| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 116.46 Billion |

| Market Size (2030) | USD 159.26 Billion |

| CAGR (2025 - 2030) | 6.46 % |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Naval Vessels Market Analysis

The Naval Vessels Market size is estimated at USD 116.46 billion in 2025, and is expected to reach USD 159.26 billion by 2030, at a CAGR of 6.46% during the forecast period (2025-2030).

The naval vessels industry is experiencing significant transformation driven by technological advancements and evolving maritime security requirements. Global defense spending reached an unprecedented USD 2,443 billion in 2023, reflecting the growing emphasis on maritime security and naval defense capabilities worldwide. The integration of advanced manufacturing technologies, including 3D printing and robotics, has revolutionized military shipbuilding processes, reducing construction times and improving efficiency. Additionally, the industry is witnessing a paradigm shift towards green technologies and integrated electric propulsion systems, which offer enhanced operational capabilities while reducing environmental impact.

The emergence of autonomous and unmanned naval vessels represents a revolutionary development in maritime operations. These platforms provide enhanced situational awareness and can execute mission-critical tasks without risking human lives. The industry is increasingly focusing on developing multi-role support vessels that can adapt to various missions, including amphibious warfare operations, force projection, and humanitarian relief operations. This trend towards versatility is reshaping fleet compositions and operational strategies across naval forces globally.

International collaboration and technology transfer have become crucial drivers of innovation in the naval vessels sector. For instance, in May 2024, UAE defense conglomerate Edge Group announced its partnership with Italian shipbuilder Fincantieri to manufacture sophisticated military vessels for global markets. The industry is also witnessing increased investment in cybersecurity solutions, with countries like Saudi Arabia signing multiple memoranda of understanding for cooperation in cybersecurity with Romania, Qatar, Spain, and Kuwait in 2023, highlighting the growing importance of digital security in naval operations.

The integration of stealth technologies has become a defining characteristic of modern warship design. Manufacturers are incorporating advanced materials and construction techniques to reduce radar, visual, sonar, and infrared signatures. This focus on stealth capabilities is complemented by the development of sophisticated naval combat systems and sensors. The industry is also witnessing significant investments in green technologies and alternative propulsion systems, with several navies exploring hybrid and electric propulsion solutions to meet environmental regulations while maintaining operational effectiveness. These technological advancements are driving the transformation of naval fleets worldwide, with a clear emphasis on enhanced capabilities and reduced environmental impact.

Naval Vessels Market Trends

Steady Growth in Annual Defense Expenditure

Global defense spending has shown consistent growth, reaching USD 2,443 billion in 2023, reflecting governments' increasing commitment to strengthening their military capabilities. This substantial investment has enabled various nations to fund their naval vessel procurement and development programs throughout the forecast period. Military powerhouses such as the US, UK, China, and India have been particularly focused on augmenting their naval fleets and sea-based combat capabilities, with several naval vessel development, procurement, and modernization programs currently underway to enhance the combat capabilities of their naval forces.

The United States exemplifies this trend with its significant naval spending, as evidenced by the US Navy's FY2023 budget proposal of USD 230.8 billion, including USD 180.5 billion for the Navy and USD 50.3 billion for the Marine Corps. This robust funding supports various procurement initiatives, including the development of new vessels and the modernization of existing fleets. The rate of growth in military spending has accelerated in recent years, with countries like Australia announcing significant investments, such as their recent USD 7.25 billion commitment to double their fleet of warships over the next decade. These substantial budgets have enabled armed forces to fund their naval vessel procurement and development programs, supporting the continuous evolution of naval capabilities.

Understand The Key Trends Shaping This Market

Download PDF

Naval Fleet Expansion and Modernization Due to Evolving Threats

The profound changes in the international strategic landscape have led to increasing maritime security challenges, driving nations to modernize and expand their naval capabilities. The configuration of the international security system has been undermined by growing hegemonism, unilateralism, and power politics, which have fueled several ongoing global conflicts. This has resulted in numerous countries implementing comprehensive fleet modernization programs to upgrade their regional naval forces' capabilities, respond to security threats effectively, and accomplish urgent, critical, and dangerous strategic missions.

The evolution of maritime threats has necessitated the development of more sophisticated naval platforms. For instance, in March 2023, the United States, Australia, and the United Kingdom announced a framework enabling Australia to acquire nuclear-powered submarines, making Australia the seventh country globally to possess this technology. This development exemplifies how nations are responding to evolving threats through strategic partnerships and advanced technology acquisition. Additionally, the rise in maritime terrorism, piracy, trafficking of prohibited substances, and illegal immigration through sea routes has compelled global naval forces to enhance their capabilities. This has led to the procurement of various types of newer-generation combat vessels, including surface combatants and submarines, equipped with advanced anti-ship, anti-air, and anti-submarine systems, sensors, and command-and-control networks.

Segment Analysis: Application

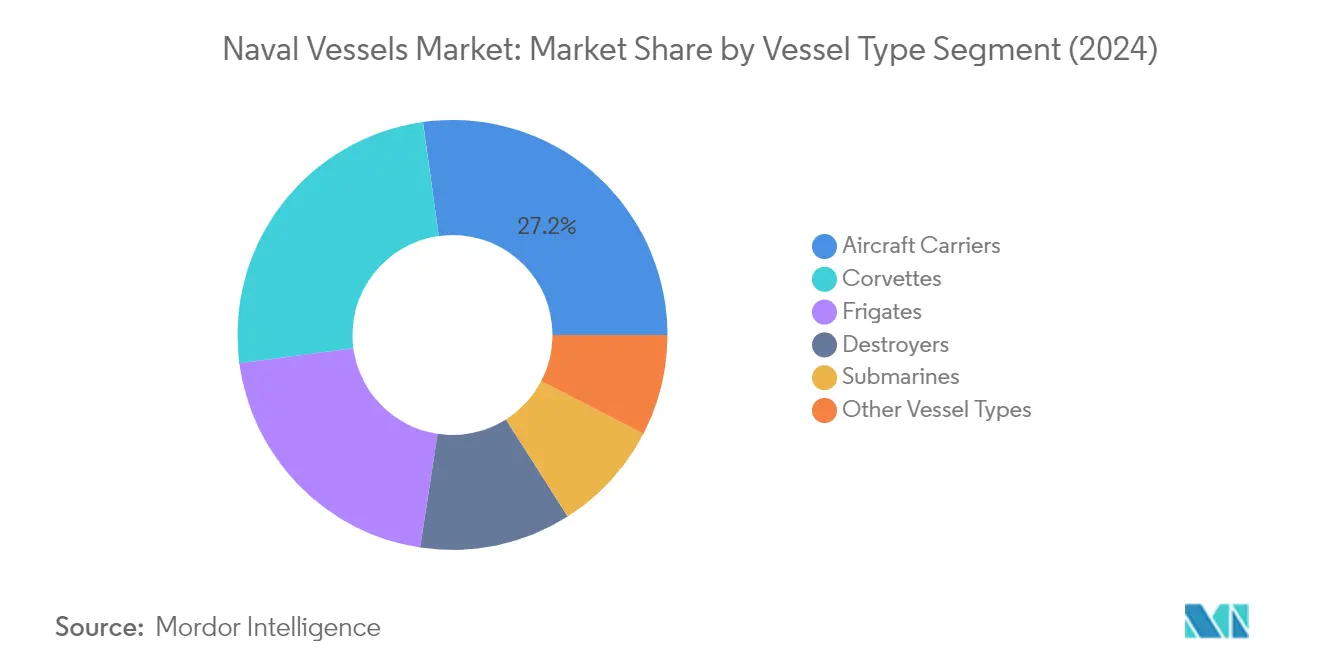

Aircraft Carriers Segment in Naval Vessels Market

Aircraft carriers dominate the naval vessels market, commanding approximately 27% market share in 2024. These vessels serve as force multipliers by enhancing the capabilities of naval task forces through their ability to deploy diverse aircraft for offensive and defensive operations. Modern aircraft carriers can conduct complex military operations across multiple domains, including air-to-air combat, ground attack, maritime interdiction, and anti-submarine warfare. The segment's dominance is reinforced by major procurement programs from naval powers like the United States, China, and India. For instance, China's launch of its third advanced aircraft carrier, Fujian, with an advanced electromagnetic catapult system, demonstrates the continued investment in this segment. Additionally, the development of the PANG (Porte-Avions de Nouvelle Génération) new-generation aircraft carrier program by France further solidifies the segment's market leadership.

Submarines Segment in Naval Vessels Market

The submarines segment is projected to witness the highest growth rate of approximately 8% during the forecast period 2024-2029. This remarkable growth is driven by significant technological advancements in submarine capabilities, including improved stealth features, longer endurance, enhanced sensor systems, and advanced weapon systems. The segment's growth is further supported by major submarine procurement programs worldwide, such as Australia's nuclear-powered military submarine acquisition under the AUKUS agreement and Indonesia's collaboration with Naval Group for Scorpène submarines. The increasing focus on underwater warfare capabilities and the strategic importance of submarines in modern naval operations have led to substantial investments in this segment. Additionally, the development of new submarine classes with advanced technologies, such as air-independent propulsion systems and enhanced combat management systems, continues to drive the segment's growth in the submarine market.

Remaining Segments in Naval Vessels Market

The naval vessels market encompasses several other significant segments, including corvettes, naval frigates, naval destroyers, and other vessel types. Corvettes represent a substantial portion of the market, offering advantages in fast attack capabilities and coastal defense operations. Naval frigates continue to be essential for multi-role operations, particularly in anti-submarine warfare and maritime patrol missions. Naval destroyers maintain their importance as powerful surface combatants with advanced air defense and missile capabilities. Other vessel types, including patrol boats and auxiliary vessels, play crucial supporting roles in naval operations. Each of these segments contributes uniquely to naval capabilities, with ongoing modernization programs and new vessel developments across various nations driving their continued relevance in the global naval vessels market.

Naval Vessels Market Geography Segment Analysis

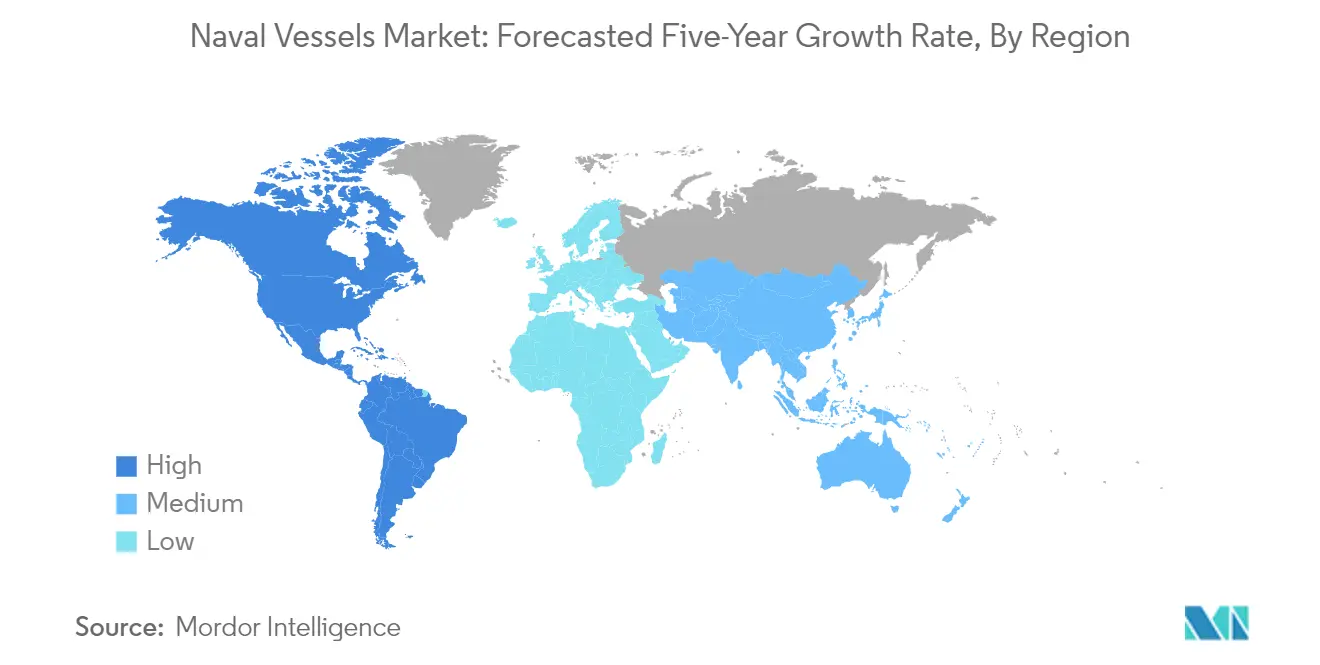

Naval Vessels Market in North America

North America represents a dominant force in the global naval vessels market, driven by substantial defense spending and continuous fleet modernization initiatives. The region's market is primarily shaped by the United States and Canada, with both nations focusing on developing advanced naval capabilities to maintain maritime superiority. The strategic importance of naval power in the region is emphasized through various procurement programs and the presence of major shipbuilding companies that contribute to technological advancement and innovation in naval vessel construction.

Naval Vessels Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 95% of the regional market share in 2024. The country operates the largest naval fleet in North America and ranks fourth globally in fleet size, with over 484 ships in active service and the reserve fleet. The U.S. Navy has been actively implementing force structure expansion plans, aiming to reach its 355-ship goal by 2034 through a mix of service life extensions and new construction. The country's robust shipbuilding infrastructure, supported by major defense contractors and shipyards, enables the development of various vessel types, from aircraft carriers to submarines.

Naval Vessels Market Growth in United States

The United States is projected to maintain the highest growth trajectory in North America with an expected CAGR of around 8% from 2024 to 2029. This growth is driven by significant investments in naval modernization programs and the development of next-generation vessels. The U.S. Navy's commitment to expanding its fleet capabilities is evident through various ongoing programs, including the Columbia-class submarine program and the procurement of new Constellation-class naval frigates. The country's focus on incorporating advanced technologies and maintaining naval superiority continues to drive market expansion, supported by substantial defense budgets and long-term fleet modernization strategies.

Naval Vessels Market in Europe

The European naval vessels market demonstrates significant diversity in terms of capabilities and requirements across different nations. The region's market is characterized by strong participation from countries like Russia, the United Kingdom, France, Germany, and Spain, each contributing unique technological expertise and naval traditions. European nations are increasingly focusing on collaborative defense initiatives while maintaining sovereign capabilities in naval vessel construction and maintenance.

Naval Vessels Market in Russia

Russia emerges as the largest market in Europe, holding approximately 28% of the regional market share in 2024. The country maintains one of the largest navy fleets globally, supported by strong indigenous manufacturing and technological capabilities. Russia's naval forces have been steadily growing with the introduction of new warships, focusing on upgrading its navy fleet and weapons development as part of its military modernization drive. The country's comprehensive naval fleet includes submarines, aircraft carriers, cruisers, naval destroyers, and various support vessels.

Naval Vessels Market Growth in France

France demonstrates the highest growth potential in Europe with an anticipated CAGR of around 8% from 2024 to 2029. The country's naval sector benefits from continuous high-intensity combat exercises and regular maintenance and upgrade programs. France's commitment to maintaining a modern naval fleet is evident through various procurement initiatives and technological advancements. The country's focus on developing advanced naval capabilities and strengthening international defense cooperation continues to drive market growth.

Naval Vessels Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for naval vessels, characterized by increasing defense budgets and maritime security concerns. Countries like China, Japan, India, South Korea, Australia, and Singapore are actively expanding their naval capabilities in response to regional security challenges. The region's market is driven by territorial disputes, modernization of aging fleets, and the development of indigenous shipbuilding capabilities.

Naval Vessels Market in China

China maintains its position as the dominant force in the Asia-Pacific naval vessels market. The country's extensive shipbuilding capabilities and comprehensive naval modernization programs have established it as a major player in the region. China's focus on developing advanced naval vessels, including aircraft carriers, submarines, and naval destroyers, reflects its strategic maritime objectives and growing naval capabilities.

Naval Vessels Market Growth in Australia

Australia emerges as the fastest-growing market in the Asia-Pacific region. The country's commitment to strengthening its naval capabilities is evident through significant investments in fleet modernization and new vessel acquisitions. Australia's strategic focus on developing advanced naval capabilities and partnerships with major global defense contractors continues to drive market expansion.

Naval Vessels Market in Latin America

The Latin American naval vessels market is characterized by modernization efforts and indigenous shipbuilding initiatives across Brazil, Mexico, and other regional nations. Brazil emerges as the largest market in the region, while also demonstrating the strongest growth potential. The region's focus on coastal defense capabilities and maritime security drives the demand for various vessel types, from patrol boats to submarines.

Naval Vessels Market in Middle East & Africa

The Middle East & Africa region shows increasing investment in naval capabilities, particularly driven by maritime security concerns and offshore resource protection. Saudi Arabia represents the largest market in the region, while the United Arab Emirates shows significant growth potential. The region's focus on modernizing naval fleets and developing indigenous shipbuilding capabilities continues to shape market dynamics.

Get Analysis on Important Geographic Markets

Download PDF

Naval Combat Vessels Industry Overview

Top Companies in Naval Vessels Market

The naval vessels market is characterized by established players focusing on continuous innovation in vessel design, propulsion systems, and combat capabilities. Companies are investing heavily in advanced manufacturing technologies like 3D printing and robotics to improve production efficiency and reduce build times. Strategic partnerships and collaborations with technology providers are becoming increasingly common to develop next-generation naval platforms incorporating stealth features, autonomous capabilities, and integrated electric propulsion systems. Market leaders are expanding their capabilities in cybersecurity solutions and digital technologies while simultaneously strengthening their maintenance, modernization, and support service offerings. There is also a growing emphasis on developing environmentally sustainable vessels and green technologies to meet evolving international regulations and requirements.

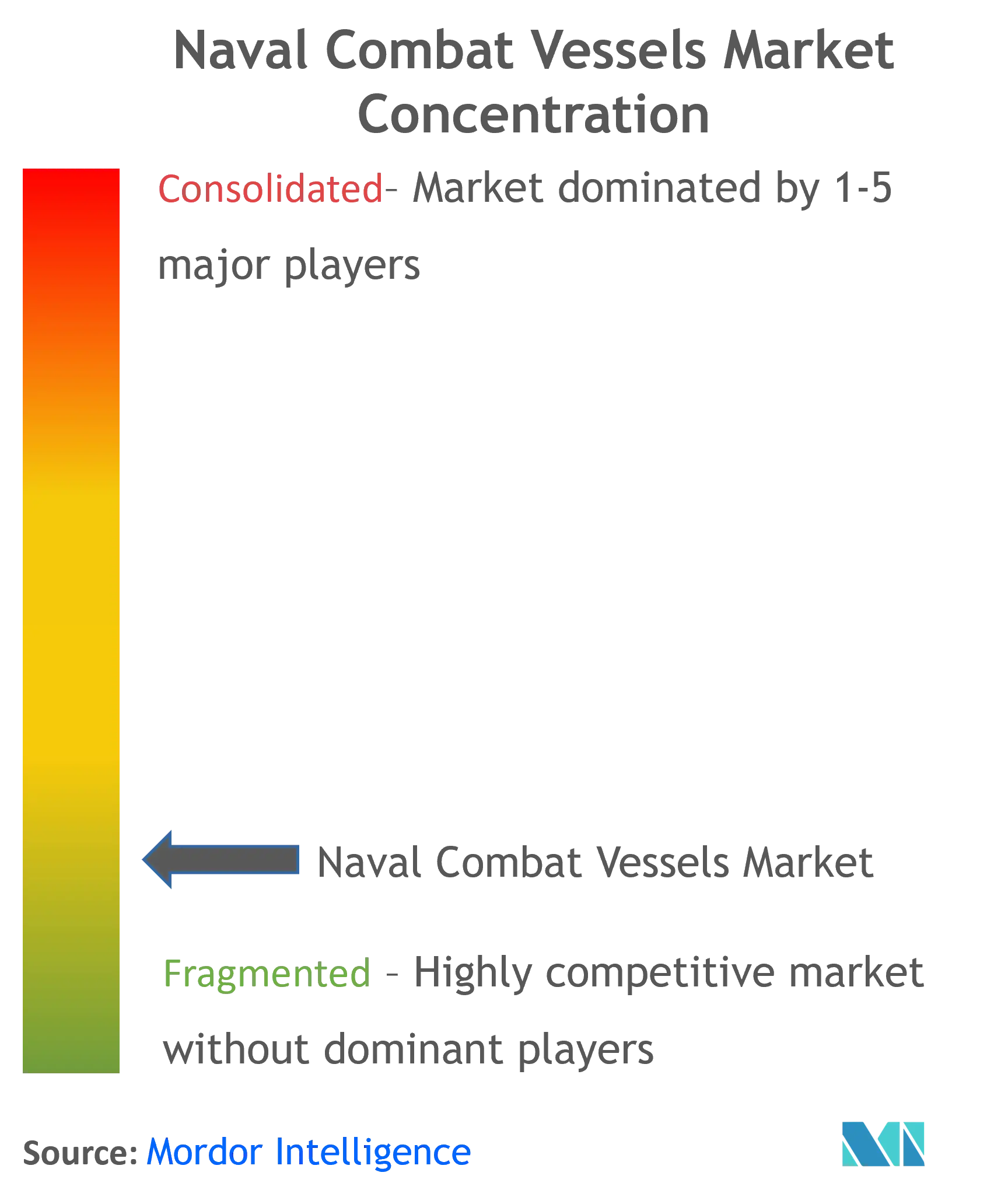

Market Structure Shows Strong Regional Players

The naval vessels market exhibits a mix of global defense conglomerates and specialized shipbuilding companies, with strong regional players dominating their respective domestic markets. Major players like General Dynamics Corporation, BAE Systems, and ThyssenKrupp maintain significant market presence through their established relationships with national defense forces and comprehensive vessel portfolios. These companies leverage their extensive experience, technical expertise, and established infrastructure to secure large-scale government contracts while continuously expanding their global footprint through strategic partnerships and local manufacturing facilities.

The market demonstrates moderate consolidation, with ongoing merger and acquisition activities focused on expanding technological capabilities and geographic reach. Companies are increasingly pursuing vertical integration strategies to strengthen their supply chains and reduce dependence on external suppliers. Regional players, particularly in Asia-Pacific, are gaining prominence through government support for indigenous shipbuilding capabilities and strategic partnerships with established global players for technology transfer and capability development. The industry also sees collaboration between shipyards and technology companies to integrate advanced systems and capabilities into military shipbuilding.

Innovation and Adaptability Drive Future Success

Success in the naval vessels market increasingly depends on companies' ability to innovate and adapt to evolving military requirements while maintaining cost competitiveness. Incumbent players must focus on developing modular and flexible vessel designs that can be easily upgraded with new technologies and weapons systems throughout their operational lifecycle. Companies need to invest in research and development to address emerging threats in areas such as cyber warfare, autonomous systems, and advanced sensor technologies while maintaining strong relationships with defense agencies and understanding their long-term strategic requirements.

Market contenders can gain ground by specializing in specific vessel types or technologies, developing unique capabilities that complement existing platforms, and forming strategic partnerships with established players. The high concentration of government buyers and the long-term nature of naval procurement programs create significant barriers to entry, making it essential for new entrants to demonstrate reliable performance and establish credibility through smaller contracts or specialized capabilities. Regulatory requirements regarding national security, export controls, and environmental compliance continue to shape market dynamics, while the risk of substitution remains low due to the specialized nature of military vessels and their critical role in national defense strategies.

Naval Combat Vessels Market Leaders

-

General Dynamics Corporation

-

Huntington Ingalls Industries Inc.

-

BAE Systems plc

-

Naval Group SA

-

ThyssenKrupp AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Naval Combat Vessels Market News

- April 2023: The UK Ministry of Defence awarded a USD 57 million contract to BAE Systems plc to support communication, command, control, computer, and intelligence (C4I) services for surface vessels. According to the contract, BAE Systems will likely be able to help with C4I services and data deliverables throughout the five phases of shipboard integration.

- March 2023: The Indian Navy contracted Goa Shipyard (GSL) and Garden Reach Shipbuilders & Engineers (GRSE) to produce 11 offshore patrol vessels and six next-generation missile vessels.

Naval Vessels Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Vessel Type

- 5.1.1 Destroyers

- 5.1.2 Frigates

- 5.1.3 Submarines

- 5.1.4 Corvettes

- 5.1.5 Aircraft Carriers

- 5.1.6 Other Vessel Types

-

5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Singapore

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 ThyssenKrupp AG

- 6.2.3 BAE Systems PLC

- 6.2.4 Naval Group SA

- 6.2.5 EDGE Group PJSC

- 6.2.6 Damen Shipyards Group

- 6.2.7 HD Korea Shipbuilding & Offshore Engineering Co. Ltd

- 6.2.8 Huntington Ingalls Industries Inc.

- 6.2.9 Lockheed Martin Corporation

- 6.2.10 Austal Limited

- 6.2.11 FINCANTIERI SpA

- 6.2.12 Hanwha Ocean (Hanwha Group)

- 6.2.13 LARSEN & TOUBRO LIMITED

- *List Not Exhaustive

-

6.3 Other Players

- 6.3.1 PT PAL Indonesia

- 6.3.2 Navantia SA SME

- 6.3.3 Kalashnikov Group

- 6.3.4 Fr. Lurssen Werft Gmbh & Co. KG

- 6.3.5 China State Shipbuilding Corporation Limited

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Naval Vessels Industry Segmentation

A naval combat vessel is a specialized watercraft operated by naval forces for military and security purposes. These vessels serve diverse roles, including defense, surveillance, and power projection at sea. They encompass various types, such as aircraft carriers, submarines, destroyers, and patrol boats, each designed for specific missions. Equipped with advanced weaponry and technology, naval vessels safeguard a nation's maritime interests and territorial waters, contributing significantly to its national security and defense strategy.

The naval combat vessels market is segmented by vessel type and geography. By vessel type, the market is segmented into destroyers, frigates, submarines, corvettes, aircraft carriers, and other vessel types (including amphibious warfare ships, littoral combat ships, mine countermeasure ships, and patrol ships). The report also covers the market sizes and forecasts for the naval combat vessels market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Vessel Type | Destroyers | ||

| Frigates | |||

| Submarines | |||

| Corvettes | |||

| Aircraft Carriers | |||

| Other Vessel Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Mexico | |||

| Rest of Latin America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Naval Vessels Market Research FAQs

How big is the Naval Vessels Market?

The Naval Vessels Market size is expected to reach USD 116.46 billion in 2025 and grow at a CAGR of 6.46% to reach USD 159.26 billion by 2030.

What is the current Naval Vessels Market size?

In 2025, the Naval Vessels Market size is expected to reach USD 116.46 billion.

Who are the key players in Naval Vessels Market?

General Dynamics Corporation, Huntington Ingalls Industries Inc., BAE Systems plc, Naval Group SA and ThyssenKrupp AG are the major companies operating in the Naval Vessels Market.

Which is the fastest growing region in Naval Vessels Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Naval Vessels Market?

In 2025, the North America accounts for the largest market share in Naval Vessels Market.

What years does this Naval Vessels Market cover, and what was the market size in 2024?

In 2024, the Naval Vessels Market size was estimated at USD 108.94 billion. The report covers the Naval Vessels Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Naval Vessels Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Naval Vessels Market Research

Mordor Intelligence offers a thorough analysis of the naval vessels industry. We leverage extensive expertise in the military shipbuilding and maritime defense sectors. Our research covers all major vessel categories, including submarines, aircraft carriers, naval destroyers, naval frigates, and naval corvettes. The report provides detailed insights into combat vessel technologies and naval combat systems. It also explores the evolving landscape of naval defense capabilities, such as coastal defense vessels and maritime patrol vessels.

Stakeholders in the military vessel and warship sectors can access our detailed report PDF, available for immediate download. This report covers crucial developments in naval ships construction and deployment. The analysis examines various vessel types, from military submarines to amphibious warfare ships and naval auxiliary ships, offering strategic insights for industry participants. Our comprehensive coverage of the submarine industry and military shipbuilding industry provides valuable intelligence for decision-makers involved in naval defense procurement and development programs.