Non-Alcoholic Fatty Liver Disease (NAFLD) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 17.56 Billion |

| Market Size (2030) | USD 36.94 Billion |

| Growth Rate (2025 - 2030) | 16.04% CAGR |

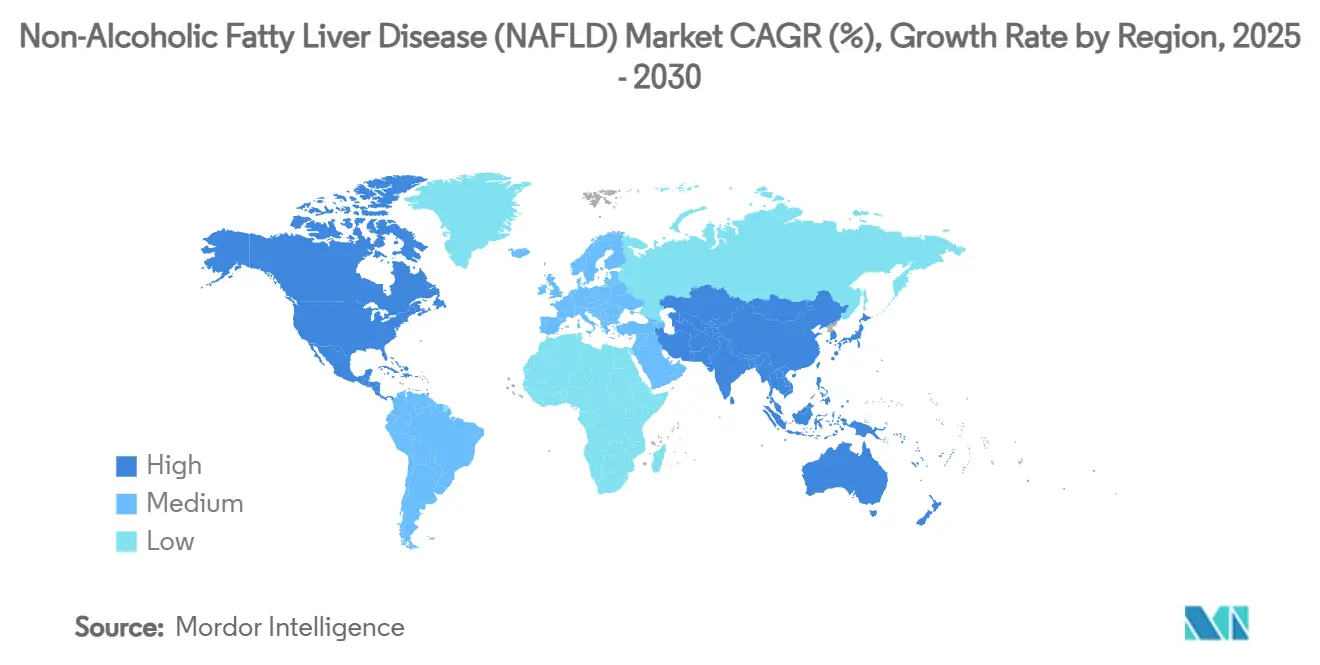

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

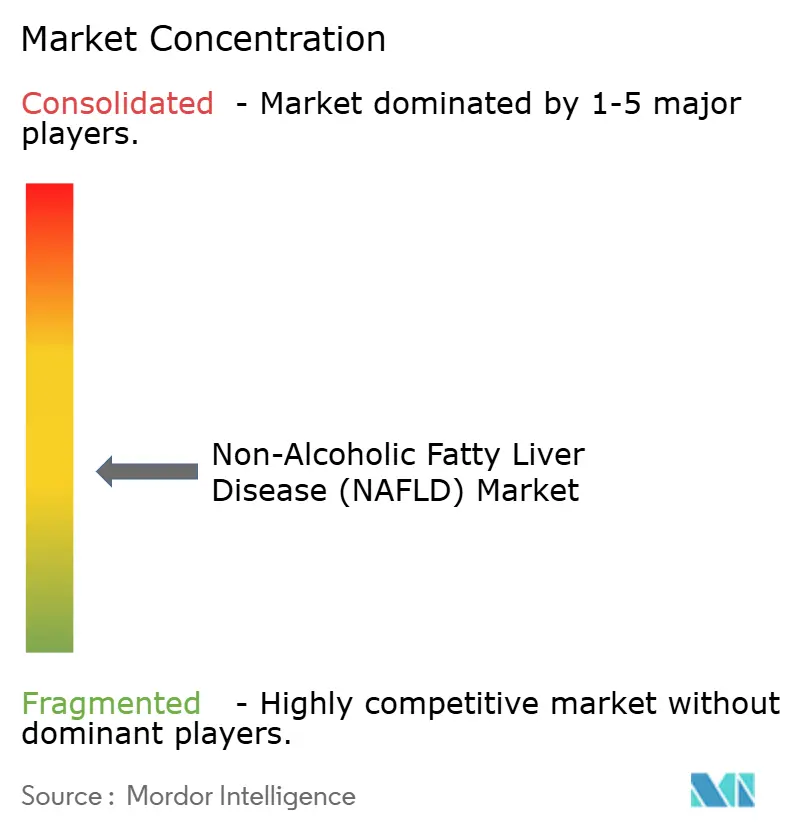

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Non-Alcoholic Fatty Liver Disease (NAFLD) Market Analysis by Mordor Intelligence

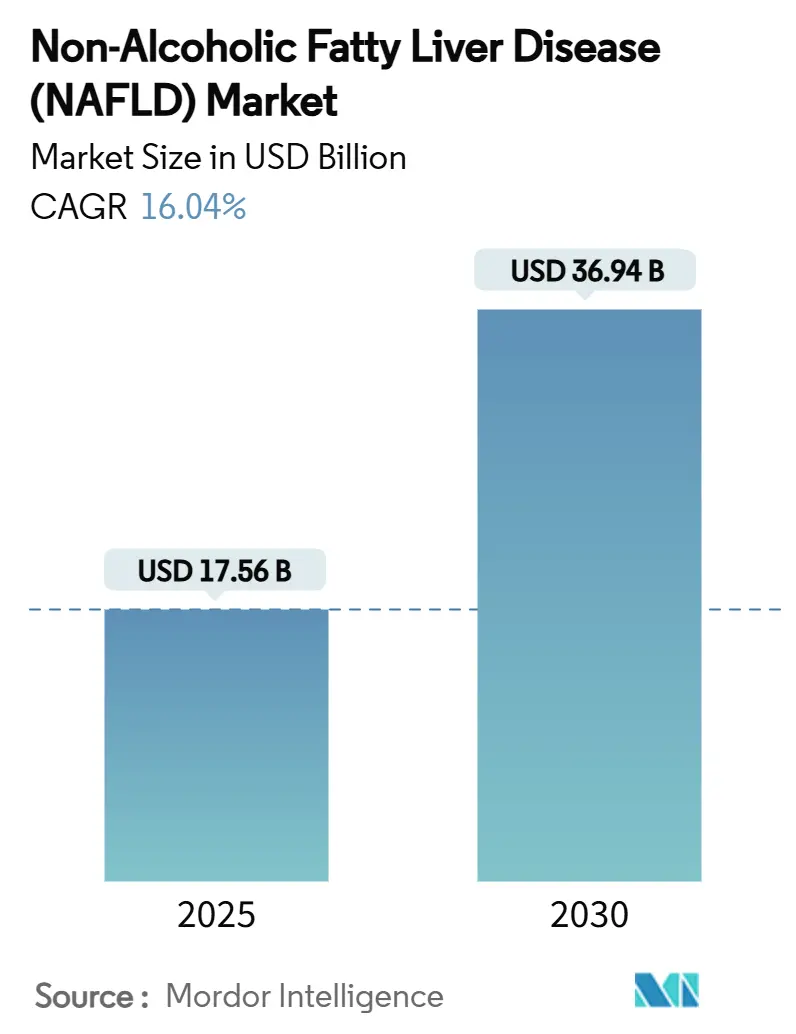

The non-alcoholic fatty liver disease market is valued at USD 17.56 billion in 2025 and is forecast to reach USD 36.94 billion by 2030, translating into a 16.04% CAGR that underscores the field’s rapid transformation from an underserved specialty to a high-priority therapeutic arena. Growth is propelled by the first-in-class approval of Rezdiffra (resmetirom) [1]Food and Drug Administration, “FDA approves Rezdiffra,” fda.gov , rising obesity and type 2 diabetes rates, AI-enabled diagnostic advances, and accelerated regulatory pathways that have reframed NAFLD as a treatable metabolic disorder rather than a diagnosis of exclusion. Investment momentum is evident in multi-billion-dollar acquisitions by large pharmaceutical companies, reflecting confidence that metabolic liver disease will deliver durable revenue streams as prevalence rises. Expanding screening programs, favorable reimbursement for non-invasive tests, and greater public awareness are broadening the diagnosed patient pool, while breakthrough drugs targeting fibrosis pathways signal the start of a robust product cycle. Collectively, these forces position the non-alcoholic fatty liver disease market for sustained double-digit growth across all major regions.

Key Report Takeaways

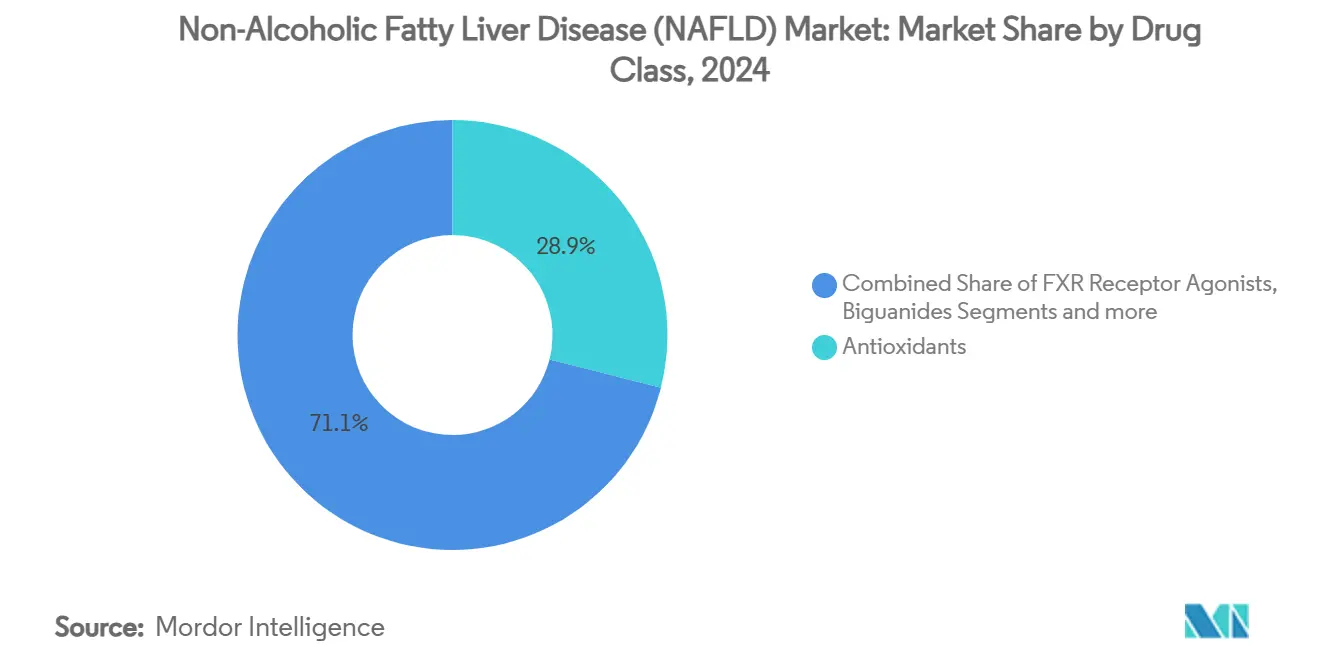

- By drug class, antioxidants held 28.94% of the non-alcoholic fatty liver disease market share in 2024, while FXR agonists are projected to expand at a 17.01% CAGR through 2030.

- By distribution channel, hospital pharmacies led with 47.88% revenue share in 2024; online pharmacies record the fastest growth at 16.98% CAGR to 2030.

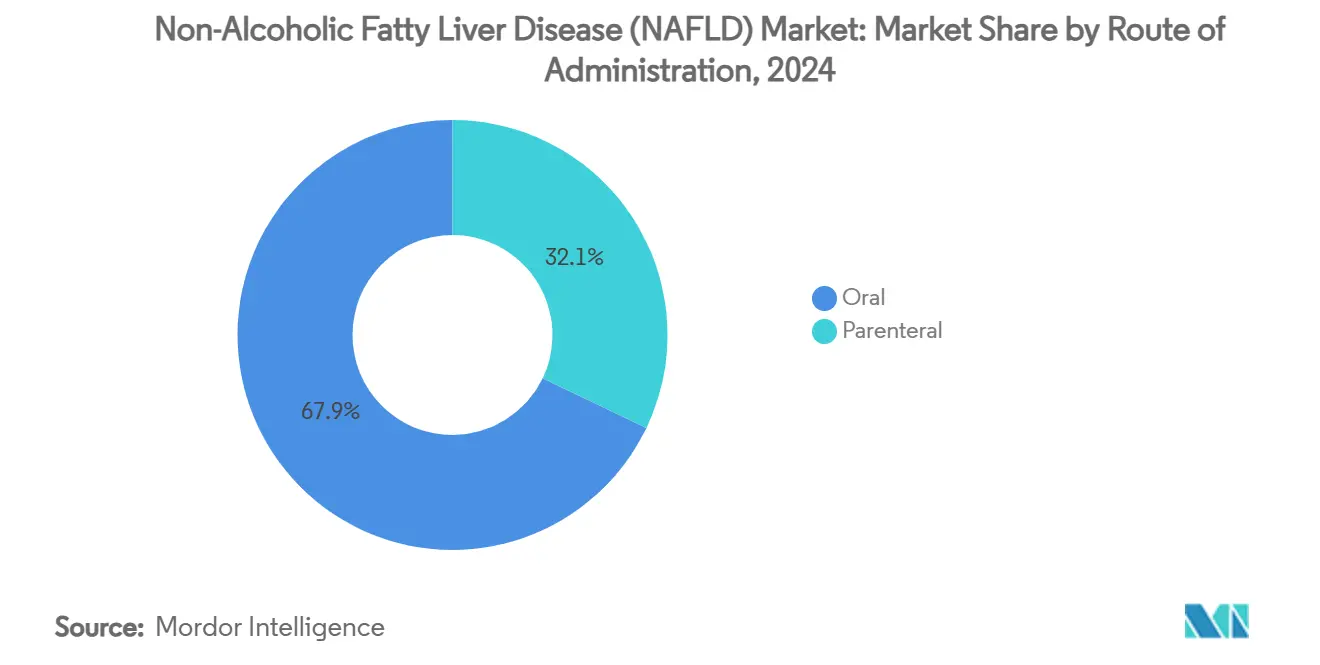

- By route of administration, oral formulations accounted for 67.89% share of the non-alcoholic fatty liver disease market size in 2024, whereas parenteral products advance at a 16.86% CAGR.

- By age group, adults captured 65.34% share of the non-alcoholic fatty liver disease market size in 2024; the geriatric segment exhibits the highest CAGR at 18.81% through 2030.

- By geography, North America dominated with 39.99% revenue share in 2024, while Asia-Pacific is forecast to grow at 17.22% CAGR to 2030.

Global Non-Alcoholic Fatty Liver Disease (NAFLD) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global NAFLD Patient Pool | +4.2% | Global, with highest concentration in North America and Asia-Pacific | Long term (≥ 4 years) |

| Escalating Prevalence of Obesity & Type-2 Diabetes | +3.8% | Global, particularly pronounced in developed markets | Medium term (2-4 years) |

| Expanding Public-Sector Screening & Awareness Programs | +2.1% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| AI-Enabled Non-Invasive Diagnostics Gaining Traction | +2.9% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Accelerated R&D In Multi-Target Combination Therapies | +2.4% | Global, concentrated in major pharmaceutical hubs | Long term (≥ 4 years) |

| Reimbursement Expansion for Metabolic/Bariatric Surgery | +1.0% | Primarily North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global NAFLD Patient Pool

Metabolic dysfunction-associated steatotic liver disease (MASLD) prevalence is projected to rise from 33% in 2020 to 41% by 2050, while U.S. MASH cases needing pharmacologic intervention may double to 12 million, dramatically enlarging the addressable base [2]Fatty Liver Alliance, “Global MASLD Projections,” fattyliveralliance.org . Eighty-three percent of patients meeting MASLD criteria remain undiagnosed, indicating substantial headroom for growth. High-frequency genetic variants in several Asia-Pacific populations elevate regional susceptibility, reinforcing the long-term opportunity outside Western markets [3]Lung-Yi Mak, "Liver diseases and hepatocellular carcinoma in the Asia-Pacific region: burden, trends, challenges and future directions," Nature Reviews Gastroenterology & Hepatology, nature.com. The emergence of pediatric NAFLD lengthens lifetime therapy horizons, and the recent terminology shift from NAFLD to MASLD reduces stigma and helps clinicians identify cases earlier.

Escalating Prevalence of Obesity & Type-2 Diabetes

Type 2 diabetes confers a 65% likelihood of MASLD, far above the 25-30% seen in the general population, thereby accelerating progression to advanced fibrosis. Medicare’s 2026 decision to reimburse anti-obesity medicines removes a key cost barrier for an aging cohort at heightened metabolic risk. GLP-1 receptor agonists such as semaglutide demonstrated 62.9% MASH resolution in Phase 3, highlighting the dual benefit of simultaneous weight and liver fat reduction. Expanded bariatric surgery coverage by major insurers positions surgical options as adjuncts where pharmacology falls short, while the multifaceted nature of metabolic syndrome is spurring combination-therapy pipelines across leading sponsors.

Expanding Public-Sector Screening & Awareness Programs

Cost-effectiveness studies show that FIB-4-based two-step algorithms deliver acceptable incremental cost per quality-adjusted life-year in 40-49-year-olds, encouraging payer adoption. The American Heart Association’s 2025 cardio-liver-metabolic guidelines formalize MASLD screening for cardiovascular patients, institutionalizing detection in high-risk groups. Major payers including Aetna now reimburse non-invasive fibrosis tests, easing entry for early-stage patients. Veterans Affairs studies confirm that multicomponent care pathways can be scaled across primary care networks, and advocacy by the Global Liver Institute propels supportive legislative efforts.

AI-Enabled Non-Invasive Diagnostics Gaining Traction

Machine-learning algorithms using electronic health record data achieve 96% sensitivity and 92.5% specificity in detecting fatty liver disease, reducing reliance on biopsies. AI-assisted digital pathology standardizes NASH scoring and cuts inter-observer variability in trials, speeding regulatory review. Portable ultrasound systems like Velacur deliver an area-under-curve of 0.846 for moderate steatosis, expanding rural screening capacity. Combining machine learning with transient elastography yields predictive tools that achieve 0.80 AUC for MAFLD risk stratification in primary care settings. Integration with telemedicine platforms positions non-invasive tests as the backbone of population-scale NAFLD management programs, improving access and lowering systemic costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence Of Widely Approved Disease-Modifying Drugs | -2.8% | Global, with varying regulatory timelines | Medium term (2-4 years) |

| Lengthy, High-Risk Late-Stage Clinical Trials | -1.9% | Global, concentrated in major pharmaceutical markets | Long term (≥ 4 years) |

| Regulatory Uncertainty Over Histologic Surrogate Endpoints | -1.2% | Primarily US and EU regulatory jurisdictions | Short term (≤ 2 years) |

| Low Physician Confidence in Emerging Metabolic Biomarkers | -0.8% | Global, with regional variations in adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Absence of Widely Approved Disease-Modifying Drugs

Rezdiffra is presently the only FDA-approved therapy for non-cirrhotic NASH, obliging prescribers to depend mainly on lifestyle modification for early-stage disease. Its accelerated approval status requires confirmatory outcomes studies, creating a risk of label withdrawal if long-term benefits are not demonstrated. Patients with steatosis but no fibrosis remain without approved pharmacologic options, keeping a large share of the potential market untapped. Clinical failures, such as previous setbacks with obeticholic acid, highlight the steep attrition facing late-stage candidates and may deter new entrants. Lifestyle-only management paradigms will continue to restrain market size until multiple drug classes obtain global regulatory clearance.

Lengthy, High-Risk Late-Stage Clinical Trials

Disease progression in NAFLD is slow, forcing Phase 3 designs of 54 months or longer to prove clinical benefit, as seen in the MAESTRO-NASH program. High placebo response linked to lifestyle changes complicates statistical power, requiring large samples and inflating cost. Recruitment is hampered by asymptomatic presentation and biopsy requirements, extending timelines and raising patient-burden concerns. Regulators remain cautious about surrogate histology endpoints, pushing companies to pursue clinical outcomes such as transplant-free survival that may take a decade to accrue. The protracted and expensive path to approval limits the field to sponsors with deep capital reserves.

Segment Analysis

By Drug Class: FXR Agonists Challenge Antioxidant Dominance

Antioxidants held 28.94% of the non-alcoholic fatty liver disease market share in 2024 owing to long-established safety and generic availability, yet their moderate efficacy caps upside in an era of targeted innovation. FXR agonists are forecast to post a 17.01% CAGR through 2030 as resmetirom’s success validates nuclear-receptor modulation as a disease-modifying strategy that tackles lipid handling and fibrosis pathways. Growing cardiovascular risk awareness supports lipid-lowering agents, including oral PCSK9 inhibitors that combine LDL reduction with potential hepatic benefit, while thiazolidinediones face headwinds from safety perceptions. The pivot from diabetes-centric repurposing toward liver-specific mechanisms reflects a maturing therapeutic paradigm that is likely to diversify further into FGF-21 analogs, CCR2/5 inhibitors, and anti-fibrotic small molecules.

The next wave of R&D emphasizes combination regimens that exploit complementary pathways, aiming to improve histologic endpoints beyond single-agent ceilings. Partnering deals that bundle FXR agonists with GLP-1s or anti-fibrotics illustrate the shift toward cocktail approaches to reach broad histological and metabolic targets. As these agents advance, antioxidants may settle into supportive roles or over-the-counter adjuncts, while specialty drugs capture premium pricing in fibrosis-stage patients. Leading players are therefore augmenting pipelines with multi-mechanism portfolios to hedge against single-asset risk and to align with future combination-therapy standards.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies commanded 47.88% of 2024 sales, reflecting the specialist-driven initiation of advanced therapies that require lab monitoring and prior authorization support. However, online outlets are expanding at 16.98% CAGR as telemedicine normalizes chronic-disease follow-up and as specialty drugs move into long-term maintenance phases that suit home delivery models. Integrated health systems are scaling specialty-pharmacy hubs able to manage reimbursement hurdles for high-cost agents like resmetirom, maintaining hospital channels’ dominance for complex cases.

Retail chains remain relevant for comorbidity prescriptions and may partner with digital platforms to extend reach, but their share growth is expected to trail online competitors. Regulatory scrutiny of mail-order drug safety is prompting investments in track-and-trace technology, while patient-support apps enhance adherence for lifelong therapies. Overall, distribution is converging on hybrid service models that blend clinician oversight with e-commerce convenience, reinforcing the importance of omnichannel capability for manufacturers looking to maximize uptake across patient segments.

By Route of Administration: Parenteral Innovation Challenges Oral Dominance

Oral therapies controlled 67.89% of 2024 revenue given patient preference, lower manufacturing complexity, and the historical focus on small molecules. The non-alcoholic fatty liver disease market size for parenteral products is projected to expand at 16.86% CAGR through 2030, underpinned by GLP-1 injectables and emerging RNA-based approaches that demand systemic delivery. Injectable semaglutide’s 62.9% histology-resolved MASH rate exemplifies how parenteral pharmacology can deliver superior efficacy, particularly in high-BMI cohorts.

Pipeline innovation includes long-acting subcutaneous depots, hepatic-targeted nanoparticles, and implantable pumps designed to cut dosing frequency and raise compliance. These formats could erode oral dominance in advanced disease stages where higher potency or localized action is required. Nevertheless, oral convenience and payers’ preference for lower-cost formulations will preserve a substantial share for pills in early and maintenance settings. Companies able to provide phased oral-to-injectable treatment ladders may secure competitive advantage across disease progression.

By Age Group: Geriatric Surge Outpaces Adult Dominance

Adults accounted for 65.34% revenue in 2024 as mid-life metabolic syndrome converged with lifestyle risks to drive peak incidence. The geriatric segment is expected to grow at 18.81% CAGR as global aging amplifies fibrosis progression and comorbidity complexity. Polypharmacy and reduced hepatic clearance in older patients necessitate careful dosing, spurring demand for agents with favorable safety and interaction profiles. Sponsors are responding by designing age-stratified trials and by exploring lower-dose or extended-release formulations that suit geriatric physiology.

Conversely, increasing pediatric obesity is seeding a future adult pipeline of chronically treated patients, though strict safety thresholds and formulation needs temper near-term commercial impact. Regulators encourage pediatric investigation plans, hinting that child-specific indications may emerge once adult safety is established. Over the next decade, age-tailored regimens are likely to diversify, with clinical practice guidelines differentiating between metabolic drivers in younger adults and fibrosis mitigation in the elderly.

Geography Analysis

North America held 39.99% of 2024 revenue, leveraging early FDA approvals, comprehensive reimbursement, and dense networks of hepatology centers that accelerate product uptake. Medicare’s forthcoming coverage of anti-obesity drugs expands eligibility among seniors, and major insurers now fund non-invasive fibrosis tests, enabling earlier entry into the treatment funnel. Strong academic–industry collaboration and ample venture funding sustain a rich trial pipeline, cementing the region’s leadership in first-to-launch opportunities.

Asia-Pacific is forecast to grow at 17.22% CAGR, powered by higher genetic susceptibility, rapid urbanization, and rising metabolic syndrome prevalence. Regional clinical-trial participation already comprises roughly one-third of industry-sponsored NAFLD studies, accelerating access to investigational agents. National screening programs in South Korea and China are increasing diagnosis rates, while Japan’s super-aging demographics boost geriatric demand. Government investments in healthcare infrastructure and domestic biotech capabilities underpin sustained expansion.

Europe maintains a steady trajectory, aided by EMA regulatory harmonization and strong social-insurance funding that reduces out-of-pocket burden. Anticipated EMA clearance of resmetirom in late 2025 sets the stage for broad EU launches starting with Germany. Preventive-care emphasis and unified clinical guidelines foster early intervention, while academic medical centers contribute high-quality trial data. Meanwhile, Middle East and Africa and parts of Latin America represent nascent but rising opportunities as non-communicable disease strategies mature.

Competitive Landscape

The competitive field is moderately fragmented yet trending toward consolidation as large pharmaceutical groups seek to shortcut R&D timelines through acquisitions. GSK’s USD 2 billion deal for efimosfermin and Gilead’s USD 4.3 billion purchase of CymaBay underscore the appetite for late-stage assets that complement metabolic franchises. Madrigal enjoys first-mover advantage but faces imminent pressure from Novo Nordisk, Eli Lilly, and AstraZeneca, each advancing differentiated mechanisms ranging from GLP-1s to PCSK9 inhibitors and triple-hormone agonists.

Strategic alliances are proliferating: Boehringer Ingelheim partnered with Ribo to co-develop RNAi therapeutics targeting hepatic genes, while smaller biotechs pursue FGF-21, ACC, and CCR2/5 pathways to capture niche fibrosis segments. Digital pathology and AI-diagnostic capabilities are emerging as competitive differentiators by reducing trial risk and compressing development timelines. Health-economic evidence generation is now integral to launch planning, given payers’ scrutiny of high acquisition costs.

White-space areas include pediatric indications, combination therapy regimens, and precision-medicine models based on genetic polymorphisms. Firms with comprehensive liver portfolios stand to benefit from bundling opportunities as health systems prefer integrated solutions across the metabolic continuum. Against this backdrop, marketing success will hinge on demonstrating clinically meaningful fibrosis reversal, cardiovascular risk reduction, and real-world safety in diverse populations.

Non-Alcoholic Fatty Liver Disease (NAFLD) Industry Leaders

-

Intercept Pharmaceuticals

-

Madrigal Pharmaceuticals

-

Novo Nordisk A/S

-

Gilead Sciences, Inc.

-

AbbVie, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GSK announced acquisition of efimosfermin for up to USD 2 billion, adding a Phase III-ready therapy targeting steatotic liver disease progression.

- May 2025: Madrigal Pharmaceuticals reported Q1 2025 net sales of USD 137.3 million for Rezdiffra and expects an EMA decision later in the year.

- March 2025: AstraZeneca’s AZD0780 oral PCSK9 inhibitor achieved 50.7% LDL reduction in PURSUIT Phase IIb, highlighting cardiovascular-liver synergies.

- March 2024: FDA granted accelerated approval to Rezdiffra as the first treatment for non-cirrhotic NASH with moderate-to-advanced fibrosis.

Global Non-Alcoholic Fatty Liver Disease (NAFLD) Market Report Scope

As per the scope of the report, non-alcoholic fatty liver disease is a condition characterized by the accumulation of excess fat in the liver of people. This is caused due to the growing burden of obesity, type 2 diabetes, metabolic syndrome, sedentary lifestyle, and genetic factors.

The non-alcoholic fatty liver disease is segmented into drug class, distribution channel, and geography. By drug class, the market is segmented into antioxidants, lipid lipid-lowering agents, fibrosis treatment agents, thiazolidinedione, FXR receptor agonists, biguanides, and other drug classes. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts were done based on the value (USD).

| Antioxidants |

| Lipid-Lowering Agents |

| Thiazolidinediones (TZDs) |

| FXR Receptor Agonists |

| Fibrosis Treatment Agents |

| Biguanides |

| Other Drug Classes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Oral |

| Parenteral |

| Adults |

| Geriatric |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antioxidants | |

| Lipid-Lowering Agents | ||

| Thiazolidinediones (TZDs) | ||

| FXR Receptor Agonists | ||

| Fibrosis Treatment Agents | ||

| Biguanides | ||

| Other Drug Classes | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| By Age Group | Adults | |

| Geriatric | ||

| Pediatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the non-alcoholic fatty liver disease market?

The market stands at USD 17.56 billion in 2025 and is projected to reach USD 36.94 billion by 2030.

Which drug class is growing fastest in the non-alcoholic fatty liver disease market?

FXR agonists are the fastest-growing class, expected to post a 17.01% CAGR through 2030.

Why is Asia-Pacific considered a high-growth region for NAFLD therapies?

Higher genetic susceptibility, rapid increases in obesity and diabetes, and expanding screening programs drive a 17.22% CAGR forecast for the region.

How does Rezdiffra differ from traditional NAFLD treatments?

Rezdiffra is the first FDA-approved disease-modifying therapy for non-cirrhotic NASH, targeting FXR pathways to improve liver histology, whereas earlier care relied mainly on lifestyle changes.

What role does AI play in accelerating NAFLD diagnosis?

AI-powered algorithms integrated with non-invasive tests achieve high sensitivity and specificity, reducing the need for liver biopsies and enabling large-scale screening.

Which distribution channel is expanding the fastest for NAFLD medications?

Online pharmacies are the fastest-growing channel, advancing at 16.98% CAGR as telemedicine adoption rises.