Netherlands Commercial Greenhouse Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

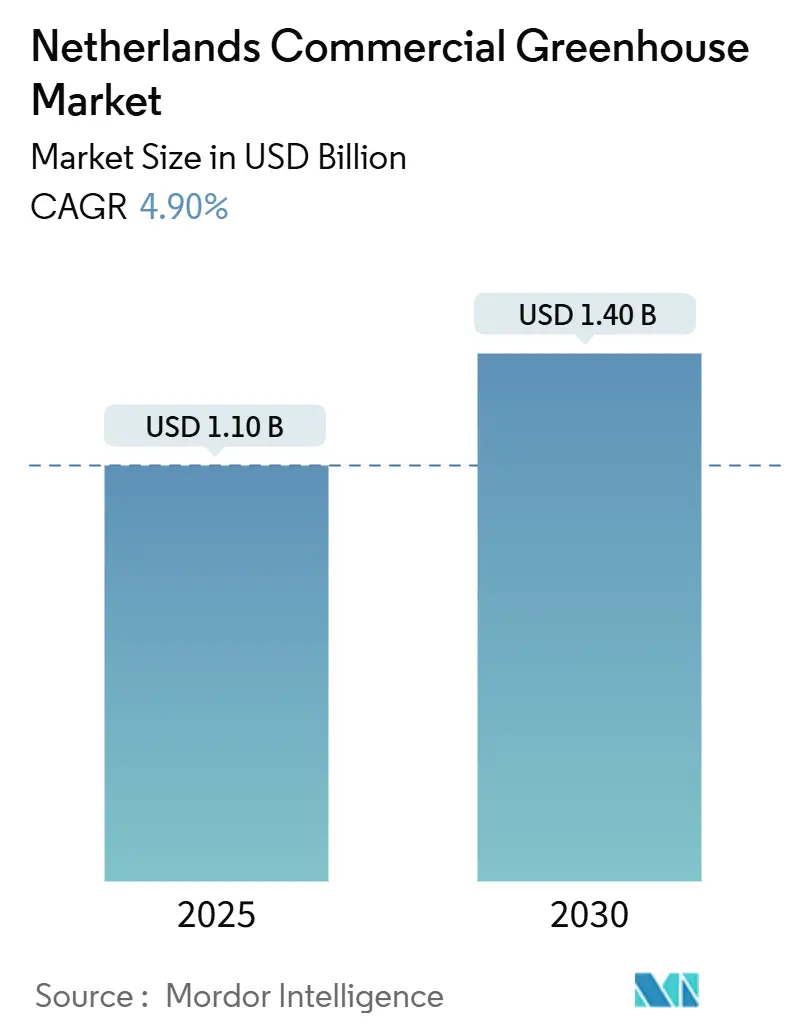

| Market Size (2025) | USD 1.10 Billion |

| Market Size (2030) | USD 1.40 Billion |

| Growth Rate (2025 - 2030) | 4.90% CAGR |

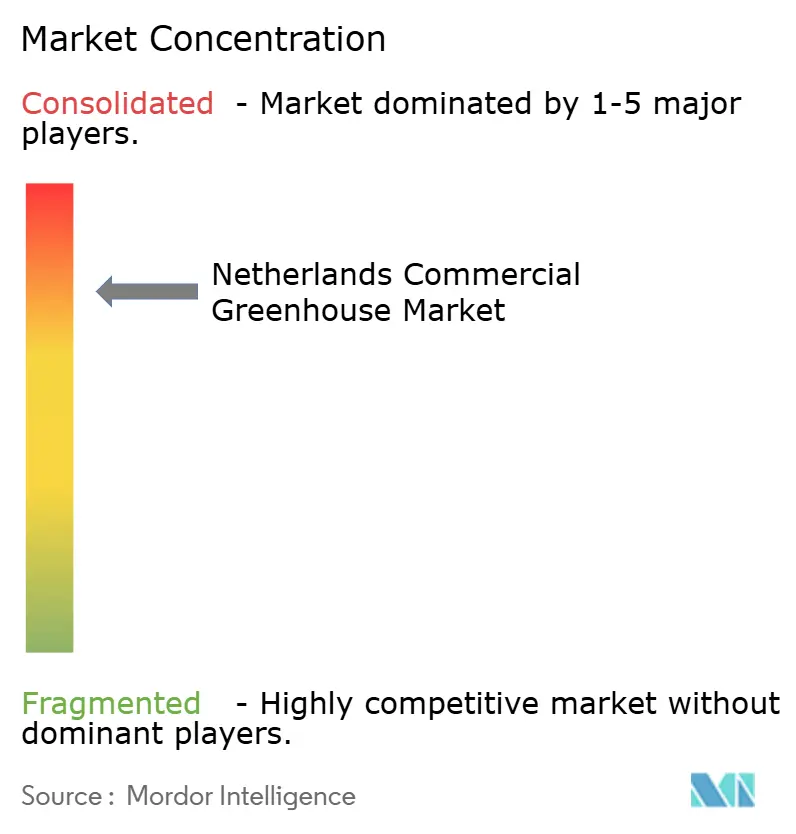

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Netherlands Commercial Greenhouse Market Analysis by Mordor Intelligence

The Netherlands commercial greenhouse market size stands at USD 1.1 billion in 2025 and is forecast to reach USD 1.4 billion by 2030, advancing at a 4.9% CAGR over the period. This steady trajectory reflects the industry’s careful navigation of energy-price swings, land scarcity, and rising automation costs. Export-oriented growers are retrofitting legacy glass structures with climate computers, heat pumps, and geothermal links to stay competitive against lower-cost Mediterranean suppliers. High upfront capital requirements favor the top quartile of operators, accelerating consolidation and strengthening the bargaining power of equipment vendors. Government carbon dioxide (CO₂) levies and Sustainable Energy Production and Climate Transition (SDE++) subsidies encourage investments in heat pumps and semi-closed systems, which reduce fossil fuel use[1]Source: Government of the Netherlands, “CO₂ Levy and SDE++ Scheme,” government.nl. Meanwhile, data-driven climate platforms reduce labor hours by up to 80% and trim energy consumption by approximately 15%. The market’s technology pivot is opening white-space niches for software-led entrants that overlay onto existing infrastructure rather than displacing it.

Key Report Takeaways

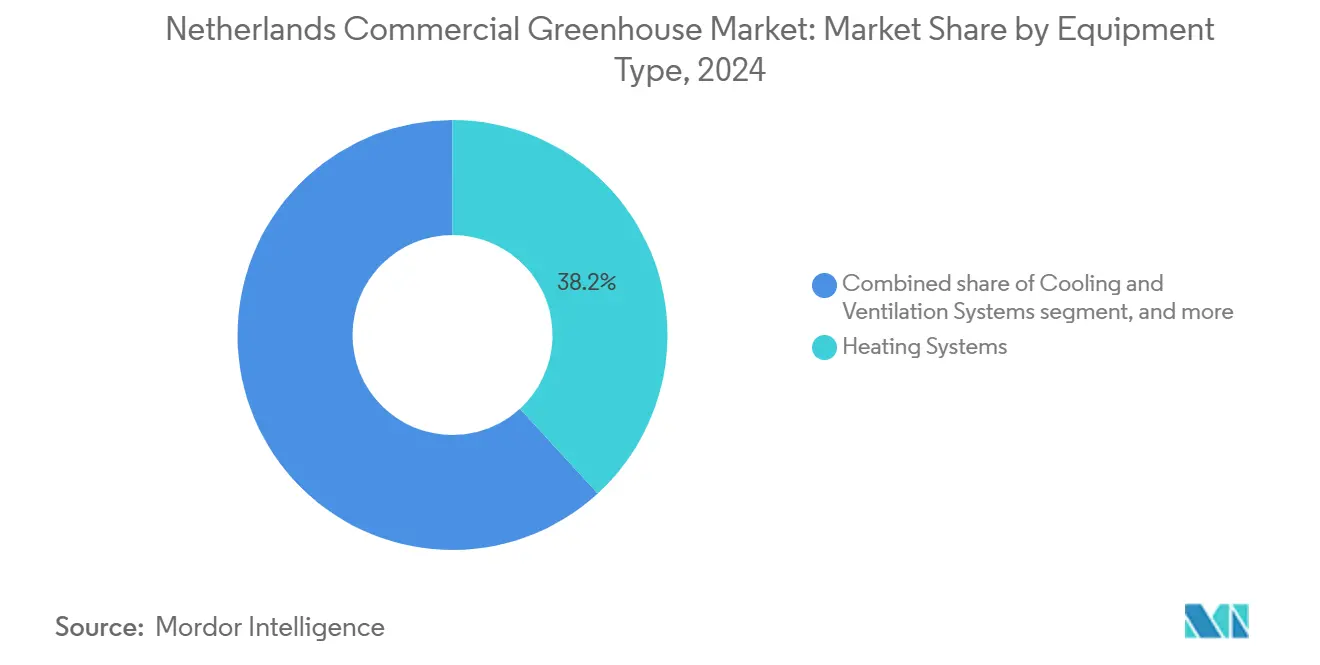

- By equipment type, heating systems led with 38.2 of % Netherlands commercial greenhouse market share in 2024, while control and automation is projected to deliver the fastest 9.4% CAGR through 2030.

- By crop type, fruits and vegetables captured 64.0% revenue in 2024, while herbs and microgreens are poised for an 8.6% CAGR to 2030.

- By greenhouse type, glass structures accounted for 54.5% of the Netherlands commercial greenhouse market size in 2024, and high-tech semi-closed and closed configurations are expanding at a 10.3% CAGR to 2030.

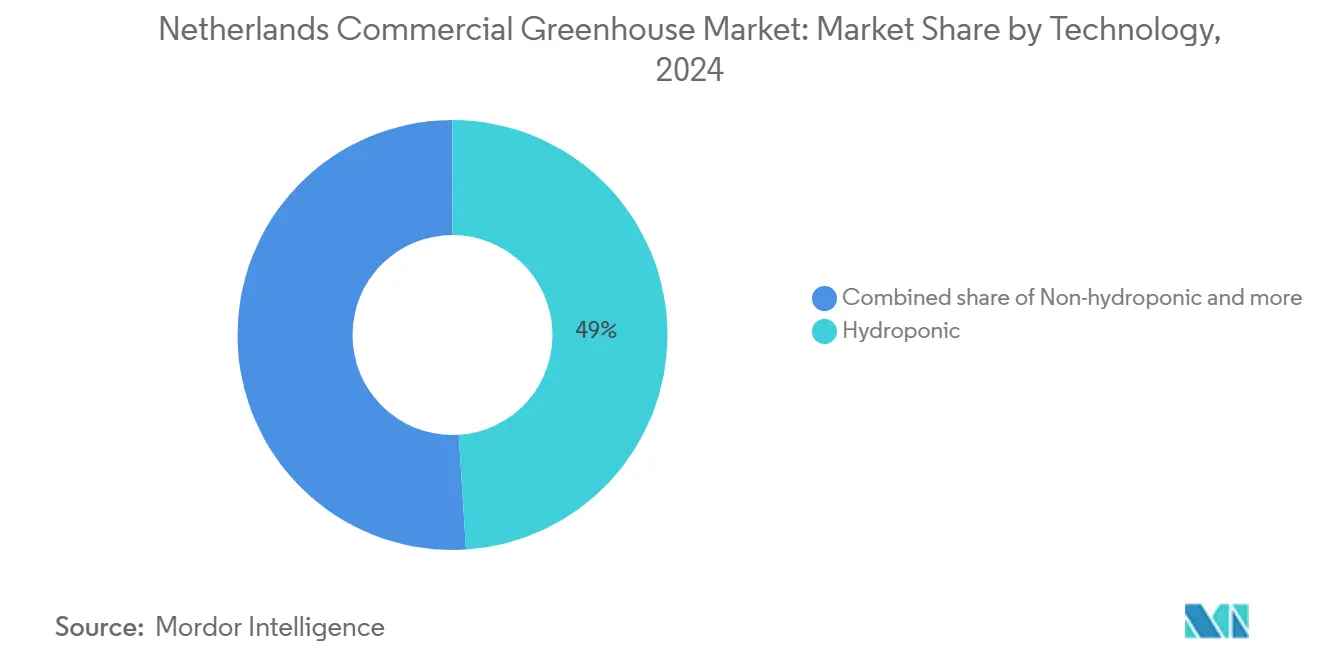

- By technology, hydroponics accounted for 49.0% revenue in 2024, whereas hybrid and vertical integration systems are projected to grow at a 12.5% CAGR through 2030.

Netherlands Commercial Greenhouse Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-oriented horticulture demand resilience | +1.2% | Netherlands core, spillover to Belgium and Germany | Medium term (2-4 years) |

| Government CO₂-reduction subsidies for greenhouse retrofits | +0.9% | Netherlands national, early adoption in Westland and Venlo | Short term (≤ 2 years) |

| Rapid adoption of data-driven climate control systems | +1.1% | Netherlands national, pilot expansion to North America and Middle East | Medium term (2-4 years) |

| Declining availability of arable land nationwide | +0.6% | Netherlands national, acute in Randstad urban corridor | Long term (≥ 4 years) |

| Energy-price hedging through combined heat and power | +0.5% | Netherlands core, limited replication in Belgium and United Kingdom | Short term (≤ 2 years) |

| Integration with district heat networks and geothermal wells | +0.7% | Netherlands national, concentrated in Westland and Venlo clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-Oriented Horticulture Demand Resilience

Roughly 80% of grower revenue is generated from cross-border shipments, insulating the Netherlands' commercial greenhouse market from domestic fluctuations. Cut-flower exports rose 7% to EUR 3.4 billion (USD 3.74 billion) in the first nine months of 2024 despite uneven European demand, and Royal FloraHolland cleared EUR 5.1 billion (USD 6.05 billion) in annual turnover, reinforcing its role as Europe’s price-discovery hub[2]Source: Royal FloraHolland, “Export Statistics Q1-Q3 2024,” royalfloraholland.com. Continuous reinvestment in lighting and climate technology ensures that Dutch stems remain within supermarket quality tolerances, providing a stable foundation for equipment demand even when building permits are slow. The sector maintains logistics links with 119 countries, as evidenced by the 12,200 overseas attendees at GreenTech Amsterdam 2024, and contributes USD 8.7 billion, equivalent to approximately 1.5% of the national gross domestic product.

Government CO₂-Reduction Subsidies for Greenhouse Retrofits

The SDE++ program earmarked EUR 11.5 billion (USD 12.65 billion) in 2024 for daylight greenhouses, air-water heat pumps and photovoltaic-thermal (PV-T) systems, while a CO₂ levy that started at EUR 9.50 per metric ton (USD 10.45 per ton) in 2025 climbs to EUR 17.70 per metric ton (USD 19.47 per metric ton) by 2030. This push-pull policy mix triggered geothermal projects, such as the Koekoekspolder well, which cost EUR 12.5 million (USD 13.75 million), and Warmte Netwerk Westland’s 500-megawatt district heat build-out[3]Source: Warmte Netwerk Westland, “500 MW District-Heat Plan,” warmtenetwerkwestland.nl. Banks now label “future-proof” projects as those with zero natural-gas combustion, effectively excluding mid-tier farms from credit unless they embrace low-carbon heat.

Rapid Adoption of Data-Driven Climate Control Systems

Platforms such as Blue Radix Crop Controller reduce operator workload by 80%, increase yields by 7%, and decrease energy use by 15% in commercial pilots. Priva B.V.'s Plantonomy and Hoogendoorn’s IIVO suites mirror these gains, integrating sensor arrays with reinforcement learning to shift lighting to off-peak tariffs and adjust CO₂ dosing on the fly. The AGROS II consortium demonstrated fully autonomous management in a tomato block that achieved yields comparable to those of experts, while Ridder Productive increased labor productivity by 30% in customer trials. The software layer is becoming a decisive factor in equipment tenders, as subscription fees are replacing one-off sales.

Energy-Price Hedging Through Combined Heat and Power

Approximately 60% of sites operate combined heat and power (CHP) engines, totaling 2,500 megawatts, which consumed 3.9 billion cubic meters of gas in 2021. Spark-spread arbitrage cushioned the Title Transfer Facility (TTF) spike to EUR 45 per megawatt-hour (USD 49.5 per megawatt-hour) in November 2024, but grid operator Stedin has frozen new CHP feed-ins, steering newcomers toward geothermal heat. A looming hydrogen tax in 2026 closes blended-fuel gaps, sharpening the choice between paying the escalating CO₂ levy or financing zero-emission wells.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capital expenditure | -0.8% | Netherlands national, acute for mid-tier and family-owned operations | Medium term (2-4 years) |

| Volatile natural-gas pricing post-2022 | -0.6% | Netherlands national, spillover to Belgium and Germany | Short term (≤ 2 years) |

| Labor scarcity in skilled greenhouse operations | -0.5% | Netherlands national, concentrated in Westland and Venlo | Medium term (2-4 years) |

| Strict nitrate-emission caps limiting expansion | -0.4% | Netherlands national, most restrictive near Natura 2000 areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Expenditure

Building a conventional glass unit costs EUR 150–250 per square meter (USD 165–275 per square meter). Semi-closed conversions exceed EUR 500 per square meter (USD 550 per square meter), and light-emitting diode (LED) retrofits add EUR 25–40 per square meter (USD 27.5–44 per square meter). Only top-quartile farms can self-fund, the rest rely on Rabobank Group, which finances only geothermal-ready projects. Consolidation is inevitable, the ten biggest tomato growers occupy over 50% of the national area.

Labor Scarcity in Skilled Greenhouse Operations

Autonomous systems lessen headcount but heighten the need for data-literate technicians who can fine-tune fertigation algorithms and troubleshoot machine-vision harvesters. The gap between the declining supply of manual labor and the increasing demand for data-literate technicians has created a bottleneck. Growers are unable to fully capitalize on the 15% energy savings and 7% yield improvements offered by autonomous climate control systems due to a lack of personnel to monitor dashboards and manage algorithmic errors during extreme weather conditions.

Segment Analysis

By Equipment Type: Automation Outpaces Legacy Heating Demand

Heating systems, which captured 38.2% of the Netherlands commercial greenhouse market share in 2024, rely on an aging Combined Heat and Power (CHP) base vulnerable to CO₂ penalties, steering capital toward heat pumps integrated into Warmte Netwerk Westland’s scheme. Control and automation devices are forecasted to grow at a 9.4% CAGR, the fastest among all categories, as growers retrofit climate computers with artificial intelligence modules that reduce labor hours by 80% and lower energy use by 15% [4]Source: Blue Radix, “Crop Controller Commercial Trials 2024,” blueradix.com.

Lighting, irrigation, and fertigation upgrades remain closely linked to the overall size of the Netherlands' commercial greenhouse market, with LED efficiency races driving demand for Signify’s 3.7 µmol/J GreenPower TLF and Hortilux’s 4.1 µmol/J NXTLED fixtures. Cooling and ventilation components face slower growth as semi-closed designs recirculate conditioned air, trimming ridge-vent demand. Niche products such as Ridder climate screens and Logiqs transport robots find traction as incremental retrofits that avoid full permit reviews.

Note: Segment shares of all individual segments available upon report purchase

By Crop Type: Herbs Surge as Tomatoes Plateau

Herbs and microgreens are projected to post an 8.6% CAGR through 2030, boosted by urban grocers paying premiums for 24-hour-old basil and cress. Fruits and vegetables that accounted for 64.0% of the Netherlands commercial greenhouse market size in 2024, face margin pressure from Spain and Morocco. Flower exports rose to EUR 3.4 billion (USD 3.74 billion) in the first 3 quarters of 2024, demonstrating resilience despite shifting consumer tastes toward experiences over decorative items.

Other crop niches, including protein-rich legumes under study at Maastricht University, trail the Netherlands commercial greenhouse market size but present upside if plant-based diets accelerate. Growers are increasingly rotating energy-intensive tomatoes with lower-heat herbs during the winter, thereby optimizing LED and heat pump economics.

By Greenhouse Type: Semi-Closed Designs Capture Retrofit Spend

Semi-closed and closed units are anticipated to expand at a 10.3% CAGR, outpacing glass greenhouses, which still account for 54.5% of the area, due to legacy installations. Land prices exceeding EUR 1 million (USD 1.10 million) per hectare, combined with 18- to 24-month nitrogen-permit cycles, discourage new glass builds and favor upgrading existing stock. Bom Group’s Wageningen project demonstrates the semi-closed integration of heat pumps and underground storage, compliant with future-proof lending.

Film and polycarbonate houses occupy niches in propagation or short-cycle crops but cannot match the 25-year lifespan of glass. KUBO Group’s Ultra-Clima design, recognized in 2025 for its low CO₂ footprint, indicates a hybrid path that combines modular speed with semi-closed energy efficiency.

By Technology: Vertical Integration Disrupts Substrate Orthodoxy

Hybrid and vertical systems are projected to surge 12.5% through 2030, which is double the average annual growth rate of the Netherlands commercial greenhouse market. Wageningen’s Fieldlab Vertical Farming 2.0 shows how stacking tiers multiplies output per square meter. Hydroponics maintains a 49.0% revenue share but sees slower growth as growers trial aeroponics and LED-dense vertical racks to save water and electricity. LettUs Grow achieved 20% yield uplifts in leafy greens by optimizing root oxygenation, while Grodan’s rock-wool and Signify lighting partnership showed a 50% reduction in heat input in tomatoes.

Non-hydroponic soil systems persist in organic-certified channels but lag the Netherlands commercial greenhouse market size expansion because water-use premiums outweigh price gains. Software convergence is the emerging battleground: Blue Radix integrates across greenhouses, hydroponic ponds, and vertical racks, letting growers standardize on one algorithm regardless of build type.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Westland-Rotterdam corridor hosts 4,500 of the country’s 10,500 hectares and accounts for the bulk of the Netherlands commercial greenhouse market size. This clustering drives network efficiencies yet strains power grids, prompting Stedin’s CHP moratorium. Export ratios remain unmatched, with EUR 10.8 billion (USD 11.88 billion) in fresh produce representing 17.5% of 2024 national exports.

Carbon policies are reshaping heat choices across provinces. Limburg and Noord-Brabant attract new acreage thanks to laxer nitrogen limits, but longer hauls to Royal FloraHolland erode cost savings. The CO₂ levy is set to rise to EUR 17.70 per ton (USD 19.47 per ton) in 2030, plus SDE++ retrofit subsidies, positioning geothermal clusters such as Koekoekspolder to expand.

Innovation hubs in Bleiswijk and Venlo anchor R&D, while Dutch turnkey vendors export design know-how to China and Canada as a hedge against domestic land scarcity. GreenTech’s 2024 edition drew 510 exhibitors and 12,200 visitors, confirming the Netherlands as a global knowledge broker for controlled-environment agriculture.

Competitive Landscape

The Netherlands commercial greenhouse industry is dominated by a few key players, including Ridder Group, Priva, KUBO Group, Certhon, and Bom Group, which collectively account for a significant share of the revenue. Capital intensity and multi-year service contracts entrench these leaders. Ridder invested in agritech in 2024, earmarking for controlled-environment modules. Priva and Hoogendoorn embed academic partnerships to validate proprietary algorithms early, while Netafim’s acquisition of Gakon illustrates multinationals buying Dutch integrators to reach growers directly.

Disruptors such as Blue Radix and Organifarms penetrate via software subscriptions or harvest robotics, targeting pain points that incumbents have not fully addressed. Vendors increasingly bundle zero-interest financing on hardware in exchange for five-year cloud contracts, smoothing cash flows for growers but tightening vendor lock-in.

These developments are projected to drive innovation and efficiency in the Netherlands' commercial greenhouse market. The integration of advanced technologies and strategic partnerships will likely enhance productivity and sustainability. Furthermore, the entry of disruptors and flexible financing options will provide growers with more accessible solutions, fostering growth and competitiveness in the market.

Netherlands Commercial Greenhouse Industry Leaders

-

Priva B.V.

-

KUBO Group

-

Ridder Group

-

Bom Group

-

Certhon (Denso Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: KUBO Group's Ultra-Clima greenhouse received official recognition for its low carbon dioxide footprint, validating its compliance with the Dutch government's 2040 climate-neutral mandate and positioning it as a preferred solution for growers seeking Rabobank future-proof financing.

- January 2025: Hoogendoorn Growth Management launched a smart irrigation software add-on, enabling growers to optimize water and fertilizer delivery based on real-time sensor data and reducing input costs by approximately 10 percent in early trials.

- September 2024: Certhon (Denso Corporation) commenced construction of a state-of-the-art greenhouse for Opti-flor, incorporating advanced climate control, energy-efficient systems, and fertigation automation to meet the client's sustainability targets and secure compliance with the Dutch carbon dioxide levy.

Netherlands Commercial Greenhouse Market Report Scope

The Netherlands Commercial Greenhouse Market Report is Segmented by Equipment Type (Heating Systems, Cooling and Ventilation Systems, and Others), by Crop Type (Fruits and Vegetables, Flowers and Ornamentals, and Others), Greenhouse Type (Glass Greenhouses, Polyethylene-Film Greenhouses, and Others), and Technology (Hydroponic, and Others). The Market Forecasts are Provided in Terms of Value in USD.

| Heating Systems |

| Cooling and Ventilation Systems |

| Irrigation and Fertigation Systems |

| Lighting Systems |

| Control and Automation |

| Other Equipment Types |

| Fruits and Vegetables |

| Flowers and Ornamentals |

| Herbs and Microgreens |

| Other Crop Types |

| Glass Greenhouses |

| Polyethylene-Film Greenhouses |

| Polycarbonate Greenhouses |

| High-Tech (Semi-Closed / Closed) Greenhouses |

| Hydroponic |

| Non-hydroponic (Soil/Substrate) |

| Hybrid and Vertical Integration |

| By Equipment Type | Heating Systems |

| Cooling and Ventilation Systems | |

| Irrigation and Fertigation Systems | |

| Lighting Systems | |

| Control and Automation | |

| Other Equipment Types | |

| By Crop Type | Fruits and Vegetables |

| Flowers and Ornamentals | |

| Herbs and Microgreens | |

| Other Crop Types | |

| By Greenhouse Type | Glass Greenhouses |

| Polyethylene-Film Greenhouses | |

| Polycarbonate Greenhouses | |

| High-Tech (Semi-Closed / Closed) Greenhouses | |

| By Technology | Hydroponic |

| Non-hydroponic (Soil/Substrate) | |

| Hybrid and Vertical Integration |

Key Questions Answered in the Report

How fast is Netherlands commercial greenhouse market projected to grow to 2030?

The Netherlands commercial greenhouse market is projected to expand from USD 1.1 billion in 2025 to USD 1.4 billion in 2030 at a 4.9% CAGR.

Which equipment category is growing the quickest?

Control and Automation is forecast to lead with a 9.4% CAGR, outpacing heating, lighting and irrigation devices.

Why are semi-closed greenhouses gaining traction?

Semi-closed designs recirculate air, cut CO₂ emissions and qualify for SDE++ subsidies, helping growers meet the rising CO₂ levy.

Which companies dominate the market?

Ridder Group, Priva, KUBO Group, Certhon and Bom Group jointly control major share of the market revenue, reflecting high entry barriers and strong turnkey integration capabilities.

Page last updated on: