Next Generation Memory Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

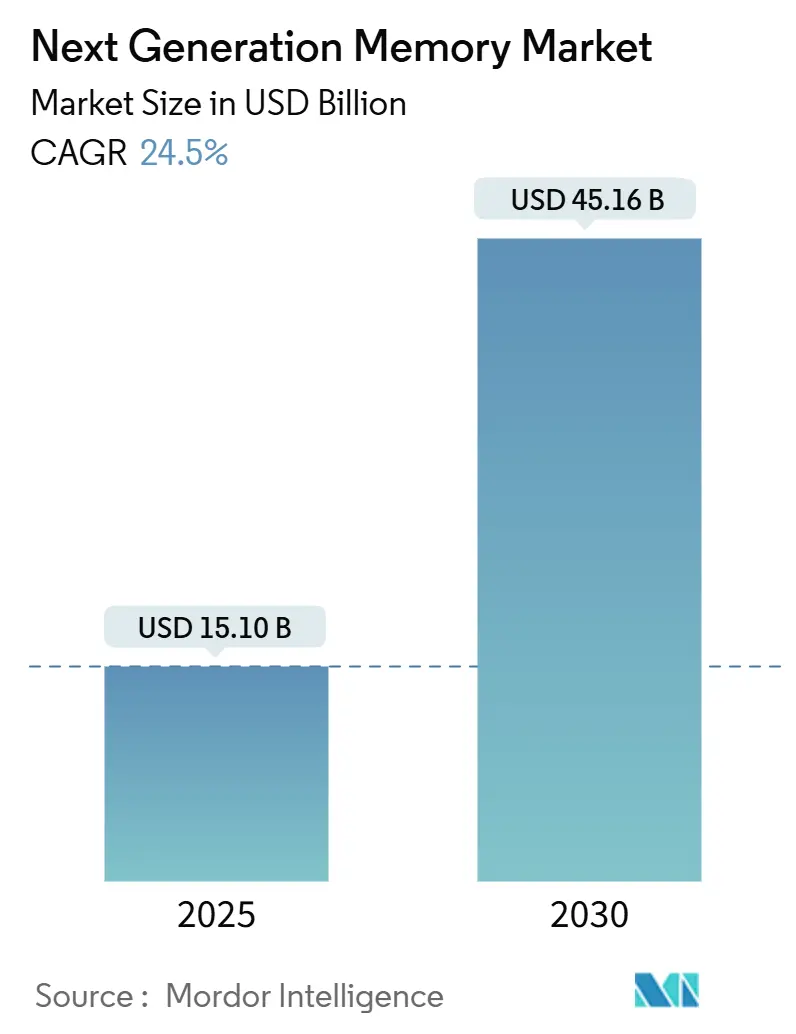

| Market Size (2025) | USD 15.10 Billion |

| Market Size (2030) | USD 45.16 Billion |

| Growth Rate (2025 - 2030) | 24.50% CAGR |

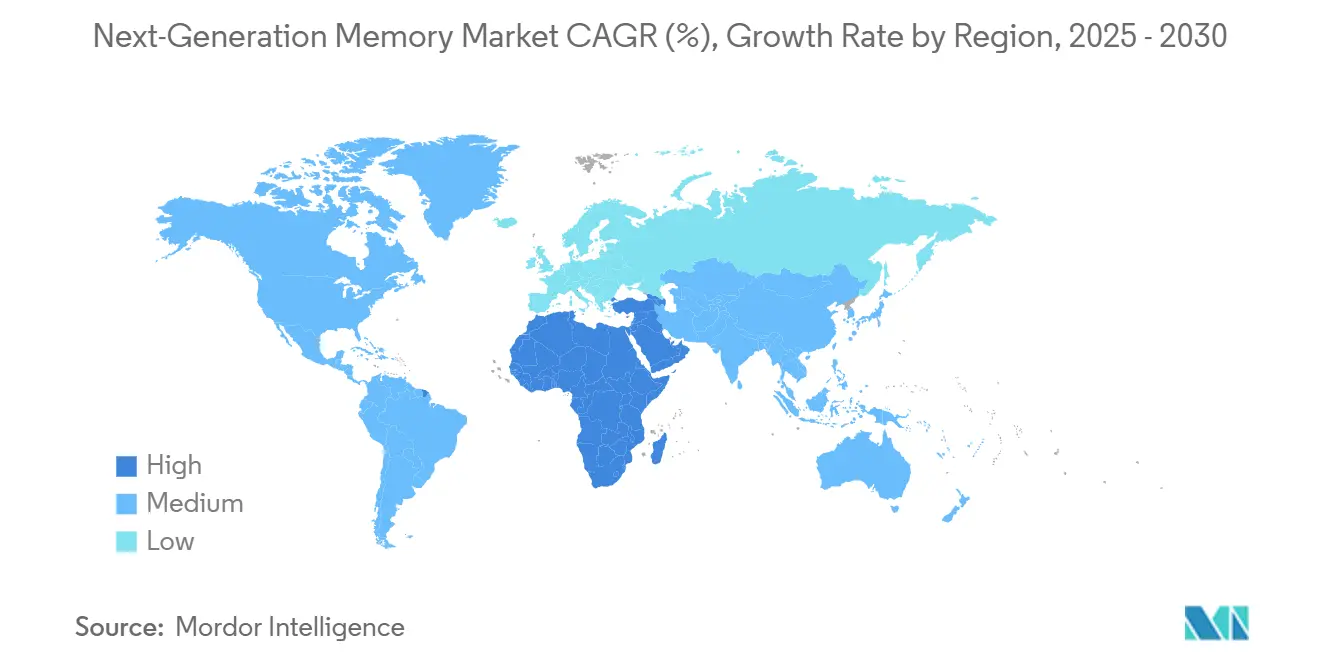

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

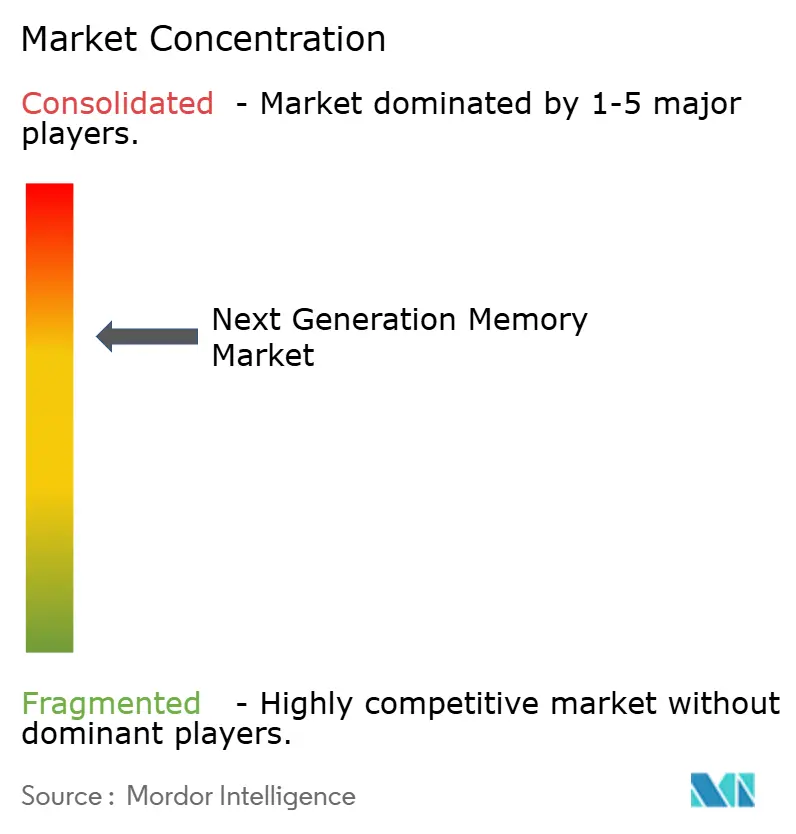

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Next Generation Memory Market Analysis by Mordor Intelligence

The Next Generation Memory market size was valued at USD 15.10 billion in 2025 and is forecast to reach USD 45.16 billion by 2030, reflecting a vigorous 24.5% CAGR. Demand accelerated as AI training clusters, edge servers, and autonomous vehicles all confronted the latency wall of conventional DRAM–NAND hierarchies. Vendors prioritized high-bandwidth architectures, persistent storage class devices, and advanced packaging to close the widening compute-to-memory gap. Asia-Pacific remained the production powerhouse, while North American fab incentives fostered parallel capacity. Interface innovations such as Compute Express Link (CXL) and Universal Chiplet Interconnect Express (UCIe) have begun to redraw system design philosophies, encouraging disaggregated memory pools that scale almost linearly with accelerator count. Supply constraints for premium nodes and wafers, however, continued to shape pricing and allocation strategies across the Next Generation Memory market.

Key Report Takeaways

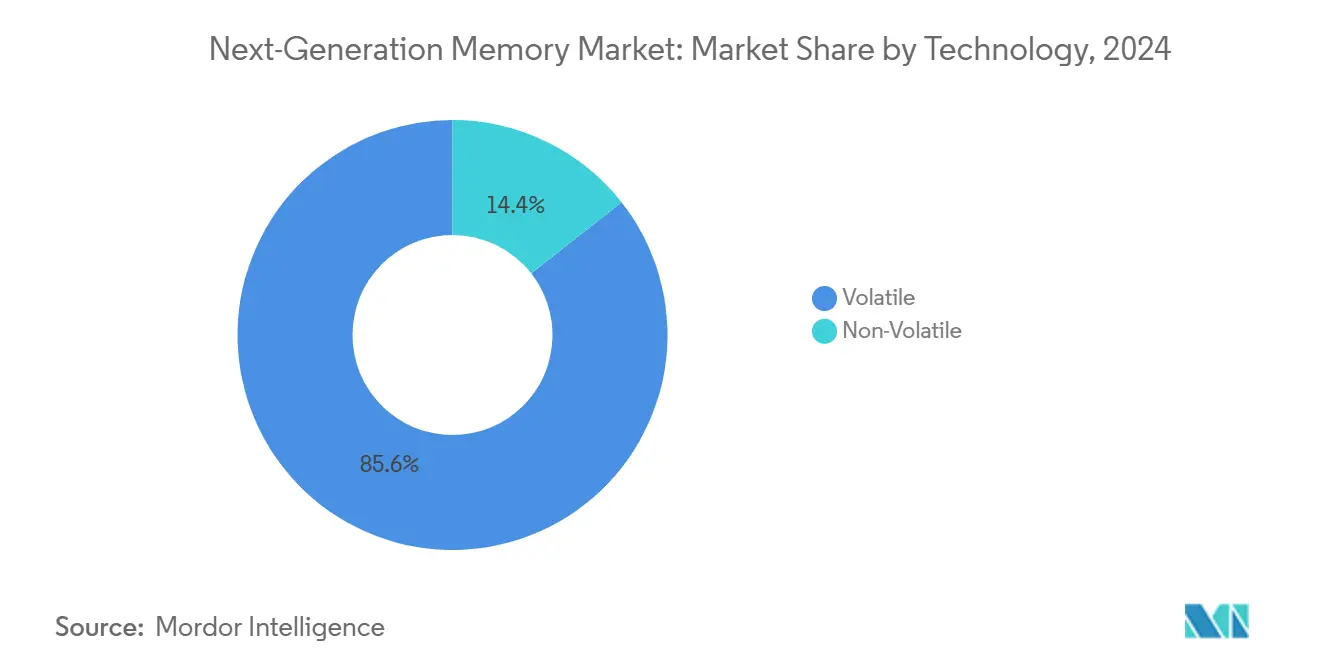

- By technology, volatile devices (HBM, HMC, LPDDR5X) led with 85.6% revenue share in 2024, while ReRAM is projected to expand at a 38.3% CAGR to 2030.

- By memory interface, DDR/LPDDR held 38.3% of the Next Generation Memory market share in 2024; CXL / UCIe is growing at 48.3% CAGR through 2030.

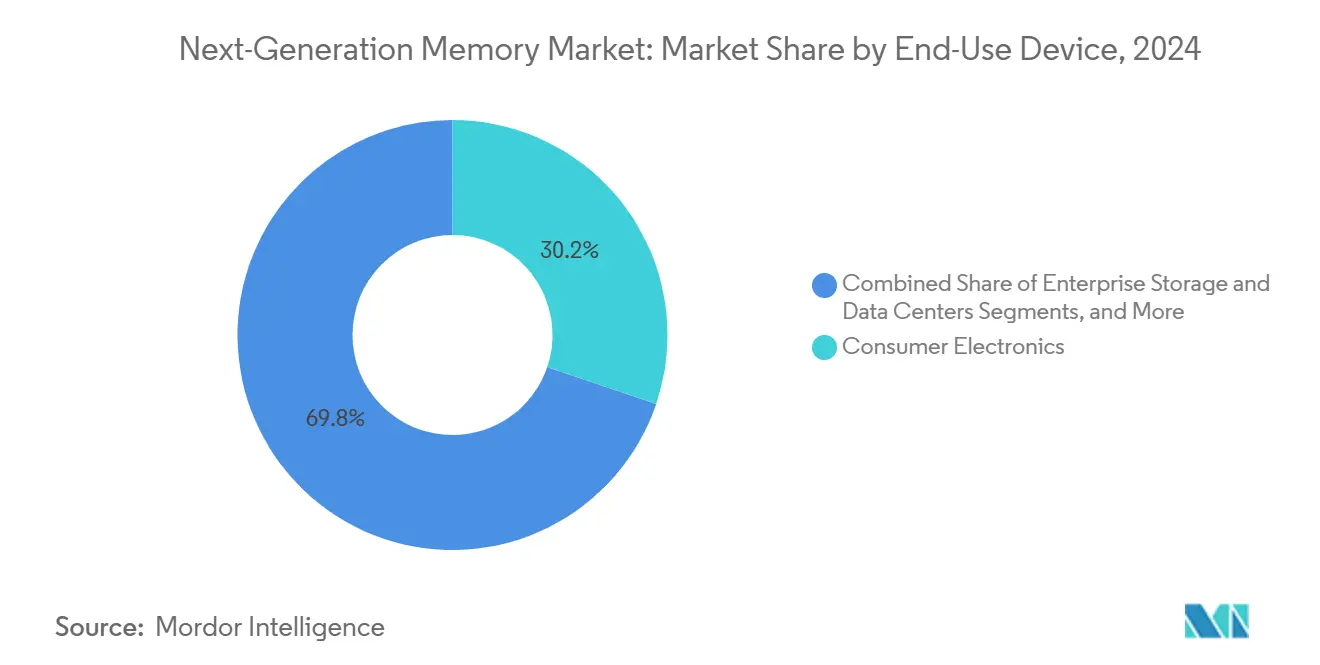

- By end-use device, consumer electronics commanded 30.2% of the Next Generation Memory market size in 2024; automotive electronics is set to rise at 37.3% CAGR to 2030.

- By wafer size, 300 mm occupied 72.5% of production in 2024, while 450 mm wafers are forecast to climb at 42.3% CAGR.

- By geography, Asia-Pacific held 47.3% of revenue in 2024; the Middle East and Africa region is poised for a 31.2% CAGR over 2025-2030.

Global Next Generation Memory Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Demand for HBM in Hyperscale Data Centers | 7.0% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Automotive L4 ADAS Need for Instant-On Persistent Memory | 4.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Smartphone Migration to LPDDR5X and Embedded ReRAM | 3.8% | Global, with strongest impact in Asia-Pacific | Short term (≤ 2 years) |

| National Memory Localization Programs | 2.5% | Middle East and Africa, Europe, Asia-Pacific | Medium term (2-4 years) |

| Industrial Edge-IoT Requiring Ultra-Low-Power FRAM | 1.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Data-Privacy-Driven Persistent In-Memory Databases Using 3D XPoint | 1.2% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

| Source: Mordor Intelligence | |||

AI-driven demand for HBM in hyperscale data centres

Surging transformer model sizes forced cloud operators to double server-level DRAM and solid-state budgets, making bandwidth rather than capacity the primary bottleneck. High Bandwidth Memory multiplied link throughput beyond 1.5 TB/s and delivered dramatic energy savings per bit moved.[1]SK hynix, “SK hynix Sold Out of HBM for 2025,” tweaktown.com Global allocation tightened when SK Hynix reported its entire 2025 HBM output sold in advance, which prompted long-term volume reservations for 2026. Micron observed that an AI server deploys nearly twice the DRAM of a classic x86 node. The Next Generation Memory market, therefore, pivoted from bit-cost leadership toward bandwidth leadership, creating premium pricing tiers and margin expansion opportunities.

Automotive L4 ADAS needs instant-on persistent memory

Level 4 autonomy demands deterministic recovery after power events and harsh operating temperatures beyond 150 °C. Ferroelectric RAM devices withstand 10¹⁴ cycles while retaining data without standby power, ensuring cold-start availability for sensor fusion stacks that generate up to 100 GB/s. Automakers now evaluate asymmetric persistent-volatile hybrids combining FRAM with LPDDR5X scratch pads. These architectures protect mission logs, facilitate over-the-air updates, and support functional safety goals under ISO 26262, reinforcing growth in the Next Generation Memory market across the mobility value chain.

Smartphone migration to LPDDR5X and embedded ReRAM

Flagship handsets released after Q3 2025 shipped exclusively with LPDDR5X capable of 9.6 GT/s, cutting dynamic energy per bit by 30% versus LPDDR5. Simultaneously, global OEMs embedded ReRAM blocks to store AI models and biometric credentials, removing the latency of external Flash accesses. Samsung’s announcement to sunset DDR4 production by June 2025 crystallized the inflection. Integrated LPDDR+ReRAM modules balance performance and standby endurance, expanding total addressable revenue per handset and advancing the Next Generation Memory market.

National memory localization programs

Geopolitical tension and pandemic-era shortages pushed governments to de-risk supply chains. The USD 52.7 billion U.S. CHIPS Act incentivized domestic DRAM and HBM fabs, while Malaysia became Micron’s secondary HBM assembly hub. The Czech Republic mapped a plan to triple its semiconductor sector by 2029 to reinforce technological sovereignty. In parallel, China’s local champions lifted their share from zero to 5% by 2024 and targeted 10% by 2025. Such programs are re-balancing global capacity footprints, fostering regional clusters, and broadening participation in the Next Generation Memory market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 450 mm Wafer Delay Constraining ReRAM Scale-up | -1.7% | Global, with strongest impact in Asia-Pacific | Medium term (2-4 years) |

| High Per-Bit MRAM Cost versus NAND | -1.2% | Global | Short term (≤ 2 years) |

| Thermal Stability Failures of Automotive-Grade PCM | -2.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Foundry Concentration for Sub-28 nm STT-MRAM | -3.8% | Global, with strongest impact in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

| Source: Mordor Intelligence | |||

Thermal stability failures of automotive-grade PCM

Phase-change alloys struggled to retain data above 150 °C, jeopardizing event recorder integrity in desert and under-hood deployments. Material engineering explored Ge-rich GeSbTe and serial PCM cell pairs that push endurance windows to 153 °C but add lithography steps and cost. OEM qualification cycles, therefore, slowed PCM adoption, shifting near-term design wins to FRAM and ReRAM until reliability goals are met. The constraint compressed overall growth, particularly within the automotive subset of the Next Generation Memory market.

Foundry concentration for sub-28 nm STT-MRAM

Spin-transfer MRAM integration at 16 nm requires perpendicular magnetic tunnel junctions, rare etch chemistries, and tight process controls. Only two logic foundries presently support volume STT-MRAM, prompting capacity bidding wars and leaving emerging fab-less suppliers exposed to lead-time shocks. Reliability issues, such as read disturb and process-induced variability, further prolong product cycles. This chokepoint amplifies capital intensity and curbs the scalability momentum otherwise expected in the Next Generation Memory market.

Segment Analysis

By Technology: volatile dominance with non-volatile disruption

Volatile devices delivered 85.6% of 2024 revenue, anchored by HBM’s steep capacity premiums. That dominance has persisted because AI accelerators saturate anything below 1 TB/s, ensuring HBM purchase commitments stretch multiple fiscal years. The Next Generation Memory market size for volatile solutions is projected to keep expanding in absolute terms even while share slips, as ReRAM, PCM, and MRAM gain credibility in edge and instrumentation workloads. ReRAM leads non-volatile momentum, growing at 38.3% CAGR thanks to simple metal-oxide stacks that co-fabricate on 28 nm nodes without extra masks.[2]“Advances of Embedded Resistive Random Access Memory,” IOPscience, iopscience.iop.org PCM’s gradual thermal-stability gains are expected to unlock automotive attach once the 10-year, 150 °C retention benchmark is certified. MRAM advances remain tied to future EUV capacity and to process simplification that narrows the per-bit premium versus NAND.

Structurally, volatile makers now explore stacked chiplet topologies, trimming die area, and spreading yield risk. Non-volatile challengers respond with cross-point arrays and selector-less designs that eliminate area-consuming transistors. Over the outlook period, supply acceleration for ReRAM and PCM is expected to erode volatile share by roughly 10 percentage points, although absolute volatile revenue still rises because the AI server TAM doubles. Designers will continue to co-package volatile and non-volatile dies, cultivating hybrid stacks that trade endurance for persistence. Those dynamics ensure a multi-node roadmap, widening solution diversity within the Next Generation Memory market.

Note: Segment shares of all individual segments available upon report purchase

By Memory Interface: CXL / UCIe re-architectures

Interfaces adapted to bandwidth-hungry accelerators long before monolithic silicon could keep pace. In 2024, DDR and LPDDR channels retained a 38.3% share, but adoption ceilings emerged at four channels per socket. CXL’s cache-coherent attach over PCIe 5.0 eased that limit, pooling terabytes of memory behind shared switches and slashing stranded capacity. The arrival of the UCIe 2.0 spec in August 2024 delivered 3D-stacked chiplets with 75 × the prior inter-die bandwidth, empowering hyperscalers to tile dozens of compute dies against a single HBM stack.

Looking ahead, 50% of new HPC tape-outs in 2025 will embed 2.5D or 3D die-to-die links, elevating CXL or UCIe from optional to mandatory design elements. Retiming hubs and retimers emerge as ancillary profit pools. Synchronous to these shifts, PCIe/NVMe continues incremental generational moves, but SATA fades toward archival niches. Collectively, novel interfaces propel modular deployments that decouple capacity planning from CPU upgrade cycles, enlarging diversification options within the Next Generation Memory market.

By End-Use Device: automotive ADAS acceleration

Consumer electronics retained a 30.2% revenue slice in 2024, with premium smartphones integrating LPDDR5X and system-in-package ReRAM-backed always-on caches. Yet vehicle compute domains are the standout. Assisted driving stacks expand from level 2+ to level 4, requiring persistent logs, sensor checkpoint buffers, and safety microcontrollers that must power-cycle in milliseconds. Consequently, automotive memory revenue is forecast to rise at 37.3% CAGR, outpacing handset upgrades.

Enterprise storage maintained steady procurement for AI training arrays, but edge-industrial installations adopted low-power FRAM to mitigate battery constraints. Medical implants exploited MRAM’s radiation tolerance, and aerospace used rad-hard ReRAM for guidance computers. Each use case added volume diversity, broadening risk profiles, but enhancing the total resilience of the Next Generation Memory market.

Note: Segment shares of all individual segments available upon report purchase

By Wafer Size: scaling toward 450 mm

In 2024, 300 mm substrates generated 72.5% of total wafer starts, anchored by DRAM and 3D NAND fabs optimized for high throughput. 200 mm lines lingered for mature specialty memories, especially industrial FRAM, where tooling is fully depreciated. Migration economics now shift toward 450 mm, promising 2.5 × die output per cycle. Pilot runs posted a 42.3% CAGR outlook even as capex hurdles rose to USD 20 billion per fab. Lithography and metrology vendors race to adapt scanners and defect inspection to the larger field.

However, ReRAM and MRAM adoption on 450 mm remains constrained by delayed tool readiness, echoing one of the key restraints above. Still, first-mover advantage may allow mega-fabs to earn favourable learning curves, squeezing cost structures and ultimately expanding addressable applications across the Next Generation Memory market.

Geography Analysis

Asia-Pacific maintained its leadership with 47.3% revenue in 2024, sustained by Samsung, SK Hynix, and TSMC, whose combined capital plans exceeded USD 85 billion for next-generation nodes. China advanced its indigenous DRAM capacity to a 5% global share and targeted 10% by 2025, guided by state grants and preferential loan terms. Japan’s renewed subsidies preserved local NAND output and specialty equipment clusters. India launched fabrication incentive programs that attracted joint ventures geared toward assembly, test, and eventually 3D NAND slicing. This regional depth anchored supply security and fostered volume leverage for the Next Generation Memory market.

North America’s CHIPS incentive catalysed Micron’s Idaho HBM fab and Texas memory assembly centres, ensuring domestic capacity for defense and hyperscale procurement.[3]Emily G. Blevins et al., “Semiconductors and the CHIPS Act: The Global Context,” Congressional Research Service, congress.gov Mexico captured backend assembly flows, complementing the United States front-end wafer starts. Canadian institutes contributed materials science breakthroughs aimed at ultra-low-power non-volatiles, expanding the research and development halo of the continent.

Europe pursued strategic autonomy under its semiconductor act, targeting a 20% global share by 2030. Germany funnelled grants toward automotive-grade memory consortia, while France invested in ReRAM pilot lines. The United Kingdom prioritized foundry-agnostic IP for chiplet die-to-die fabrics. Collectively, the bloc sought tighter integration between automotive OEMs and local memory houses, reinforcing regional demand in the Next Generation Memory market.

The Middle East and Africa exhibited the fastest trajectory, with a 31.2% CAGR outlook underpinned by sovereign wealth-fund backed fabs in Saudi Arabia and the UAE. Turkey marketed itself as a Eurasian packaging hub, and South Africa leveraged telecom densification to spur consumer memory uptake. While the base is modest, aggressive capital allocations and labour-force upskilling suggest durable upside for the region’s share of the Next Generation Memory market.

Competitive Landscape

The competitive field remained oligopolistic. Samsung, SK Hynix, and Micron jointly controlled around 60% of aggregate revenue, with dominance even higher in HBM tiers. Long-term supply agreements, advanced packaging patents, and pre-priced volume slots entrenched their positions. Yet Chinese new entrants such as CXMT and YMTC applied cost-down strategies, offering 20-30% lower per-gigabyte pricing for mainstream DRAM, thereby edging into laptop and IoT contracts. Their combined share is forecast to double by 2025, gradually diluting incumbents’ margin leadership.

In the non-volatile specialty corner, Everspin and Weebit Nano differentiated through design-centric approaches rather than wafer-scale. Weebit Nano secured fresh patents covering selector-less cell arrays, addressing endurance drift below 40 nm. Everspin shipped STT-MRAM modules for industrial robotics needing deterministic write latency. Such niche positioning allowed agility despite restricted foundry access, fostering innovation layers that enrich the Next Generation Memory market.

All players increasingly explored collaboration. Marvell partnered with the top three DRAM houses to co-define SOCAMM, a module spec bundling DRAM and logic dies for AI notebooks. Synopsys taped out UCIe PHY IP on TSMC N3E, offering turnkey tool flows to fab-less firms.[4]Farhana Goriawalla and Yervant Zorian, “Multi-Die Health and Reliability Advances,” Synopsys, synopsys.com These alliances suggest an ecosystem where interface, packaging, and software co-optimization yield new leverage beyond wafer volume alone.

Next Generation Memory Industry Leaders

-

Samsung Electronics Co., Ltd.

-

SK Hynix Inc.

-

Micron Technology, Inc.

-

Kioxia Holdings Corporation

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung disclosed a 400-layer 3D NAND milestone delivering 5.6 Gb/s per pin, aimed at flagship smartphones and edge server blocks and files.

- April 2025: Weebit Nano obtained three additional patents for ReRAM cell and selector technology, strengthening its specialty portfolio.

- April 2025: SK Hynix debuted the 12-layer, 48 GB HBM4 device, shipping end-2025 for AI accelerators.

- March 2025: Micron sampled 1γ DDR5 with reduced EUV steps, lowering future cost exposure while sustaining speed leadership.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the next-generation memory market as the global demand and supply for high-bandwidth volatile devices (HBM, HMC, LPDDR5X) and emerging non-volatile formats such as PCM, STT-MRAM, ReRAM, 3D XPoint, FeRAM, and NanoRAM that are designed to accelerate AI, edge, automotive, and data-centric workloads. The unit of analysis is new, factory-calibrated chips and modules shipped to OEMs, foundries, and service providers, valued at prevailing average selling prices.

Scope exclusion: Conventional DDR3/DDR4 DRAM and commodity planar NAND flash are not counted because they follow distinct cost curves and maturity paths.

Segmentation Overview

- By Technology

- Non-Volatile

- Phase-Change Memory (PCM)

- Spin-Transfer MRAM (STT-MRAM)

- Toggle MRAM

- Resistive RAM (ReRAM)

- 3D XPoint / Optane

- Ferroelectric RAM (FeRAM)

- NanoRAM

- Volatile

- High-Bandwidth Memory (HBM)

- Hybrid Memory Cube (HMC)

- Low-Power DDR5 / LPDDR5X

- Non-Volatile

- By Memory Interface

- DDR / LPDDR

- PCIe / NVMe

- SATA

- Others (CXL, UCIe)

- By End-Use Device

- Consumer Electronics

- Enterprise Storage and Data Centers

- Automotive Electronics and ADAS

- Industrial IoT and Manufacturing Automation

- Aerospace and Defense

- Healthcare and Medical Devices

- Others (Smart Cards, Wearables)

- By Wafer Size

- ≤ 200 mm

- 300 mm

- 450 mm

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Conversations and structured questionnaires with fabs, EDA tool vendors, memory-controller architects, hyperscale procurement managers, and Tier-1 auto electronics integrators enabled us to validate adoption timelines, price erosion curves, and yield learning rates across North America, Europe, and Asia-Pacific. Feedback from these experts filled gaps that desk research alone could not cover and sharpened our scenario assumptions.

Desk Research

We began by assembling trade statistics from bodies such as WSTS, customs manifests available through Volza, and wafer shipment tallies released by SEMI. Analysts next screened technical papers on PCM and MRAM in IEEE Xplore, patent filings accessed through Questel, and quarterly fab-capacity disclosures in company 10-Ks. Market signals from Asia Metal for specialty sputtering targets, Bestsellingcarsblog for EV adoption, and Dow Jones Factiva news flows helped gauge downstream pull. Financial data inside D&B Hoovers enriched price-volume estimates.

These publicly available records established the historical baseline while allowing us to cross-reference fab ramp-ups, design wins, and interface transitions. The sources listed illustrate our approach; many additional databases and journals were tapped during verification and context building.

Market-Sizing & Forecasting

A top-down reconstruction using production volumes, die sizes, and trade data set the initial 2024 pool, which is then stress-tested through selective bottom-up roll-ups of sampled ASP × unit shipments reported by key suppliers. Variables such as AI server deployments, wafer-size migration shares, automotive Level-3 + ADAS penetration, ReRAM licensing deals, and HBM price progression feed a multivariate regression that projects demand. Where supplier splits were opaque, we bridged gaps with channel-check ranges and adjusted the model toward the convergent midpoint.

Data Validation & Update Cycle

Outputs pass two rounds of anomaly checks, peer review, and senior-analyst sign-off. We revisit models at least once a year and trigger interim refreshes when large wafer expansions, major design wins, or disruptive price moves occur, ensuring clients always receive the latest calibrated view.

Why Our Next Generation Memory Baseline Commands Reliability

Published numbers often vary because firms pick different technology baskets, currency bases, and refresh cadences. Mordor analysts disclose inclusions up front and keep every assumption traceable.

Key gap drivers emerge when other studies fold legacy NAND into totals, apply aggressive HBM price compression without cross-checking fab guidance, or extrapolate single-region surveys to global volumes. Our work anchors to verified multi-source inputs, annual refreshes, and balanced scenario weighting, producing a figure decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.10 B (2025) | Mordor Intelligence | - |

| USD 11.11 B (2025) | Global Consultancy A | Counts only non-volatile chips and leans on vendor shipment press releases with limited primary validation |

| USD 14.87 B (2025) | Trade Journal B | Uses broader tech list plus optimistic 450 mm ramp and unverified HBM ASP declines |

These comparisons show that while figures sit in the same ballpark, Mordor's disciplined scope choices, cross-checked variables, and timely updates provide a balanced, transparent baseline that is reproducible with public data and focused expert insight.

Key Questions Answered in the Report

What is the current size of the Next Generation Memory market?

The Next Generation Memory market size reached USD 15.10 billion in 2025 and is projected to hit USD 45.16 billion by 2030.

Which region leads global production?

Asia-Pacific accounted for 47.3% of revenue in 2024, driven by Samsung, SK Hynix, and TSMC capacity expansions.

Why is HBM critical for AI workloads?

Large language models saturate traditional DRAM bandwidth; HBM delivers multi-terabyte-per-second throughput, removing the training bottleneck.

How fast is automotive memory demand growing?

Automotive electronics revenues are forecast to rise at a 37.3% CAGR as Level 4 ADAS systems need instant-on and high-endurance memory.

What role will CXL and UCIe play in future systems?

Both interfaces enable disaggregated, chiplet-based architectures that pool large memory blocks, improving utilization and scalability.

Page last updated on: