Nigeria Satellite Communications Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

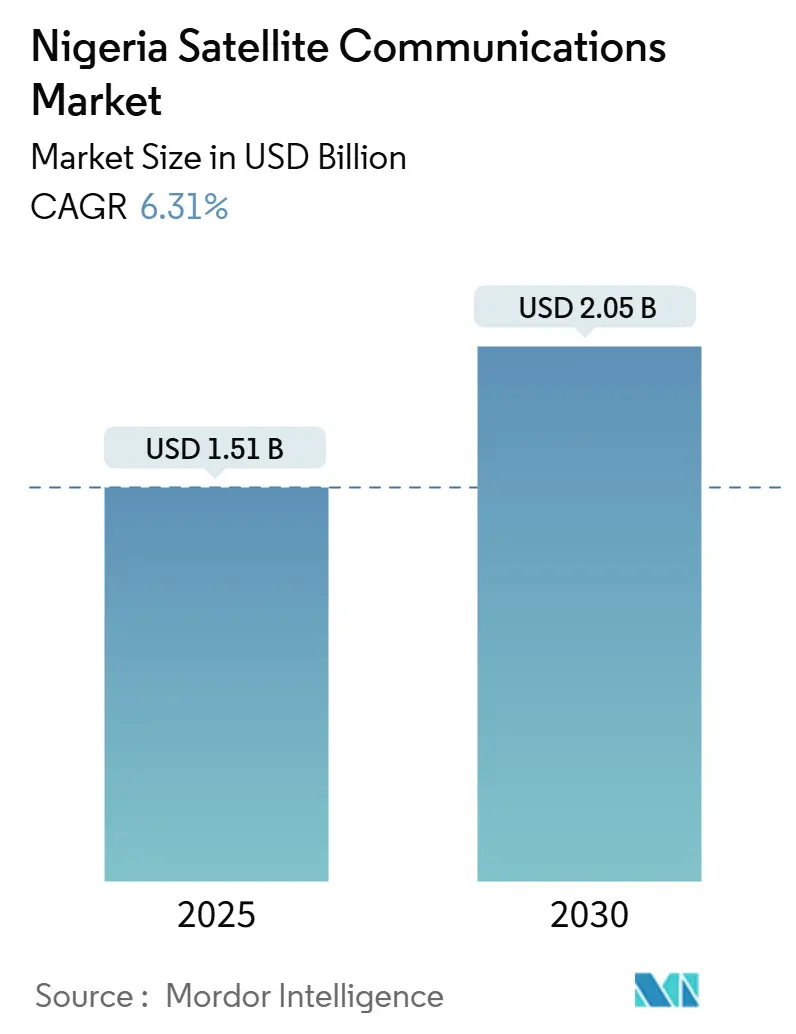

| Market Size (2025) | USD 1.51 Billion |

| Market Size (2030) | USD 2.05 Billion |

| Growth Rate (2025 - 2030) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nigeria Satellite Communications Market Analysis by Mordor Intelligence

The Nigerian Satellite Communications Market size is estimated to be USD 1.51 billion in 2025 and is expected to reach USD 2.05 billion by 2030, growing at a CAGR of 6.31% during the forecast period (2025-2030). Commercial demand is shifting from legacy geostationary capacity to low-Earth-orbit (LEO) constellations, which can deliver lower latency for rural broadband, cellular backhaul, and enterprise links. Defense procurement and offshore oil and gas operators are anchoring multi-year contracts that terrestrial fiber cannot economically support in conflict or deep-water zones, while government subsidy programs under the Universal Service Provision Fund (USPF) reduce deployment risk in low-ARPU states. Despite USD 1.6 billion in blended financing through the World Bank’s BRIDGE initiative, chronic right-of-way disputes, vandalism, and Nigeria’s fragile power grid keep satellite services in a strategic position as the resilient fallback for the National Broadband Plan’s 90% coverage mandate. Competitive intensity is rising as Starlink, OneWeb, and future Kuiper service offerings undercut geostationary incumbents on latency and price, even after Starlink’s October 2024 tariff increase. Meanwhile, Nigeria’s import tariffs, averaging 49.6% on VSAT and gateway hardware, continue to inflate capital costs and slow rural rollouts.

Key Report Takeaways

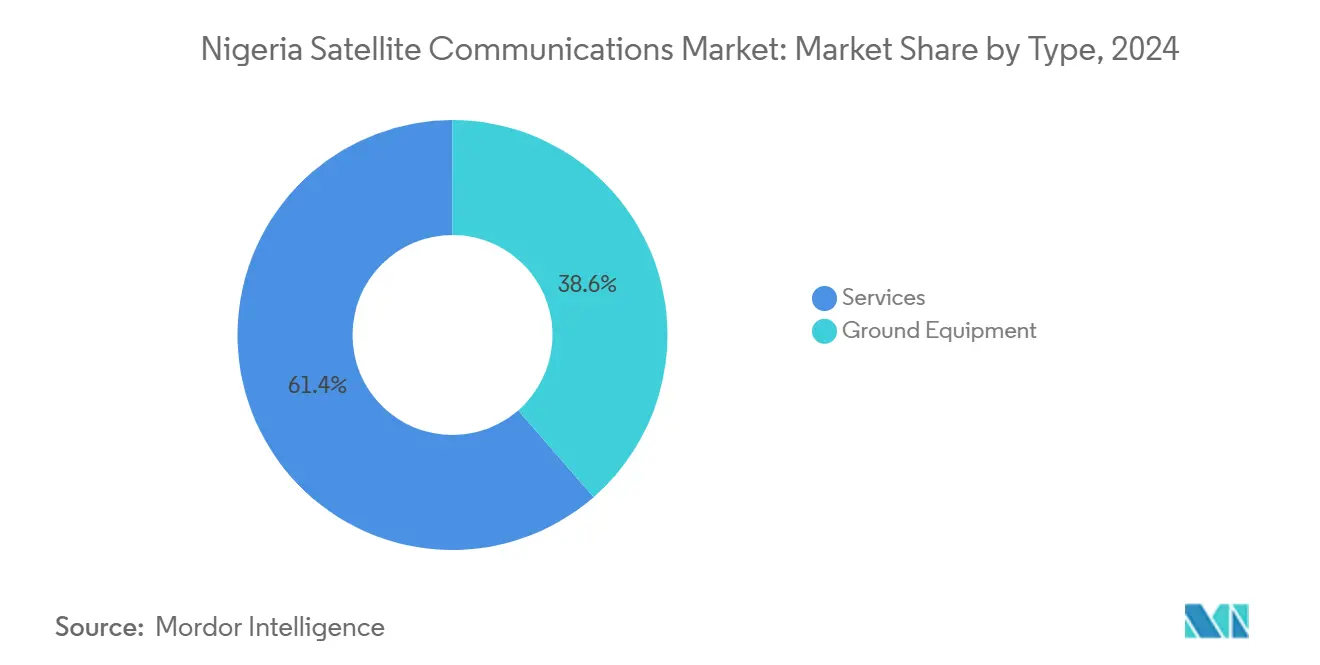

- By type, services led the Nigerian satellite communication market with a 61.40% share in 2024, whereas ground equipment is projected to expand at a 7.19% CAGR through 2030, the fastest among all types.

- By technology type, Very Small Aperture Terminal (VSAT) commanded 38.90% of the Nigerian satellite communication market in 2024, while Low-Earth-Orbit (LEO) Constellations are forecast to record an 8.11% CAGR to 2030.

- By platform, land installations accounted for 51.30% of the Nigerian satellite communication market in 2024; maritime connectivity is expected to advance at a 7.25% CAGR by 2030.

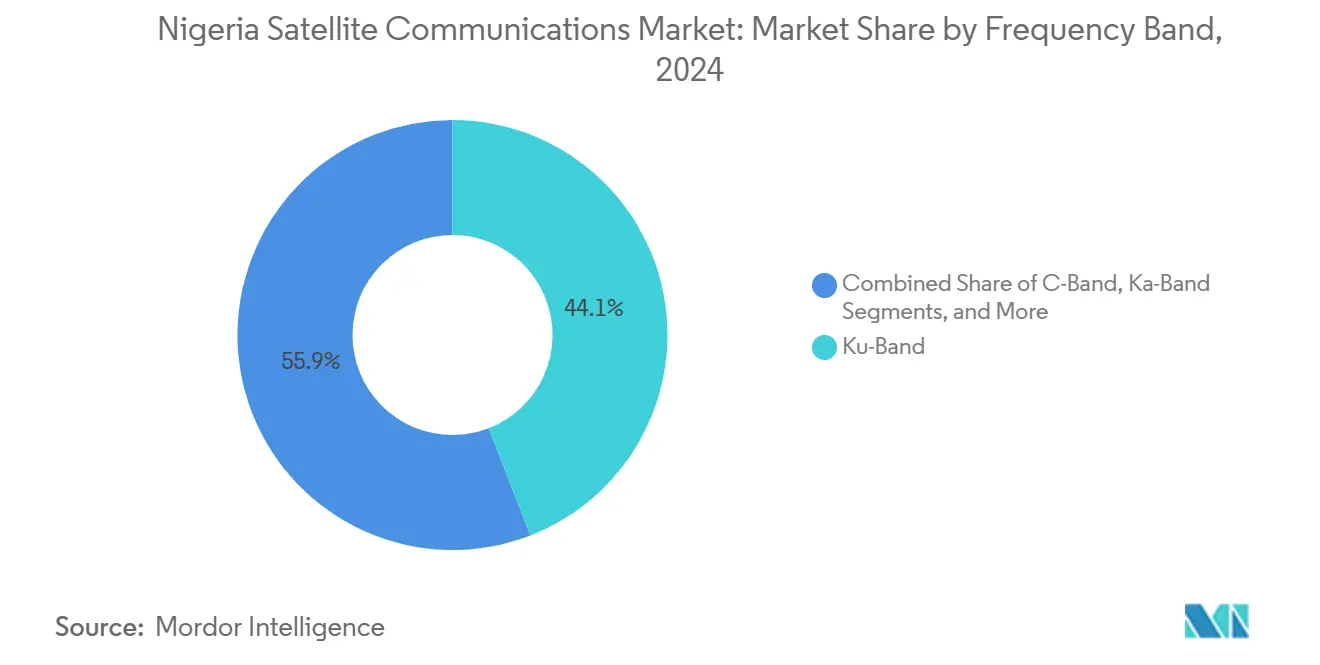

- By frequency, Ku-band accounted for 44.10% of the Nigerian satellite communication market size in 2024, whereas Ka-band is projected to rise at a 7.95% CAGR to 2030.

- By end user, consumer broadband/SOHO users represented 36.80% in 2024, while the defense and government segment is poised to climb at an 8.65% CAGR through 2030.

Nigeria Satellite Communications Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Broadband Plan and NigComSat Expansion | +1.2% | National, with priority in North-Central (FCT Abuja hub) and rural North-East/North-West | Medium term (2-4 years) |

| OTT/Video Traffic Surge in Rural Areas | +0.9% | National, concentrated in South-West (Lagos, Oyo) and South-South (Rivers, Delta) urban spillover to rural | Short term (≤ 2 years) |

| Defense and Offshore Oil-Gas Connectivity Demand | +1.5% | North-East (Borno, Yobe, Adamawa conflict zones), South-South (Niger Delta offshore), Gulf of Guinea maritime | Long term (≥ 4 years) |

| Rural Telephony via Universal Service Provision Fund | +0.8% | National, emphasis on Tier 4 and Tier 5 states (Adamawa, Ebonyi, Gombe, Jigawa, Katsina, Kebbi, Taraba, Yobe, Zamfara) | Medium term (2-4 years) |

| Fintech/Agency-Banking Backhaul Needs | +0.7% | National, urban-rural corridors in South-West and South-East (Anambra, Imo, Enugu agency-banking hubs) | Short term (≤ 2 years) |

| Drone-Based Precision Agriculture Links | +0.4% | North-Central (Middle Belt crop zones), North-West (Kaduna, Kano commercial farms) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Broadband Plan and NigComSat Expansion

The 2020-2025 broadband roadmap targets 90% population coverage; however, penetration stood at 43.53% in March 2024, leaving a 46.47-point gap that satellite technology can bridge in fiber-deficient regions. [1]Nigerian Communications Commission, “Quality of Service Regulations,” ncc.gov.ng NigComSat’s January 2025 agreement with Eutelsat to distribute OneWeb capacity and the July 2024 Hotspot Network deal to connect rural communities reposition the agency from a single-orbit operator to a hybrid LEO-GEO provider. [2]NigComSat, “NigComSat and Eutelsat Partnership Announcement,” nigcomsat.gov.ng A June 2024 partnership with Infratel Africa to build 100 Ka-band hubs front-loads ground-equipment spending, accelerating the Nigeria satellite communication market beyond traditional GEO services. Execution risk persists because NigComSat must launch two delayed satellites or lose International Telecommunication Union (ITU) slots. New quality-of-service regulations impose fines of NGN 5 million, plus NGN 500,000 daily penalties for non-compliance, raising the operational stakes for all licensees.

Defense and Offshore Oil-Gas Connectivity Demand

May 2025 government approval for four surveillance satellites and the 2024 NigComSat-Army capacity-sharing pact tilt procurement toward sovereign, defense-grade bandwidth. Offshore, Shell’s pilot using Globalstar and Identec on nine vessels shows oil majors’ willingness to pay premium rates for low-latency links that avoid cellular dead zones. It is expected that oil and gas IoT endpoints will rise, a trajectory that channels high-margin enterprise revenue into the Nigerian satellite communication market. Together, defense and energy clients underpin multi-year contracts that buffer operators against fluctuations in consumer prices.

OTT/Video Traffic Surge in Rural Areas

Intelsat’s October 2024 CellBackhaul Nigeria launch in Lagos and Africa Mobile Networks’ integration of Starlink backhaul illustrate a pivot: satellite is now a first-choice solution for rural cell-site expansion. According to the International Telecommunication Union (ITU), the number of global satellite users is expected to double to 500 million by 2030, supporting tele-education, e-health, and live-streaming services that will significantly amplify rural video traffic. [3]International Telecommunication Union, “State of Broadband 2024,” itu.int

Fintech and Agency-Banking Backhaul Needs

Agency-banking points in Anambra, Imo, and Enugu rely on always-on connectivity for point-of-sale transactions, yet terrestrial outages persist. Starlink terminals and Ka-band VSAT links enable fintech providers to clear transactions within regulatory settlement windows, minimizing failed payments that erode trust. USPF subsidies further de-risk deployments in Tier 3 and Tier 4 states, extending digital financial inclusion and steadily enlarging the Nigeria satellite communication market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Import Tariffs on VSAT/Gateways | -0.9% | National, acute in Tier 1 (Lagos) and Tier 2 (FCT Abuja, Kaduna, Kano, Rivers) due to higher spectrum fees | Short term (≤ 2 years) |

| Spectrum-Allocation Delays and Regulatory Bottlenecks | -0.6% | National, federal-level NCC licensing and ITU coordination | Medium term (2-4 years) |

| Power-Grid Unreliability Inflating OPEX | -1.1% | National, most severe in North-East (Borno, Yobe) and rural Tier 4/Tier 5 states with <60% grid reach | Long term (≥ 4 years) |

| Gateway Sabotage Risk in Conflict Zones | -0.4% | North-East (Borno, Yobe, Adamawa), spillover to North-West (Zamfara, Katsina, Sokoto) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Import Tariffs on VSAT/Gateways

World Trade Organization data place Nigeria’s average tariff on non-agricultural imports at 49.6%, making landed costs for Ka-band hubs and VSAT terminals unpredictable and often unviable for smaller providers. The Nigerian Customs Service classifies satellite gear under multiple HS codes, some of which attract double-digit duties, compressing margins in rural deployments. NCC spectrum fees add more pressure, with a national Ka-band license topping NGN 50 million annually for 500 MHz. Revised type-approval rules now require physical samples within 60 days or applications lapse, raising logistical costs for vendors. Collectively, these factors slow hardware refresh cycles and dampen near-term growth in the Nigeria satellite communication market.

Power-Grid Unreliability Inflating OPEX

Nigeria delivers only 5 GW to end users, against an installed capacity of 14-16 GW, forcing operators to run diesel generators or solar-battery hybrids at every teleport and VSAT hub. The World Bank pegs grid‐failure costs at roughly 2% of GDP each year, a burden that translates into high operating expenses for satellite networks that must uphold 99.9% uptime SLAs. The 2023 Electricity Act decentralizes regulation, complicating multi-state permitting and adding compliance overhead. Operators like EtinPower bundle solar power with satellite links to mitigate outages, but the premium inflates the total cost of ownership by as much as 30% compared to markets with stable grids.

Segment Analysis

By Type: Services Remain Dominant while Ground Equipment Accelerates

Services captured 61.40% of the 2024 value, owing to recurring mobile and fixed satellite contracts. However, ground equipment is forecast to grow at a CAGR of 7.19% within the forecast period, outpacing the overall Nigerian satellite communication market. This surge reflects 100 planned Ka-band hub locations under the NigComSat-Infratel build-out, as well as widespread LEO terminal deployments for OneWeb and Starlink. Gateway clustering around Lagos, Abuja, and Port Harcourt enables operators to offload traffic to submarine cables, reducing satellite hop costs. VSAT uptake in Tier 4 and Tier 5 states benefits from lower NGN 300,000 per MHz spectrum fees and USPF support, widening rural footprints. Upgraded network operation centers are adopting software-defined networking that can dynamically route across GEO, MEO, and LEO capacity, a capability older NOCs lack.

Between 2024 and 2026, companies are making front-loaded equipment purchases, setting the stage for service revenue growth later in the decade. While satellite news-gathering trucks play a crucial role in covering conflict zones, they generate only modest incremental revenue. With the introduction of Draft Commercial Satellite Regulations, which may enforce local-content quotas on equipment sourcing, international suppliers are eyeing potential joint ventures with Nigerian integrators.

By Technology Type: LEO Constellations Disrupt VSAT Incumbency

VSAT solutions accounted for 38.90% of the 2024 spend, primarily driven by long-standing Ku-band and C-band enterprise contracts. However, LEO subscriber counts are growing at an 8.11% CAGR, driven by Starlink’s 65,564 subscribers and new OneWeb enterprise trials. High-throughput satellites such as Avanti’s HYLAS-4 and Yahsat’s forthcoming AY4/AY5 expand Ka-band capacity over West Africa, positioning GEO operators to bundle backhaul with managed cybersecurity and quality-of-service guarantees. SES’s O3b mPOWER brings medium-orbit connectivity optimized for trunking and 5G backhaul, adding a middle-latency tier to service portfolios.

Direct-to-home broadcasting has reached a plateau, with MultiChoice's price increases aimed at addressing content inflation rather than driving subscriber growth. In this context, legacy VSAT providers are transitioning toward hybrid LEO-GEO bundles, emphasizing managed services, cybersecurity, and quality-of-service-backed SLAs to protect their margins against competition from pure-play LEO offerings. As a result, the Nigerian satellite communication industry is expected to experience technological diversification rather than complete replacement.

By Platform: Maritime Connectivity Gains Momentum

Land installations still account for 51.30% of the 2024 Nigerian satellite communication market size, servicing consumer broadband, enterprise links, and cellular backhaul. Maritime demand, however, is projected to expand at a 7.25% CAGR as offshore operators upgrade rig-to-shore telemetry, crew welfare internet, and environmental monitoring. Vessel-borne M2M links also support regulatory compliance and fuel-efficiency analytics, making ARPU in maritime significantly higher than land-based consumer packages.

Portable terminals cater to disaster response and field journalism, while airborne links remain niche due to the expense of aeronautical-rated hardware and regulatory inertia surrounding in-flight connectivity. NCC’s streamlined GMPCS rules, released in 2024, lower barriers for entry into maritime and aeronautical services, coaxing foreign operators to localize gateways or establish Nigerian subsidiaries.

By Frequency Band: Ka-Band Ascends while Ku-Band Plateaus

Ku-band maintained a 44.10% share in 2024, supported by entrenched DTH and enterprise VSAT networks. Yet Ka-band is forecast to rise at a 7.95% CAGR, buoyed by NigComSat-1R’s capacity and new AY4/AY5 satellites that offer higher throughput per megahertz. Ka-band spot beams maximize frequency reuse in dense urban markets, facilitating competitive pricing for high-speed links. C-band remains the fallback for rain-fade resilience, especially in maritime and government applications. Nigeria’s adoption of 6 GHz for Wi-Fi 6E may introduce adjacent-band interference, prompting some operators to migrate feeder links to Q/V-band trials.

In Lagos and Abuja, spectrum fees are steering operators towards higher-frequency deployments. This trend is pushing them to favor Ka-band and, in the future, millimeter-wave backhaul in these Tier 1 cities. Meanwhile, in rural Tier 5 states, the Ku-band remains the preferred choice, thanks to its affordable terminal prices and broader coverage. As a result, operators are adopting dual-band strategies, continuing to use Ku-band for its extensive reach while transitioning to Ka-band to boost capacity.

Note: Segment shares of all individual segments available upon report purchase

By End User: Defense and Government Outpace Consumer Broadband

Consumer and SOHO users accounted for 36.80% of 2024 revenue, driven by the rapid adoption of Starlink and peri-urban fixed wireless access. Nonetheless, defense and government spending are projected to climb at an 8.65% CAGR, reshaping demand patterns in the Nigeria satellite communication market. The Defense Space Administration’s reliance on NigeriaSat-2 and NigeriaSat-X for counter-terrorism tasks highlights an enduring preference for sovereign, encrypted capacity.

Transport and logistics firms are adopting satellite IoT for cargo visibility along the Lagos-Kano routes, while media organizations rely on satellite news gathering during elections and emergencies. Agriculture, supported by NASRDA’s CropWatch, leverages satellite imagery for yield estimation and drought alerts, though volumes remain modest. The education and healthcare segments exhibit latent demand that could be unlocked once affordable micro-VSAT kits become available.

Geography Analysis

A blend of high-density cities and vast, underserved rural expanses characterizes Northern Nigeria. In the North-West, Kano and Kaduna drive enterprise contracts, whereas Jigawa, Kebbi, and Zamfara rely on subsidized VSAT deployments due to lower spectrum fees. Security threats in Zamfara and Katsina heighten the value proposition of LEO backhaul for government and NGO communications. Rainfall deficits, 64% below normal in early 2024, underscore the importance of satellite imagery for agricultural early warning.

North-East states such as Borno and Yobe are the epicenter of defense-centric demand. Government approval for four new satellites underpins 24/7 reconnaissance, making the region a priority for secure gateway sites that can withstand sabotage and other threats. Starlink devices smuggled across borders prompted calls for geofencing, potentially restricting consumer service areas but deepening enterprise demand for controlled networks.

North-Central, anchored by Abuja, hosts NigComSat and NASRDA headquarters along with prime teleport locations. Project 774 aims to connect every local government secretariat via satellite backhaul, extending administrative digitalization into Benue and Niger. Spectrum management and policy decisions emanating from Abuja directly steer nationwide capacity allocation. South-West, spearheaded by Lagos, combines dense fiber with satellite redundancy. Intelsat’s CellBackhaul service and MainOne’s 2Africa cable landing highlight a hybrid model where terrestrial and satellite links coexist. USPF subsidies drive satellite fixed wireless into peri-urban areas of Ogun and Ondo, where fiber lags behind demand.

South-East fintech corridors depend on satellite for agency-banking uptime. Tier 3 spectrum fees keep capacity affordable for small and midsize enterprises. Meanwhile, the South-South’s Niger Delta offshore sector fuels maritime growth; Shell’s Globalstar pilot demonstrates vessel telemetry use cases that will scale as oil and gas IoT endpoints near 19 million globally by 2028.

Competitive Landscape

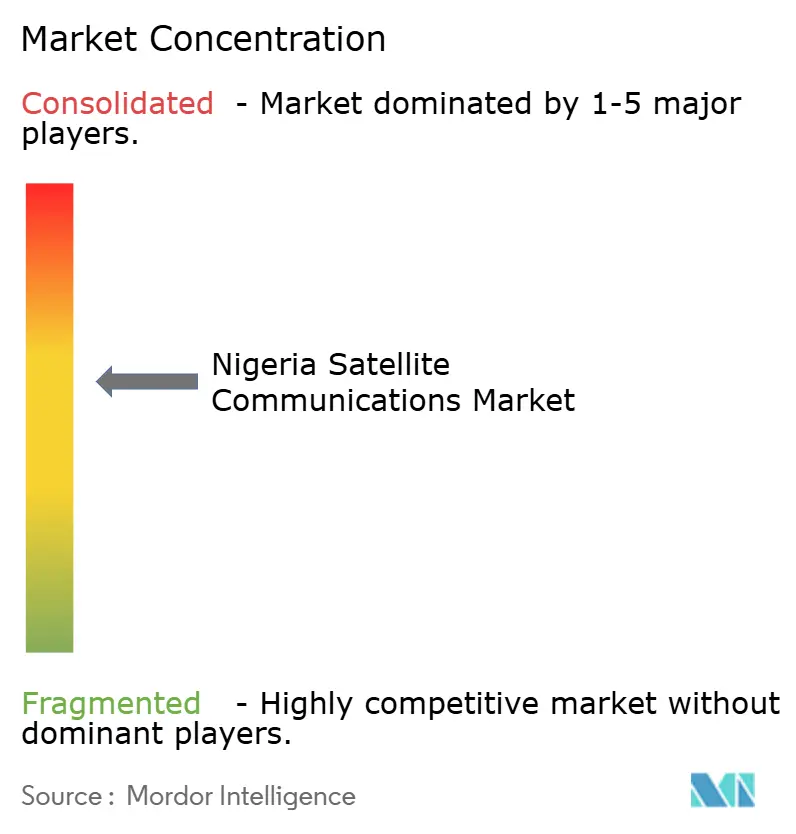

Nigeria's satellite communication market is highly competitive, with NigComSat, Starlink, and Eutelsat-OneWeb controlling 45% of the revenue and setting pricing and service standards, despite the presence of smaller VSAT resellers. The market operates as a league table, with major players dominating capacity leases, while regional specialists target niches such as satellite news gathering and precision agriculture.

NigComSat's deal with Eutelsat integrates OneWeb's low-latency links with its geostationary bandwidth to retain enterprise customers. However, delays in spacecraft construction risk losing two ITU orbital slots, potentially ceding spectrum rights to competitors. Starlink, with 65,564 subscribers by Q3 2024, became Nigeria's second-largest ISP in under two years. Despite backlash over an October 2024 fee hike from NGN 38,000 to NGN 75,000, demand for 200 Mbps speeds remains strong. The Nigerian Communications Commission has tightened quality-of-service and device registration rules, increasing compliance costs for operators.

Mobile carriers are expanding into satellite. MTN Nigeria renewed its 800 MHz license through 2034 and partnered with Omnispace to test non-terrestrial 5G. Intelsat launched CellBackhaul in Lagos to reduce rural microwave costs, while SES is expanding its O3b mPOWER fleet to meet regional bandwidth demand. Startups like EtinPower are bundling solar mini-grids with satellite connectivity, appealing to businesses seeking alternatives to diesel and grid outages. These developments drive competition, improving service diversity and network reliability for Nigerian enterprises and households.

Nigeria Satellite Communications Industry Leaders

-

Nigerian Communications Satellite Ltd. (NigComSat)

-

Galaxy Backbone Plc

-

Globacom Ltd.

-

Gilat Satellite Networks Ltd.

-

Eutelsat Group (OneWeb)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NASRDA and China’s Galaxy Space agree on direct-to-device satellite services, including joint R&D and CubeSat production.

- January 2025: Eutelsat and NigComSat sign a multi-year LEO capacity partnership to extend high-speed connectivity nationwide.

- January 2025: MTN Nigeria secures a 10-year 800 MHz license renewal, aligning both channel tenures to December 2034.

- October 2024: Intelsat Launches CellBackhaul Nigeria in Lagos to Support MNO Rural Expansion.

Nigeria Satellite Communications Market Report Scope

The Nigeria Satellite Communication Market Report is Segmented by Type (Ground Equipment [Gateway, Very Small Aperture Terminal (VSAT), Network Operation Centre (NOC), Satellite News Gathering (SNG)], Services [Mobile Satellite Services (MSS), Fixed Satellite Services (FSS), Earth-Observation Services]), Technology Type (Very Small Aperture Terminal (VSAT), High-Throughput Satellites (HTS), Low-Earth-Orbit (LEO) Constellations, Medium-Earth-Orbit (MEO) Constellations, Direct-to-Home (DTH) Broadcasting), Platform (Portable, Land, Maritime, Airborne), Frequency Band (C-Band, Ku-Band, Ka-Band, Other Bands), and End-user Vertical (Consumer Broadband/SOHO Users, Defense and Government, Transport and Logistics, Media and Entertainment, Agriculture, and Other End-user Verticals). The Market Forecasts are Provided in Value (USD).

| Ground Equipment | Gateway |

| Very Small Aperture Terminal (VSAT) | |

| Network Operation Center (NOC) | |

| Satellite News Gathering (SNG) | |

| Services | Mobile Satellite Services (MSS) |

| Fixed Satellite Services (FSS) | |

| Earth-Observation Services |

| Very Small Aperture Terminal (VSAT) |

| High-Throughput Satellites (HTS) |

| Low-Earth-Orbit (LEO) Constellations |

| Medium-Earth-Orbit (MEO) Constellations |

| Direct-to-Home (DTH) Broadcasting |

| Portable |

| Land |

| Maritime |

| Airborne |

| C-Band |

| Ku-Band |

| Ka-Band |

| Other Bands (L, S, X, Q/V, etc.) |

| Consumer Broadband/SOHO Users |

| Defense and Government |

| Transport and Logistics |

| Media and Entertainment |

| Agriculture |

| Other End-user Verticals (Education, Healthcare, etc.) |

| By Type | Ground Equipment | Gateway |

| Very Small Aperture Terminal (VSAT) | ||

| Network Operation Center (NOC) | ||

| Satellite News Gathering (SNG) | ||

| Services | Mobile Satellite Services (MSS) | |

| Fixed Satellite Services (FSS) | ||

| Earth-Observation Services | ||

| By Technology Type | Very Small Aperture Terminal (VSAT) | |

| High-Throughput Satellites (HTS) | ||

| Low-Earth-Orbit (LEO) Constellations | ||

| Medium-Earth-Orbit (MEO) Constellations | ||

| Direct-to-Home (DTH) Broadcasting | ||

| By Platform | Portable | |

| Land | ||

| Maritime | ||

| Airborne | ||

| By Frequency Band | C-Band | |

| Ku-Band | ||

| Ka-Band | ||

| Other Bands (L, S, X, Q/V, etc.) | ||

| By End-user Vertical | Consumer Broadband/SOHO Users | |

| Defense and Government | ||

| Transport and Logistics | ||

| Media and Entertainment | ||

| Agriculture | ||

| Other End-user Verticals (Education, Healthcare, etc.) | ||

Key Questions Answered in the Report

How large is the Nigeria satellite communication market in 2025?

The Nigeria satellite communication market size is USD 1.51 billion in 2025 and is projected to reach USD 2.05 billion by 2030.

What is driving rapid adoption of LEO services?

LEO constellations offer sub-100 ms latency and faster throughput than legacy geostationary links, making them attractive for rural broadband, cellular backhaul, and offshore applications.

Which segment is growing fastest?

Ground equipment is forecast to post a 7.19% CAGR as operators deploy Ka-band gateways, VSAT terminals, and LEO tracking antennas.

Why are defense and government users increasing spend?

Four new surveillance satellites and multi-year capacity leases for border monitoring and counter-terrorism have elevated defense demand, leading to an 8.65% CAGR through 2030.

How do tariffs affect satellite equipment costs?

Average applied import duties of 49.6% on non-agricultural goods significantly raise landed costs for VSAT and gateway hardware, hindering rollouts in price-sensitive regions.

Page last updated on: