Market Size of North America ADAS Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | 16.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North American ADAS Market Analysis

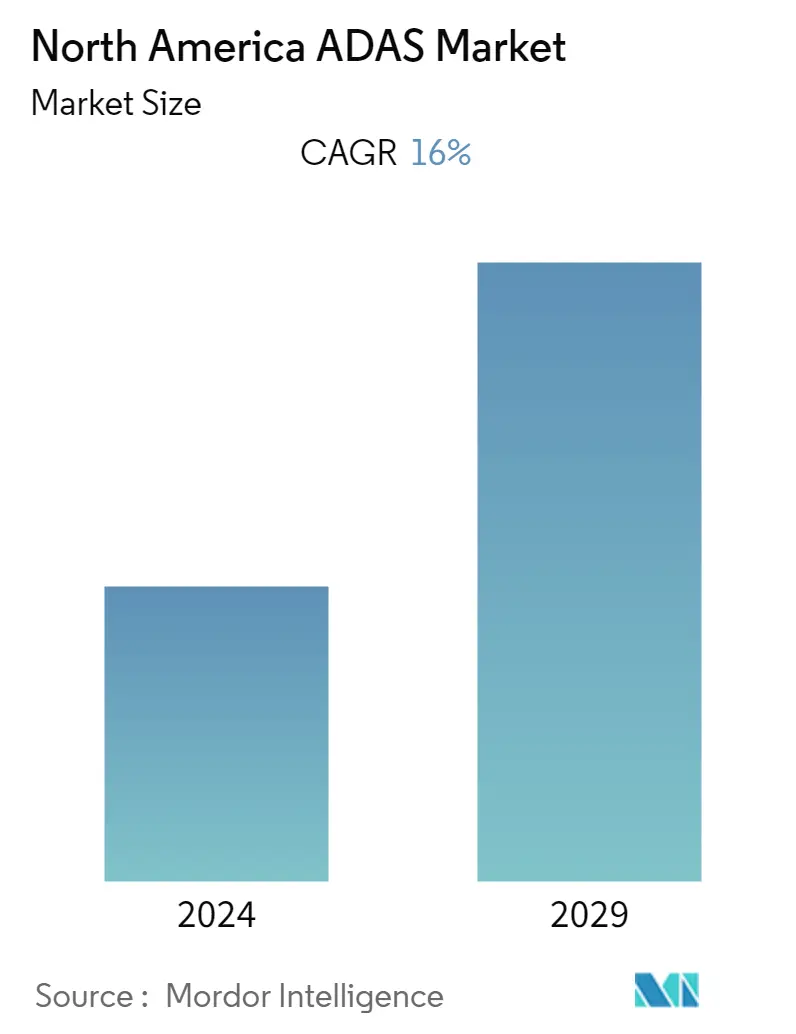

Currently, the North American ADAS Market is valued at USD 9.22 billion and is expected to reach USD 22.92 billion and grow at a CAGR of 16.54 % in the next five years.

Since automotive manufacturers have resumed operations due to steadily rising automobile sales in countries with a limited number of COVID-19 cases, the market is likely to recover during the forecast market. Furthermore, the manufacturers are implementing contingency plans to mitigate future business uncertainties to retain continuity with clients in the critical sectors of the automobile industry.

Over the long term, increasing investments in R&D by major industry players, entry of many new startups and technology companies in the ADAS industry, and a rise in sales of electric and autonomous vehicles as well as the advent of robo taxis and autonomous commercial vehicles are creating demand in the automotive and transportation industry with a surge in sales of cars installed with ADAS systems.

Key players in the market are expanding their R&D efforts, engaging in mergers and acquisitions, and developing new technologies' production capacity to cater to the increased demand for ADAS systems. For instance,

- January, 2022: Aptiv Plc signed a definitive agreement to acquire Wind River from TPG Capital for USD 4.3 billion in cash. Wind River is a global leader in developing and delivering software for the intelligent edge, catering to aerospace and defense, telecommunications, manufacturing, and automotive industries.

Thus, the development of new ADAS technologies, rising sales of electric and autonomous vehicles, entry of many new startups and technology companies, and various activities undertaken by the incumbent players for their business expansion are expected to drive the North American ADAS market during the forecast period. (2022-2027).

North American ADAS Industry Segmentation

Advanced Driving Assistance Systems (ADAS) is a group of driving technologies consisting of hardware and software specifically developed to assist drivers in daily vehicle driving tasks like parking and reversing the vehicle. The hardware-based ADAS technologies comprised sensors, microchips, and cameras, while the software-based ADAS technologies consisted of software required to control these components. ADAS are also classified into Active and Passive systems.

The North American ADAS Market is Segmented by Type, Vehicle Type, and Country. By Type, the market is segmented into Adaptive Cruise Control Systems, Adaptive Front-lighting, Night Vision Systems, Blind Spot Detection, Autonomous Emergency Braking Systems, Lane Keeping Assist, Driver Drowsiness Alerts, Lane Departure Warnings, and Other Types. Technology segments the market into Radar, Li-Dar, and Camera. The market is segmented by Vehicle Type: Passenger Cars and Commercial Vehicles. By Country, the market is segmented into United States, Canada, and Mexico. The report offers the market size in value (USD billion), volume (In units), and forecasts for all above segments.

| By Type | |

| Adaptive Cruise Control System | |

| Adaptive Front-lighting | |

| Night Vision System | |

| Blind Spot Detection | |

| Autonomous Emergency Braking System | |

| Lane Keeping Assist | |

| Driver Drowsiness Alert | |

| Lane Departure Warning | |

| Other Types |

| By Technology Type | |

| Radar | |

| Li-Dar | |

| Camera |

| By Vehicle Type | |

| Passenger Cars | |

| Commercial Vehicles |

| By Country | |

| United States | |

| Canada | |

| Mexico |

North America ADAS Market Size Summary

The North American Advanced Driver Assistance Systems (ADAS) market is poised for significant growth, driven by a resurgence in automotive manufacturing and increased vehicle sales following the easing of COVID-19 restrictions. The market is experiencing a surge in demand due to heightened investments in research and development by key industry players, the entry of new startups, and the growing sales of electric and autonomous vehicles. These factors are further bolstered by the introduction of robo-taxis and autonomous commercial vehicles, which are contributing to the rising adoption of ADAS technologies. Major players in the market are expanding their research and development efforts, engaging in strategic mergers and acquisitions, and enhancing their production capacities to meet the growing demand for ADAS systems. The market is characterized by a diverse landscape of global and local players, all vying to strengthen their market positions through innovative collaborations and technological advancements.

The United States is expected to lead the North American ADAS market, supported by a robust automotive components industry, high awareness of vehicle safety features, and substantial investments in automotive software and electronics. The market is further propelled by the increasing sales of electric vehicles, which are often equipped with advanced ADAS technologies. Canada is also anticipated to be a significant market, driven by a strong preference for vehicle safety and connectivity features. The LiDAR segment is projected to dominate the market due to its widespread application in various ADAS systems. The market's expansion is supported by initiatives such as the NHTSA's Automated Vehicle Transparency and Engagement for Safe Testing Initiative, which aims to highlight the benefits of ADAS-equipped vehicles. As companies continue to launch new vehicles featuring advanced ADAS technologies, the North American market is expected to experience healthy growth over the forecast period.

North America ADAS Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.2 Market Restraints

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size in USD Billion)

-

2.1 By Type

-

2.1.1 Adaptive Cruise Control System

-

2.1.2 Adaptive Front-lighting

-

2.1.3 Night Vision System

-

2.1.4 Blind Spot Detection

-

2.1.5 Autonomous Emergency Braking System

-

2.1.6 Lane Keeping Assist

-

2.1.7 Driver Drowsiness Alert

-

2.1.8 Lane Departure Warning

-

2.1.9 Other Types

-

-

2.2 By Technology Type

-

2.2.1 Radar

-

2.2.2 Li-Dar

-

2.2.3 Camera

-

-

2.3 By Vehicle Type

-

2.3.1 Passenger Cars

-

2.3.2 Commercial Vehicles

-

-

2.4 By Country

-

2.4.1 United States

-

2.4.2 Canada

-

2.4.3 Mexico

-

-

North America ADAS Market Size FAQs

What is the current North America ADAS Market size?

The North America ADAS Market is projected to register a CAGR of 16% during the forecast period (2024-2029)

Who are the key players in North America ADAS Market?

Continental AG, Aptiv Plc, Visteon Corp., MobilEye and Bosch Mobility Solutions are the major companies operating in the North America ADAS Market.