Market Size of Next-generation Computing Industry

| Study Period | 2019 - 2029 |

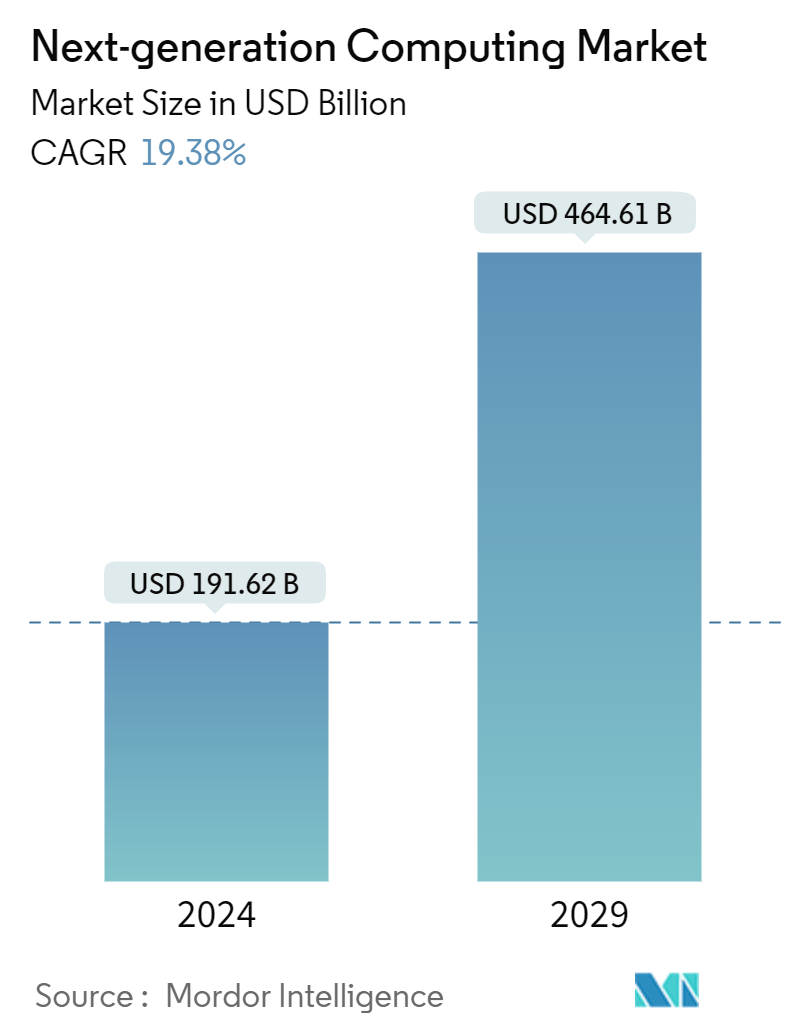

| Market Size (2024) | USD 191.62 Billion |

| Market Size (2029) | USD 464.61 Billion |

| CAGR (2024 - 2029) | 19.38 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Next-generation Computing Market Analysis

The Next-generation Computing Market size is estimated at USD 191.62 billion in 2024, and is expected to reach USD 464.61 billion by 2029, growing at a CAGR of 19.38% during the forecast period (2024-2029).

Implementing Next-generation computing solutions gives end users a shorter lead time in product development, flexibility, process efficiencies, enhanced productivity, higher quality, more intuitive customer experiences, and improved profitability, fueling market adoption worldwide.

- Next-generation computing market is evolving from the emergence of new technologies such as Distributed computing, Machine learning, Artificial intelligence, and Cloud computing for efficient computing by using centralizing storage, memory, processing, and bandwidth, driving the market in various end-user applications.

- The demand for High-performance computing is increasing and becoming crucial for organizations as it enables them to compute and analyze large volumes of data quickly and efficiently, which is significantly essential in scientific research, engineering, and finance, where the ability to process large amounts of data to give insights for better operational efficiencies and customer services. The need for next-gen computing solutions for High-performance computing applications drives the market.

- Additionally, with better supply chain management, increased productivity, and streamlined operations, SMEs have benefited from digital transformation. SMEs have been automating their processes and reducing costs using cloud computing, AI, and blockchain, which would drive the market during the forecast period. For instance, in December 2022, UST, a digital transformation solutions provider, announced a collaboration with Intel and SAP to enable the Industry 4.0 digital transformation journey for small and medium-sized enterprises in northern Malaysia, creating an opportunity for the market vendors due to their next-gen computing solutions for Industry 4.0.

- However, the next-gen solutions and computing technology involve processing & data shared between local devices, mobile devices, cloud-based servers, etc., which generates a threat of data privacy risk in the end users while implementing the solutions for their business processes, which could restrict the market adoption in many end-users, such as defense, BFSIs, etc. during the forecast period.

Next-generation Computing Industry Segmentation

Global Next-generation Computing Market can be defined as computing solutions offered by the market vendors using advanced processors and AI & ML enabled software for managing, storing, and processing data automatically for high-power computational needs in the end-users, which are replacing older CPUs with newer chip architectures, such as GPUs and field-programmable gate arrays (FPGAs).

Global Next-generation Computing Market is components (hardware, software, and services), computing type (high-performance computing, quantum computing, cloud computing, edge computing), deployment type (cloud, on-premise), end-user (automotive & transportation, energy & utilities, healthcare, BFSI, aerospace & defense, media & entertainment, IT & telecom, retail, manufacturing), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Component | |

| Hardware | |

| Software | |

| Services |

| By Computing Type | |

| High-Performance Computing | |

| Quantum Computing | |

| Optical Computing | |

| Edge Computing | |

| Other Computing Types |

| By Deployement | |

| Cloud | |

| On-Premise |

| By End-user | |

| Automotive & Transportation | |

| Energy & Utilities | |

| Healthcare | |

| BFSI | |

| Aerospace & Defense | |

| Media & Entertainment | |

| IT & Telecom | |

| Retail | |

| Manufacturing | |

| Other End Users |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Next-generation Computing Market Size Summary

The Next-generation Computing Market is poised for significant growth, driven by the adoption of advanced technologies such as distributed computing, machine learning, artificial intelligence, and cloud computing. These technologies enhance efficiency by centralizing storage, memory, processing, and bandwidth, making them essential for various end-user applications. The increasing demand for high-performance computing is a key factor propelling the market, as it allows organizations to process large volumes of data swiftly, which is crucial in sectors like scientific research, engineering, and finance. Additionally, small and medium-sized enterprises (SMEs) are leveraging digital transformation through cloud computing, AI, and blockchain to streamline operations and reduce costs, further fueling market expansion. However, concerns over data privacy risks associated with these solutions may hinder adoption in certain sectors, such as defense and BFSI, during the forecast period.

The market is also witnessing a surge in the adoption of cloud-based computing solutions, offering benefits like cost savings, security, flexibility, and increased collaboration. This trend is supported by government investments in ICT infrastructure across developed and developing economies. Major market players, including Microsoft, Amazon, IBM, and Google, are investing in quantum computing and offering SaaS models to make these technologies accessible to mainstream enterprises. The Asia-Pacific region, with its emerging economies, is a significant growth area due to the increasing digitalization in sectors like healthcare, automotive, and finance. The establishment of large data centers in countries like Singapore, Malaysia, and Indonesia further supports the adoption of next-generation computing solutions. The market remains highly fragmented, with global companies focusing on product innovations, collaborations, and R&D investments to enhance their market presence.

Next-generation Computing Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Assessment of the Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Component

-

2.1.1 Hardware

-

2.1.2 Software

-

2.1.3 Services

-

-

2.2 By Computing Type

-

2.2.1 High-Performance Computing

-

2.2.2 Quantum Computing

-

2.2.3 Optical Computing

-

2.2.4 Edge Computing

-

2.2.5 Other Computing Types

-

-

2.3 By Deployement

-

2.3.1 Cloud

-

2.3.2 On-Premise

-

-

2.4 By End-user

-

2.4.1 Automotive & Transportation

-

2.4.2 Energy & Utilities

-

2.4.3 Healthcare

-

2.4.4 BFSI

-

2.4.5 Aerospace & Defense

-

2.4.6 Media & Entertainment

-

2.4.7 IT & Telecom

-

2.4.8 Retail

-

2.4.9 Manufacturing

-

2.4.10 Other End Users

-

-

2.5 By Geography***

-

2.5.1 North America

-

2.5.2 Europe

-

2.5.3 Asia

-

2.5.4 Australia and New Zealand

-

2.5.5 Latin America

-

2.5.6 Middle East and Africa

-

-

Next-generation Computing Market Size FAQs

How big is the Next-generation Computing Market?

The Next-generation Computing Market size is expected to reach USD 191.62 billion in 2024 and grow at a CAGR of 19.38% to reach USD 464.61 billion by 2029.

What is the current Next-generation Computing Market size?

In 2024, the Next-generation Computing Market size is expected to reach USD 191.62 billion.