Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

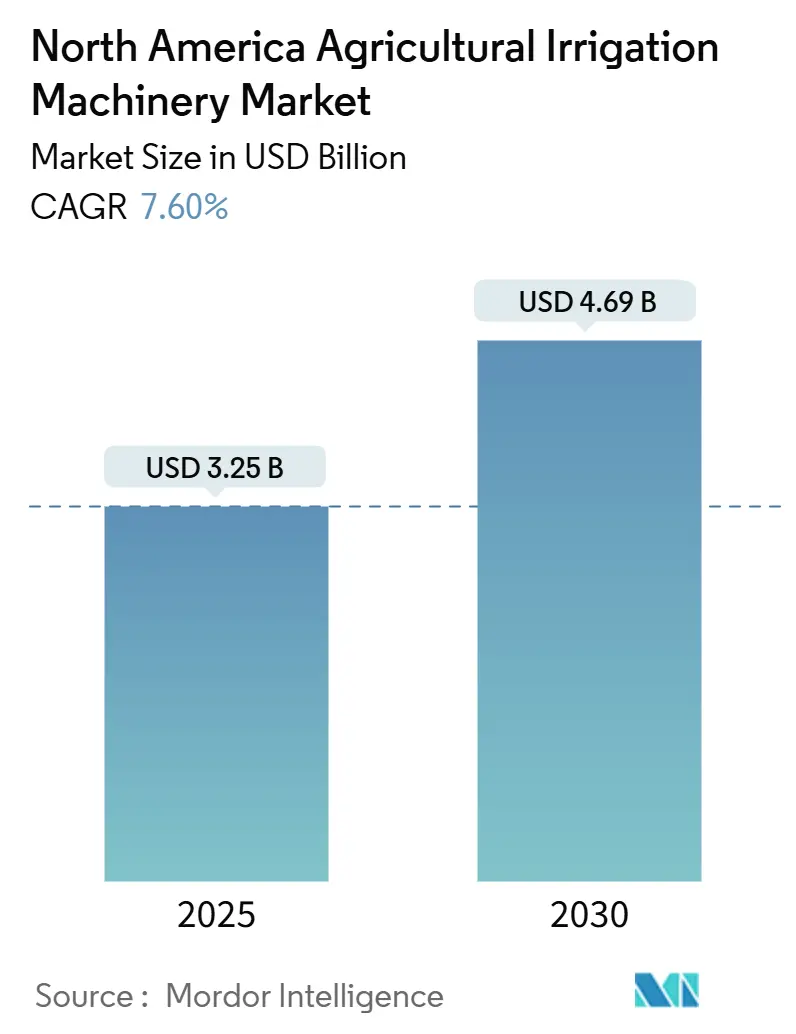

| Market Size (2025) | USD 3.25 Billion |

| Market Size (2030) | USD 4.69 Billion |

| Growth Rate (2025 - 2030) | 7.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Agricultural Irrigation Machinery Market Analysis by Mordor Intelligence

The North America agricultural irrigation machinery market size stands at USD 3.25 billion in 2025 and is projected to climb to USD 4.69 billion by 2030, reflecting a 7.60% CAGR. Robust public-funding streams, rising water scarcity in the High Plains Aquifer, and stricter efficiency mandates in California are underpinning this expansion. Growers are replacing gravity systems with pressurized pivot, sprinkler, and drip technologies that embed real-time soil-moisture sensors and variable-rate algorithms, lowering water application on commercial row-crop operations [1]Source: USDA Natural Resources Conservation Service, “Environmental Quality Incentives Program,” nrcs.usda.gov. Government incentives, notably Environmental Quality Incentives Program allocation for fiscal 2025, compress payback periods to fewer than five seasons for many retrofits. Meanwhile, digital-twin design tools shave engineering cycles and reduce installation errors. Competitive pressure is elevating software integration, with edge-Artificial intelligence (AI) predictive-maintenance modules now standard on new pivots and drip controllers, cutting unplanned downtime. Policy momentum in Mexico, to modernize 50,000 hectares, signals a region-wide shift toward mechanized irrigation.

