| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 4.80 Million cubic feet |

| Market Volume (2030) | 5.16 Million cubic feet |

| CAGR | 1.45 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Nigeria Upstream Oil and Gas Market Analysis

The Nigeria Oil and Gas Upstream Market size is estimated at 4.80 million cubic feet in 2025, and is expected to reach 5.16 million cubic feet by 2030, at a CAGR of 1.45% during the forecast period (2025-2030).

Nigeria's oil and gas upstream sector is undergoing significant transformation driven by regulatory reforms and infrastructure development initiatives. The country possesses substantial hydrocarbon resources, with approximately 208.62 trillion cubic feet of proven gas reserves as of 2022, marking a 1.01% increase from the previous year. The Nigerian government has been actively implementing gas-centric policies and programs, including the National Gas Policy (NGP), to ensure gas-based industrialization and sustainable economic growth. The sector has witnessed increased attention towards gas infrastructure development, particularly through the Nigerian Gas Flare Commercialization Program (NGFCP), which aims to reduce gas flaring and optimize resource utilization.

The oil and gas upstream sector has attracted significant investments from major international oil companies, demonstrating continued confidence in Nigeria's hydrocarbon potential. In December 2023, Shell announced plans to invest approximately USD 5 billion in offshore oil opportunities and committed an additional USD 1 billion over the next five to ten years to boost natural gas output. This investment surge coincides with TotalEnergies' significant Ntokon oil and gas exploration discovery in mid-2023, which successfully tested at approximately 5,000 barrels per day of 40° API oil, highlighting the continued exploration success in the region.

Security challenges and operational inefficiencies continue to impact the sector's performance, particularly in onshore operations. In 2022, Nigeria's daily natural gas production averaged 44.3 billion standard cubic meters, representing relatively low utilization of its vast reserves. The government has responded by implementing new security measures and technological solutions to combat these challenges. The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) has also taken steps to optimize resource management, including reviewing inactive petroleum exploration leases and promoting more efficient operational practices.

The export market plays a crucial role in Nigeria's oil and gas upstream sector, with approximately 27% of natural gas production directed towards exports in 2022, contributing significantly to government revenue. The country is actively working to expand its export capabilities while simultaneously developing domestic gas infrastructure. Recent developments include the implementation of the Mini Bid Round 2022, which opened up seven offshore blocks covering approximately 6,700 km² in water depths of 1,150m to 3,100m for international investment. These initiatives are complemented by the government's ambitious energy transition plan, which seeks USD 10 billion in funding to expand gas power generation and achieve universal electricity access by 2030.

Nigeria Upstream Oil and Gas Market Trends

Increasing Investments in Exploration and Production Activities

Nigeria's oil and gas exploration and production sector is witnessing a significant surge in investments, driven by government reforms and attractive opportunities in both offshore drilling and onshore drilling assets. In December 2023, Shell announced plans to invest approximately USD 5 billion in offshore drilling opportunities in Nigeria, along with an additional USD 1 billion commitment over the next five to ten years to boost natural gas output. This substantial investment demonstrates growing confidence in Nigeria's upstream sector, particularly as the country holds significant proven gas reserves of 208.62 trillion cubic feet as of 2022. The investment climate has been further enhanced by the Nigerian government's implementation of the Petroleum Industry Bill (PIB) in 2021, which has created a more conducive environment for foreign investment through amendments to regulations, royalties, and taxes.

The momentum in exploration and production activities is evidenced by recent discoveries and development projects. In mid-2023, TotalEnergies announced the Ntokon oil and gas discovery on OML102 offshore Nigeria, with successful testing achieving up to 5,000 barrels per day of 40° API oil. Additionally, the Nigerian National Petroleum Company Limited secured a USD 5 billion corporate finance commitment from the African Export-Import Bank to fund major investments in the upstream sector. The government's proactive approach is also reflected in the 2022/2023 Mini Bid Round, which offered seven offshore blocks covering approximately 6,700 km² in water depths of 1,150m to 3,100m. These initiatives align with Nigeria's ambitious target to increase crude production to 2.6 MMbbl/d by 2027, supported by the renewal of production-sharing contracts for five Oil Mining Leases (OMLs) - 128, 130, 132, 133, and 138, which is expected to generate approximately USD 500 billion in revenue for the country.

Understand The Key Trends Shaping This Market

Download PDF

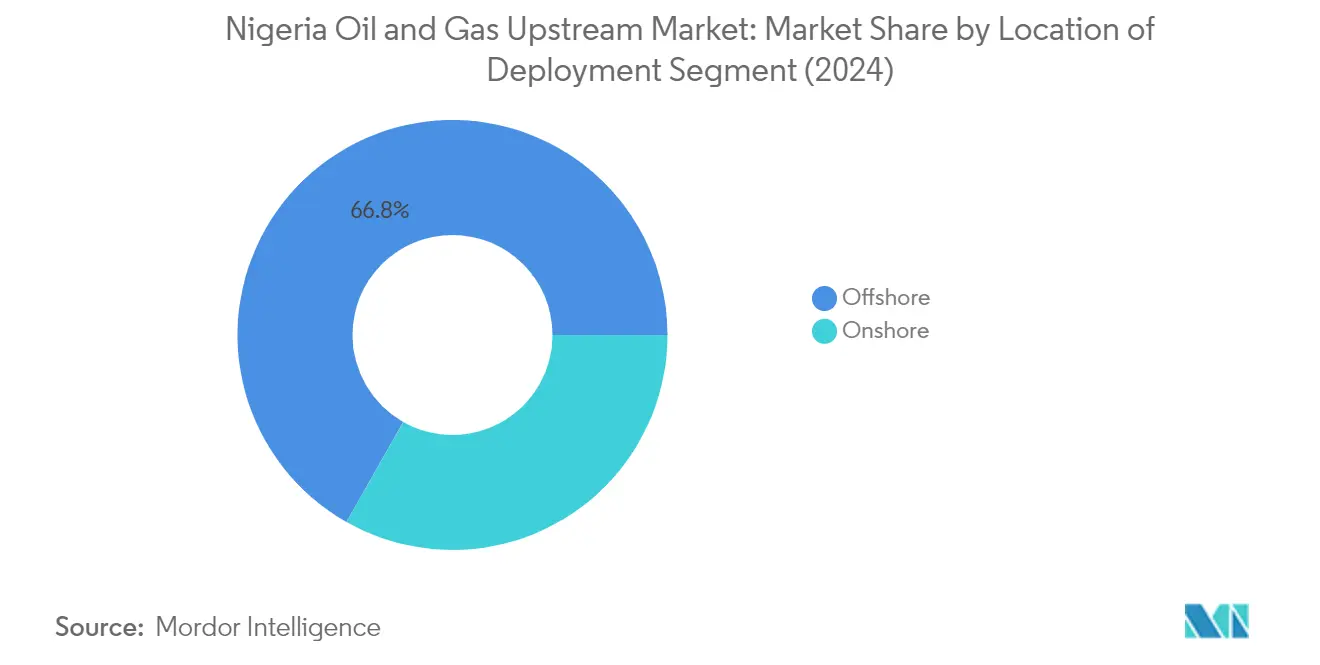

Segment Analysis: Location of Deployment

Offshore Segment in Nigeria Oil and Gas Upstream Market

The offshore drilling segment dominates the Nigeria oil and gas upstream market, commanding approximately 67% market share in 2024. This segment's prominence is driven by significant developments in both deep and shallow water projects, with several major international oil companies focusing their investments in offshore drilling exploration and production activities. The segment's growth is further bolstered by recent discoveries like TotalEnergies' Ntokon oil and gas discovery on OML102 offshore, which successfully tested at rates of approximately 5,000 barrels per day. Shell's announcement in 2024 to invest about USD 5 billion in offshore oil opportunities and an additional USD 1 billion over the next five to ten years for natural gas output expansion demonstrates the continued attractiveness of Nigeria's offshore sector. The segment is projected to grow at around 2.5% CAGR from 2024 to 2029, driven by upcoming projects such as TotalEnergies' offshore Preowei Phase I development and Shell's Bonga North development.

Onshore Segment in Nigeria Oil and Gas Upstream Market

The onshore drilling segment plays a crucial role in Nigeria's oil and gas upstream market, particularly in the development of mainland oil fields and gas deposits. This segment faces unique challenges, including security concerns, oil theft, and infrastructure vandalism, which have impacted production levels and investment decisions. However, the segment continues to attract attention from domestic players and some international operators who are working to optimize production from existing fields and develop new ones. Recent initiatives by the Nigerian government to revoke unused oil exploration licenses and promote new investments aim to reinvigorate onshore drilling exploration and production activities. The segment's development is also supported by the government's focus on increasing domestic gas utilization and reducing gas flaring, which creates opportunities for onshore gas field development. Additionally, the use of well intervention techniques is being explored to enhance production efficiency.

Nigeria Upstream Oil and Gas Industry Overview

Top Companies in Nigeria Oil and Gas Upstream Market

The Nigerian oil and gas upstream market is dominated by major international and domestic players, including Nigerian National Petroleum Corporation, Shell PLC, Chevron Corporation, ExxonMobil Corporation, TotalEnergies SE, and Oando Energy Resources Inc. These companies are focusing on technological advancement through robotics, advanced instrumentation, drones, and upstream technology solutions to enhance operational efficiency. Strategic collaborations and joint ventures remain key growth drivers, with companies partnering to develop new fields and expand production capacity. Companies are increasingly investing in offshore exploration and development projects while also maintaining onshore operations. Environmental sustainability and local content development have become crucial aspects of corporate strategy, with companies investing in gas monetization projects and reducing flaring activities. Digital transformation initiatives are being implemented across operations to improve production monitoring, maintenance, and safety protocols.

Market Structure Shows Dynamic Competitive Environment

The Nigerian oil and gas upstream market exhibits a balanced mix of international oil companies (IOCs) and indigenous operators, with the state-owned NNPC playing a central role through joint ventures and production sharing contracts. The market structure is characterized by significant consolidation activities, particularly among indigenous players seeking to acquire divested assets from international oil companies. Recent years have witnessed notable merger and acquisition activities, including Oando's acquisition of Nigerian Agip Oil Company and strategic partnerships between local and international players for field development.

The competitive landscape is evolving with the emergence of new indigenous players and the strategic repositioning of established companies. International oil companies are increasingly focusing on deepwater assets while divesting from onshore operations, creating opportunities for local players to expand their portfolios. The market is seeing increased participation from independent oil companies and marginal field operators, contributing to a more diverse competitive environment. Companies are adopting various partnership models, including joint ventures and production sharing contracts, to share risks and leverage complementary capabilities.

Innovation and Adaptation Drive Future Success

Success in the Nigerian upstream sector increasingly depends on companies' ability to adopt advanced technologies and maintain operational efficiency while managing security challenges. Incumbent players are focusing on deepwater exploration and development, leveraging their technical expertise and financial capabilities to maintain market leadership. Companies are investing in local content development and community engagement programs to ensure sustainable operations. The ability to navigate regulatory requirements, particularly regarding environmental protection and local content development, has become a critical success factor.

New entrants and growing players can gain market share by focusing on specialized capabilities, particularly in marginal field development and enhanced oil recovery techniques. Strategic partnerships with technology providers and service companies are becoming essential for maintaining competitiveness. Companies must develop robust risk management strategies to address security concerns and operational challenges in both onshore and offshore environments. The increasing focus on gas development and monetization presents opportunities for diversification and growth. Success also depends on companies' ability to maintain strong relationships with regulatory authorities and local communities while adapting to evolving market conditions and environmental requirements. Additionally, the integration of oil and gas software and oil and gas equipment is crucial for production optimization and enhancing operational efficiency.

Nigeria Upstream Oil and Gas Market Leaders

-

Chevron Corporation

-

ExxonMobil Corporation

-

Royal Dutch Shell PLC

-

Nigerian National Petroleum Corporation

-

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Nigeria Upstream Oil and Gas Market News

- In February 2021, the government announced its plans to overhaul the Nigerian Petroleum Exchange (NIPEX) to shed more light on inventory management. The country's oil management is plagued by no synergy between different sets of the institution, both public and private. The government is expected to take more proactive steps in this direction in the coming years.

- The government planned to pass the Petroleum Industry Bill (PIB) in 2021. This bill may directly aid in creating clear structures, which may boost the development of the industry.

- In February 2021, Nigeria launched an exercise to cut upstream production costs to secure the country's energy future, primarily due to the low cost of oil, which leads to meager profit even on high expenditures.

Nigeria Upstream Oil and Gas Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Oil and Gas Reserves in Nigeria, till 2020

- 4.3 Crude Oil and Natural Gas Production, Historic and Forecast, in thousand barrels and billion cubic feet, till 2027

- 4.4 Active Rig Count, by Location of Deployment, till 2020

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Key Upcoming Upstream Oil and Gas Projects

-

4.8 Market Dynamics

- 4.8.1 Drivers

- 4.8.2 Restraints

- 4.9 Supply Chain Analysis

- 4.10 PESTLE Analysis

5. Location of Deployment

- 5.1 Onshore

- 5.2 Offshore

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Nigerian National Petroleum Corporation

- 6.3.2 Royal Dutch Shell PLC

- 6.3.3 Chevron Corporation

- 6.3.4 ExxonMobil Corporation

- 6.3.5 TotalEnergies SE

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Nigeria Upstream Oil and Gas Industry Segmentation

The Nigerian oil and gas upstream market report includes:

Need A Different Region or Segment?

Customize Now

Nigeria Upstream Oil and Gas Market Research FAQs

How big is the Nigeria Oil and Gas Upstream Market?

The Nigeria Oil and Gas Upstream Market size is expected to reach 4.80 million cubic feet in 2025 and grow at a CAGR of 1.45% to reach 5.16 million cubic feet by 2030.

What is the current Nigeria Oil and Gas Upstream Market size?

In 2025, the Nigeria Oil and Gas Upstream Market size is expected to reach 4.80 million cubic feet.

Who are the key players in Nigeria Oil and Gas Upstream Market?

Chevron Corporation, ExxonMobil Corporation, Royal Dutch Shell PLC, Nigerian National Petroleum Corporation and TotalEnergies SE are the major companies operating in the Nigeria Oil and Gas Upstream Market.

What years does this Nigeria Oil and Gas Upstream Market cover, and what was the market size in 2024?

In 2024, the Nigeria Oil and Gas Upstream Market size was estimated at 4.73 million cubic feet. The report covers the Nigeria Oil and Gas Upstream Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Nigeria Oil and Gas Upstream Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Nigeria Oil and Gas Upstream Market Research

Mordor Intelligence provides a comprehensive analysis of the oil and gas upstream sector in Nigeria. We leverage extensive expertise in petroleum upstream research and consulting. Our detailed report covers crucial aspects such as offshore drilling, onshore drilling, and well drilling operations. It also includes advanced well logging and geological survey methodologies. The analysis addresses oil and gas exploration activities, well completion processes, and emerging unconventional resources. We offer detailed insights into subsea systems and deepwater exploration developments. Our research thoroughly examines oil field services, well intervention strategies, and enhanced oil recovery techniques. This information is available in an easy-to-download report PDF format.

Stakeholders gain valuable insights into production optimization strategies, reservoir characterization methods, and well stimulation techniques essential for Nigeria's evolving energy sector. The report provides a detailed analysis of oil and gas equipment deployment, oil and gas software applications, and advanced upstream technology implementations. Our comprehensive coverage includes geophysical services, seismic services, and shale exploration developments, supporting strategic decision-making across the value chain. The analysis particularly focuses on hydrocarbon exploration trends and emerging petroleum exploration opportunities. It offers stakeholders actionable intelligence for informed investment and operational decisions.