Needle Coke Market Size

| Study Period | 2019 - 2029 |

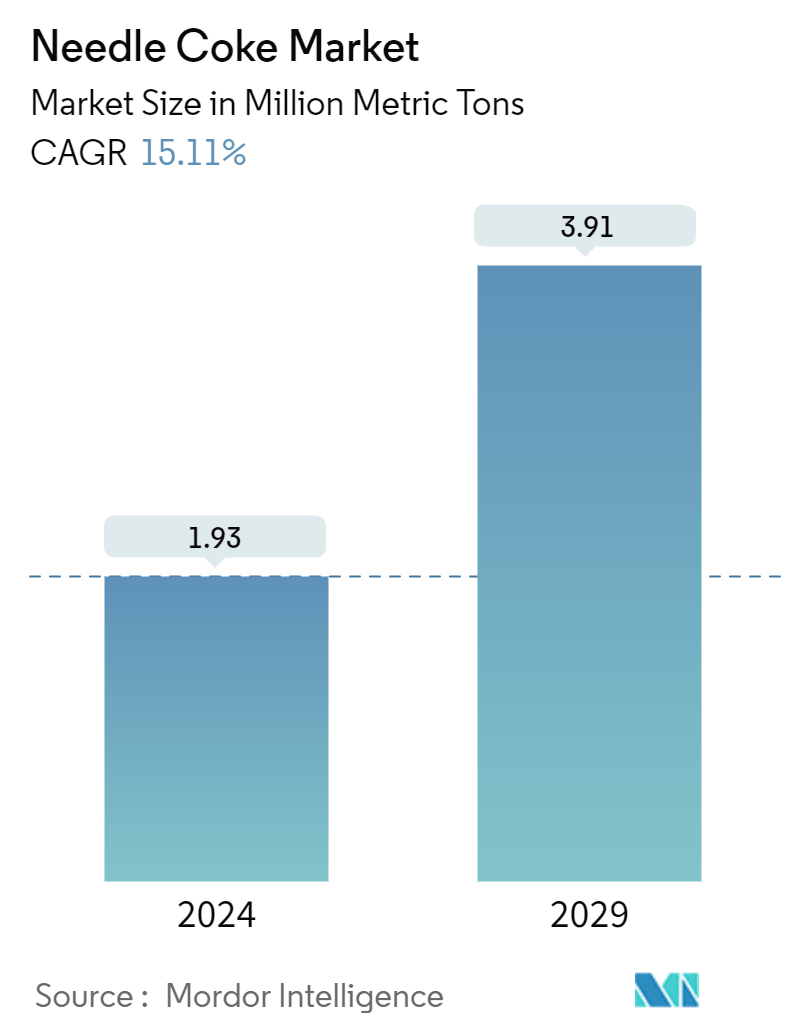

| Market Volume (2024) | 1.93 Million metric tons |

| Market Volume (2029) | 3.91 Million metric tons |

| CAGR (2024 - 2029) | 15.11 % |

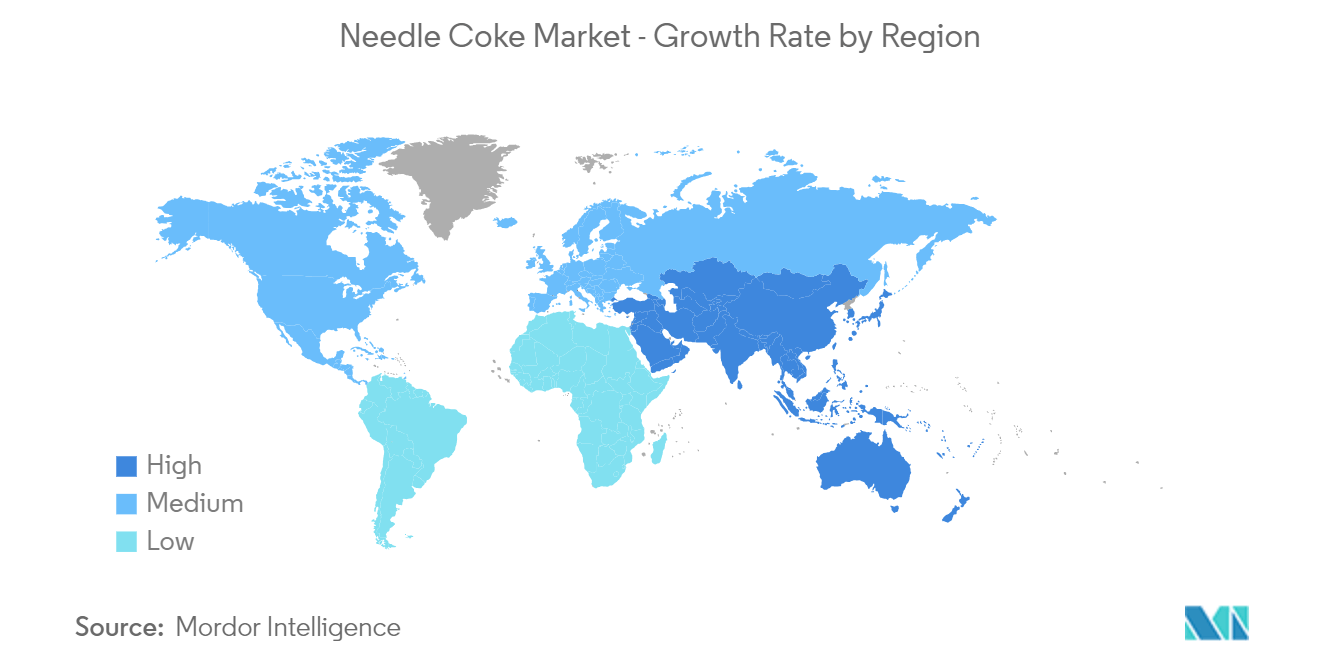

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Needle Coke Market Analysis

The Needle Coke Market size is estimated at 1.93 Million metric tons in 2024, and is expected to reach 3.91 Million metric tons by 2029, growing at a CAGR of 15.11% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the needle coke market. During the pandemic, the manufacturing of graphite electrodes was heavily affected due to less demand from the steel manufacturing plants, which reduced the consumption of needle coke. However, the market registered a significant growth rate after the restrictions were lifted due to the recovering demand for lithium-ion batteries and graphite electrodes.

• Over the medium term, increasing investments in EAF steel manufacturing and favorable government policies to increase scrap steel consumption are significant factors driving the growth of the studied market.

• However, health hazards associated with petroleum coke are likely to hinder the growth of the studied market.

• The increase in lithium-ion battery production globally is likely to act as an opportunity for the market studied during the forecast period.

• Asia-Pacific emerged as the dominant market. It is also expected to register the highest CAGR from 2024 to 2029 due to the high demand from countries such as India, China, Japan, and others.

Needle Coke Market Trends

Graphite Electrodes Segment to Dominate the Market

• Needle coke is a primary raw material for graphite electrodes in electric furnaces. It is a premium-grade, high-value petroleum coke used to manufacture graphite electrodes with a very low coefficient of thermal expansion (CTE).

• Owing to the wide application of graphite electrodes in electric arc furnaces, which are used in steel and other metal industries, the application of needle coke for graphite electrodes accounts for the largest application of needle coke.

• Graphite has high thermal conductivity and is resistant to heat and any impact. Also, it has low electrical resistance, which is needed to conduct large electrical currents necessary to melt iron. Thus, it can sustain extremely high heat levels generated by EAF (electric arc furnace). Making the electrodes requires processing coke, including baking and rebaking, to convert it into graphite, which can take up to six months.

• Graphite electrodes are divided into four types: RP graphite electrodes, HP graphite electrodes, SHP graphite electrodes, and UHP graphite electrodes.

• Graphite electrodes are primarily used to manufacture electric arc furnace steel, alloy steel, various alloys, and nonmetals. These electrodes can generate high levels of heat and are also used in refining steel and similar smelting processes. They can melt iron scrap in an electric arc furnace at about 1,600℃.

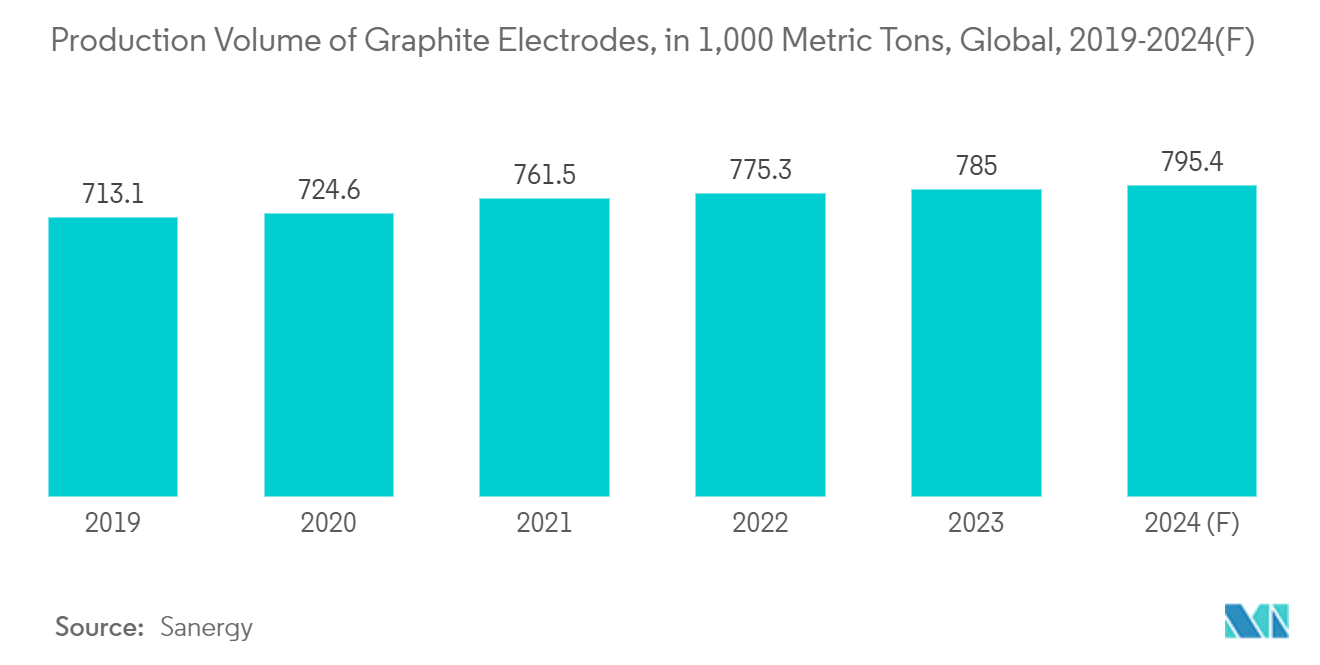

• According to data from Sanergy Group Limited, the production volume of graphite electrodes worldwide was 8785 thousand metric tons in 2023 and is projected to reach 795.4 thousand metric tons in 2024.

• In December 2023, Graphite India Limited (GIL) invested INR 50 crore (approximately USD 6 million) in compulsorily convertible preference shares of Godi India Private Ltd. This investment provides GIL with a 31% equity shareholding in Godi India. Godi India is engaged in advanced Research and development to support the production of sustainable batteries for electric vehicles (EVs) and supercapacitor-based energy storage systems. Godi India’s environment-friendly and carbon-neutral processes include Aqueous Electrode ProcessingTM, Active Dry CoatingTM, and Pranic BinderTM. This investment aligns with GIL’s strategy to diversify into advanced battery and energy storage technologies.

• In November 2023, HEG Limited successfully expanded its graphite electrode capacity in Madhya Pradesh, India, from 80 kilotons per annum to 100 kilotons per annum. The company made a substantial investment of INR 1,200 crore (USD 143.741 million) for this capacity expansion. As a result, HEG is the third-largest graphite electrode company in the Western world.

• The factors mentioned above are expected to affect the demand for needle coke for graphite electrode application during the forecast period.

Asia-Pacific to Dominate the Market

• Asia-Pacific is expected to dominate the needle coke market, as it includes countries such as China (the biggest producer and consumer of needle coke) and Japan.

• China holds the largest share of graphite electrode consumption and production capacity in the global scenario. There are over 40 official graphite electrode manufacturers in China. The Chinese market's demand for graphite electrodes and further diversification into lithium-ion battery anodes, fueled by the EV industry's growth, are both driving a comeback in the demand for needle coke. For the foreseeable future, this demand is expected to continue to increase steadily, with corresponding pricing support.

• In addition to this, the Chinese government is also focusing on developing eco-friendly means of producing steel. Hence, Chinese authorities are actively promoting Electric Arc Furnace (EAF) technology as a means to curb carbon emissions and foster sustainability in the steel industry. EAF technology relies primarily on steel scrap as its raw material, with electricity used to melt it. Driven by supportive national policies, the adoption of EAF technology is poised to become a prevailing trend in China, consequently bolstering the demand for graphite electrodes.

• Japan is one of the leading producers and exporters of petroleum, coal, and tar-based pitch needle coke. Japanese companies are one of the largest producers of graphite electrodes in the world. The market giants of graphite electrodes include Showa Denko, Nippon Carbon, SEC Carbon, and Tokai Carbon.

• The Indian steel industry is actively working to reduce carbon emissions through intensified efforts to decarbonize. As part of this push, there is a rising trend in adopting electric arc furnace (EAF) technology for steel production. EAFs rely on electricity and steel scrap, making them a more sustainable choice than traditional methods.

• With the growing adoption of EAFs, there is a significant expected surge in demand for graphite electrodes. The Indian government's move to eliminate customs duty on scrap imports directly benefits EAF steel manufacturers. Coupled with favorable national policies, these further fuel the shift toward EAFs and drive the demand for graphite electrodes.

• JFE Steel, Japan's second-largest steelmaker, announced in November 2023 its plans to construct a large-scale electric arc furnace (EAF). The EAF is slated to replace an existing blast furnace at its Kurashiki plant by around 2027. This strategic move underscored the company's commitment to curbing carbon emissions, which is in line with global climate change initiatives. The new EAF will primarily cater to automotive and other sectors, with an anticipated annual emissions reduction of 2.6 million tons.

• Graphite electrodes play an important role in the electric arc furnace (EAF) process, a key method for steel production. The steel sector in South Korea is significant, driving the nation's economic growth by catering to industries like automotive, construction, and shipbuilding. The steel industry accounts for 1.5% of the nation's GDP and 4.9% of its manufacturing sector, as reported by the Korean Iron & Steel Association. Notably, South Korea ranks as the sixth-largest steel producer globally.

• Hence, Asia-Pacific is likely to dominate the global needle-coke market based on the aspects mentioned above.

Needle Coke Industry Overview

The needle coke market is partially consolidated. Some of the major players in the market (not in any particular order) include Phillips 66 Company, China National Petroleum Corporation (CNPC), Shandong Yida Rongtong Trading Co., Shandong Jing Yang Technology Co. Ltd, and Mitsubishi Chemical Corporation.

Needle Coke Market Leaders

-

Phillips 66 Company

-

China National Petroleum Corporation (CNPC)

-

Shandong Yida Rongtong Trading Co.

-

Shandong Jing Yang Technology Co. Ltd

-

Mitsubishi Chemical Corporation

*Disclaimer: Major Players sorted in no particular order

Needle Coke Market News

• January 2024: CNPC hoisted and docked the top tower of the 400,000 tons/year of needle coke at the construction site in Jinzhou, China. The project is likely to be completed in the coming years.

• December 2022: Gazprom Neft announced its plans to launch a project to produce needle coke in its Omsk refinery, which will be utilized in manufacturing Li-ion batteries and graphite electrodes. This project is expected to be completed by 2024.

• December 2022: POSCO Chemical announced the agreement with Ultium Cells LLC to supply graphite anode material for the expansion of EV battery cells in the United States. In POSCO Chemical, the entire product was sourced from needle coke.

Needle Coke Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Investments in EAF Steel Manufacturing

4.1.2 Government Policies to Increase Scrap Steel Consumption

4.2 Restraints

4.2.1 Health Hazards Associated with Petroleum Coke

4.3 Industry Value-Chain Analysis

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Price Overview

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Petroleum Based

5.1.2 Coal-tar Pitch Based

5.2 Application

5.2.1 Graphite Electrodes

5.2.2 Lithium-ion Batteries

5.2.3 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Baosteel Group

6.4.2 China National Petroleum Corporation (CNPC)

6.4.3 China Petroleum & Chemical Corporation (Sinopec)

6.4.4 Indian Oil Corporation

6.4.5 Liaoning Baolai Bioenergy Co., Ltd.

6.4.6 Mitsubishi Chemical Corporation

6.4.7 Nippon Steel Corporation

6.4.8 Phillips 66

6.4.9 Posco Mc Materials

6.4.10 Seadrift Coke LP (Graftech International)

6.4.11 Shandong Dongyang Technology Co. Ltd

6.4.12 Shandong Yida New Materials Co. Ltd

6.4.13 Shanxi Hongte Coal Chemical Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Lithium-ion Batteries to Boost the Demand for Needle Coke

Needle Coke Industry Segmentation

Needle coke is a high-quality carbon raw material produced from coal tar and petroleum. It is generally formed as highly crystalline graphene-like carbons exhibiting long-range microstructural order with few impurities and a low coefficient of thermal expansion. It is primarily used for the manufacturing of graphite electrodes and lithium-ion batteries.

The needle coke market is segmented by product type, application, and geography. By type, it is divided into petroleum-based and coal-tar pitch-based. By application, it is divided into graphite electrodes, lithium-ion batteries, and other applications. The report also covers the market sizes and forecasts for the needle coke market in 15 countries across major regions. For each segment, the market sizing and forecasts were made on the basis of volume (kilotons).

| Product Type | |

| Petroleum Based | |

| Coal-tar Pitch Based |

| Application | |

| Graphite Electrodes | |

| Lithium-ion Batteries | |

| Other Applications |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Needle Coke Market Research Faqs

How big is the Needle Coke Market?

The Needle Coke Market size is expected to reach 1.93 million metric tons in 2024 and grow at a CAGR of 15.11% to reach 3.91 million metric tons by 2029.

What is the current Needle Coke Market size?

In 2024, the Needle Coke Market size is expected to reach 1.93 million metric tons.

Who are the key players in Needle Coke Market?

Phillips 66 Company, China National Petroleum Corporation (CNPC), Shandong Yida Rongtong Trading Co., Shandong Jing Yang Technology Co. Ltd and Mitsubishi Chemical Corporation are the major companies operating in the Needle Coke Market.

Which is the fastest growing region in Needle Coke Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Needle Coke Market?

In 2024, the Asia Pacific accounts for the largest market share in Needle Coke Market.

What years does this Needle Coke Market cover, and what was the market size in 2023?

In 2023, the Needle Coke Market size was estimated at 1.64 million metric tons. The report covers the Needle Coke Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Needle Coke Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Needle Coke Industry Report

Statistics for the 2024 Needle Coke market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Needle Coke analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Needle Coke Market Report Snapshots