Key Report Takeaways

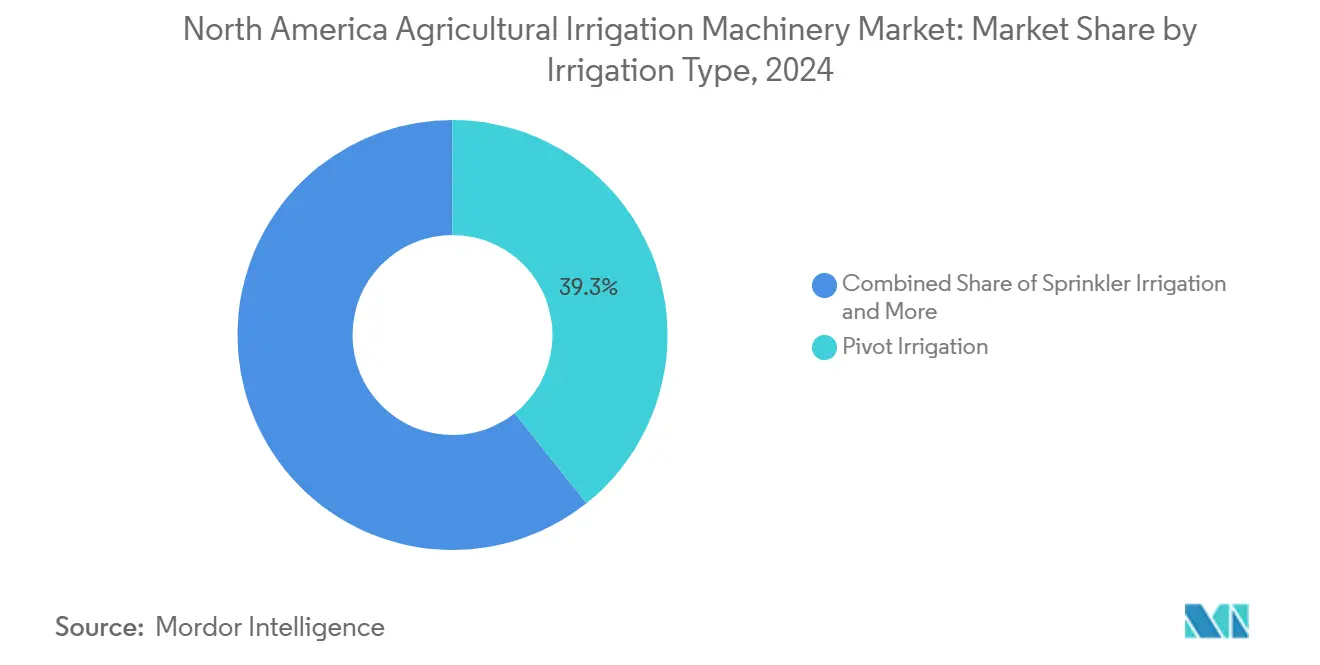

- By irrigation type, pivot systems led with a 39.3% share of the North America agricultural irrigation machinery market in 2024, while drip-sensor solutions are advancing at a 12.4% CAGR through 2030.

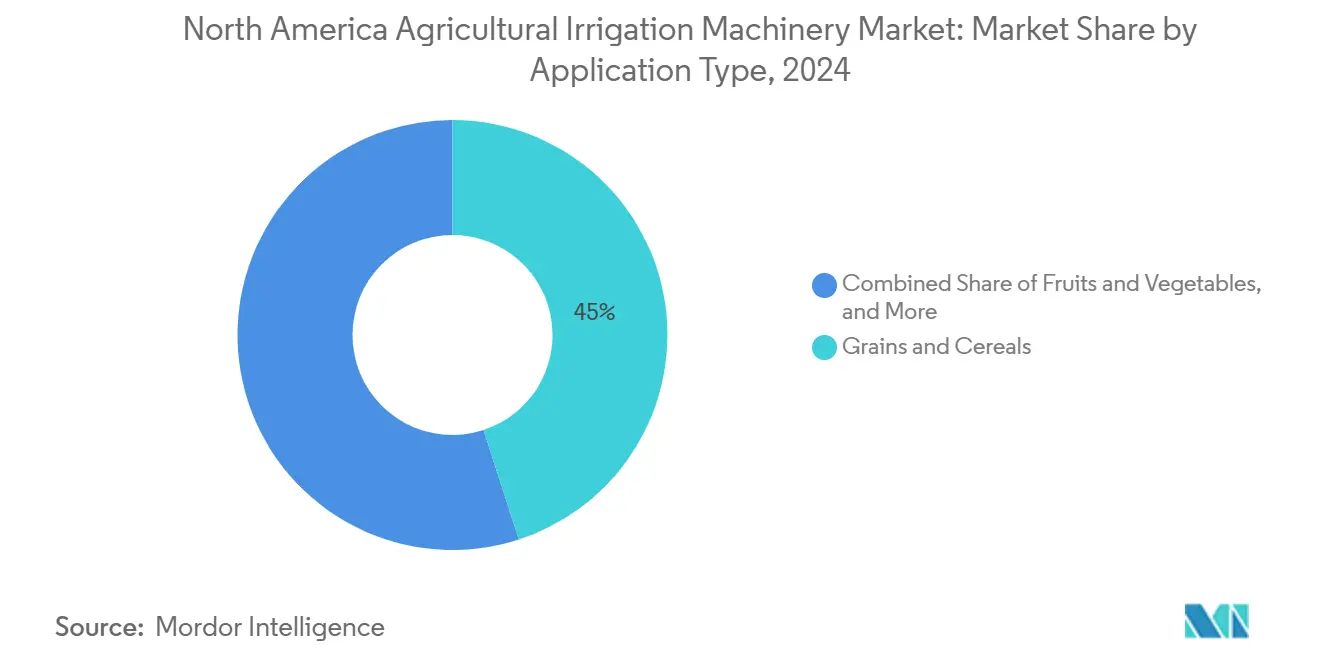

- By application type, grains and cereals accounted for 45% of the North America agricultural irrigation machinery market size in 2024, whereas fruits and vegetables are forecast to expand at a 10.6% CAGR to 2030.

- By geography, the United States held 68% of the North America agricultural irrigation machinery market share in 2024, while Mexico is projected to log the fastest 9.1% CAGR between 2025 and 2030.

North America Agricultural Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-twin enabled design optimization | +1.2% | United States (High Plains, Corn Belt), Western Canada | Medium term (2-4 years) |

| Increasing area under irrigation | +1.8% | United States (Nebraska, Kansas, Texas), Canadian Prairies, Northern Mexico | Long term (≥ 4 years) |

| Government support to enhance mechanized irrigation | +2.1% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Climate-resilience funding tied to smart irrigation | +0.9% | United States, and Mexico | Medium term (2-4 years) |

| Adoption of new technological irrigation methods | +1.5% | United States, and Mexico | Medium term (2-4 years) |

| Edge-Artificial Intelligence (AI) based predictive maintenance lowers OPEX | +0.7% | United States, and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-Twin Enabled Design Optimization

Virtual modeling platforms shorten center-pivot retrofit planning from weeks to days, trimming engineering outlays by as much as 18%. The CropTwin project, with heavy funding in 2024, uses soil maps, weather forecasts, and crop coefficients to simulate nozzle packages before hardware is ordered. Growers in Nebraska and Kansas report that the software highlights pressure bottlenecks and span mismatches overlooked during manual sizing, preventing yield loss tied to uneven distribution. Variable-rate retrofits benefit most because correct zone mapping is critical for water savings. As manufacturers embed these simulators into customer portals, mid-sized farms with limited technical staff gain affordable access to advanced design capability.

Increasing Area Under Irrigation

The United States Department of Agriculture (USDA) data show a gradual expansion of irrigated acreage in the High Plains and Mississippi Delta, while Canadian programs subsidize up to 50% of new irrigation districts in Alberta and Saskatchewan [2]Source: Agriculture and Agri-Food Canada, “Programs and Services,” agriculture.canada.ca. Mexico’s northern states are phasing out flood irrigation in favor of pressurized systems eligible for Conagua subsidies, boosting equipment demand despite higher upfront costs. Producers view irrigation infrastructure as insurance against erratic rainfall. Even with elevated interest rates, many operations stretch repayment schedules because stabilized yields support long-term profitability.

Government Support to Enhance Mechanized Irrigation

Federal and provincial incentives compress the return-on-investment period below five years for many upgrades. The Environmental Quality Incentives Program (EQIP) covers 50% to 75% of drip conversions and variable-rate retrofits, while Alberta’s programs lower district infrastructure costs, and Mexico’s subsidies cover up to 70% for ejido cooperatives. These programs de-risk private capital, accelerating the retirement of gravity systems. Dealers bundle financing packages with cost-share paperwork assistance, simplifying adoption for smaller farms.

Climate-Resilience Funding Tied to Smart Irrigation

Carbon-credit protocols reward farms that verify water and energy savings. United States Department of Agriculture (USDA) pilots allow producers to bank credits for diesel and electricity reductions achieved through the Internet of Things (IoT)-enabled irrigation. Private registries such as Verra publish methodologies quantifying avoided groundwater extraction. Manufacturers embed data loggers and telemetry modules into controllers, generating audit trails for credit validation. Demand is strongest in California and the Midwest, where buyers pay premiums for sustainability-certified crops.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High investment and maintenance costs | -1.4% | United States, and Mexico | Short term (≤ 2 years) |

| Complex functioning of high-tech systems | -0.8% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Scarcity of skilled irrigation technologists | -0.6% | Canada, and United States | Long term (≥ 4 years) |

| Cyber-security risks in connected irrigation assets | -0.4% | United States, and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Investment and Maintenance Costs

Modern drip systems cost USD 1,000 to USD 3,000 per acre, while pivots can range from USD 50,000 to USD 150,000 depending on span length and automation features. Annual upkeep averages 4% of capital value, a heavy burden for farms operating on slim margins. Conagua subsidies reduce acquisition costs for Mexican smallholders but do not offset recurring expenses such as filter cleaning and electricity bills. When grain prices soften, payback timelines lengthen, deterring upgrades.

Scarcity of Skilled Irrigation Technologists

Installer vacancies exceed seven months in rural Canadian provinces and the United States Great Plains. Community-college enrollment in agricultural mechanics programs is falling, and many technicians retire without replacements. Manufacturers respond by dispatching factory crews, adding cost and time. Labor shortages particularly hinder installation peaks in spring.

Segment Analysis

By Irrigation Type: Pivot Dominance Meets Drip-Sensor Acceleration

Pivot irrigation held a 39.3% share of the North America agricultural irrigation machinery market in 2024, reflecting its fit with large-scale row-crop geometry. Variable-rate retrofits, which swap fixed nozzles for zone-controlled heads, are adding momentum. Drip-sensor solutions remain the fastest rising subsegment at a 12.4% CAGR, buoyed by California distribution uniformity mandates and permanent-crop adoption. Tubing, filters, and pressure regulators dominate component sales, while pressure-compensating emitters cut maintenance intervals. Traveling guns and solid-set systems capture the balance of niche demand in sod and nursery operations.

Valmont’s Valley brand saw the pivot revenue decline in the third quarter of 2024, but the firm invested significantly to expand variable-rate pivot production, signaling long-term confidence. Flow meters and telemetry modules are now standard to satisfy water-reporting rules in Ogallala Aquifer counties. Solar-hybrid pumps and variable-frequency drives lower operating electricity costs, while retrofit kits extend service life for aging pivots. Edge-computing panels record run-time data, enabling growers to claim carbon credits for energy savings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application Type: Grains Anchor Demand, Fruits and Vegetables Drive Growth

Grains and cereals represented 45% of the North America agricultural irrigation machinery market size in 2024, supported by corn, wheat, and soybean acreage across the Corn Belt and Canadian Prairies. This segment advances as producers convert dryland acres to pivots for yield stability. Fruits and vegetables, although smaller, grow the fastest at 10.6% CAGR, propelled by California specialty crops, Florida citrus, and Mexico’s berry and avocado exports that require precise fertigation to meet retailer standards. Pulses and oilseeds offer niche opportunities, especially in rotations aimed at soil health.

California’s Sustainable Groundwater Management Act drives almond and pistachio growers toward subsurface drip monitored for extraction limits. Mexico’s berry exporters install drip to satisfy GlobalGAP audits. Toro’s micro-irrigation division reported revenue gains as specialty farms seek pressure-compensating emitters tailored to crop physiology [3]Source: The Toro Company, “Investor Materials,” investors.thetorocompany.com . Divergent regulatory thresholds between grains and horticulture create contrasting equipment demand patterns.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States remained the anchor geography, holding 68% of the North America agricultural irrigation machinery market share in 2024. United States Department of Agriculture Environmental Quality Incentives Program (USDA EQIP) funding and conservation mandates fuel steady replacement of gravity systems. California’s Model Water Efficient Landscape Ordinance compels new installations to embed flow sensors and pressure-compensating emitters, accelerating drip adoption. Despite softer farm-equipment purchases in 2024 attributed to higher interest rates, pivot makers Lindsay and Valmont are expanding digital-twin design and remote-monitoring platforms to capture precision-irrigation demand.

In Canada, provincial cost-share schemes under Alberta’s Irrigation Rehabilitation and Expansion Program subsidize half the capital costs for pivots and drip laterals. Producers in Saskatchewan and Alberta view irrigation as a hedge against yield volatility linked to erratic precipitation. Longer equipment lifecycles and remote farm locations raise service expectations, spurring manufacturers to train dealers and deploy mobile fleets.

Mexico shows the fastest 9.1% CAGR as Conagua’s Programa de Tecnificación de Riego funds modernization of 50,000 hectares, covering 50% to 70% of equipment costs for ejidos and smallholders. Export-oriented berry, avocado, and vegetable sectors seek drip and micro-irrigation to meet GlobalGAP and Rainforest Alliance certifications. Manufacturers with local supply chains, such as Netafim’s Fresno plant, reduce delivery lead times by 30% to serve this expansion. The rest of North America, including Central American nations, remains small but is exploring subsidy-driven models for coffee and banana drip systems.

Competitive Landscape

The North America agricultural irrigation machinery market remains moderately concentrated, with the top five firms controlling a significant share of 2024 revenue. Lindsay Corporation, Valmont Industries, Inc., Deere & Company, The Toro Company, and Netafim Ltd. command extensive dealer networks and broad portfolios. Competitive parity is shifting toward software integration, with all major players embedding cloud platforms that bundle design, scheduling, and maintenance analytics. White-space niches include variable-rate retrofit kits for legacy pivots, solar-hybrid pumps tied to carbon credits, and turnkey service bundles that offset the shortage of skilled technologists.

Valmont Industries, Inc.’s USD 15 million line expansion focuses on variable-rate pivots that meet state water-reporting mandates, while Netafim Ltd.’s USD 20 million Fresno plant localizes drip-tube extrusion to slash lead times. Lindsay Corporation’s FieldNET Advisor 2.0 integrates predictive maintenance that forecasts pump failures 14 days out, reducing costly downtime. Deere & Company leverages its precision-ag suite to bundle irrigation assets with See and Spray weed-control and ExactApply nozzle technologies, appealing to large enterprises seeking unified data ecosystems.

Smaller entrants combat scale disadvantages by specializing in the Internet of Things (IoT) sensors and decision-support algorithms that retrofit across diverse equipment fleets. Precision-agriculture firms such as CropX Technologies Ltd, Trimble Inc., and Pessl Instruments GmbH are capturing share by offering subscription-based scheduling that integrates with multiple hardware brands, enabling growers to avoid vendor lock-in. Cyber-security is now a differentiator, manufacturers scramble to harden firmware and add over-the-air updates after a ransomware incident underscored the vulnerability of connected pivots.

North America Agricultural Irrigation Machinery Industry Leaders

-

Valmont Industries.

-

Lindsay Corporation

-

Deere & Company

-

The Toro Company

-

Netafim Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: CropX has acquired Nebraska's CropMetrics, a leading provider of cloud-based precision irrigation tools. With this acquisition, partners and customers of both CropMetrics and CropX gain access to a unique blend of in-soil data, sophisticated farm management analytics, and enhanced decision-support tools.

- February 2025: Netafim USA, headquartered in Fresno, has introduced its FlexNet Medium Pressure Pipes, aiming to enhance the efficiency, durability, and reliability of water distribution. Unlike conventional lay-flat irrigation pipes, which are susceptible to leaks and demand intensive labor for installation, FlexNet offers farmers a 20-30% reduction in labor costs and significantly cuts down installation times.

- January 2024: Lindsay Corporation has launched an upgraded user interface for its FieldNET platform. This platform serves as a remote monitoring and control solution for all brands of center pivot irrigation. With the enhancements, farmers can now benefit from routine monitoring, extending to advanced agronomic recommendations for irrigation.

North America Agricultural Irrigation Machinery Market Report Scope

By Irrigation type

| Sprinkler Irrigation | Pumping Unit |

| Injectors | |

| Sensors | |

| Controllers | |

| Fittings and Accessories | |

| Spray/Sprinklers Heads | |

| Tubing | |

| Couplers | |

| Flow Meters | |

| Other Sprinkler Irrigations | |

| Drip Irrigation | Tubing |

| Backflow Preventers | |

| Pressure Regulators | |

| Emitters | |

| Valves | |

| Filters | |

| Other Drip Irrigations | |

| Pivot Irrigation | |

| Other Irrigation Types |

By Application Type

| Grains and Cereals |

| Fruits and Vegetables |

| Pulses and Oilseeds |

| Other Application Types |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Irrigation type | Sprinkler Irrigation | Pumping Unit |

| Injectors | ||

| Sensors | ||

| Controllers | ||

| Fittings and Accessories | ||

| Spray/Sprinklers Heads | ||

| Tubing | ||

| Couplers | ||

| Flow Meters | ||

| Other Sprinkler Irrigations | ||

| Drip Irrigation | Tubing | |

| Backflow Preventers | ||

| Pressure Regulators | ||

| Emitters | ||

| Valves | ||

| Filters | ||

| Other Drip Irrigations | ||

| Pivot Irrigation | ||

| Other Irrigation Types | ||

| By Application Type | Grains and Cereals | |

| Fruits and Vegetables | ||

| Pulses and Oilseeds | ||

| Other Application Types | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the North America agricultural irrigation machinery market by 2030?

The market is forecast to reach USD 4.69 billion by 2030 at an 7.60% CAGR.

Which irrigation type is growing the fastest in North America?

Pivot irrigation solutions are advancing at a 7.8% CAGR through 2030, driven by specialty-crop adoption and efficiency mandates.

How much public funding supports United States irrigation upgrades in 2025?

United States Department of Agriculture Environmental Quality Incentives (USDA EQIP) Program has allocated USD 7.7 billion for conservation practices in fiscal 2025, with irrigation efficiency a major category.

Why is Mexico the fastest-growing geography for irrigation machinery?

Conagua’s Programa de Tecnificación de Riego covers up to 70% of equipment costs, accelerating adoption among berry, avocado, and vegetable growers.

What technology trend is reducing unplanned irrigation downtime?

Edge-Artificial intelligence (AI) predictive-maintenance modules detect pump and gearbox issues up to 14 days before failure, lowering downtime by 11%.

Page last updated on: