Naphtha Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

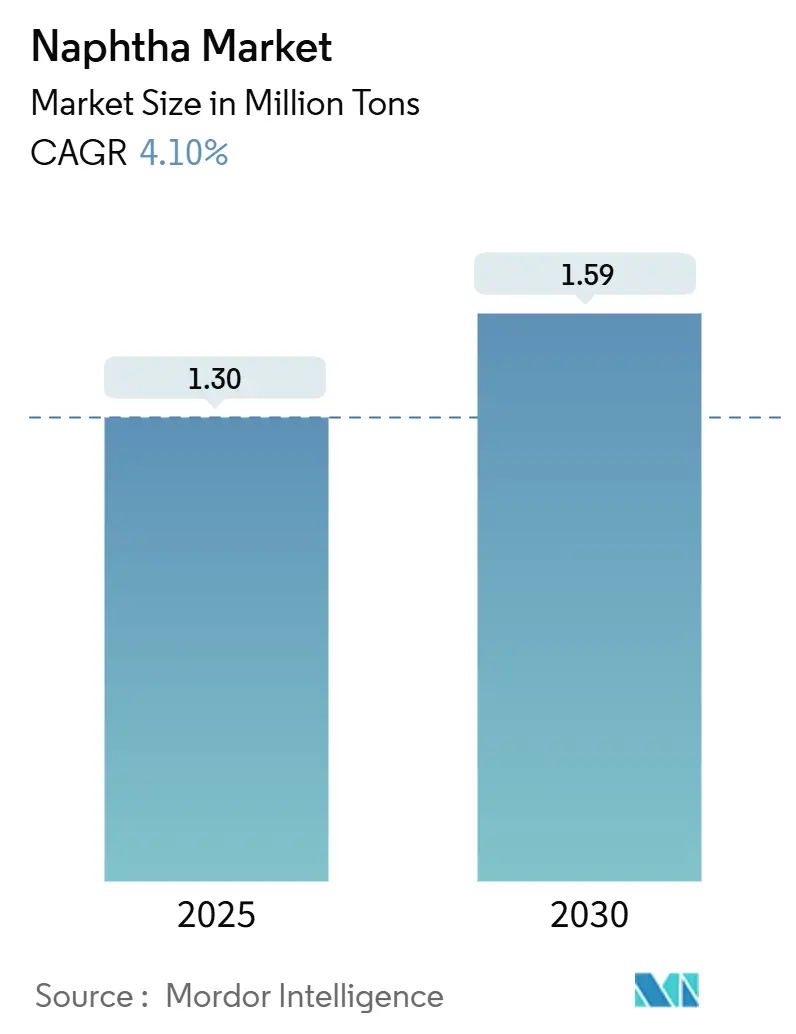

| Market Volume (2025) | 1.30 Million tons |

| Market Volume (2030) | 1.59 Million tons |

| Growth Rate (2025 - 2030) | 4.10% CAGR |

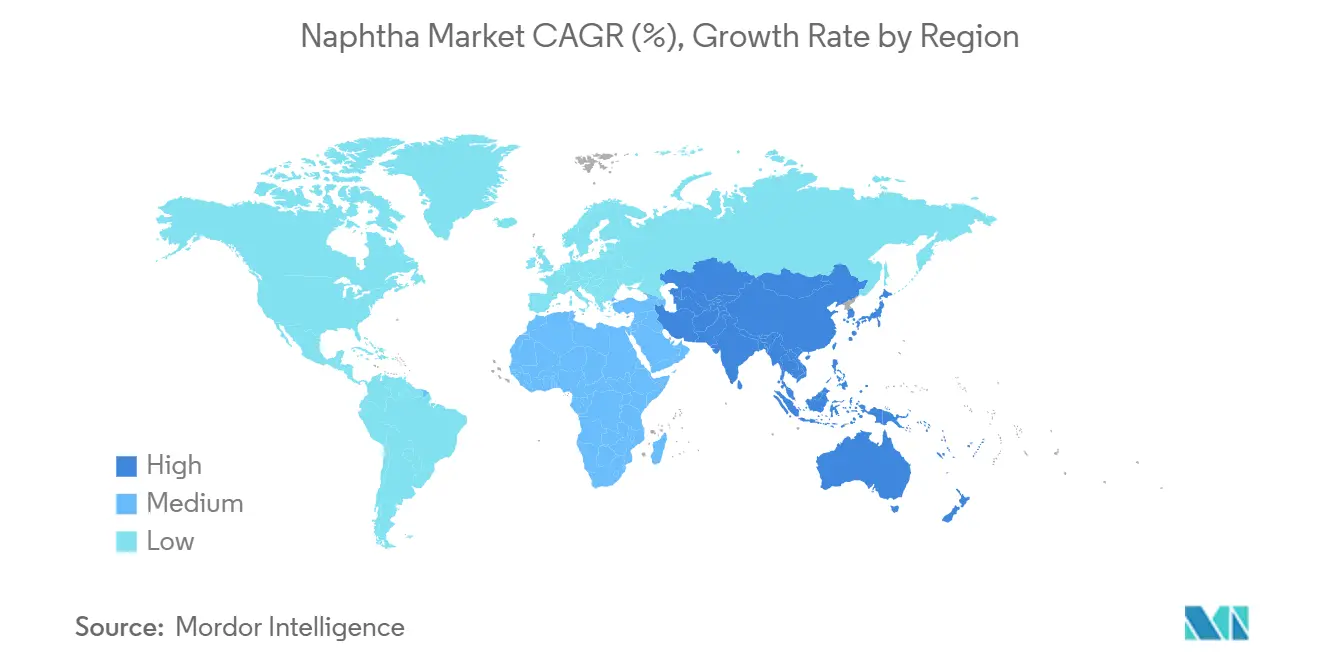

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Naphtha Market Analysis by Mordor Intelligence

The Naphtha Market size is estimated at 1.30 million tons in 2025, and is expected to reach 1.59 million tons by 2030, at a CAGR of 4.10% during the forecast period (2025-2030). Demand is anchored by naphtha’s role as the dominant petrochemical feedstock for olefins and aromatics, a position reinforced by large‐scale steam crackers that prefer light fractions for higher ethylene yields. Investments in condensate splitters along the U.S. Gulf Coast and new integrated refineries in Asia are reshaping global trade flows, while bio-naphtha capacity additions provide a complementary, low-carbon supply stream. Leading refiners integrate upstream crude supply with downstream petrochemical conversion to capture value across the chain. However, volatile crude–naphtha spreads, the growing appeal of natural gas liquids as alternative feedstocks, and increasingly stringent carbon regulations inject uncertainty into margin stability and capital-allocation decisions.

Key Report Takeaways

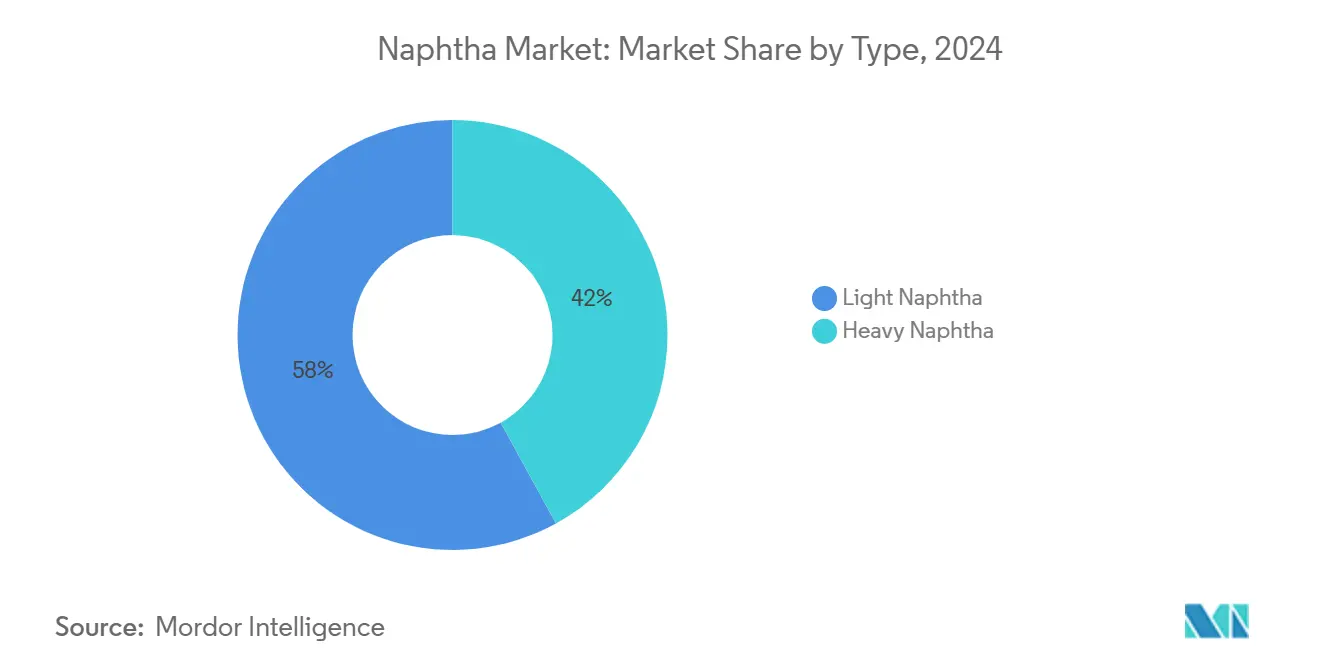

- By type, light naphtha captured 58% of the naphtha market share in 2024 and is set to post the fastest 4.80% CAGR to 2030.

- By source, refinery-derived grades retained 80% revenue share in 2024; bio-naphtha is projected to expand at a 5.70% CAGR through 2030.

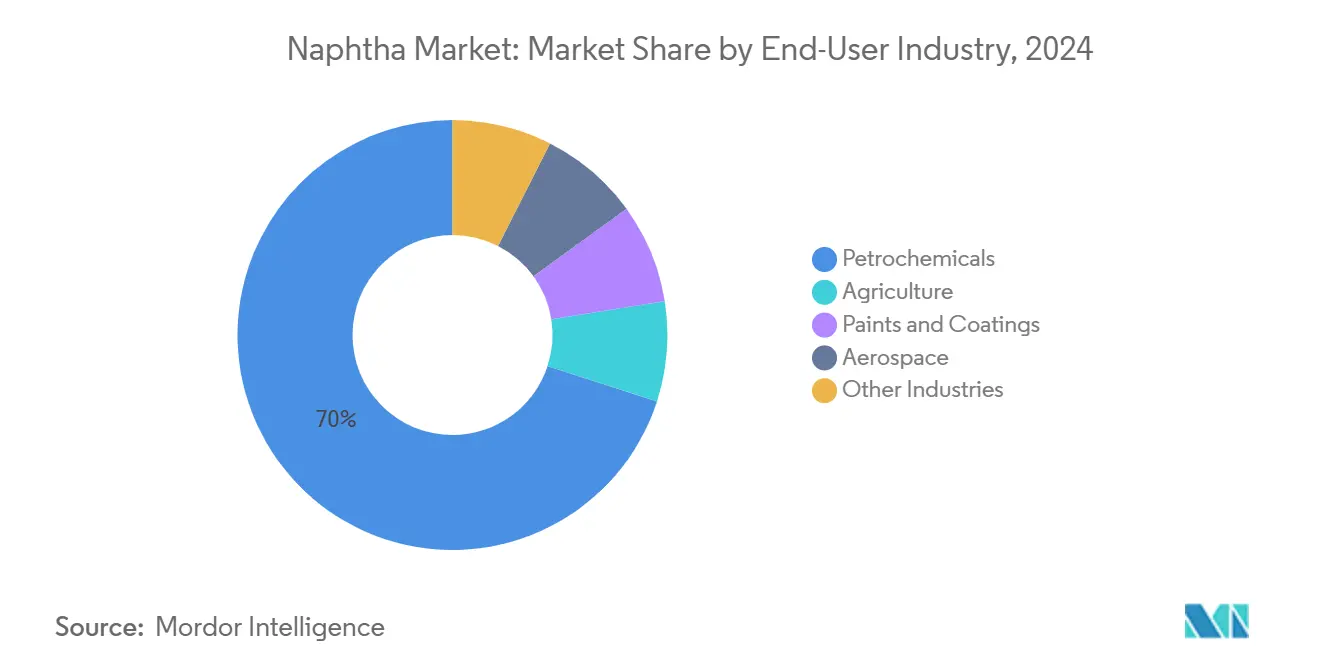

- By end-user industry, petrochemicals commanded 70% of the naphtha market size in 2024, and are projected to increase 4.60% annually to 2030.

- By region, Asia–Pacific held 44% of the naphtha market in 2024 and is advancing at a 4.9% CAGR to 2030.

Global Naphtha Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Olefins & Aromatics Feedstocks from Asian Steam Crackers | +1.20% | Asia-Pacific, with spillover to Middle East | Medium term (2-4 years) |

| Integration of Naphtha Reformers with Refinery Upgrading Projects in the Middle East | +0.80% | Middle East, with global export impact | Medium term (2-4 years) |

| Rising Demand for Fertilizers in India | +0.60% | India, with regional influence in South Asia | Short term (≤ 2 years) |

| Rising Investments in USGC Condensate Splitters Targeting Light Naphtha Output | +0.70% | North America, particularly US Gulf Coast | Medium term (2-4 years) |

| Bio-Naphtha Scale-up Backed by Renewable-Fuel Mandates | +0.30% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Olefins and Aromatics Feedstocks from Asian Steam Crackers

China is commissioning a wave of mega-crackers that elevate consumption of light naphtha because its paraffinic composition maximizes ethylene output. New capacity totaling 0.8–1.1 million b/d of refining throughput by 2028 is designed with integrated condensate splitters that raise naphtha yield ratios. Capacity additions at Hengli Petrochemical and Fujian Petrochemical will maintain upward demand momentum, translating into structurally higher imports of condensate-rich crudes and driving regional price alignment with the broader naphtha market. Supply security incentives are prompting long-term offtake agreements between Middle-East producers and Asian crackers, further knitting regional value chains. Net-back calculations suggest that each incremental steam cracker complex boosts regional light naphtha requirements by 1.5 million tons annually, underpinning the driver’s substantial contribution to overall growth.

Integration of Naphtha Reformers with Refinery Upgrading Projects in the Middle East

Bahrain’s Bapco Modernization Programme and Saudi Aramco’s USD 11 billion AMIRAL complex illustrate the strategic shift toward co-locating catalytic reformers with mixed-feed crackers to enhance gasoline octane and aromatic output[1]TotalEnergies, “Amiral Petrochemical Complex,” totalenergies.com . The model diverts straight-run naphtha that previously entered the motor-fuel pool into higher-margin petrochemical streams, improving overall refinery gross margins. Integration delivers energy-efficiency gains through shared utilities and furnishes flexible feedstock menus that dampen margin volatility. With AMIRAL alone requiring about 5 million tons of naphtha annually, the region becomes a swing supplier to Asia, tightening inter-regional balances and supporting a more robust naphtha market.

Rising Demand for Fertilizers in India

The Indian government’s capital allocation toward chemical and fertilizer capacity drives incremental ammonia plants that depend on naphtha in regions with limited gas pipeline coverage. Deepak Fertilisers’ 500 KTPA ammonia facility and 1,600 KTPA nitric acid expansion exemplify industry response. Coupled with expected 300% growth in industrial natural gas consumption by 2050, near-term naphtha demand rises as operators hedge against gas supply risks. Fertilizer-linked offtake agreements secure refinery disposition routes for heavy-to-medium naphtha grades, ensuring balanced utilization across refinery cut points. The incremental pull from India adds depth to the naphtha market, offsetting potential demand erosion elsewhere.

Bio-Naphtha Scale-up Backed by Renewable-Fuel Mandates

Legislated carbon-intensity reductions in Europe and North America are catalyzing investments in renewable diesel and sustainable aviation fuel units that co-produce bio-naphtha. UPM’s wood-based biorefinery in Finland produces 130,000 tons per year of renewable output, including a bio-naphtha stream that attracts premium pricing as a low-carbon petrochemical feedstock. U.S. SAF capacity is climbing from 2,000 b/d to nearly 30,000 b/d in 2025, implying a proportional gain in renewable naphtha coproduct volumes. Although the segment’s share is still modest, lifecycle carbon advantages and compatibility with existing crackers position bio-naphtha to secure dedicated offtake contracts with brand-conscious polymer producers. Early adopters lock in feedstock diversity and hedge regulatory risks, supporting long-term growth in the naphtha market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural Gas Liquid Demand in the United States | -0.90% | North America, with global market effects | Medium term (2-4 years) |

| Volatile Crude–Naphtha Spreads Undermining Crack Margins | -0.60% | Global, with pronounced impact in Europe and Asia | Short term (≤ 2 years) |

| Regulatory Push for Low-Carbon Alternatives & Recycled Feedstocks | -0.30% | Europe, North America, with gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude–Naphtha Spreads Undermining Crack Margins

Geopolitical incidents and refining capacity outages drive sharp swings in naphtha crack spreads, challenging refinery scheduling and prompting throughput cuts. An attack on a product tanker in the Gulf of Aden sent Asian naphtha cracks to a two-year high in early 2024, yet spreads retraced swiftly as arbitrage cargoes arrived. With post-2019 U.S. refinery capacity still 620,000 b/d below the peak, global supply buffers remain thin, magnifying volatility. This instability dampens refinery utilization rates by up to 8% in adverse periods and raises working-capital requirements for traders, tempering naphtha market expansion.

Regulatory Push for Low-Carbon Alternatives and Recycled Feedstocks

European Low Carbon Fuel mandates now recognize recycled carbon fuels, and the California LCFS includes incentives for chemically recycled feedstocks[2]ResourceWise, “UK Low Carbon Mandates Now Include Recycled Carbon Fuels,” resourcewise.com . This policy landscape accelerates investment in pyrolysis oil and hydrogenated vegetable oil, which compete with fossil naphtha in flexible crackers. While adoption is gradual, forward-looking polymer producers secure pilot volumes to meet recycled-content pledges, replacing conventional naphtha in select applications. Refiners respond with capital-light retrofits to process renewable intermediates, diverting capital away from conventional naphtha assets, and trimming aggregate demand growth over the long horizon.

Segment Analysis

By Type: Light Naphtha Drives Market Growth

Light naphtha generated 58% of the global naphtha market in 2024 as modern crackers favor its high paraffin content for superior ethylene yield. The segment is projected to grow at 4.80% CAGR to 2030, the briskest pace among cut types. Condensate splitter expansions in the United States and Asia are calibrated to produce paraffinic cuts that align with cracker slate requirements, reinforcing segment leadership in the naphtha market. Each 100,000 b/d splitter yields around 30,000 b/d of light naphtha, tightening balances and supporting premiums to gasoline-grade material. Integrated operators blend splitter streams with reformer output to hedge margin cycles and improve overall asset utilization.

Heavy naphtha lags with mid-single-digit growth owing to its higher aromatic content and lower ethylene productivity. Nonetheless, it remains an essential feedstock for catalytic reformers that upgrade octane and generate benzene, toluene, and xylenes. Investments in platinum-tin and platinum-rhenium bimetallic catalysts improve reformer severity tolerance, widening the processing window for heavier grades. Refiners leverage aromatics marketing agreements to monetize heavy cuts when gasoline spreads compress, preserving a supportive though less dynamic contribution to the naphtha market.

By Source: Bio-Naphtha Emerges as Growth Leader

Refinery-derived naphtha retained an 80% stake in the global naphtha market in 2024, benefiting from established logistics and integration within crude-based complex refineries. The naphtha market size for refinery grades is forecast to rise steadily, yet its share eases marginally as renewable alternatives claim incremental demand. Refiners invest in energy-efficiency retrofits, hydrogen management, and flare-gas recovery to lower embedded emissions, protecting the competitiveness of conventional supply.

Bio-naphtha, albeit from a low base, records the fastest 5.70% CAGR through 2030, buoyed by renewable diesel and SAF projects that co-produce paraffinic streams compatible with existing crackers. UPM’s EUR 175 million Lappeenranta plant validates commercial viability, while U.S. capacity linked to SAF output scales tenfold between 2024 and 2025[3]U.S. Energy Information Administration, “U.S. SAF Production Capacity to Grow,” eia.gov . Early adopters secure offtake agreements indexed to certified carbon-intensity premiums, providing visibility for project finance and accelerating the maturation of this emerging pillar of the naphtha market. Coal-and-gas-to-liquids sources maintain niche relevance in feedstock-rich geographies, although lifecycle-emission scrutiny caps their long-term expansion prospects.

By End-User Industry: Petrochemicals Maintain Market Leadership

The petrochemical segment consumed 70% of global naphtha in 2024, anchored by ethylene and propylene production via steam cracking. Eleven Indian naphtha or dual-feed cracker complexes deliver a combined ethylene capacity of 7.05 million tpa, illustrating the scale of demand growth across emerging economies. The naphtha market size allocated to petrochemicals is projected to climb at a 4.60% CAGR, sustained by downstream packaging, automotive, and construction applications. Crackers co-located with refineries capture energy and hydrogen synergies, lowering marginal production costs and ensuring resilience in cyclical downturns.

Agriculture, driven by ammonia and nitric acid production for fertilizers, serves as a significant outlet. In regions with constrained gas distribution, naphtha remains an indispensable hydrogen source for syngas units. Paints, coatings, aerospace fuels, and specialty chemicals fill the remainder of demand, each leveraging naphtha’s solvency or hydrocarbon chain attributes for niche performance criteria. Collectively, these sectors diversify end-use exposure and mitigate the impact of any single industry downturn on the broader naphtha market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia–Pacific led the naphtha market with 44% share in 2024, and its 4.90% forecast CAGR to 2030 stems from synchronized growth in petrochemicals and fertilizers. China processed a record 14.8 million b/d of crude in 2023, underpinning self-sufficiency in feedstocks, while India’s polymer demand is on track to hit 35 million tons by 2028. Aramco’s 10% stake in Hengli Petrochemical and the Fujian project further expand regional integration, aligning Middle-East supply with East-Asian demand growth.

North America remains structurally long light naphtha due to condensate splitter investments and rising shale liquids output. U.S. refining capacity climbed 2% in 2023, taking operable nameplate to 18.4 million b/d at the start of 2024. Yet surging NGL availability diverts petrochemical demand, moderating the regional naphtha market expansion pace. Export growth into Latin America and occasional arbitrage to Europe balances seasonal surpluses.

Europe’s naphtha demand contracts modestly as renewable fuel production displaces fossil feedstocks, but residual reformer capacity supplies aromatics chains and high-octane gasoline blendstocks. Refiners retrofit existing units for HVO and SAF rather than building greenfield assets, freeing investment for carbon-capture pilots that lower the embedded emissions of conventional naphtha. The Middle East capitalizes on integration projects that couple reformers and crackers, positioning itself as the marginal supplier into Asia and Europe when arbitrage windows open. South America and Africa gain influence through projects such as Nigeria’s Dangote refinery, which will produce up to 80 kbd of gasoline and naphtha, gradually transforming regional trade balances.

Competitive Landscape

The global naphtha market exhibits a highly fragmented concentration. Saudi Aramco exemplifies vertical integration by acquiring feedstock-secure stakes such as its 10% share of Hengli Petrochemical and a joint venture in the AMIRAL complex. These moves guarantee crude disposition and petrochemical offtake while diversifying regional exposure. TotalEnergies adopts a co-investment model, embedding mixed-feed crackers within its refinery system to capture upgrading margin and reduce carbon intensity.

Asia–Pacific players such as China Petrochemical Corporation pursue scale through greenfield capacity, leveraging domestic demand and state support to challenge incumbent exporters. Middle-East refiners emphasize export-oriented specialization, marketing reformate, aromatics, and light naphtha to Asia under long-term supply contracts that protect capacity utilization. Western super-majors concentrate on debottlenecking existing assets and adding splitter or hydrocracker flexibility rather than building new grassroots plants, reflecting capital discipline and energy-transition priorities.

Technological differentiation emerges around bio-naphtha and chemical recycling. Start-ups in pyrolysis oil upgrading collaborate with established refiners to blend recycled feedstocks into cracker slates. The competitive race increasingly hinges on securing low-carbon molecules, optimizing energy efficiency, and orchestrating balanced product portfolios that mitigate regulatory risks.

Naphtha Industry Leaders

-

BP p.l.c.

-

China Petrochemical Corporation

-

Exxon Mobil Corporation

-

Shell plc

-

Saudi Arabian Oil Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: QatarEnergy has entered into a landmark 20-year agreement with Shell to supply up to 18 million metric tons of naphtha. This long-term deal is expected to enhance supply stability and strengthen QatarEnergy's position in the global naphtha market, potentially influencing pricing dynamics and ensuring a reliable supply chain for downstream industries.

- January 2025: Indian Oil Corporation Ltd. signed a memorandum of understanding with the government of Odisha to develop a naphtha cracker project in the port town of Paradip, with an estimated investment of INR 61,000 crore. This project is expected to significantly enhance the naphtha market by increasing production capacity.

Global Naphtha Market Report Scope

Naphtha is a light flammable liquid containing a mixture of hydrocarbon molecules, typically between 5 and 10 carbon atoms. It mainly consists of straight-chain alkanes (paraffin), but it may also have cyclohexanes (naphthenes) and aromatics. The naphtha market is segmented by type, end-user industry, and region. By type, the market is segmented into light naphtha and heavy naphtha. By end-user industry, the market is segmented into petrochemical, agriculture, paints and coatings, aerospace, and other end-user industries. The report also covers the market size and forecasts for the naphtha market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (kilo metric tons).

| Light Naphtha |

| Heavy Naphtha |

| Refinery-Based |

| Bio-Naphtha |

| Others |

| Petrochemicals |

| Agriculture |

| Paints and Coatings |

| Aerospace |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Light Naphtha | |

| Heavy Naphtha | ||

| By Source | Refinery-Based | |

| Bio-Naphtha | ||

| Others | ||

| By End-user Industry | Petrochemicals | |

| Agriculture | ||

| Paints and Coatings | ||

| Aerospace | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the naphtha market?

The naphtha market is valued at 1.30 million tons in 2025 and is projected to reach 1.59 million tons by 2030.

Which segment holds the largest share of the naphtha market?

Light naphtha led with a 58% share in 2024 because it delivers the highest ethylene yield in steam crackers.

How fast is bio-naphtha expected to grow?

Bio-naphtha is forecast to expand at a 5.70% CAGR from 2025 to 2030, the fastest among all source categories.

Why is Asia–Pacific critical to naphtha demand?

Asia–Pacific commands 44% of global demand and continues to build steam crackers and integrated refineries that rely on naphtha feedstocks.

What are the main restraints on the naphtha market?

Substitution by low-cost natural gas liquids in the United States, volatile crude–naphtha spreads, and regulatory pressure for low-carbon alternatives restrain market growth.

Page last updated on: