Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.93 Billion |

| Market Size (2026) | USD 9.33 Billion |

| Market Size (2031) | USD 11.59 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Home Furniture Market Analysis by Mordor Intelligence

The Netherlands home furniture market size was valued at USD 8.93 billion in 2025 and estimated to grow from USD 9.33 billion in 2026 to reach USD 11.59 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). Current growth reflects resilient residential renovation activity, expanding mortgage approvals, and increasing consumer preference for premium, sustainably produced furnishings. Strong wage gains amid a tight labor market are lifting discretionary spending, while digital transformation is unlocking broader access to online channels and data-driven shopping journeys. At the same time, regulatory pressures such as the EU’s formaldehyde cap are prompting accelerated innovation in materials and production processes. Supply-side challenges, chiefly volatile timber prices and skilled-labor shortages, moderate margins yet simultaneously incentivize automation and circular models across the Netherlands home furniture market. Digital transformation demands substantial technology investments while traditional retailers struggle to compete with pure-play online platforms that offer superior customer experiences and operational efficiencies.

Key Report Takeaways

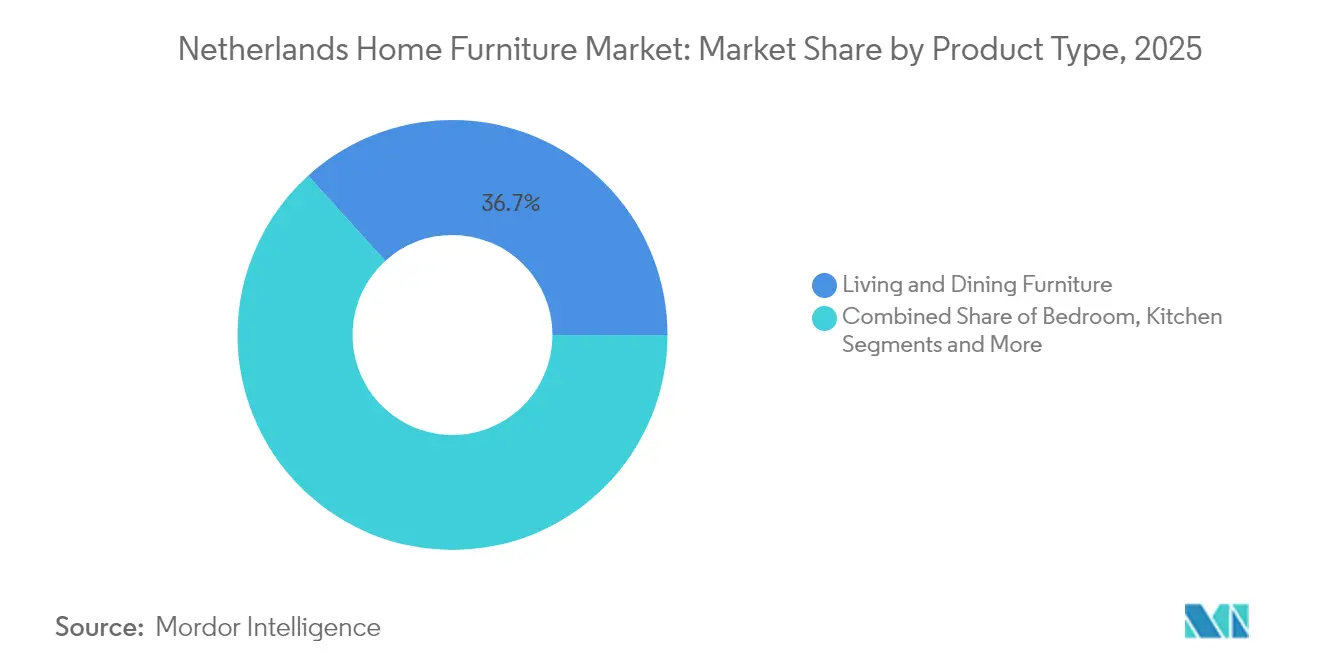

- By product type, Living and Dining Furniture led with 36.72% revenue share in 2025, whereas Bedroom Furniture is projected to expand at a 6.35% CAGR through 2031.

- By material, wood accounted for a 56.88% share of the Netherlands home furniture market size in 2025, and the Plastic and Polymer segment is poised to grow at a 7.02% CAGR to 2031.

- By price range, mid-range products captured 45.62% Netherlands home furniture market share in 2025, while premium offerings are forecast to rise at a 6.95% CAGR over the same horizon.

- By distribution channel, specialty stores dominated with 40.95% market share in 2025, whereas online channels are expected to climb at an 8.05% CAGR through 2031.

- Randstad held 51.63% of the Netherlands home furniture market in 2025; Southern Netherlands will register the fastest regional CAGR at 10.78% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust residential renovation demand | +1.2% | National; strongest in Randstad & key urban centers | Medium term (2-4 years) |

| Growing work-from-home culture | +0.8% | Nationwide; higher impact in knowledge hubs | Short term (≤ 2 years) |

| Rising mortgage approvals & new-builds | +1.0% | National; concentrated in Southern Netherlands growth corridors | Medium term (2-4 years) |

| Circular-design mandates | +0.6% | EU-wide; early Dutch adoption | Long term (≥ 4 years) |

| Digital-first direct-to-consumer brands | +0.9% | Urban centers; expanding in rural markets | Short term (≤ 2 years) |

| Advanced Dutch smart-factory mass customization | +0.5% | Regional; manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Residential Renovation Demand

House price growth of 10.9% in Q1 2025 and a 6% rise in housing transactions are fueling a vibrant replacement cycle in the Netherlands home furniture market[1]Source: Centraal Bureau voor de Statistiek, “House Prices and Transactions Q1 2025,” cbs.nl. Each new completion triggers additional relocation chains that intensify purchase frequency across multiple households. Elevated wealth effects, average transaction prices hit EUR 472,054 in April 2025, encourage home-owners to upgrade furnishings commensurate with property values. Renovations increasingly incorporate sustainable energy retrofits, stimulating demand for eco-labeled furniture that matches efficiency goals. Consumers living in smaller city apartments favor multifunctional designs that maximize limited space without sacrificing style, broadening opportunities for modular, fold-away solutions tailored to Dutch urban living.

Growing Work-From-Home Culture Spurring Ergonomic Furniture Uptake

Around 45% of Dutch employees now work from home, averaging 11 hours weekly. Hybrid work patterns elevate home-office requirements beyond desks and chairs to encompass task-lighting, acoustic panels, and flexible storage. Health-oriented consumers invest in adjustable desks and certified ergonomic seating, accepting price premiums when products demonstrably improve well-being and productivity. Corporate stipends and leasing schemes create a fresh B2B channel inside the Netherlands home furniture market, where volume contracts favor brands offering rapid delivery and assembly. Tech-embedded furniture such as wireless-charging desks is transitioning from novelty to mainstream, signaling convergence between office equipment and consumer electronics categories. Retailers capturing this niche leverage digital configurators that let buyers customize finishes, leg profiles, and accessory kits, thereby shrinking return rates and deepening loyalty.

Rising Mortgage Approvals and New-Build Completions

Nearly 6,200 newly built homes changed hands in Q1 2025, up 28% year-on-year. First-time buyers dominate this segment, valuing affordability and turnkey furnishing packages that simplify move-in timelines. Developers increasingly partner with furniture retailers to bundle entire room settings, lifting average order values in the Netherlands home furniture market. Energy-positive buildings push demand for sustainably sourced wood and low-VOC finishes, aligning with EU green-building certifications. Banks such as ABN AMRO expanded mortgage portfolios by EUR 1.8 billion, signaling liquidity that underpins big-ticket purchases far beyond closing costs[2]Source: ABN AMRO, “Housing Market Monitor 2025,” abnamro.com. Concentrated growth corridors in Southern Netherlands provide geographic focus for logistics hubs and localized marketing.

Circular-Design Mandates Under EU Green Deal

The National Program for Circular Economy requires all furniture sold after 2030 to comply with high circularity benchmarks[3]Source: Ministerie van Infrastructuur en Waterstaat, “Circular Economy Program 2023-2030,” gov.nl. Dutch manufacturers pioneer modular construction that facilitates repair, refurbishment, and eventual disassembly. Retail take-back schemes, exemplified by IKEA’s buy-back program, gain traction and unlock secondary revenue streams while satisfying extended producer-responsibility rules. Consumers increasingly equate sustainability with durability; a survey shows 78% willing to pay premium prices for certified green products. Investment in recycled plastics and FSC-certified wood reduces regulatory risk and enhances market access across EU borders. Early adopters secure marketing advantages and hedge against future compliance costs, reinforcing their brand equity within the Netherlands home furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile timber prices linked to global supply constraints | -0.7% | Global; intensified in Dutch import-reliant market | Short term (≤ 2 years) |

| Shrinking average dwelling size | -0.4% | Urban centers; high-density housing | Long term (≥ 4 years) |

| Tightening EU formaldehyde & VOC rules | -0.3% | EU-wide; Dutch factories under early scrutiny | Medium term (2-4 years) |

| Skilled-labor shortages in cabinetry & upholstery | -0.6% | Nationwide; severe in traditional clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Timber Prices Linked to Global Supply Constraints

Softwood and plywood costs fluctuate as climate events, sanctions, and bio-energy demand disrupt supply pipelines. Dutch firms, heavily dependent on imports, find it difficult to lock long-term contracts, leading to narrower margins in the Netherlands home furniture market. Some producers shift toward engineered laminates incorporating recycled fibers to stabilize input expenses and satisfy circular goals. Yet substituting high-grade hardwoods proves complex for premium segments that rely on natural aesthetics and tactile appeal. SMEs feel the brunt, lacking scale to hedge or stockpile, prompting consolidation or collaborative purchasing pools. The impact extends beyond direct material costs to include transportation, storage, and inventory management expenses that fluctuate with price volatility and supply uncertainty. Smaller furniture manufacturers face disproportionate challenges due to limited negotiating power and working capital constraints that prevent them from securing favorable supply contracts or maintaining strategic inventory buffers.

Skilled-Labor Shortages in Local Cabinetry and Upholstery Workshops

With 114 vacancies per 100 unemployed workers, artisanal talent is scarce. Demographic decline deepens gaps as retirements outpace apprenticeships, threatening capacity for bespoke joinery favored in high-end trade. Wage inflation raises end-product prices, risking substitution by imports from low-cost countries. Automation helps, but cannot fully replicate hand-finished detailing prized by luxury consumers. National training grants aim to re-skill workers, but results will materialize only mid-term, keeping labor a constraining factor for the Netherlands home furniture market until at least 2027. The skills gap is creating opportunities for companies that invest in training programs and apprenticeships, potentially creating competitive advantages through workforce development initiatives that ensure long-term production capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Living Spaces Drive Market Leadership

Living and Dining Furniture commanded 36.72% of the Netherlands home furniture market in 2025, reflecting the cultural emphasis on communal spaces where families and guests congregate. Rising disposable income fuels upgrades in tables, cabinets, and sectional seating crafted from sustainably certified oak. Multifunctional sofa-beds meet demand for flexible hosting in compact city apartments. Bedroom Furniture logs the fastest CAGR of 6.35%, powered by consumer focus on wellness and sleep ergonomics. Adjustable bases, hybrid mattresses, and smart headboards featuring USB ports typify innovations that justify higher ticket values. Home-office furniture surged parallel to remote work, with brands bundling chairs and sit-stand desks in ergonomic starter kits. Overall, the Netherlands home furniture market size for the Living and Dining segments will keep expanding as renovation cycles stay strong and entertaining regains pre-pandemic prominence.

Consumer priorities are shifting from pure aesthetics to functionality, durability, and environmental footprint. Product personalization, choice of leg colors, fabric textures, and modular add-ons align with Dutch minimalism while catering to individual taste. Companies differentiate through service: in-room deliveries, old-furniture haul-away, and augmented-reality design support reduce friction and deepen loyalty. Local artisanship remains a prestige marker in high-end cabinetry and dining sets, even as imported flat-pack solutions court value-oriented buyers. Premium Living and Dining brands increasingly market circular buy-back guarantees, reinforcing sustainability claims and easing purchase hesitation in the Netherlands home furniture market. Smaller furniture manufacturers face disproportionate challenges due to limited negotiating power and working capital constraints that prevent them from securing favorable supply contracts or maintaining strategic inventory buffers.

By Material: Wood Dominance Faces Sustainable Innovation

Wood retained a 56.88% share in 2025, anchoring its dominance through cultural preference and perceived quality. Yet formaldehyde curbs and price swings propel interest in recycled plastics and engineered composites. Plastic and Polymer products will grow 7.02% annually, bolstered by bio-based resins and closed-loop manufacturing that align with EU circularity rules. Metal frames gain popularity in loft-style interiors and contract segments, prized for strength and slim profiles, maximizing floor area. Meanwhile, hybrid materials, such as wood-plastic composites, balance a natural look with improved moisture resistance, widening options in the Netherlands home furniture market.

Producers fast-track low-VOC lacquers and water-based adhesives to meet the 0.062 mg/m³ formaldehyde limit effective August 2026. FSC and PEFC certifications transform from niche badges to baseline entry tickets for retail listings. Material lifecycle transparency via QR codes boosts customer trust and meets EUDR documentation demands. Research into mycelium-based panels and algae-derived foams hints at radical diversification ahead, with early pilots already incorporated in accent tables and lamps. Such advances reinforce the Netherlands home furniture market reputation for design ingenuity married to ecological stewardship. The skills gap is creating opportunities for companies that invest in training programs and apprenticeships, potentially creating competitive advantages through workforce development initiatives that ensure long-term production capabilities.

By Price Range: Premium Growth Reflects Quality Consciousness

Mid-range SKUs constituted 45.62% Netherlands home furniture market share in 2025, serving households balancing quality aspirations with budget discipline. Premium lines, however, are forecast at a 6.95% CAGR through 2031, buoyed by rising salaries and wealth effects from booming real-estate valuations. Consumers adopt a “buy better, keep longer” mindset, favoring timeless designs built from durable, low-impact materials with extendable warranty coverage. Pay-over-time services extend purchasing power without steep interest costs, widening premium category entry. Economy offerings face input-cost inflation undermining their traditional price gap, hastening a flight to value rather than just low cost within the Netherlands home furniture market.

Distinct consumer segments emerge, minimalist professionals splurge on statement pieces that elevate open-plan apartments, while family households prioritize modular, expandable systems that adapt over life stages. Premium digital-native brands lure shoppers via transparent supply chains and direct pricing, compressing the once-clear boundary between designer showrooms and mainstream retail. Across the spectrum, resale value enters decision criteria as circular programs promise trade-in credits, underscoring total cost-of-ownership over sticker price.

By Distribution Channel: Digital Transformation Accelerates

Specialty stores retained 40.95% market share in 2025 due to curated assortments and tactile experiences valued during high-involvement purchases. Nevertheless, online channels will grow 8.05% annually as frictionless checkout, free returns, and enriched visualization tools melt historical barriers. Omnichannel hybrids deploy showrooms primarily as inspiration hubs and last-mile pickup points for digital orders. Home centers thrive on project bundles, kitchen cabinets, lighting, and tiles offered alongside financing through bank partners, simplifying renovations. Hypermarkets maintain relevance for quick-turnover décor but lag in furniture depth, nudging them toward leasing shelf space to specialty concessions.

Logistics prowess becomes a decisive battleground: next-day delivery of flat-packed items, in-home assembly, and carbon-neutral shipping elevate brand perception. iDEAL and Buy-Now-Pay-Later solutions smooth checkout, while AI chatbots guide sizing and fabric selections, cutting abandonment rates. Live-stream shopping events with designers and influencers inject entertainment value, closing gaps between inspiration and purchase. Players that fuse data analytics with human expertise set the benchmark for customer centricity in the evolving Netherlands home furniture market.

Geography Analysis

Randstad dominates the Netherlands furniture market with 51.63% share in 2025, reflecting its concentration of population, economic activity, and high-value housing stock that drives premium furniture demand. The region's dense urban environment creates unique market dynamics, with consumers prioritizing space-efficient, multifunctional furniture designs that maximize utility within constrained living spaces while maintaining aesthetic appeal. Apartments average under 75 m², prompting above-average spending on space-saving pieces such as nesting tables and vertical storage. Digital maturity ranks high, resulting in e-commerce penetration above the national means and click-and-collect pickup accounting for a growing share of urban deliveries.

Sustainability awareness peaks here; retailers’ spotlight FSC labels and circular take-back programs prominently in Randstad showrooms. Southern Netherlands is forecast to outpace all regions with an 10.78% CAGR through 2031, propelled by substantial housing starts around Eindhoven-Tilburg growth corridors. Job creation in high-tech manufacturing attracts young professionals who favor contemporary Scandinavian aesthetics and integrated home-office solutions. Warehouse expansion along the Dutch Belgian border reduces shipping times to German and French customers, transforming the region into a cross-border fulfillment hub integral to the Netherlands home furniture market.

Eastern Netherlands rides steady growth anchored in woodworking heritage and proximity to German export markets. Local SMEs specialize in bespoke cabinetry serving premium rural homes and hospitality projects. However, talent shortages in joinery sectors risk capping capacity unless automation and apprenticeships scale rapidly. Northern Netherlands remains a niche yet rising market as infrastructure upgrades and university expansions lure residents to lower housing costs. Retailers testing micro-fulfillment centers here aim to shorten delivery lead-times and capture first-mover loyalty. Regional economic development policies and EU funding programs are supporting furniture industry modernization and sustainability initiatives, particularly in traditional manufacturing areas seeking to maintain competitiveness through innovation and automation investments.

Regulatory Landscape

Home furniture sold in the Netherlands falls under the Dutch Commodities Act (Warenwet) framework for consumer product safety, with the Netherlands Food and Consumer Product Safety Authority (NVWA) overseeing compliance and enforcement. Conformity is commonly demonstrated through European EN standards and Netherlands-specific NEN standards coordinated by the Royal Netherlands Standardisation Institute (NEN), which shape requirements for structural safety, finishes, and labeling practices across retail and e-commerce assortments.

On the sustainability and trade side, EU-level rules increasingly influence sourcing and documentation. The EU Deforestation Regulation (EUDR) introduces due diligence statements for relevant commodity-based products, with obligations taking effect for large businesses from 30 December 2026, increasing traceability expectations for wood-based furniture and components. Furniture imports from non-EU countries follow the EU Common Customs Tariff, and the Netherlands is also implementing EU Regulation 2023/988 on general product safety through national measures that took effect in March 2026, tightening accountability across supply chains and marketplace sellers.

Value Chain Analysis

The Netherlands home furniture value chain is shaped by import-heavy sourcing and a strong distribution role, supported by the country’s logistics network and re-export flows through gateways such as the Port of Rotterdam. Upstream inputs include timber, panels, textiles, foams, metals, and polymers, with sourcing risk concentrated in imported materials and components. Domestic manufacturing and assembly remain relevant for specific niches such as custom cabinetry, upholstery, and design-led collections, while a large share of finished goods enters via international suppliers and is routed through national distribution centers to specialty stores, home centers, and online fulfillment networks.

Midstream, wholesalers, private-label owners, and retailers influence product selection, compliance testing, and packaging optimization, then manage warehousing, last-mile delivery, and assembly and returns services. Industry coordination and standard setting are also visible through sector bodies such as Koninklijke CBM (representing around 600 companies) and multi-stakeholder initiatives such as the Circulaire Meubel Standaard project with CBM and INretail, which targets standardized product and material data to support circularity claims and reduce greenwashing risk. Downstream, customer experience (configuration tools, delivery slots, installation, and take-back) and reverse logistics are becoming more central as circular programs expand and compliance requirements increase the need for product-level documentation.

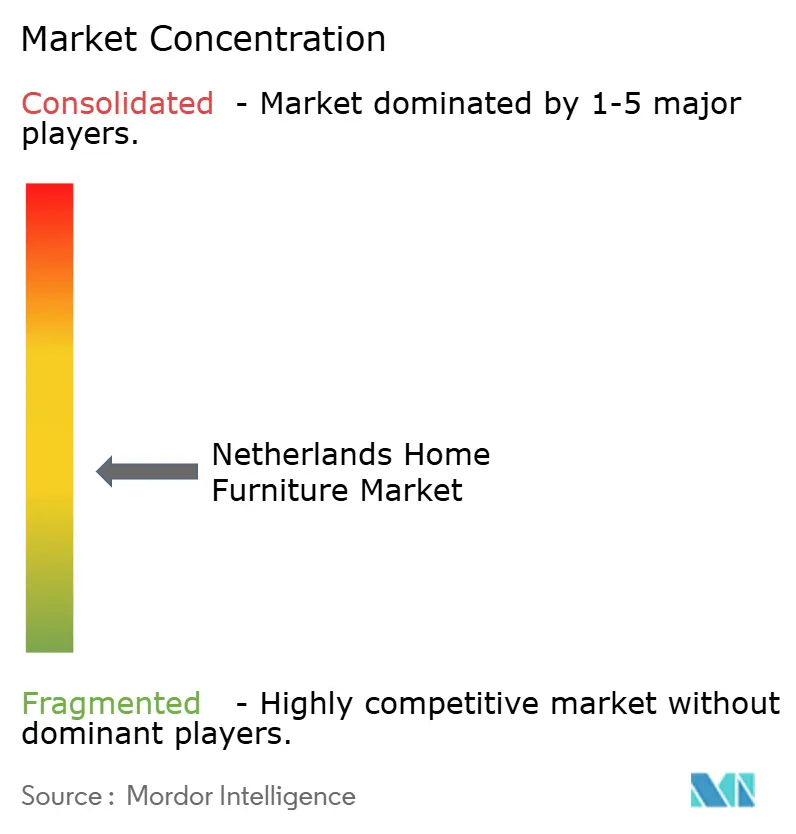

Competitive Landscape

Moderate fragmentation defines the Netherlands home furniture market, yet consolidation momentum is unmistakable. XXXLutz’s March 2025 squeeze-out of home24 SE strengthens its continental e-commerce position and injects omnichannel expertise for faster Dutch roll-out. IKEA sustains leadership by investing EUR 2.1 billion in Europe-wide price adjustments, defending affordability despite input inflation. JYSK’s automation blueprint halves order-processing times and signals escalation in the logistics arms race among big-box retailers. Domestic players like Made by Valk adapt through niche craft positioning, touting Dutch oak provenance and tailor-made dimensions.

Digital tools differentiate between front-runners: augmented-reality platforms decrease return rates below 4% versus the industry’s 8% norm, enhancing profitability. Sustainability is no longer a unique selling point but a license to operate; non-compliant producers face delisting by 2026 when new formaldehyde rules bite. Workforce investments, including in-house academies for upholstery skills, secure production continuity and feed employer-branding campaigns that resonate with socially conscious talent pools. Collaborative innovation-as-a-service pilots between insurers and manufacturers, embodies the sector’s search for recurring revenue and lower resource intensity.

Emerging threats stem from Asian low-cost exporters, whose 50% import surge in 2024 underscores price pressure. Dutch firms counter by emphasizing shorter lead-times, localized after-sales, and transparent sourcing. Market entries by technology giants exploring smart-home ecosystems may disrupt incumbent hierarchies, transforming furniture into platforms for integrated services. Agility in design iterations, enabled by digital twins and small-lot production, becomes the hallmark of winners in the dynamic Netherlands home furniture market. Regulatory compliance with EU formaldehyde emission limits and circular economy mandates is creating barriers to entry while potentially disrupting established market positions based on cost leadership rather than sustainability performance

Netherlands Home Furniture Industry Leaders

Ikea

Leen Bakker

Home24

Beliani

Meubella

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circular assortment expansion and traceable material sourcing create room for retailers and brands to operationalize take-back, refurbishment, and material reuse at scale. Intergamma’s pilot to sell circular wood and board materials through selected Gamma and Karwei stores (Netherlands and Belgium) serves as a concrete signal of demand-side and channel readiness for more circular inputs and products, while also pushing private-label and supplier specifications toward documented recycled or certified content. With wood holding 56.88% of material share (2025) and formaldehyde and VOC scrutiny tightening, suppliers with low-emission panels, water-based adhesives, and verified chain-of-custody credentials have a clearer path to listings, while reducing delisting risk in modern retail.

Digital operations and data backbone investments are also translating into practical routes for mass customization, faster lead times, and auditable ESG reporting. Royal Ahrend’s selection of IFS Cloud to integrate operations across 19 countries and 5 production sites (supporting ESG reporting and furniture-as-a-service execution) and Meubelfabriek De Toekomst’s move to SAP S/4HANA Public Cloud to centralize financial and operational processes show how firms are improving production flexibility. These updates support opportunities in configurable, space-efficient, and ergonomic categories tied to hybrid work and smaller dwelling footprints, while also enabling commercial models such as leasing, buy-back credits, and service contracts through better asset tracking, lifecycle data capture, and reverse-logistics coordination.

Recent Industry Developments

- June 2026: JYSK opened a new store in Barneveld as part of its Netherlands expansion, aligning the footprint toward a stated total of 110 locations. The added capacity improves local availability for value-oriented furniture and increases competitive pressure on incumbent specialty retailers through broader store coverage and faster pickup and returns options.

- April 2026: JYSK opened four stores (Amsterdam, Leek, Veendam, and Zierikzee) on 15 April 2026 after acquiring these locations from Leen Bakker. The conversions accelerated JYSK’s network build-out and illustrated how distressed or divested retail sites are being recycled into active growth platforms in the Dutch home furnishings channel.

- October 2024: IQVentures acquired The Aaron’s Company for USD 504 million, expanding lease-to-own retail capabilities. The transaction supports the broader shift toward alternative payment and access models for big-ticket household purchases, reinforcing the role of leasing and subscription-style propositions in furniture retail.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the Netherlands home furniture market as the value of furniture purchased for residential use, covering common household rooms and outdoor home settings, across offline and online retail, measured in current USD.

Scope exclusions: We exclude contract and office-only furniture used mainly in commercial spaces, along with services such as installation, repair, and interior design fees.

Segmentation Overview

- By Product

- Living Room and Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Furniture Stores (incl. exclusive brand outlets & local unorganized)

- Online

- Other Distribution Channels (hypermarkets, supermarkets, teleshopping, department stores)

- By Geography

- Randstad

- Southern Netherlands

- Eastern Netherlands

- Northern Netherlands

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand and supply context for household furniture in the Netherlands before assumptions were built into the model. We relied on public datasets and policy references that explain household spending, construction and renovation activity, and trade flows that shape furniture availability and pricing.

Illustrative sources included Eurostat (COICOP household consumption and retail indicators), Statistics Netherlands (CBS) releases on retail turnover and household trends, European Commission and EU product-safety guidance (including formaldehyde emission limits), UN Comtrade for import and export patterns, and relevant trade association and customs publications where data is openly accessible. We also reviewed company filings, investor presentations, reputable news coverage, and, where required, an approved paid subscription for company financials and for patent checks to validate material and product innovation signals. These sources are not exhaustive, and many other public references were consulted to cross-check data points and clarify assumptions.

Primary Interviews and Surveys

Primary work centered on interviews and structured surveys with furniture retailers, importers and distributors, selected manufacturers, and industry specialists who track housing-linked demand. We used these conversations to sanity-check room-level demand drivers for the Netherlands, online versus offline mix, price movement expectations, and the practical impact of materials compliance and supply constraints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | |

| Mid tier: 43% | Functional/Unit leaders: 33% | |

| Smaller Players: 20% | Managers: 51% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where household demand is reconstructed using national consumption patterns, housing and renovation signals, and furniture trade exposure that influences on-shelf availability in the Netherlands. Those totals are then checked with selective bottom-up approximations, such as sampled average selling price (ASP) bands by major furniture types multiplied by implied unit movement, followed by channel checks with retailers to adjust for gaps.

Key inputs were chosen because they are observable and can be refreshed, including household spending trends on furnishings, housing turnover and renovation intent, online share progression, import dependency and shipping frictions, and ASP movement linked to wood and other material cost swings (plus compliance-driven material substitutions). Forecasting uses scenario analysis, where expected paths for housing activity and discretionary spending are converted into category-level growth, then weighted by what primary respondents described as the most likely base case. When bottom-up signals were thin for a niche category, we filled the gap using adjacent category ratios and then re-tested the result with retailer feedback before finalizing.

Data Validation & Update Cycle

We validate outputs through triangulation across independent signals, where market totals are compared against household spending direction, retail turnover momentum, and trade-based supply indicators, and then variances are investigated. Outliers are reviewed in more than one step, and assumptions are revisited when category growth or price movement looks inconsistent with what interviews and public data suggest.

The model is refreshed annually, and interim updates are triggered when there is a material shift in housing demand, inflation, or regulatory compliance that would move prices or product availability. Before delivery, an analyst performs a fresh pass on key inputs and recent events so clients receive the latest updated view.

Mordor Intelligence's Netherlands Home Furniture Market Size Compared With Other Published Estimates

Published numbers for the Netherlands home furniture market can vary even when they sound like they measure the same thing, because the market can be counted from consumer spending, from retail turnover, or from production and trade value. Differences also show up when publishers treat e-commerce and cross-border deliveries differently, or when they mix furniture with wider home furnishings.

The main gap comes from whether the estimate captures the full home furniture demand pool across channels and regions, where Mordor Intelligence counts residential furniture purchases in value terms across major room categories and distribution channels, rather than focusing only on specialist retail turnover or a narrower product set. Other gaps usually come from how prices are converted to USD, whether mid-range and premium ASP changes are modeled explicitly, and how recently assumptions were refreshed after cost and compliance shifts that affect materials.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.93 B (2025) | |

| Trade Data Platform A | USD 6.35 B (2025) | Often closer to furniture retail turnover or a narrower tracked channel set, which can undercount online-only players and general merchandisers that sell furniture alongside other goods. |

| Industry Data Portal B | USD 12.95 B (2025) | May reflect broader household furnishings consumption and related categories beyond furniture, and can apply EUR to USD conversion timing that lifts the USD value versus a furniture-only scope. |

The spread across the figures is mainly explained by what is included (furniture-only versus wider furnishings) and whether the value is built from consumer demand or from a limited retail lens. By tying the model to repeatable signals like household spending direction, channel mix shifts, and realistic ASP movement checks, our estimate stays traceable to clear inputs that can be updated each year.

Key Questions Answered in the Report

How fast is the Netherlands home furniture market expected to grow to 2031?

It is projected to expand at a 4.45% CAGR, lifting value from USD8.93 billion in 2025 to USD11.59 billion by 2031.

Which product category currently leads Dutch furniture spending?

Living and Dining Furniture holds the largest share, accounting for 36.72% of 2025 revenues.

Why are premium furniture sales rising so quickly?

Wage growth and sustainability preferences drive consumers toward higher-quality, longer-lasting pieces, pushing premium segment CAGR to 6.95%.

What region shows the fastest furniture demand growth?

Southern Netherlands is forecast to post an 10.78% CAGR thanks to strong new-build activity and industrial expansion.

How are formaldehyde rules affecting manufacturers?

The August 2026 EU limit is forcing investment in low-VOC materials and new finishing techniques to maintain market access.

Page last updated on: