (2030) | USD 43 Billion |

| Growth Rate (2025 - 2030) | 4.20% CAGR |

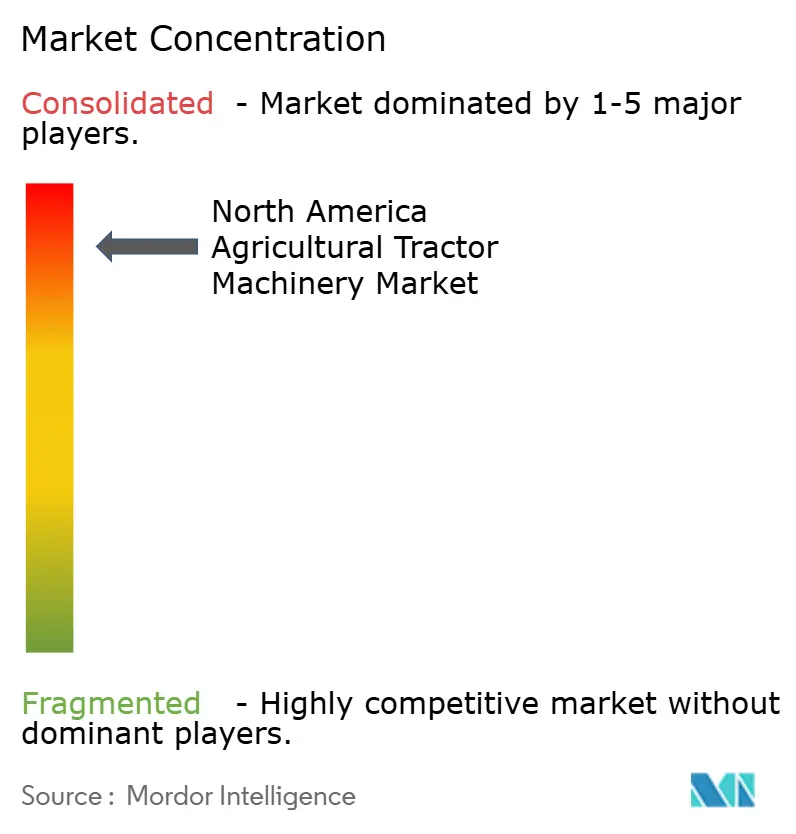

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The North America agricultural tractor machinery market stands at USD 35 billion in 2025 and is projected to reach USD 43 billion by 2030, reflecting a 4.20% CAGR over the forecast period. The combination of labor shortages, climate-smart incentives, and the first commercially viable autonomous and electric tractor platforms is reshaping demand patterns. Growers are replacing aging fleets not to expand acreage but to raise productivity per acre amid tighter environmental compliance windows [1]Source: USDA Economic Research Service, “Farm Income and Wealth Statistics,” ERS.USDA.GOV. Federal and state cost-share programs that cover as much as 75% of the purchase price for low-disturbance equipment have shortened replacement cycles. Meanwhile, retrofit autonomy kits priced between USD 50,000 and USD 150,000 enable mid-sized farms to unlock supervised autonomy without purchasing new, seven-figure machines [2]Source: USDA Natural Resources Conservation Service, “Environmental Quality Incentives Program,” NRC.USDA.GOV. At the same time, rising steel costs and dealership consolidation threaten to slow adoption in price-sensitive segments, creating a bifurcated upgrade path in which large growers move quickly and smaller farms defer purchases.

Key Report Takeaways

- By product type, plowing and cultivating machinery led with a 38.2% market share of the North America agricultural tractor machinery in 2024, while sprayers are projected to grow at a 6.9% CAGR from 2025 to 2030.

- By geography, the United States commanded 63.4% market share of the North America agricultural tractor machinery in 2024, and Mexico is advancing at a 5.9% CAGR through 2030.

North America Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Retrofit Demand for Autonomous Tractor Retrofit Kits | +0.6% | United States and Canada, and early Midwest adoption | Medium term (2-4 years) |

| Government Carbon-Smart" Tillage Incentives Accelerating Equipment Upgrades" | +0.8% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Ongoing Labor Shortages Boosting Tractor-Implement Packages | +0.7% | United States, Canada, and Mexico export horticulture zones | Long term (≥ 4 years) |

| Electrification Pilots by OEMs (Original Equipment Manufacturers) Lowering Lifetime Operating Cost | +0.4% | California, Northeastern dairy, and peri-urban Mexico | Long term (≥ 4 years) |

| Resilient Grain Price Outlook Sustaining Farmer Cash-Flow for Machinery | +0.5% | United States Corn Belt, Canadian prairies, and Mexico feed-grain importers | Medium term (2-4 years) |

| Shift Toward Strip-Tillage Favors Higher-Horsepower Articulated Tractors | +0.5% | United States Midwest, Saskatchewan, and Alberta dryland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Retrofit Demand for Autonomous Tractor Retrofit Kits

Aftermarket autonomy packages now allow growers to extend the useful life of tractors built as recently as 2015 for a fraction of the cost of factory-equipped autonomous units. Kits priced at USD 50,000–USD 150,000 bolt onto legacy 200- to 400-horsepower models and deliver supervised autonomy for tillage, planting, and spraying. Payback periods fall below three years when labor savings and longer operating windows are counted, especially in the 2,000- to 5,000-acre operations that dominate the United States Corn Belt [3]Source: AGCO Investor Presentation, “Quarterly Earnings and Strategic Updates,” AGCOCORP.COM. Deere’s 8R fully autonomous tractor, launched in production in 2024, retails above USD 500,000, underscoring the appeal of retrofit paths. Rapid kit adoption pressures OEMs (Original Equipment Manufacturers) to unbundle software from hardware and monetize autonomy as a subscription, a shift that could reshape long-term revenue models across the North America agricultural tractor machinery market.

Government Carbon-Smart" Tillage Incentives Accelerating Equipment Upgrades"

Federal and state cost-share programs covering up to 75% of equipment purchase prices have accelerated the shift from moldboard plows to vertical-tillage and strip-till tools. The United States Department of Agriculture disbursed USD 3.1 billion through the Environmental Quality Incentives Program (EQIP) in fiscal 2024, a large share of which financed low-disturbance tillage implements [4]USDA Natural Resources Conservation Service, “Environmental Quality Incentives Program,” NRC.USDA.GOV. Inflation Reduction Act provisions extend additional rebates for electric and hybrid tractors, and California’s Clean Off-Road Equipment Voucher Program can lower net costs by 40%–50% for qualifying models. Canada’s prairie provinces mirror these incentives through soil carbon credit schemes, while Mexico has begun including mechanization grants in Sembrando Vida. These overlapping subsidies compress replacement cycles from 10–12 years to as little as seven, offering OEMs (Original Equipment Manufacturers) near-term order visibility in the North America agricultural tractor machinery market.

Ongoing Labor Shortages Boosting Tractor-Implement Packages

Agricultural employment declined 3.2% year-over-year in 2024, and visa caps limit the availability of seasonal workers. Growers respond by pairing higher-horsepower tractors with wider implements such as 60-foot air seeders and 120-foot sprayers that let a single operator cover up to 1,000 acres per day. Canadian prairie farms averaging 1,800 acres amplify this trend, as do Mexican berry and avocado exporters where wages rose 25% since 2020 [5]Source: Statistics Canada, “Farm and Farm Operator Data,” STATCAN.GC.CA . Telemetry subscriptions bundled with new equipment deliver predictive maintenance and job analytics, easing the service burden when dealerships close or merge. These dynamics sustain demand for integrated tractor-implement packages across the North America agricultural tractor machinery market.

Electrification Pilots by OEMs (Original Equipment Manufacturers) Lowering Lifetime Operating Cost

OEM (Original Equipment Manufacturer) field trials between 2024 and 2025 show meaningful total cost of ownership gains in targeted use cases. CNH Industrial’s T6 180 compressed natural gas tractor achieved a 30% fuel saving at a California dairy, while AGCO’s Fendt e100 Vario pilot cut maintenance bills in half by removing diesel aftertreatment systems. Department of Energy forecasts put battery pack costs below USD 100/kWh by 2027, at which point 75- to 150-horsepower electric tractors reach purchase-price parity after tax credits. Although battery weight and rural charging gaps confine electric units to orchards, dairies, and vegetable farms today, road-mapped density improvements could see compact and utility electrics capture 10%–15% of segment revenue by 2030 within the North America agricultural tractor machinery market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Cost of Tier 4 Final / Stage V Compliant Engines | –0.7% | United States, Canada, and phased Stage V in Mexico | Short term (≤ 2 years) |

| Dealer Network Consolidation Limiting Service Accessibility in Rural Belts | –0.4% | United States Great Plains, Appalachia, and Canadian prairies | Medium term (2-4 years) |

| Volatile Steel Prices Squeezing OEM (Original Equipment Manufacturer) Margins and Inflating Sticker Prices | –0.5% | North America-wide, and greatest impact on domestic manufacturers | Short term (≤ 2 years) |

| Data-Ownership Concerns Slowing Adoption of Sensor-Integrated Implements | –0.3% | United States Corn Belt, and Canadian prairies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost of Tier 4 Final / Stage V Compliant Engines

Tier 4 Final compliance adds 12%–15% to sticker prices for new tractors above 75 horsepower, hiking a 200-horsepower model from USD 180,000 in 2014 to USD 210,000–USD 220,000 in 2025 [6]Source: U.S. Environmental Protection Agency, “Nonroad Diesel Engines – Exhaust Emission Standards,” EPA.GOV. Manufacturers unable to spread R&D costs across high volumes, such as Buhler Industries, face higher engine sourcing expense, shrinking margins. Mexican growers import used Tier 3 units from the United States ahead of Stage V rules, undermining new-equipment demand. Although supplier scale should temper after-treatment costs after 2027, price premiums will persist, limiting growth for price-sensitive slices of the North America agricultural tractor machinery market.

Dealer Network Consolidation Limiting Service Accessibility in Rural Belts

Full-service locations in rural North America fell 15% since 2020, with drive times exceeding 90 minutes in some counties. Deere cut 8% of its dealer points between 2022 and 2024, with similar reductions at CNH Industrial. Longer service travel inflates downtime risk: a single lost planting day can cost a grower USD 10,000-USD 20,000 in unrealized yield. Farmers stockpile parts and advocate for right-to-repair rules, but mid-sized operations lacking in-house mechanics still face service gaps, damping replacement demand across the North America agricultural tractor machinery market.

Segment Analysis

By Product Type: Precision Tillage Leads, Sprayers Accelerate

Plowing and cultivating machinery accounted for 38.2% of the North America agricultural tractor machinery market share in 2024, underscoring its role in seedbed preparation across more than 200 million acres of row crops. Within this segment, conservation-oriented vertical-tillage and strip-till tools are displacing moldboard plows, with state and federal incentives reinforcing adoption patterns. The North America agricultural tractor machinery market size for sprayers is projected to expand at a 6.9% CAGR as variable-rate application and the Global Positioning System (GPS) section control minimizes herbicide drift and meets buffer-zone mandates in California and Minnesota [7]Source: U.S. Environmental Protection Agency, “Nonroad Diesel Engines – Exhaust Emission Standards,” EPA.GOV.

Planting equipment forms the second-largest slice, with down-force automation and singulation sensors raising germination uniformity. Haying and forage machinery caters to beef and dairy operations; declines in Northeastern dairy herds offset gains in Pacific Northwest forage exports. Drone-generated prescription maps are boosting demand for high-clearance sprayers, a trend projected to keep chemical application equipment the fastest-growing segment of the North America agricultural tractor machinery market through 2030.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United States captured 63.4% of the North America agricultural tractor machinery market in 2024 due to vast corn, soybean, and wheat acreage. Nevertheless, unit sales slipped 13.4% year-over-year in November 2024 as elevated interest rates and inventory destocking weighed on demand. Federal climate-smart outlays and right-to-repair legislation in Colorado and Minnesota affect regional purchasing. California and New York have been early adopters of electric tractors, supported by substantial rebate programs, contributing to the growth of the North American agricultural tractor machinery market.

Mexico is forecast to grow 5.9% annually from 2025 to 2030, the fastest in the region, driven by export horticulture, smallholder mechanization grants, and the United States-Mexico-Canada Agreement (USMCA) tariff exemptions. Large northern vegetable farms demand high-capacity sprayers, while compact tractors dominate in the south. Stage V engine phase-in and gray-market used imports will shape competitive positioning in the North America agricultural tractor machinery market.

Canada is experiencing growth, driven by prairie wheat, canola, and pulse producers increasingly utilizing high-horsepower articulated tractors and air seeders to manage large farm sizes. The short growing seasons emphasize the importance of equipment reliability, while dealership consolidation follows patterns observed in the United States. The rest of North America, including Central America and the Caribbean, shows steady growth, supported by the expansion of sugarcane, coffee, and banana cultivation areas.

Competitive Landscape

The North America agricultural tractor machinery market is highly concentrated, with the top manufacturers dominating the revenue share. Deere & Company’s significant share derives from vertically integrated engines, transmissions, and early autonomy offerings like the 8R. CNH Industrial and AGCO Corporation hold a major share combined through brands such as Case IH, New Holland, Fendt, and Massey Ferguson. Kubota Corporation and Mahindra&Mahindra Ltd. gain traction in sub-200-horsepower niches by pricing 15%–20% below premium competitors and focusing on simplicity.

Agtech startups offering retrofit autonomy kits threaten to commoditize hardware and force OEMs (Original Equipment Manufacturers) toward software-as-a-service models. Electric and hybrid tractors remain niche but represent a strategic white space. Colorado’s right-to-repair law of 2024 marks a regulatory shift that could dilute OEM (Original Equipment Manufacturer) aftermarket revenue streams, which account for 30%–40% of total profitability.

Competitive responses include dealer consolidation, direct-to-farmer sales portals, and partnership announcements such as AGCO Corporation’s sourcing agreement with SDF for sub-85-horsepower tractors, freeing engineering capacity for autonomous and electric platforms.

North America Agricultural Tractor Machinery Industry Leaders

-

Deere & Company

-

AGCO Corporation

-

CNH Industrial N.V.

-

Kubota Corporation

-

Mahindra&Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: New Holland has launched the Roll-Belt 1 Series, a redesigned range of variable chamber round balers aimed at enhancing efficiency, increasing baling speed, and improving connectivity for producers. Comprising three updated models, this series incorporates enhanced durability, improved feeding capacity, and advanced technology, offering significant upgrades to New Holland's round balers.

- April 2025: AGCO Corporation expanded its dealer network by integrating Carter Agri-Systems into Utah and launching Mississippi’s first full-line Fendt and Massey Ferguson dealership through Delta Ag Equipment. This expansion strengthens AGCO’s presence in key farming regions, improving access to advanced machinery and support services for North American farmers.

- March 2025: New Holland has launched IntelliSense Sprayer Automation, a comprehensive application automation solution available as a factory-installed feature for the Model Year 2026 Guardian series front boom sprayers, including the SP310F, SP370F, and SP410F. The system is compatible with a wide range of crops.

North America Agricultural Tractor Machinery Market Report Scope

By Product Type

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Equipment | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Sprayers | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Other Types |

By Geography

| United States |

| Mexico |

| Canada |

| Rest of North America |

| By Product Type | Plowing and Cultivating Machinery | Plows |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Equipment | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Sprayers | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Other Types | ||

| By Geography | United States | |

| Mexico | ||

| Canada | ||

| Rest of North America | ||

Key Questions Answered in the Report

How big is the North America agricultural tractor machinery market in 2025?

The market stands at USD 35 billion in 2025 and is projected to reach USD 43 billion by 2030 at a 4.20% CAGR.

Which product segment is growing fastest?

Sprayers are forecast to grow at a 6.9% CAGR because variable-rate technology cuts chemical use and meets drift regulations.

Why is Mexico recording the highest growth rate?

Government precision-equipment subsidies and export horticulture expansion push Mexico’s CAGR to 5.9% through 2030.

What impact do autonomous retrofit kits have on equipment demand?

Kits priced at USD 50,000–USD 150,000 let farms extend tractor life and unlock supervised autonomy, shortening payback periods to under three years.

Are electric tractors commercially viable today?

They work best in dairy and orchard settings with short duty cycles, and battery costs are projected to reach parity with diesel models by 2027.

Page last updated on: