| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 8.73 Billion |

| Market Size (2030) | USD 10.51 Billion |

| CAGR (2025 - 2030) | 3.78 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

NATO Ammunition Market Analysis

The NATO Ammunition Market size is estimated at USD 8.73 billion in 2025, and is expected to reach USD 10.51 billion by 2030, at a CAGR of 3.78% during the forecast period (2025-2030).

The NATO defense ammunition market continues to evolve amid significant defense spending increases across member nations, reflecting the growing emphasis on military preparedness and modernization. According to the Stockholm International Peace Research Institute, the United States maintained its position as the largest defense spender globally with USD 877 billion in 2022, followed by significant contributions from other NATO members, including the United Kingdom at USD 68.5 billion and France at USD 53.6 billion. This substantial financial commitment underscores the alliance's dedication to maintaining robust defense capabilities and ensuring adequate military ordnance stockpiles. The collective defense spending by NATO reached approximately USD 1,175 billion in 2022, with European members and Canada accounting for USD 364 billion of the total expenditure.

The ammunition manufacturing landscape is undergoing significant transformation as NATO members work to address production capacity constraints and supply chain vulnerabilities. The United States is actively expanding its production capabilities, with plans to increase monthly 155mm artillery shell production from 20,000 to 90,000 by 2025. Similarly, the European Union's combined annual capacity for large-caliber ammunition production stands at 650,000 rounds, with initiatives underway to enhance this capacity further. These expansion efforts are complemented by strategic partnerships and investments in manufacturing infrastructure to ensure sustainable supply chains of defense ammunition.

In June 2023, NATO announced a comprehensive Defense Production Action Plan designed to address ammunition stockpile shortfalls while enhancing interoperability among alliance members. This initiative has catalyzed several significant procurement programs, including the United Kingdom's USD 361 million contract with BAE Systems in July 2023 for munitions production, which aims to increase the country's 155mm artillery ammunition production capacity eightfold. These developments reflect a broader trend toward strengthening domestic production capabilities and reducing dependence on external suppliers.

The market is witnessing a shift toward more sophisticated ammunition technologies and production methods, with increased focus on precision-guided munitions and smart ammunition systems. The US Department of Defense's FY2024 budget request includes USD 30.6 billion for ammunition, marking a substantial increase of USD 5.8 billion above the FY2023 request, with significant allocations for tactical missiles, strategic missiles, and technology development. This investment pattern is mirrored across other NATO members, with the UK announcing a £5 billion increase in defense expenditure in March 2023, specifically targeting ammunition stockpile replenishment and advanced munitions development. The focus on enhancing military ordnance capabilities is evident in these strategic financial commitments.

NATO Ammunition Market Trends

Geopolitical Rift Driving Procurement of Weapons and Ammunition

The intensifying geopolitical tensions, particularly the ongoing Russia-Ukraine conflict since February 2022, have significantly accelerated defense ammunition procurement among NATO member states. According to NATO's defense expenditure data, the alliance spent around USD 1,175 billion in 2022, with Europe and Canada accounting for USD 364 billion of the total expenditure. This heightened focus on defense capabilities has led to several strategic initiatives, such as NATO's Defense Production Action Plan announced in June 2023, designed to rapidly address shortfalls in weaponry stockpiles while enhancing the interoperability of the alliance's munitions and equipment. The alliance has already implemented an active joint procurement program for 155mm shells worth USD 1 billion and has plans to procure several other weapons platforms and associated ammunition in the future.

The escalating security concerns have triggered substantial military ordnance procurement contracts across NATO nations. In July 2023, the United Kingdom awarded a USD 361 million contract to BAE Systems PLC for munitions, seeking to ramp up production to replenish its stockpiles and ensure supply for Ukraine. The contract allocates 68% of its value to fund 155mm artillery ammunition production, with the remaining designated for 30mm medium caliber rounds and 5.56mm ammunition. Similarly, in January 2023, Rheinmetall secured contracts worth USD 32.4 million to supply two European NATO member countries with 40mm ammunition, including up to 300,000 rounds of 40mm ammunition and 45,000 programmable cartridges in 40mm x 53 HV HE-T ABM caliber by June 2024. These developments underscore the growing emphasis on maintaining robust ammunition stockpiles in response to evolving security challenges.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancement in Weapons Technology Driving R&D of Ammunition

The evolution of modern warfare has catalyzed significant technological advancements in ammunition systems, particularly in precision guidance and smart ammunition capabilities. In 2024, the US Army plans to initiate the development of the XM1223 Multi-Mode Proximity Airburst (MMPA) munition with enhanced programmable capabilities specifically designed to engage and neutralize small unmanned aircraft systems. This advancement represents a significant leap in ammunition technology, incorporating sophisticated precision fuse systems that delay round detonation until target sensing. Additionally, the development of the Iron Sting by Israel Defense Force's Ground Forces and Elbit Systems, revealed in March 2021, showcases the industry's move towards networked precision fire systems that employ laser and GPS guidance to engage targets accurately while preventing collateral damage.

The industry is witnessing substantial investments in research and development focused on enhancing ammunition effectiveness and versatility. In February 2021, Rheinmetall Denel Munition formalized a ten-year agreement with Northrop Grumman to develop ammunition technology for future artillery operations, concentrating on precision-guided and enhanced-range artillery ammunition solutions by fitting 155mm artillery rounds with an integrated M1156 precision guidance kit. Furthermore, in February 2023, Saab Bofors Dynamics Switzerland unveiled a new 120mm round containing an innovative mix of shapes, materials, and fragmentation sizes, optimized for range and lethality. The THOR mortar round, with a range of approximately 8,500m, exemplifies the industry's focus on developing sophisticated defense ammunition that combines enhanced safety features with improved performance characteristics, particularly for mobile mortar systems due to its IM classification.

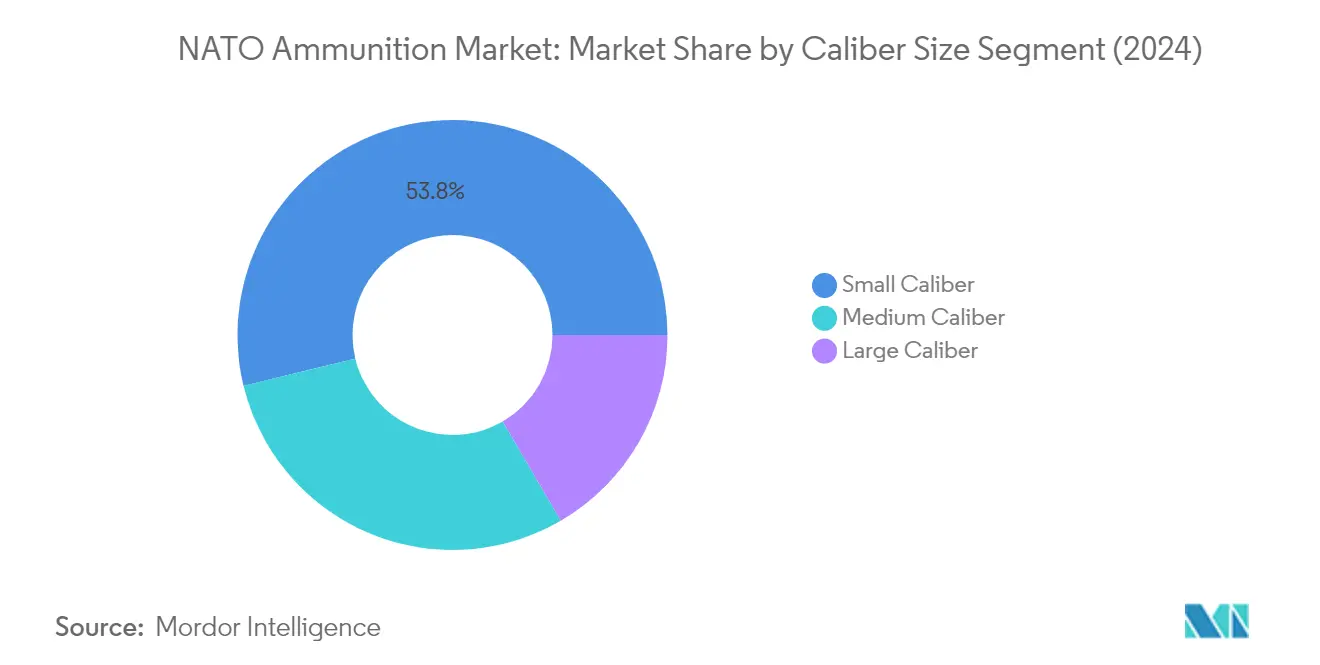

Segment Analysis: Caliber Size

Small Caliber Segment in NATO Ammunition Market

The small caliber segment continues to dominate the NATO ammunition market, commanding approximately 54% market share in 2024. This significant market position is primarily driven by the extensive use of small caliber defense ammunition in various military applications, including personal weapons, training purposes, and combat operations. The segment's dominance is further reinforced by the increasing focus on military modernization programs across NATO member countries, particularly in enhancing the capabilities of their ground forces through the induction of state-of-the-art small arms. The demand is particularly strong for ammunition types such as .50 caliber (12.7 mm), 5.56 mm, 7.62 mm, 9 mm, and other variants that are crucial for maintaining military readiness and supporting ongoing peacekeeping missions.

Medium Caliber Segment in NATO Ammunition Market

The medium caliber segment is projected to exhibit the fastest growth in the NATO ammunition market during 2024-2029, with an estimated CAGR of approximately 4%. This accelerated growth is primarily attributed to the increasing procurement of military aircraft, helicopters, infantry fighting vehicles (IFVs), and armored personnel carriers (APCs) equipped with medium caliber turret guns. The segment's growth is further bolstered by ongoing military modernization initiatives and the rising demand for military ordnance ranging from 20 mm to 60 mm, which is essential for various combat platforms. The expansion of production capabilities by key manufacturers and the development of advanced ammunition types with enhanced precision and effectiveness are also contributing to the segment's rapid growth trajectory.

Remaining Segments in Caliber Size

The large caliber segment, encompassing ammunition sizes from 60 mm and above, plays a crucial role in the NATO ammunition market by supporting heavy artillery and tank operations. This segment is characterized by ongoing technological advancements in precision guidance systems and the development of sophisticated defense ammunition types for modern combat vehicles and artillery systems. The segment's significance is underscored by the increasing focus on enhancing the accuracy and effectiveness of large caliber ammunition, particularly in addressing the evolving requirements of modern battlefield scenarios and the need for superior firepower in military operations.

Segment Analysis: Weapon Platform

Terrestrial Segment in NATO Ammunition Market

The terrestrial segment maintains its dominant position in the NATO ammunition market, commanding approximately 42% market share in 2024. This leadership position is primarily driven by substantial defense expenditure across various NATO countries focused on ground forces modernization. The increasing emphasis on upgrading armored vehicles and protecting ground troops in modern battlefield scenarios has led to significant investments in terrestrial defense ammunition. Major developments include the delivery of new armored personnel carriers to combat teams, upgrading of infantry fighting vehicles with enhanced firepower capabilities, and modernization of existing artillery systems. The segment's strength is further reinforced by ongoing efforts to enhance ground force capabilities through advanced ammunition technologies and improved battlefield effectiveness.

Aerial Segment in NATO Ammunition Market

The aerial segment is projected to demonstrate robust growth during the forecast period 2024-2029, driven by extensive fleet modernization programs and increasing procurement of next-generation combat aircraft across NATO nations. This growth trajectory is supported by significant developments in aerial military ordnance technology and increasing focus on air superiority. The segment's expansion is further bolstered by substantial contracts for fighter jets, including F-35 acquisitions, and the development of sixth-generation fighter programs. The increasing emphasis on aerial combat capabilities, coupled with the integration of advanced weapon systems and sophisticated ammunition types, positions this segment for sustained growth in the coming years.

Remaining Segments in Weapon Platform

The naval segment represents a crucial component of the NATO ammunition market, playing a vital role in maritime defense capabilities. This segment's significance is underlined by ongoing naval modernization programs across NATO member states, including the procurement of new frigates, combat ships, and patrol vessels. The segment's development is characterized by the integration of advanced naval gun systems and sophisticated ammunition types designed for maritime operations. Naval ammunition requirements continue to evolve with the modernization of naval fleets and the increasing focus on maritime security operations, contributing to the overall market dynamics.

NATO Ammunition Market Geography Segment Analysis

NATO Ammunition Market in United States

The United States continues to maintain its dominant position in the NATO ammunition market, commanding approximately 68% of the total market share in 2024. The country's market leadership is primarily driven by its substantial defense budget and comprehensive military modernization initiatives. The U.S. Department of Defense's strategic focus on enhancing defense ammunition stockpiles and developing next-generation weapon systems has created a robust demand environment. The country's emphasis on maintaining technological superiority through advanced ammunition development, including precision-guided munitions and smart ammunition systems, further strengthens its market position. The U.S. military's active participation in various NATO missions and international peacekeeping operations necessitates continuous ammunition procurement and stockpile maintenance. Additionally, the country's strong domestic ammunition manufacturing capabilities, supported by major defense contractors and extensive research and development facilities, contribute to its market dominance. The U.S. military's commitment to interoperability with NATO allies and its role in setting ammunition standards also reinforces its market leadership.

NATO Ammunition Market in Germany

Germany's NATO ammunition market is projected to grow at approximately 4% during 2024-2029, marking it as one of the most dynamic markets among NATO member states. The country's ammunition sector is experiencing significant transformation driven by its comprehensive military modernization program and increased defense spending commitments. Germany's focus on developing and procuring advanced military ordnance systems, particularly in medium and large caliber segments, demonstrates its commitment to enhancing military capabilities. The country's strong industrial base in ammunition manufacturing, led by companies like Rheinmetall, provides a solid foundation for market growth. Germany's strategic position in Central Europe and its role in NATO's eastern flank defense have led to increased investments in ammunition stockpiles and production capabilities. The country's emphasis on research and development in ammunition technology, particularly in areas such as precision-guided munitions and smart ammunition systems, positions it well for future growth. Furthermore, Germany's collaborative approach with other NATO members in ammunition development and procurement programs strengthens its market position.

NATO Ammunition Market in United Kingdom

The United Kingdom maintains a strong position in the NATO ammunition market, driven by its comprehensive defense modernization initiatives and strategic military requirements. The country's ammunition sector benefits from robust domestic manufacturing capabilities and significant investments in research and development. British defense forces' focus on maintaining high-readiness defense ammunition stockpiles and developing advanced munition technologies contributes to market growth. The UK's strategic emphasis on interoperability with NATO allies influences its ammunition procurement strategies and development programs. The country's defense industry, led by major manufacturers like BAE Systems, continues to innovate in areas such as precision-guided munitions and smart ammunition systems. The UK's commitment to maintaining its nuclear deterrent and conventional forces requires sustained investment in various ammunition types. Additionally, the country's focus on developing next-generation weapon systems drives demand for compatible ammunition solutions.

NATO Ammunition Market in France

France's position in the NATO ammunition market is characterized by its strong domestic defense industrial base and commitment to military modernization. The country's ammunition sector benefits from significant government support and investment in research and development activities. French defense forces' operational requirements, including overseas deployments and NATO commitments, drive sustained demand for various ammunition types. The country's emphasis on maintaining strategic autonomy in defense capabilities influences its ammunition procurement and development strategies. France's defense industry, with key players like Nexter Group, continues to innovate in ammunition technology, particularly in areas such as precision-guided munitions and artillery systems. The country's focus on developing next-generation weapon platforms creates opportunities for advanced military ordnance development. Additionally, France's collaborative approach with European partners in defense programs contributes to market development.

NATO Ammunition Market in Other Countries

The NATO ammunition market encompasses several other significant member states, each contributing uniquely to the alliance's collective defense capabilities. Countries like Italy, Canada, Poland, the Netherlands, and Spain demonstrate varying levels of market participation based on their defense requirements and industrial capabilities. These nations are actively investing in ammunition modernization programs and strengthening their domestic production capabilities. The focus on standardization and interoperability among NATO members drives collaboration in ammunition development and procurement. Many of these countries are enhancing their ammunition stockpiles and investing in advanced munition technologies to meet evolving security challenges. The emphasis on joint procurement programs and shared defense initiatives creates opportunities for market growth across these nations. Additionally, the increasing focus on developing indigenous ammunition manufacturing capabilities contributes to the overall market dynamics in these countries.

Get Analysis on Important Geographic Markets

Download PDF

NATO Ammunition Industry Overview

Top Companies in NATO Ammunition Market

The NATO ammunition market features prominent defense contractors who are continuously advancing their technological capabilities and manufacturing processes. Companies are investing heavily in research and development to create more precise, reliable, and sophisticated defense ammunition solutions, including smart munitions and precision-guided systems. The industry demonstrates strong operational agility through modernized production facilities and enhanced supply chain management to meet urgent military requirements. Strategic partnerships and collaborations with military organizations have become increasingly common to develop customized solutions and ensure long-term supply agreements. Market leaders are expanding their geographical presence through facility investments in NATO member countries, while also focusing on vertical integration to maintain better control over raw materials and component manufacturing processes.

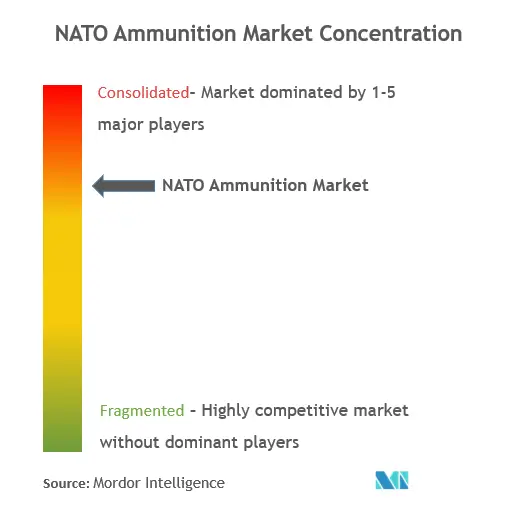

Consolidated Market Led by Defense Conglomerates

The NATO ammunition market exhibits a highly consolidated structure dominated by large defense conglomerates with diverse product portfolios and extensive manufacturing capabilities. These major players, including BAE Systems, Northrop Grumman, and General Dynamics, leverage their established relationships with military organizations and their ability to provide comprehensive defense solutions. The market demonstrates significant barriers to entry due to stringent regulatory requirements, high capital investments, and the need for specialized technological expertise. Regional specialists maintain their position through a focus on specific ammunition types or local market requirements.

The industry has witnessed strategic mergers and acquisitions aimed at expanding product portfolios, accessing new technologies, and strengthening market presence in key NATO regions. Companies are increasingly pursuing vertical integration strategies to secure supply chains and maintain quality control. The market structure favors established players who can meet the stringent quality standards, maintain necessary certifications, and demonstrate long-term reliability in ammunition production. Smaller specialized manufacturers often operate as strategic suppliers or partners to larger defense contractors, creating a complex network of interdependencies within the industry.

Innovation and Adaptability Drive Market Success

Success in the NATO ammunition market increasingly depends on companies' ability to innovate and adapt to evolving military requirements. Incumbent players must focus on developing advanced ammunition technologies, including precision-guided munitions and programmable ammunition, while maintaining cost competitiveness through efficient manufacturing processes. Companies need to establish strong research and development capabilities, maintain close relationships with military end-users, and demonstrate consistent quality and reliability in their products. The ability to quickly scale production in response to urgent requirements and maintain secure supply chains has become crucial for maintaining market position.

For contenders seeking to gain market share, specialization in niche ammunition types or focusing on specific regional markets presents viable opportunities. Success factors include developing innovative solutions for specific military applications, establishing strategic partnerships with established players, and maintaining strong compliance with NATO standards and regulations. The market's future trajectory is influenced by an increasing focus on interoperability among NATO forces, growing emphasis on environmental sustainability in ammunition production, and the need for advanced manufacturing technologies. Companies must also consider potential regulatory changes regarding ammunition specifications and environmental impact while maintaining flexibility to adapt to evolving geopolitical situations. The focus on innovation in military ordnance and adaptability ensures that companies remain competitive in this dynamic industry.

NATO Ammunition Market Leaders

-

Rheinmetall AG

-

Olin Corporation

-

General Dynamics Corporation

-

Northrop Grumman Corporation

-

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

NATO Ammunition Market News

July 2023: The UK government signed a contract worth GBP 280 million (USD 361.7 million) with BAE Systems PLC to replenish the British Army's frontline munitions. Under the agreement, the company will deliver vital defense stocks for the service, including 5.56-millimeter ammunition, 155-millimeter artillery shells, and 30-millimeter medium caliber rounds.

February 2023: Winchester, the small caliber ammunition manufacturer for the US military, announced that the US Army had awarded the company a contract to manufacture, test, and deliver 5 million 6.8mm Next Generation Squad Weapon (NGSW) cartridges.

NATO Ammunition Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Caliber Size

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

-

5.2 By Weapon Platform

- 5.2.1 Aerial

- 5.2.2 Terrestrial

- 5.2.3 Naval

-

5.3 By Geography

- 5.3.1 United States

- 5.3.2 United Kingdom

- 5.3.3 Canada

- 5.3.4 Italy

- 5.3.5 Germany

- 5.3.6 France

- 5.3.7 Rest of NATO Countries

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Olin Corporation

- 6.2.2 RUAG International Holding AG

- 6.2.3 Northrop Grumman Corporation

- 6.2.4 Global Ordnance LLC

- 6.2.5 CBC Global Ammunition

- 6.2.6 MESKO SA

- 6.2.7 Nammo AS

- 6.2.8 BAE Systems PLC

- 6.2.9 Rheinmetall AG

- 6.2.10 Nexter Groupe KNDS

- 6.2.11 General Dynamics Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

NATO Ammunition Industry Segmentation

Ammunition is a complete cartridge with components consisting of bullets or projectiles, cartridge cases, primers/caps, and propellants used in any small arm or light weapon. It is the material fired, scattered, dropped, or detonated from any weapon or weapon system. Different types of small, medium, and large ammunition are used based on the application.

The NATO ammunition market is segmented based on caliber size, weapon platform, and geography. By caliber size, the market is divided into small caliber, medium caliber, and large caliber. By weapon platform, it is classified into aerial, terrestrial, and naval. The report also offers the market sizes and forecasts for key NATO member nations. For each segment, the market sizing and forecasts have been done based on value (USD).

| By Caliber Size | Small |

| Medium | |

| Large | |

| By Weapon Platform | Aerial |

| Terrestrial | |

| Naval | |

| By Geography | United States |

| United Kingdom | |

| Canada | |

| Italy | |

| Germany | |

| France | |

| Rest of NATO Countries |

Need A Different Region or Segment?

Customize Now

NATO Ammunition Market Research FAQs

How big is the NATO Ammunition Market?

The NATO Ammunition Market size is expected to reach USD 8.73 billion in 2025 and grow at a CAGR of 3.78% to reach USD 10.51 billion by 2030.

What is the current NATO Ammunition Market size?

In 2025, the NATO Ammunition Market size is expected to reach USD 8.73 billion.

Who are the key players in NATO Ammunition Market?

Rheinmetall AG, Olin Corporation, General Dynamics Corporation, Northrop Grumman Corporation and BAE Systems plc are the major companies operating in the NATO Ammunition Market.

What years does this NATO Ammunition Market cover, and what was the market size in 2024?

In 2024, the NATO Ammunition Market size was estimated at USD 8.40 billion. The report covers the NATO Ammunition Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the NATO Ammunition Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

NATO Ammunition Market Research

Mordor Intelligence offers extensive expertise in analyzing the complex dynamics of military ordnance markets. We deliver comprehensive insights through detailed industry analysis. Our research team uses advanced methodologies to evaluate market trends, technological developments, and strategic initiatives across the NATO defense sector. The report provides an in-depth analysis of procurement patterns, manufacturing capabilities, and supply chain dynamics. It is available in an easy-to-download report PDF format.

Stakeholders in the defense ammunition sector gain valuable insights into NATO's ammunition standardization requirements, emerging technological innovations, and regional procurement trends. The report offers detailed forecasts, competitive landscape analysis, and strategic recommendations. This enables decision-makers to optimize their market positioning and operational strategies. Our analysis covers key factors influencing demand, regulatory frameworks, and technological advancements affecting NATO member states' ammunition requirements.