Market Size of North America Agricultural Chemical Packaging Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

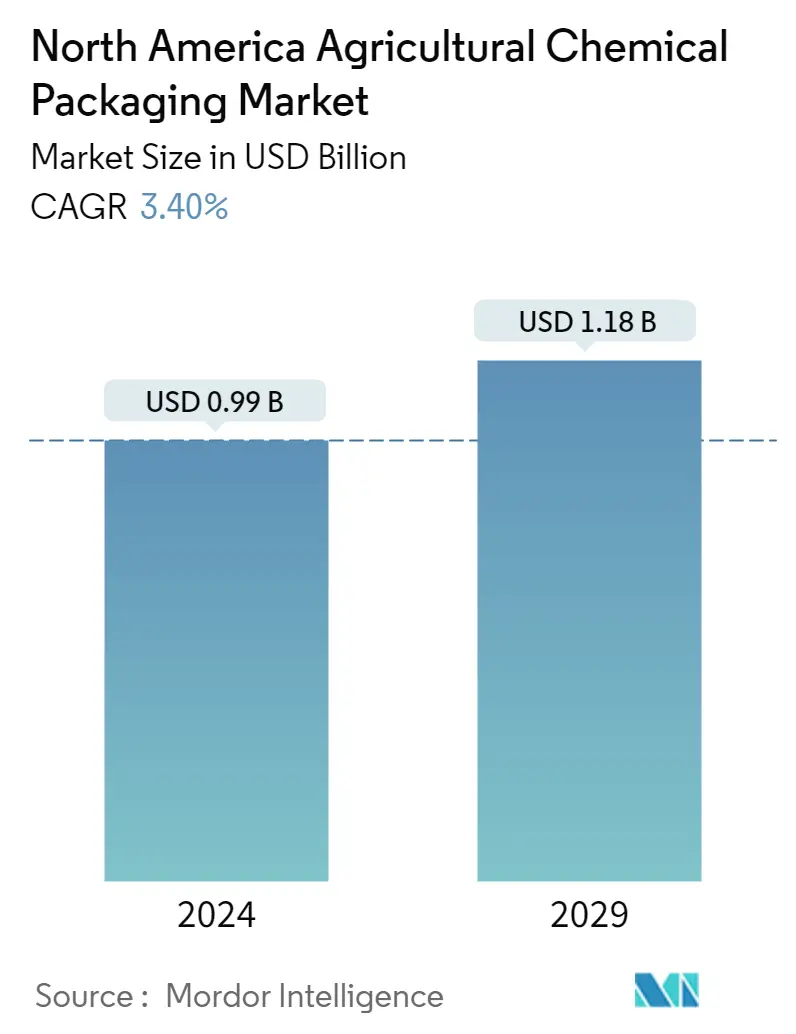

| Market Size (2024) | USD 0.99 Billion |

| Market Size (2029) | USD 1.18 Billion |

| CAGR (2024 - 2029) | 3.40 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Agricultural Chemical Packaging Market Analysis

The North America Agricultural Chemical Packaging Market size is estimated at USD 0.99 billion in 2024, and is expected to reach USD 1.18 billion by 2029, growing at a CAGR of 3.40% during the forecast period (2024-2029).

- Agrochemical packaging is one of the crucial parts of the agriculture industry as agrochemical products, such as fertilizers and pesticides, are toxic. They require advanced packaging solutions, helping reduce the risk of storing, handling, and transporting such chemical products. Packaging solutions used here are designed for better sealing.

- Among the materials, plastic is the most widely used packaging material for agrochemical products. The demand for bags, bottles, pouches, and containers is increasing, and vendors in the market are offering innovative and high-safety packaging solutions. For example, Scholle IPN offers a bag-in-a-box pouch packaging solution for packaging agricultural chemical products in the market.

- With the advancements in biodegradable packaging solutions fueling the demand for such packaging solutions, various vendors in the market are focusing on adopting such solutions as part of their offering, focusing on recycled resins. For example, in January 2021, Mauser Packaging Solutions introduced the KORTRAX Barrier Tight-Head container for transporting hazardous solvent-based products that are traditionally difficult to contain. KORTRAX containers are 100% recyclable post-use and are available in 20-liter, 5-gallon, and 10-liter sizes.

- According to Federal laws and regulations, there are many regulations with which a product's label or markings must comply before being sold in the United States. Labeling requirements related to legal metrology must abide by The Fair Packaging and Labeling Act (FPLA) and Uniform Packaging and Labeling Regulation (UPLR). In addition, all products imported into the US must conform to Title 19, United States Code, Chapter 4, Section 1304 and 19 CFR 134, Country of Origin Marking regulations.

- The packaging regulations limit vendor profits and divide them into smaller packages as weight and quantity regulations are to be followed. Packaging solution providers also invest in compliance consultants and even outsource these compliance handling processes to entities that take care of these processes, thus impacting their profits in the market.

- The COVID-19 outbreak has affected international trade and global supply chains of essential and non-essential goods and services. With the spread of COVID-19 across the world, businesses have suffered significantly. The market was initially impacted due to the pandemic. Many countries in the region postponed the ban on single-use plastic. The pandemic led to the increase in the usage of plastic packaging for chemicals due to significant growth in e-commerce.

North America Agricultural Chemical Packaging Industry Segmentation

The study on the North American agricultural chemical packaging market tracks the vendors' revenue based on the market demand for the end-packaging-based products across key segments, as captured in the segmentation. The key product types considered for the study include bags & pouches, IBCs, cans & containers, and other product types. The breakdown based on material type is provided for plastic, paper & paperboard, metal, and other materials.

| By Product Type | |

| Bags and Pouches | |

| Containers and Cans | |

| Intermediate Bulk Containers (IBCs) | |

| Other Product Types |

| By Material Type | |

| Plastic | |

| Paper and Paperboard | |

| Metal | |

| Other Materials |

| By Application Type | |

| Fertilizers | |

| Pesticides | |

| Herbicides | |

| Other Application Types |

North America Agricultural Chemical Packaging Market Size Summary

The North American agricultural chemical packaging market is a vital segment of the agriculture industry, focusing on the safe storage, handling, and transportation of toxic agrochemical products like fertilizers and pesticides. The market is characterized by the use of advanced packaging solutions, primarily plastic, which offers better sealing and safety features. Innovations such as bag-in-a-box pouch packaging and biodegradable solutions are gaining traction, driven by the demand for sustainable and high-safety packaging options. Regulatory compliance is a significant aspect of the market, with strict labeling and packaging regulations impacting vendor operations and profitability. The COVID-19 pandemic initially disrupted the market, but the rise in e-commerce led to increased plastic packaging usage, highlighting the ongoing demand for effective packaging solutions.

The market is mature, with steady demand for agrochemicals like fertilizers and pesticides, particularly nitrogen fertilizers, which dominate the market due to their extensive use in crops like maize and wheat. North America, especially the United States, plays a crucial role in the global fertilizer sector, with significant production and transportation infrastructure supporting the demand for packaging solutions. The region's plastic resin production further supports the packaging industry, with materials like polyethylene being preferred for their moisture barrier properties. The market is fragmented, with intense competition among regional and global players, and recent strategic moves, such as acquisitions and collaborations, aim to enhance market presence and address environmental concerns related to plastic waste.

North America Agricultural Chemical Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of Substitute Products

-

-

1.3 Industry Value Chain Analysis

-

1.4 Impact of COVID-19 on the Agricultural Chemical Packaging Market

-

1.5 Industry Regulations and Standards

-

1.6 Qualitative Coverage on the Beakdown of B2B and Direct Channel-based Sales

-

-

2. MARKET SEGMENTATION

-

2.1 By Product Type

-

2.1.1 Bags and Pouches

-

2.1.2 Containers and Cans

-

2.1.3 Intermediate Bulk Containers (IBCs)

-

2.1.4 Other Product Types

-

-

2.2 By Material Type

-

2.2.1 Plastic

-

2.2.2 Paper and Paperboard

-

2.2.3 Metal

-

2.2.4 Other Materials

-

-

2.3 By Application Type

-

2.3.1 Fertilizers

-

2.3.2 Pesticides

-

2.3.3 Herbicides

-

2.3.4 Other Application Types

-

-

North America Agricultural Chemical Packaging Market Size FAQs

How big is the North America Agricultural Chemical Packaging Market?

The North America Agricultural Chemical Packaging Market size is expected to reach USD 1.02 billion in 2025 and grow at a CAGR of 3.40% to reach USD 1.21 billion by 2030.

What is the current North America Agricultural Chemical Packaging Market size?

In 2025, the North America Agricultural Chemical Packaging Market size is expected to reach USD 1.02 billion.