Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 57.5 Billion |

| Market Size (2031) | USD 76.57 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Agricultural Machinery Market Analysis by Mordor Intelligence

The North America agricultural machinery market is expected to grow from USD 54.3 billion in 2025 to USD 57.5 billion in 2026 and is forecast to reach USD 76.57 billion by 2031 at 5.9% CAGR over 2026-2031. The expansion reflects persistent mechanization demand despite elevated interest rates and commodity price swings that limited capital spending in 2024. Structural labor shortages, federal subsidy programs that encourage fleet renewal, and rapid precision-ag adoption continue to underpin equipment orders. Autonomous capabilities showcased at Consumer Electronics Show (CES) 2025 are accelerating early replacement cycles because farms now weigh software compatibility on par with horsepower. Simultaneously, irrigation modernization, especially in water-stressed Mexico, widens the addressable base for specialized equipment makers. Competitive dynamics remain intense as leading OEMs bundle embedded finance, software subscriptions, and dealer support to retain customers and stabilize revenue.

Key Report Takeaways

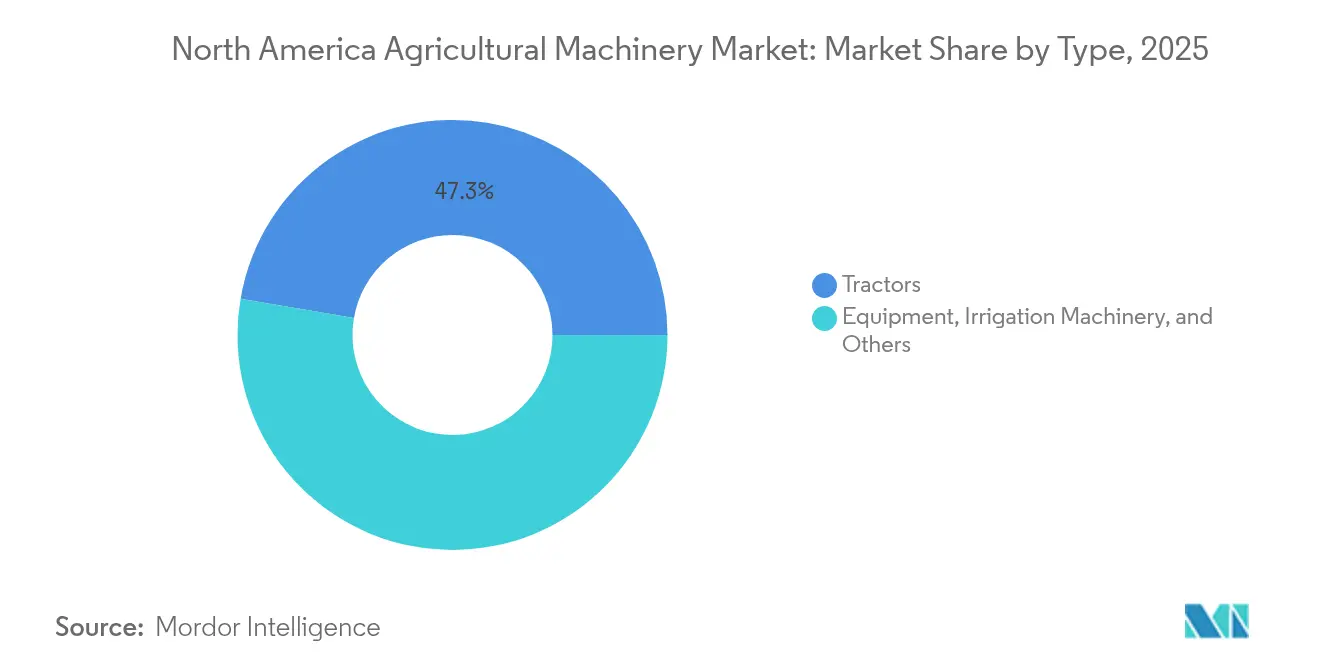

- By type, tractors led with 47.30% revenue share of the North America agricultural machinery market in 2025. Whereas irrigation machinery is projected to post the fastest 13.4% CAGR through 2031.

- By geography, the United States accounted for 61.40% of the North American agricultural machinery market share in 2025, whereas Mexico is poised to expand at a 7.6% CAGR through 2031.

- By company, Deere and Company commanded the majority share in 2024, while the top five OEMs collectively accounted for over half of the regional sales.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust farm-income outlook and subsidy programs | +1.8% | United States and Canada | Medium term (2-4 years) |

| Rising labor scarcity and wage inflation | +1.5% | North America-wide | Long term (≥ 4 years) |

| Precision-ag adoption is accelerating equipment replacement | +1.2% | United States and Canada | Medium term (2-4 years) |

| OEM embedded-finance boosts purchasing power | +0.9% | North America-wide | Short term (≤ 2 years) |

| Subscription-based machinery access models | +0.6% | United States and Canada | Long term (≥ 4 years) |

| USDA Climate-Smart grants driving low-emission equipment | +0.7% | The United States primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Farm-Income Outlook and Subsidy Programs

Federal depreciation allowances and direct grants keep capital budgets resilient. The USDA Climate-Smart Commodities program alone has allocated more than USD 3 billion since 2024 for equipment that lowers emissions and improves efficiency[1]Source: USDA, “Climate-Smart Commodities Grants,” usda.gov. Section 179 rules allow deductions up to USD 1.16 million per tax year, offsetting higher borrowing costs. Mid-sized growers respond by front-loading purchases to capture both grant and tax benefits. Dealer feedback indicates stronger demand for mid-horsepower tractors equipped with telematics that document sustainability metrics required for grant compliance. As a result, the North America agricultural machinery market enjoys a predictable baseline of subsidized orders that cushions cyclical demand dips.

Rising Labor Scarcity and Wage Inflation

Rural workforce participation keeps falling, which pushes farms to mechanize tasks once handled manually. Mexico’s crop yield setbacks in 2024 underscore how labor shortages can throttle production. Autonomous sprayers and robotic harvest aids reduce field crews and curb escalating wages that now outstrip general inflation. OEM demonstrations prove that integrated machine-vision lowers chemical use, which further offsets labor costs. Grain-elevator operators also automate with AI-enabled sensors that let facilities run at night without staff oversight. Persistent worker scarcity, therefore, sustains long-term demand for advanced equipment across the region.

Precision-Agriculture Adoption Accelerating Equipment Replacement

Software-driven agronomy tools make older machines obsolete faster than mechanical wear once did. John Deere’s See and Spray subscription, priced at roughly USD 4 per acre, delivered chemical savings of 8 million gallons during the initial field rollout. Farms willing to pay per-acre fees are also choosing newer iron with integrated processors that support over-the-air updates. This behavior shortens replacement intervals from 10–12 years to 7–8 years, thereby lifting annual unit sales. Retrofit kits remain popular, yet many growers decide a full tractor upgrade offers better long-term value once autonomy enters the equation.

USDA Climate-Smart Grants Driving Low-Emission Equipment

Grant criteria favor electrified or fuel-efficient models, nudging buyers toward battery tractors and hybrid drives. Deere’s autonomous tillage prototype operates at lower RPM and promises material fuel savings[2]Source: Shane Thomas, “John Deere 2024 Annual Report Highlights and Analysis,” Upstream Ag, upstream.ag. OEM pipelines increasingly feature alternative-power options to capture grant-driven orders. Although battery-grade semiconductor supply remains tight, funded pilot programs prove technical feasibility and set the stage for broader commercialization after 2027.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs of advanced machinery | -1.1% | North America-wide | Long term (≥ 4 years) |

| Volatile commodity prices curbing CAPEX cycles | -0.8% | North America-wide | Short term (≤ 2 years) |

| Interest-rate-driven credit tightening at farm level | -0.9% | United States and Canada | Medium term (2-4 years) |

| Battery-grade semiconductor supply constraints for e-tractors | -0.4% | North America-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Maintenance Costs of Advanced Machinery

A high-horsepower tractor exceeded USD 400,000 in 2024, while precision retrofits add USD 50,000–100,000 per unit. Total ownership costs climb further because modern engines and software demand specialized technicians that remain scarce. Nearly 87% of dealers struggle to hire qualified service staff[4]Source: DIS Corp, “DIS 2024 Agriculture Industry Trends Report,” publications.discorp.com . Extended warranties and service contracts ease uncertainty, yet they add another USD 15,000–25,000 to the purchase price. Many producers, therefore, refurbish decade-old machines, which postpones technology upgrades and raises fuel consumption during critical field windows. As a result, small and mid-sized farms often delay purchases until late-season discounting emerges, compressing dealer margins and extending replacement cycles.

Volatile Commodity Prices Curbing CAPEX Cycles

Corn prices swung between USD 4.20 and USD 5.80 per bushel in 2024. Similar variability for soybeans created income uncertainty. Growers respond by postponing machinery investments until markets stabilize, causing boom-bust ordering patterns that complicate OEM production planning. Dealers end up carrying high inventory during soft cycles, which pressures margins and leads to discounting. Although hedging tools exist, many growers lack margin capacity to lock in prices through futures contracts, leaving cash positions exposed. Line shutdowns and overtime surges at factories further elevate cost structures, which ultimately pass through to end buyers in subsequent years.

Segment Analysis

By Type: Tractors Lead while Irrigation Gains Speed

Tractors maintained a 47.30% share of the North America agricultural machinery market in 2025, underscoring their central role across crop operations. The segment benefits from autonomous retrofits tested on 50,000 acres, validating real-world uptime and lowering skepticism about driverless tillage. Yet irrigation machinery, supported by water-scarcity mitigation projects, is projected to register a 13.4% CAGR through 2031, outpacing every other equipment class. The North America agricultural machinery market size for irrigation equipment is forecast to show a significant growth during the period as center-pivot conversions accelerate in Mexico.

Secondary categories such as plows and cultivators grow modestly because precision tech shifts demand toward variable-rate applications. In harvesting, integrated grain-quality sensors and yield mapping push farms to upgrade combines earlier than the traditional 6-year cycle. Haying and forage machinery benefits from dairy and beef expansion in the Upper Midwest and Canadian Prairies, while the other types bucket now covers autonomous robots that perform weeding, spot spraying, and soil monitoring. Kubota’s KATR robot exemplifies a multifunctional design that blurs traditional equipment lines.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United States holds a 61.40% revenue share in 2025 on the back of high-capacity machinery demand and mature dealer coverage. Replacement cycles hinge on integrating GPS guidance, variable-rate systems, and autonomy. Although interest rates restrained purchases in 2024, USDA grants and Section 179 deductions partially offset financing costs. Dealers employ combined roll programs that buy back older machines, smoothing customer cash flow. The North America agricultural machinery market remains closely tied to U.S. policy that supports climate-smart agriculture.

Canada mirrors U.S. patterns yet contends with vast distances that elevate logistics costs. Kubota Canada topped all dealer satisfaction metrics except product availability in 2024, proving that support quality directly influences brand preference. Seasonal peaks create intense demand for service technicians each fall, which magnifies downtime risk. Currency fluctuations also affect import prices since most equipment arrives from U.S. factories or via U.S. distribution arms.

Mexico represents the most dynamic growth node and is poised to expand at a 7.6% CAGR through 2031. Drought affected 65% of municipalities in 2024, pressuring authorities to modernize irrigation. Government programs link smallholders to credit lines that finance drip and pivot systems. OEMs like Lindsay see international bookings rise in Mexico. Trade integration under USMCA simplifies cross-border shipment of parts and machines, thereby lowering lifetime service costs and boosting adoption.

Competitive Landscape

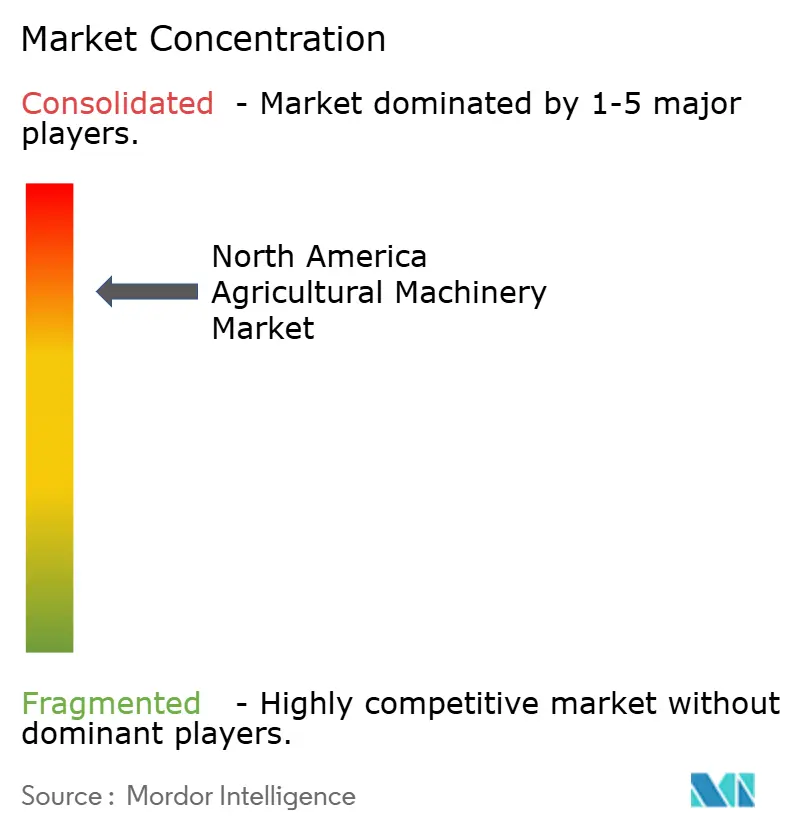

Market concentration is high as the top five OEMs command a monopolitic share of revenue. Deere and Company leads with the majority share, followed by CNH Industrial, AGCO, Kubota, and CLAAS. Competitive focus has shifted from mechanical specs to digital ecosystems. Deere promotes a per-acre SaaS model, CNH bundles Raven autonomy, and AGCO leverages its joint venture with Trimble for a mixed-fleet open platform.

Smaller brands differentiate through customer intimacy. Kubota achieved the highest NAEDA dealer satisfaction and used CES 2025 to spotlight its electric tractor lineup. CLAAS reorganized Dakota's distribution to increase direct touchpoints while Butler Machinery supplies parts during the transition. Embedded finance strategies continue to create entry barriers for startups, but subscription-based access models like MachineryLink Sharing chip away at ownership orthodoxy by monetizing idle capacity.

Innovators in field robotics and sensing increasingly partner with OEMs. Autonomous implement specialists integrate onto existing tractor platforms to accelerate commercialization. Precision-ag software houses expand revenue by selling application-specific modules that run on cab displays regardless of brand, which could erode lock-in over time.

North America Agricultural Machinery Industry Leaders

Deere & Company

AGCO Corporation

CLAAS Group

CNH Industrial (Case IH & New Holland)

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: John Deere unveiled comprehensive autonomous agriculture solutions at CES 2025, including fully autonomous tillage systems currently being tested across 50,000 acres with 12 customers, and retrofit capabilities for 8 Series and 9 Series tractors with low upfront pricing and per-acre monetization models. These launches signal Deere’s intent to embed software-as-a-service revenues into core equipment sales while demonstrating field-proven fuel savings that resonate with large row-crop producers.

- January 2025: Kubota North America showcased multiple advanced equipment concepts at CES 2025, including the Agri Concept 2.0 electric tractor with autonomous functions, a Smart Autonomous Sprayer for precision chemical application, and the KATR four-wheeled all-terrain robot that won the CES 2025 Best of Innovation award. The exhibit positions Kubota as a technology challenger by pairing compact-equipment heritage with electrification and robotics aimed at mid-sized farms.

- January 2025: CLAAS and Butler Machinery announced a strategic reorganization of sales coverage in the Dakotas, with CLAAS establishing new dealerships to offer its full product line while Butler continues service and parts support through December 2026. The staged handover reduces customer disruption and expands CLAAS’s direct market reach at a time when growers seek multi-brand support under one roof.

- April 2024: Kverneland introduced a comprehensive 0% finance promotion for business customers on new equipment through BNP Paribas Leasing Solutions, offering multiple payment structures including 1+11 monthly plans at 0% APR and extended terms up to 3+33 months at competitive rates. The program illustrates how OEM-subsidized financing can counteract rising benchmark rates and keep purchasing pipelines active.

North America Agricultural Machinery Market Report Scope

The agricultural machinery industry is considered a part of the machinery industry that comprises the manufacturing of machinery required to support agriculture.

The North American agricultural machinery market is segmented by type (tractors, equipment, irrigation machinery, harvesting machinery, haying and forage machinery, and other types) and geography (United States, Canada, Mexico, and Rest of North America). The report offers market sizes and forecast in terms of value (USD million) for the above-mentioned segments.

By Type

| Tractor | Less Than 40 HP |

| 40 to 100 HP | |

| More than 100 HP | |

| 4WD Tractors | |

| Equipment | Plows |

| Harrows | |

| Cultivators and Tillers | |

| Other Equipment | |

| Irrigation Machinery | Sprinkler |

| Drip | |

| Other Irrigation | |

| Harvesting Machinery | Combine Harvesters |

| Forage Harvesters | |

| Other Harvesting | |

| Haying and Forage Machinery | Mowers |

| Balers | |

| Other Haying and Forage | |

| Other Types |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Tractor | Less Than 40 HP |

| 40 to 100 HP | ||

| More than 100 HP | ||

| 4WD Tractors | ||

| Equipment | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Equipment | ||

| Irrigation Machinery | Sprinkler | |

| Drip | ||

| Other Irrigation | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Other Harvesting | ||

| Haying and Forage Machinery | Mowers | |

| Balers | ||

| Other Haying and Forage | ||

| Other Types | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large is the North America agricultural machinery market in 2026?

The market reached USD 57.5 billion in 2026 and is forecast to expand to USD 76.57 billion by 2031.

What is the expected CAGR for agricultural machinery demand in North America?

The compound annual growth rate is projected at 5.9% through 2031.

Which equipment type commands the largest revenue share?

Tractors hold the top spot with 47.30% share in 2025, reflecting their versatility across operations.

Why is irrigation machinery growing faster than other segments?

Water-scarcity mitigation efforts, especially in Mexico under the National Water Plan 2024-2030, drive a 13.4% CAGR for irrigation equipment.

Who are the leading OEMs in the region?

Deere and Company, CNH Industrial, AGCO, Kubota, and CLAAS together control majority of the market.

How do USDA Climate-Smart grant influence equipment purchases?

Grants subsidize low-emission machinery, effectively lowering acquisition costs and accelerating adoption of electric or fuel-efficient models.

Page last updated on: