Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

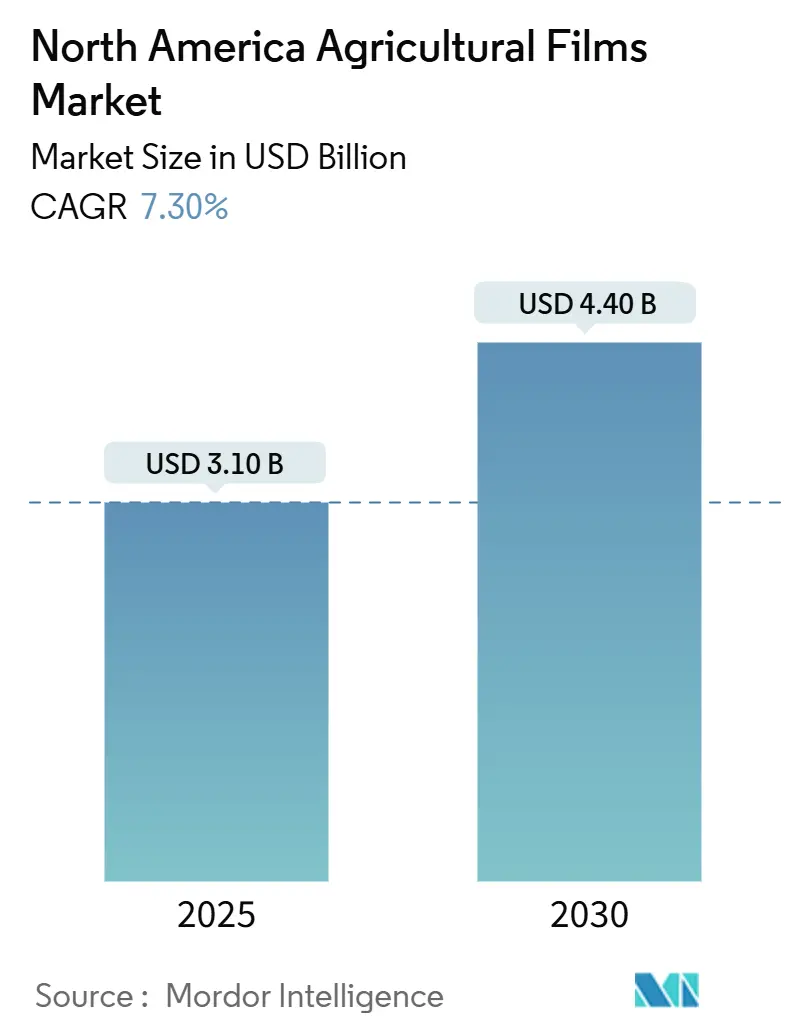

| Market Size (2025) | USD 3.10 Billion |

| Market Size (2030) | USD 4.40 Billion |

| Growth Rate (2025 - 2030) | 7.30% CAGR |

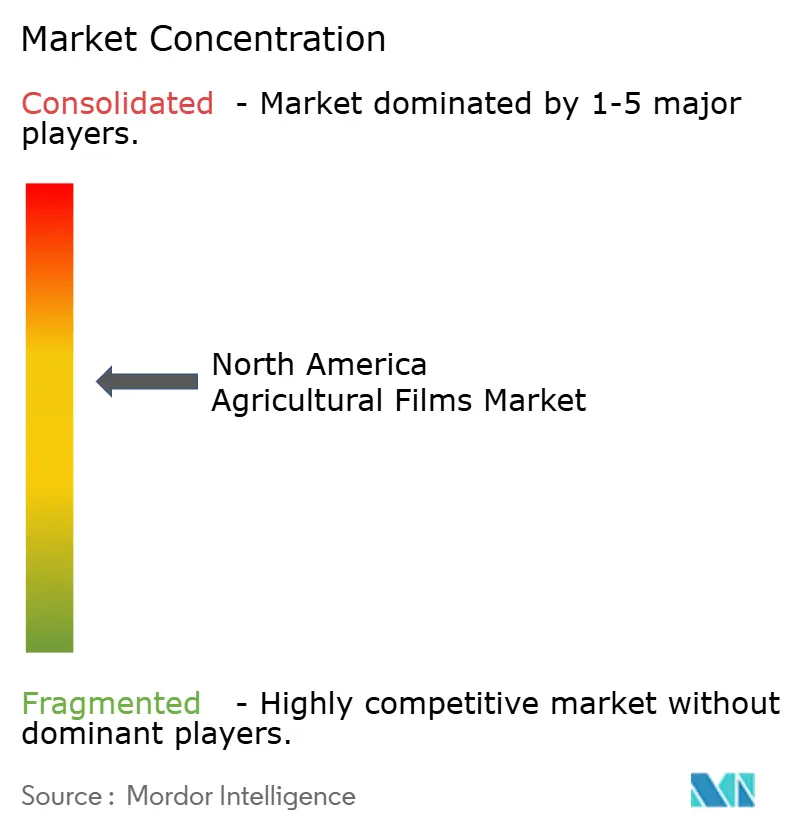

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Agricultural Films Market Analysis by Mordor Intelligence

North America agricultural films market size is USD 3.10 billion in 2025 and is forecast to advance at a 7.30% compound annual growth rate (CAGR) to USD 4.40 billion by 2030, reflecting robust adoption of plastic film technologies that help growers raise yields on shrinking arable land. Accelerated greenhouse construction, larger dairy operations that require silage wrap, and expanding precision agriculture all reinforce steady demand, while corporate net-zero targets create price premiums for recycled-content products. Plastic resin majors are integrating vertically to secure ethylene supply and recycled feedstock, because volatile raw-material costs threaten margins and state rules on plastic waste tighten each year. Mexico’s public farm-modernization budget, Canada’s controlled-environment boom, and shifting weather patterns in the United States combine to keep the growth profile balanced across the region. The market still contends with logistics gaps in agricultural-film recycling and heterogeneous rules on single-use plastics that complicate inventory planning.

Key Report Takeaways

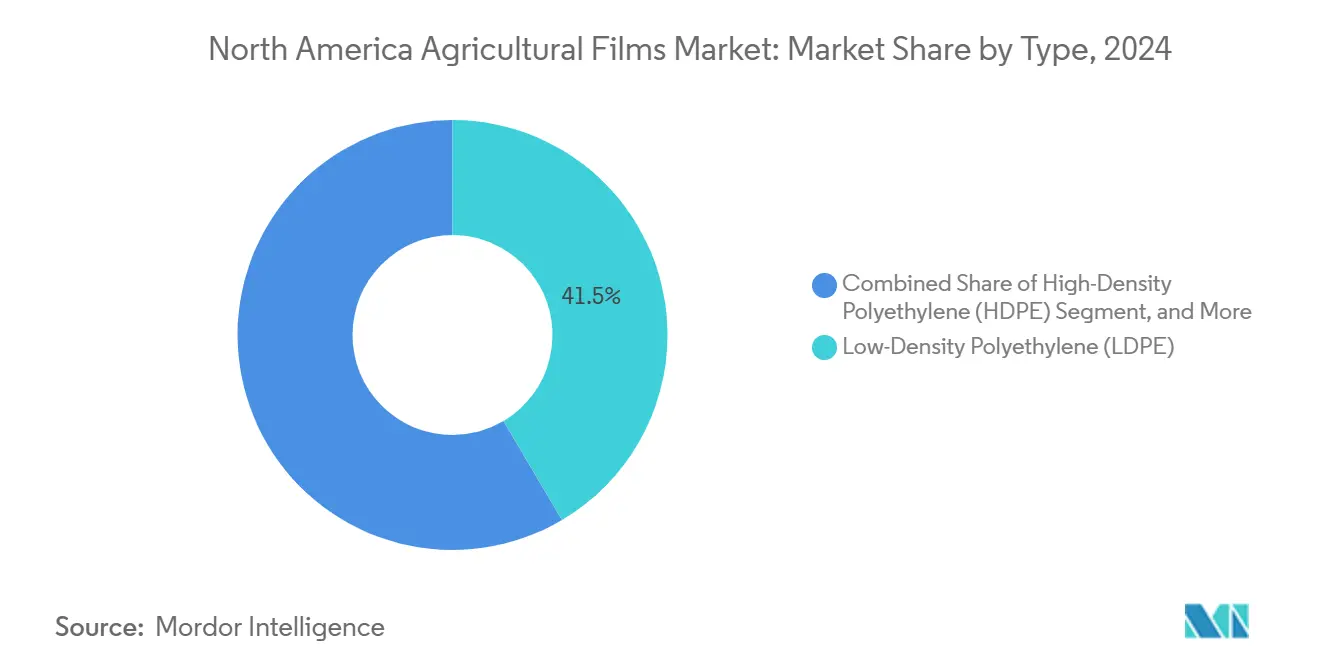

- By type, low-density polyethylene maintained a 41.5% North America agricultural films market share in 2024, but recycled films are forecast to expand at a 10.20% CAGR during the same period.

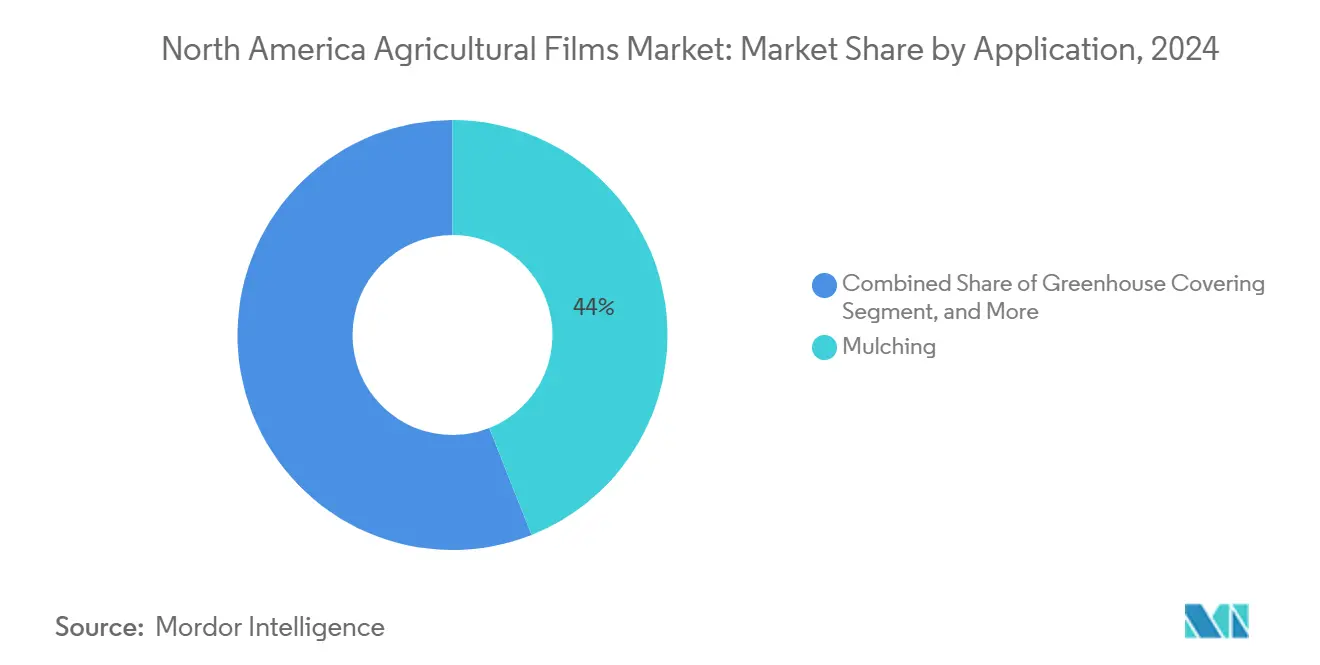

- By application, mulching films accounted for 44.0% of the North America agricultural films market size in 2024, while silage and bale wrap are poised to grow at an 8.10% CAGR to 2030.

- By thickness, films up to 80 microns led with 58.0% revenue share in 2024, whereas films above 150 microns are projected to post the fastest 9.2% CAGR through 2030.

- By geography, the United States held a 67.0% share of the North America agricultural films market in 2024, while Mexico is projected to register the fastest 7.50% CAGR through 2030.

- Key players in the market include Amcor plc, Dow Inc., BASF SE, Exxon Mobil Corporation, and RKW Group that are moderately concentrated.

North America Agricultural Films Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing need to maximize yields on shrinking arable land | +1.2% | Global, with concentration in US Midwest and Canadian Prairies | Medium term (2-4 years) |

| Expansion of controlled-environment agriculture and vertical greenhouses | +0.9% | North America, with early gains in Ontario, California, and Texas | Long term (≥ 4 years) |

| Rising silage demand from large-scale dairy operations | +0.7% | US Dairy Belt, Eastern Canada, and Northern Mexico | Short term (≤ 2 years) |

| Corporate net-zero pledges accelerating demand for recyclable films | +0.8% | North America and EU, spill-over to Mexico | Medium term (2-4 years) |

| Adoption of smart, UV-selective films integrating IoT sensors | +0.5% | US and Canada, limited Mexico penetration | Long term (≥ 4 years) |

| State incentives for compostable mulch film trials | +0.3% | California, Washington, and Oregon primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing need to maximize yields on shrinking arable land

Agricultural intensification drives film adoption as farmers confront the dual challenge of feeding growing populations while losing productive acreage to urbanization and climate impacts. Farmland conversion has accelerated since 2020, prompting growers to deploy mulch films that can lift specialty-crop yields 15-25% and cut water use up to 40%.[1]Source: Organisation for Economic Co-operation and Development, “Agricultural Policy Monitoring and Evaluation 2022,” oecd.org Multi-layer products regulate soil temperature and retain moisture, allowing multiple crop cycles each year despite higher climate volatility. These performance gains are attractive even when feedstock prices rise, because the incremental revenue per acre still offsets film costs.

Corporate net-zero pledges accelerating demand for recyclable films

Corporate sustainability commitments reshape procurement priorities as food companies establish recycled content targets and carbon reduction goals. Brand owners such as Amcor plc pledge 30% recycled content by 2030, cascading recycled-material targets down the supply chain. Chemical-recycling pilots promise contamination tolerance, opening a new outlet for used farm films. Although recycled resin costs exceed virgin prices, food companies pay premiums to validate environmental claims, sustaining double-digit growth in recycled films.

Adoption of smart, UV-selective films integrating IoT sensors

Precision agriculture adoption drives demand for intelligent film systems that integrate environmental monitoring and crop optimization capabilities. Ultraviolet-reflecting films that maximize photosynthetically active radiation generate documented yield gains in greenhouse vegetables.[2]Source: California Department of Food and Agriculture, “Healthy Soils Program Incentives,” cdfa.ca.gov Adding embedded humidity and temperature sensors permits real-time irrigation and ventilation control, but high unit costs restrict uptake to premium crops. Hardware prices are falling, which should broaden adoption from 2027 onward.

State incentives for compostable mulch film trials

California dedicated more than USD 10 million in Healthy Soils Program grants during 2024 for biodegradable mulch demonstrations. Subsidies defray the 50-100% price premium over standard polyethylene. Regulatory compliance with California's SB 54 plastic reduction mandates creates additional incentives for biodegradable film adoption in agricultural applications. The programs' limited geographic scope and budget constraints restrict broader market impact, though successful demonstrations could drive expanded funding and adoption.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent state bans on single-use plastics | -0.8% | California, New York, and Washington primarily | Short term (≤ 2 years) |

| Volatile ethylene feedstock prices | -0.6% | North America, with spillover effects globally | Short term (≤ 2 years) |

| Slow farm-level ROI on premium multi-layer films | -0.5% | US and Canada, limited Mexico impact | Medium term (2-4 years) |

| Recycling logistics gaps for contaminated agri-plastics | -0.4% | North America, with concentration in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent state bans on single-use plastics

California Senate Bill 54 requires a 25% cut in single-use plastics by 2032, and draft rules leave agricultural films in a gray area. New York and Washington in the United States pursue similar legislative frameworks that could restrict conventional polyethylene film usage in agricultural applications. Compliance costs and administrative burdens associated with producer responsibility organizations add operational complexity for film manufacturers and distributors. The regulatory patchwork across states creates market fragmentation that complicates distribution strategies and inventory management for national suppliers.

Volatile ethylene feedstock prices

Ethylene price volatility directly impacts agricultural film production costs, with feedstock representing 60-70% of total manufacturing expenses. Geopolitical tensions and supply chain disruptions create additional price uncertainty that film manufacturers struggle to pass on to price-sensitive agricultural customers. The industry's limited ability to hedge long-term feedstock costs creates margin pressure during periods of rapid price increases. Alternative feedstock sources, including bio-based ethylene from agricultural residues, offer potential price stability but remain economically uncompetitive at current scales.

Segment Analysis

By Type: Recycled Content Drives Innovation

Low-density polyethylene is anticipated to maintain a 41.5% share of the North America agricultural films market in 2024, benefiting from established supply chains and processing familiarity among film manufacturers and farming end-users. Recycled films emerge as the fastest-growing segment at 10.20% CAGR through 2030, driven by corporate sustainability mandates and regulatory pressures for circular economy adoption. Linear low-density polyethylene and high-density polyethylene serve specialized applications requiring enhanced puncture resistance and barrier properties, particularly in silage and fumigation applications. Ethylene vinyl acetate and ethylene butyl acrylate copolymers target premium greenhouse covering applications where light transmission and durability command higher pricing.

The compostable films segment, while representing a small current share, demonstrates significant growth potential as regulatory frameworks evolve and cost premiums narrow. BASF SE's ecovio mulch film technology showcases compostable alternatives that eliminate disposal concerns while maintaining agronomic performance. Novamont S.p.A.'s Mater-Bi bioplastic platform gains traction in organic farming applications, where soil compostability provides competitive advantages. The segment's evolution toward higher biobased content and improved mechanical properties addresses historical performance limitations that constrained adoption.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Silage Wrap Gains Momentum

Mulching applications command 44.0% of the North America agricultural films market size in 2024, reflecting the technology's proven effectiveness in specialty crop production and water conservation strategies. The segment benefits from established agronomic practices and demonstrated return on investment across diverse crop types and growing conditions. Greenhouse covering represents a high-value application requiring specialized properties, including light transmission optimization, condensation control, and extended durability under harsh environmental conditions. Fumigation applications serve niche markets with specific regulatory requirements and seasonal demand patterns.

Silage and bale wrap emerge as the fastest-growing application at 8.10% CAGR, driven by dairy industry consolidation and mechanization trends that favor large-scale operations. The application's technical requirements for anaerobic preservation and weather resistance create barriers to entry that support premium pricing. Advanced silage films incorporate multi-layer constructions that provide superior puncture resistance and UV protection essential for maintaining feed quality. The shift toward round bale silage systems, particularly in regions with unpredictable weather patterns, drives demand for specialized wrapping films that ensure consistent fermentation outcomes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Thickness: Demand Shifts Toward Thicker Films for Premium Tasks

Films up to 80 micron controlled 58.0% of the North America agricultural films market share in 2024, reflecting their widespread use in mulching, where material cost per acre dominates purchasing decisions. The 81–150 micron range serves intermediate needs such as greenhouse sidewalls and temporary crop covers that require moderate durability without premium prices. In contrast, films above 150 micron are on track for a 9.2% CAGR through 2030, making them the fastest-growing thickness group and lifting the overall North America agricultural films market size as growers shift toward longer-lasting solutions.

Technical demands are reshaping thickness selection. Greenhouse operators increasingly specify covers over 150 microns to withstand wind, hail, and ultraviolet exposure for several seasons while preserving high light transmission. Dairy producers favor a thicker silage wrap to resist punctures from coarse forage and to lock in the anaerobic conditions vital for fermentation. Multi-layer constructions, which increase total gauge while adding barrier and strength properties, are gaining traction wherever film failure would create costly crop or feed losses. As farms focus on total cost of ownership rather than lowest upfront price, the market continues its gradual move toward thicker, performance-driven films.

Geography Analysis

The United States commanded 67.0% of 2024 sales, anchored by the Central Valley, the Southeast vegetable belt, and the expanding greenhouse footprint in Texas. California’s plastic-reduction targets drive early trials of biodegradable mulch that could scale nationally once cost hurdles fall. Midwest growers adopt mulch film to conserve water as drought cycles intensify, while large dairy operations in the upper Midwest adopt silage wrap that preserves feed quality under variable weather.

Mexico posted a 7.50% CAGR outlook on the back of MXN 80 billion (USD 4.4 billion) in government farm-modernization funding that subsidizes greenhouse construction and drip irrigation. Greenhouse acreage exceeds a significant amount, turning the country into a high-value export supplier and a notable consumer of specialty covers. Sinaloa alone produced a significant amount of agri-food in 2023, illustrating the scale of plastic-film use in protected horticulture.

Canada’s controlled-environment sector concentrates in Ontario’s greenhouse belt, where operators overcome high energy and labor costs with automation investments that include advanced films. Federal quality regulations enforced by the Canadian Food Inspection Agency ensure consistent input standards that favor premium multilayer products. Growth remains steady despite labor shortages because automation offsets headcount and maintains yields year-round.

Competitive Landscape

The North America agricultural films market is moderately concentrated. Amcor plc, Dow Inc., BASF SE, Exxon Mobil Corporation, and RKW Group lead in volume or technology. Amcor's all-stock merger with Berry Global in April 2025 created a global packaging company with enhanced material science capabilities. The merger strengthens their agricultural film portfolio of mulch films, silage wraps, and greenhouse covers.[3]Amcor, "Amcor completes combination with Berry Global; Positioned to significantly enhance value for customers and shareholders," amcor.com Technology differentiation increasingly centers on sustainability credentials, smart film functionalities, and application-specific performance characteristics that command premium pricing in specialized segments.

Dow Inc. partnered with New Energy Blue LLC to secure bio-based ethylene, a move that insulates against fossil-feedstock volatility and supports brand decarbonization pledges. Innovation activity focuses on multilayer structures that blend recycled resin, compostable formulations that meet regional soil standards, and smart films with sensor integration. Smaller specialists such as Novamont S.p.A. and Ginegar Plastic Products Ltd. carve out niches in compostable mulch and greenhouse-specific covers, respectively, leveraging proprietary chemistries and field support services.

Market entry barriers include capital-intensive extrusion assets, customer qualification cycles, and regulatory certifications. Nonetheless, opportunities exist in recycling infrastructure build-outs because post-consumer agricultural film collection is underdeveloped. Partnerships between resin producers, waste haulers, and grower cooperatives are emerging to close the loop and capture resin value.

North America Agricultural Films Industry Leaders

-

Amcor plc

-

BASF SE

-

Dow Inc.

-

Exxon Mobil Corporation

-

RKW Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Amcor plc completed its all-stock acquisition of Berry Global, forming a global packaging company with advanced innovation and material science capabilities. The merger is anticipated to produce USD 650 million in benefits and elevate Amcor's earnings per share by 12% in fiscal 2026.

- November 2024: The University of Massachusetts Lowell received a USD 650,000 grant from the United States Department of Agriculture (USDA) to develop biodegradable plastics from food and agricultural waste. The project focuses on creating mulch films and plant containers, aiming to reduce dependency on petroleum-based agricultural inputs while promoting sustainable farming practices.

- January 2024: Revolution Sustainable Solutions, a U.S.-based company, expanded its film recycling operations through the acquisition of Canadian firm PolyAg Recycling.

North America Agricultural Films Market Report Scope

Agricultural films are specialized plastic film that acts as a protective shield to the cultivated crops, protecting tender roots from excess sunlight, retaining moisture, and shielding the plant from the attack of weeds and parasites. They are used in many innovative farming practices to increase crop output per hectare while enhancing crop quality. The North America agricultural films market is segmented by Type (Low-density Polyethylene, Linear Low-density Polyethylene, High-density Polyethylene, Ethyl Vinyl Acetate (EVA)/Ethylene Butyl Acrylate (EBA), Reclaims, and Other Films), Application (Greenhouse, Silage, and Mulch), and by Geography ( United States, Canada, Mexico, and Rest of North America). The report offers market size and forecast in terms of value (USD) for all the segments.

By Type

| Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) |

| High-Density Polyethylene (HDPE) |

| Ethylene Vinyl Acetate and Ethylene Butyl Acrylate |

| Recycled Films |

| Compostable Films |

By Application

| Mulching |

| Greenhouse Covering |

| Silage and Bale Wrap |

| Fumigation |

By Thickness

| Up to 80 Micron |

| 81 to 150 Micron |

| Above 150 Micron |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) | |

| High-Density Polyethylene (HDPE) | |

| Ethylene Vinyl Acetate and Ethylene Butyl Acrylate | |

| Recycled Films | |

| Compostable Films | |

| By Application | Mulching |

| Greenhouse Covering | |

| Silage and Bale Wrap | |

| Fumigation | |

| By Thickness | Up to 80 Micron |

| 81 to 150 Micron | |

| Above 150 Micron | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America agricultural films market?

The market is valued at USD 3.10 billion in 2025 and is forecast to reach USD 4.40 billion by 2030.

Which application segment is growing the fastest?

Silage and bale wrap is projected to grow at an 8.10% CAGR through 2030 on the back of dairy-sector consolidation.

How large is the United States share of regional sales?

The United States accounted for 67.0% of North America agricultural films market share in 2024.

Why are recycled-content films gaining traction?

Brand-owner net-zero pledges and state plastic-reduction rules support demand, even though recycled films command price premiums.