Market Size of Non-woven Packaging Industry

| Study Period | 2019 - 2029 |

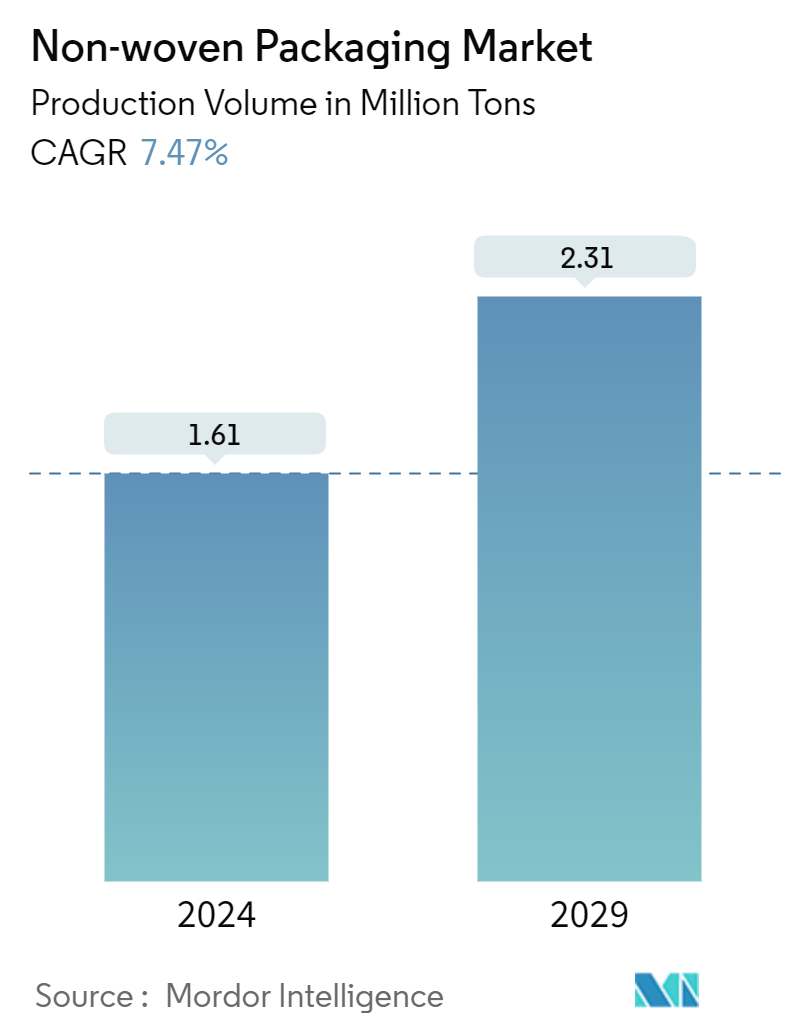

| Market Volume (2024) | 1.61 Million tons |

| Market Volume (2029) | 2.31 Million tons |

| CAGR (2024 - 2029) | 7.47 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Non-woven Packaging Market Analysis

The Non-woven Packaging Market size in terms of production volume is expected to grow from 1.61 Million tons in 2024 to 2.31 Million tons by 2029, at a CAGR of 7.47% during the forecast period (2024-2029).

Innovation and improvements in the non-woven fabric manufacturing processes have also contributed to market growth. Innovations in materials and production techniques have led to the development of non-woven fabrics with enhanced properties such as strength, flexibility, and barrier capabilities, creating opportunities for the products to substitute existing packaging products. The advancements mentioned have expanded the application scope of non-woven fabric packaging across various industries, further driving market growth.

The textile industry has become increasingly globalized, spreading production and consumption across various regions. As a result, countries with competitive advantages in textile production, such as low labor costs or access to raw materials, have been able to ramp up their yarn production for export purposes. This has led to a surge in the volume of textile yarn traded internationally.

Non-woven materials offer lightweight, durable, and cost-effective solutions for packaging in various industries such as agriculture, construction, and retail. The versatility of non-woven fabrics makes them suitable for different types of sacks and bags, driving their adoption in packaging applications.

Environmental awareness, such as eco-friendly fashion has evolved worldwide. Non-woven bags, created from sustainable resources, are at the forefront of this trend, providing a chic and responsible substitute to conventional plastic bags.

The geopolitical situation often influences global energy markets, impacting the prices of crude oil and natural gas. Since these commodities are key feedstocks for petrochemical-based raw materials used in non-woven fabric production, such as polypropylene and polyester, fluctuations in energy prices can directly affect the cost of raw materials. Sharp increases in energy prices can drive up production costs for non-woven fabric manufacturers, leading to higher prices for non-woven packaging materials.

Non-woven Packaging Industry Segmentation

Non-woven refers to a fabric-like material comprising staple fibers that have been mechanically, chemically, thermally, or solvent-bonded together. The study captures the demand for non-woven materials based on the various market dynamics, technology trends, and demand-supply conditions worldwide. The study covers the non-woven packaging market tracked in terms of volume in million tonnes. This report analyzes the factors that impact geopolitical developments in the market, which were studied based on the prevalent base scenarios, key themes, and end-use application-related demand cycles. The estimates exclude the weight of the content that is or is to be packed inside the non-woven packaging solutions.

The scope is limited to non-woven material in packaging. Non-woven shopping bags are not considered part of the scope. The global non-woven packaging market is segmented by technology (dry-laid, spun-laid, and other technologies), end-use packaging applications (food packaging, industrial, medical, and other end-uses), and geography. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The non-woven packaging market is segmented by technology (dry-laid, spun-laid, other technologies), by end-user packaging applications (food packaging, industrial, medical, other end user packaging applications), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report offers market forecasts and size in volume (tonnes) for all the above segments.

| By Technology | |

| Dry-Laid | |

| Spun-Laid | |

| Other Technologies |

| By End-user Packaging Applications | |

| Food Packaging | |

| Industrial | |

| Medical | |

| Other End User Packaging Applications |

| By Geography | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Non-woven Packaging Market Size Summary

The non-woven packaging market is poised for significant growth, driven by innovations in fabric manufacturing processes that enhance the properties of non-woven materials, such as strength and flexibility. These advancements have expanded the application scope of non-woven fabrics across various industries, including agriculture, construction, and retail, where they offer lightweight, durable, and cost-effective packaging solutions. The increasing global demand for sustainable and eco-friendly packaging alternatives has further propelled the adoption of non-woven materials, particularly in regions like China and India, where there is a strong focus on reducing plastic waste and promoting reusable packaging options. The market's growth is also influenced by geopolitical factors affecting energy prices, which can impact the cost of raw materials used in non-woven fabric production.

The non-woven packaging market is characterized by a fragmented landscape with both global players and small to medium-sized enterprises actively participating. Major companies such as Novipax Buyer, LLC, EAM Corporation, Glatfelter Corporation, Felix Non-wovens, and Dupont de Nemours, Inc. are employing strategies like mergers and acquisitions to enhance their product offerings and secure a competitive edge. Recent developments, such as the merger between Berry Global Group, Inc. and Glatfelter Corporation, highlight the industry's trend towards consolidation to strengthen market positions. Additionally, the market is witnessing increased collaboration and innovation, particularly in the food packaging sector, where non-woven materials are being integrated with natural fibers to create sustainable and efficient packaging solutions.

Non-woven Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness – Porter’s Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products and Services

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Technology

-

2.1.1 Dry-Laid

-

2.1.2 Spun-Laid

-

2.1.3 Other Technologies

-

-

2.2 By End-user Packaging Applications

-

2.2.1 Food Packaging

-

2.2.2 Industrial

-

2.2.3 Medical

-

2.2.4 Other End User Packaging Applications

-

-

2.3 By Geography

-

2.3.1 North America

-

2.3.2 Europe

-

2.3.3 Asia

-

2.3.4 Australia and New Zealand

-

2.3.5 Latin America

-

2.3.6 Middle East and Africa

-

-

Non-woven Packaging Market Size FAQs

How big is the Non-woven Packaging Market?

The Non-woven Packaging Market size is expected to reach 1.61 million tons in 2024 and grow at a CAGR of 7.47% to reach 2.31 million tons by 2029.

What is the current Non-woven Packaging Market size?

In 2024, the Non-woven Packaging Market size is expected to reach 1.61 million tons.