Motor Starter Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 6.67 Billion |

| Market Size (2030) | USD 9.20 Billion |

| Growth Rate (2025 - 2030) | 6.67% CAGR |

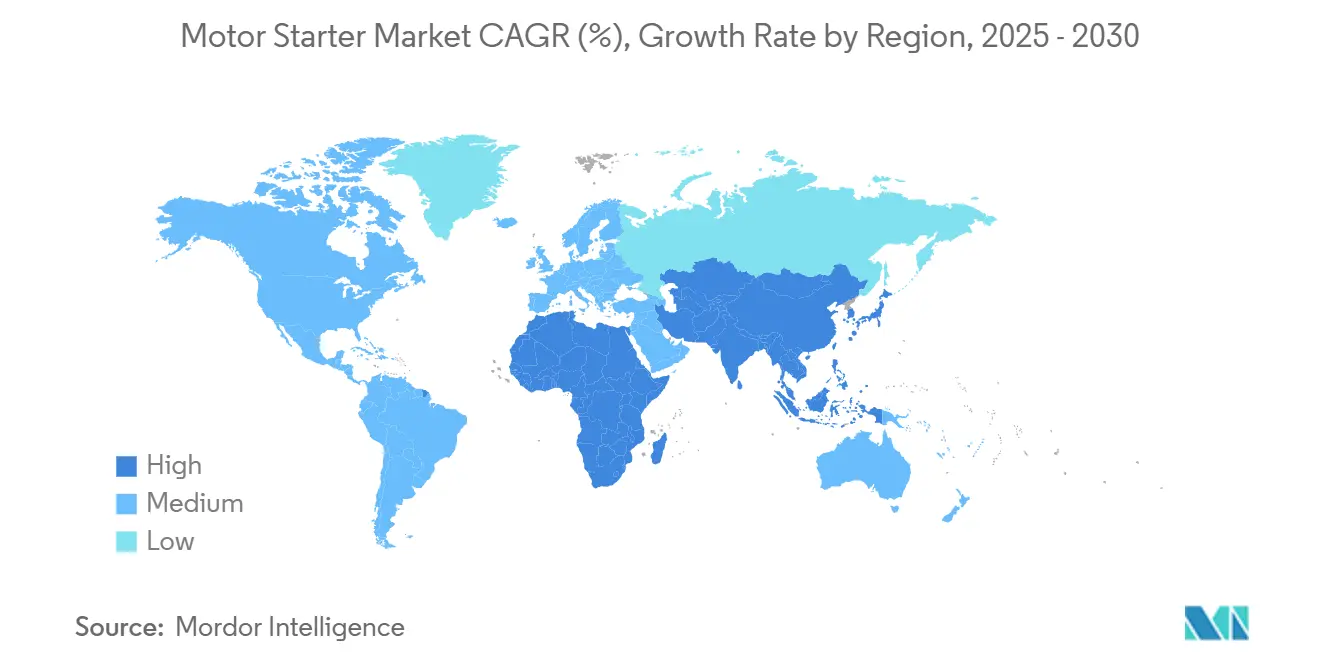

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Motor Starter Market Analysis by Mordor Intelligence

The Motor Starter Market size is estimated at USD 6.67 billion in 2025, and is expected to reach USD 9.20 billion by 2030, at a CAGR of 6.67% during the forecast period (2025-2030).

Market adoption accelerates on the back of strong industrial automation capital expenditures, fast-evolving motor efficiency mandates, and the rapid digitalization of process control. Accelerated investment originates from China’s 25% increase in capital equipment budgets, stringent European IE4 rules for motors with a capacity of 75-200 kW, and expanding water infrastructure outlays worldwide. Competitive strategies center on soft-starter innovation, IIoT integration, and regional capacity expansion to mitigate supply risk. The motor starter market also benefits from smart-city incentives that prioritize energy-efficient pumping and electrification projects in the mining and power generation sectors. However, volatile raw material prices, semiconductor shortages, and high cybersecurity expenditures in connected motor control centers are capping margins and prompting prudent inventory management.

Key Report Takeaways

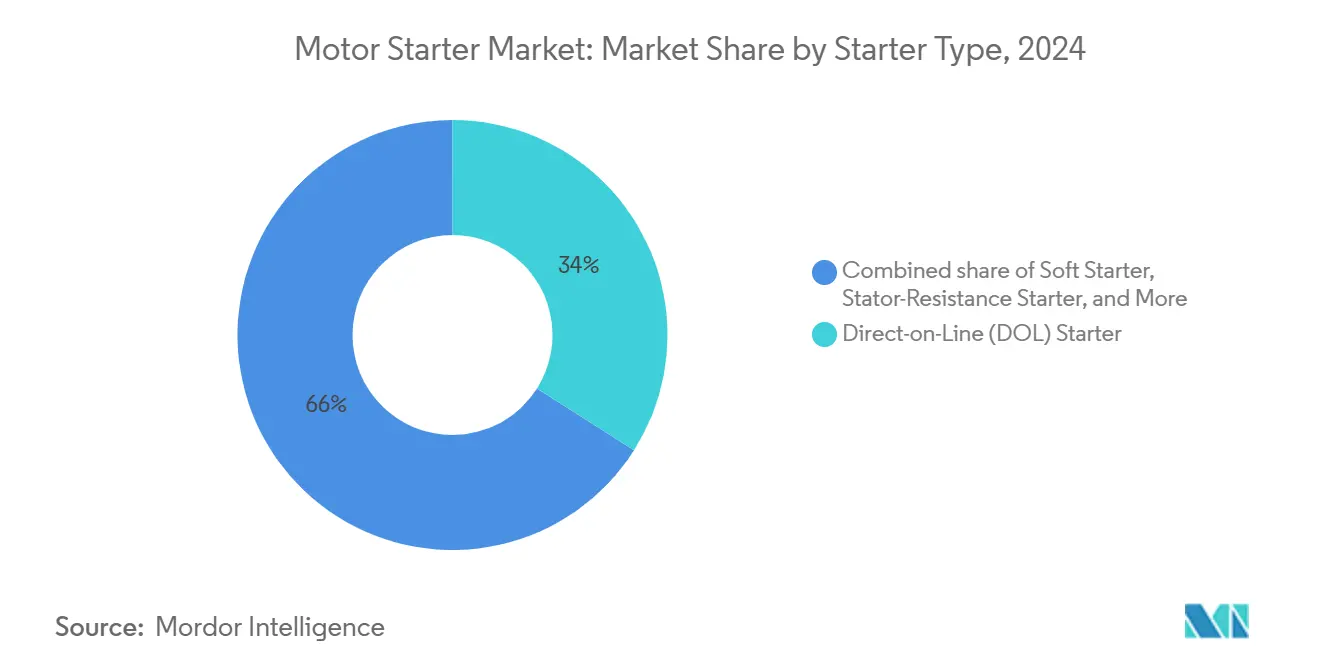

- By starter type, Direct-on-Line starters led with 34.0% of motor starter market share in 2024; soft starters are projected to post the highest 8.7% CAGR through 2030.

- By power rating, the up to 5 kW segment accounted for a 47.5% share of the motor starter market size in 2024, while the 5-50 kW band is forecast to advance at a 7.3% CAGR through 2030.

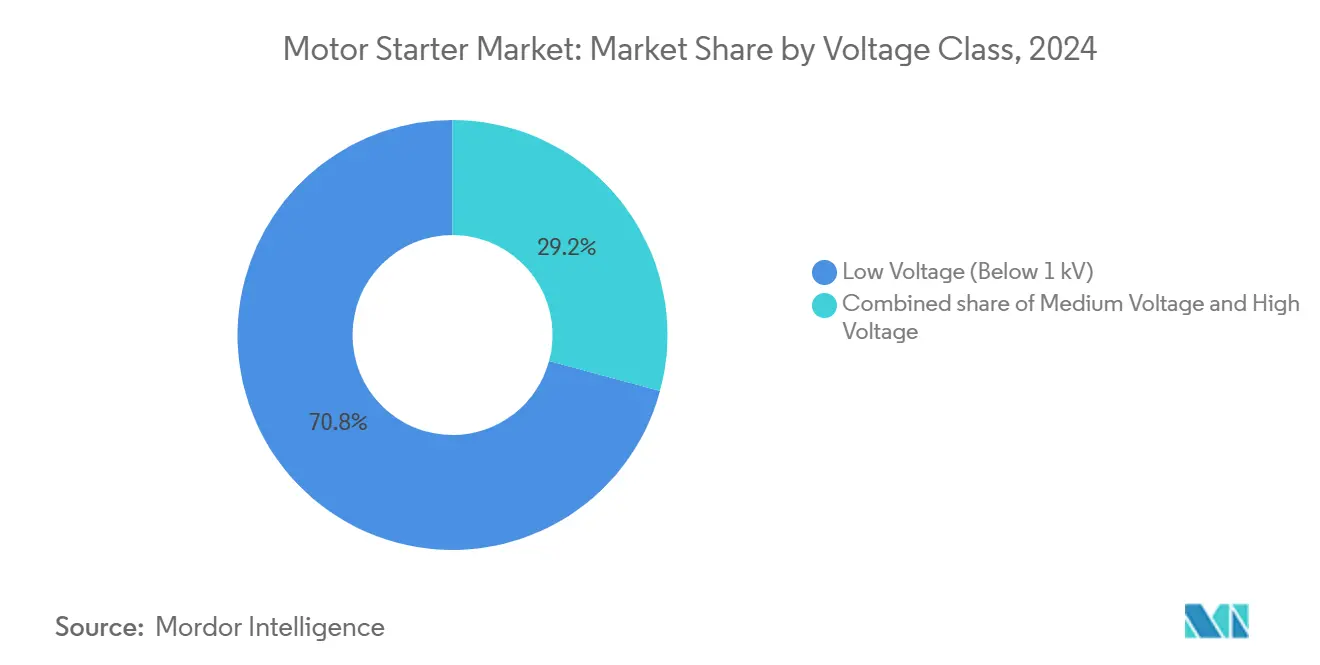

- By voltage class, low-voltage starters, which are below 1 kV, accounted for 70.8% of 2024 revenue; medium-voltage units are expected to expand at a 7.9% CAGR between 2025 and 2030.

- By end-user, manufacturing captured 24.2% of 2024 revenue, whereas water and wastewater treatment is set to grow at the fastest rate, with an 8.4% CAGR over the same horizon.

- By geography, Asia-Pacific commanded 43.6% of 2024 revenue and is on track for a 7.5% CAGR through 2030.

Global Motor Starter Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in industrial automation investments | 1.80% | Global, with APAC core leadership | Medium term (2-4 years) |

| Global energy-efficiency mandates for motors | 1.20% | EU & North America primary, expanding globally | Long term (≥ 4 years) |

| Expansion of water & wastewater infrastructure | 0.90% | Global, with emerging market focus | Long term (≥ 4 years) |

| Ageing power-plant modernisation programs | 0.70% | North America & EU primarily | Medium term (2-4 years) |

| IIoT-enabled soft-starter retrofit demand | 0.60% | Global, led by developed markets | Short term (≤ 2 years) |

| Electrification of heavy mobile mining equipment | 0.50% | APAC, MEA, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Industrial Automation Investments

Industrial automation budgets continue to rise as manufacturers seek to achieve labor productivity gains, enhance supply chain resilience, and integrate Industry 4.0. China’s five-year Action Plan targets 25% higher capital-equipment spending by 2027, while Thailand already operates 3,000 industrial robots across assembly lines and logistics cells.[1]Xinhua News Agency, “China Releases Five-Year Action Plan for Smart Manufacturing,” xinhuanet.com Rockwell Automation’s 2025 launch of the M100 electronic motor starter marks a shift toward intelligent point-on-wave switching, which reduces harmonic distortion and simplifies predictive analytics. Manufacturers such as Tenaris achieve more than 90% anomaly-prediction accuracy after installing ABB smart sensors on 460 motors, illustrating the quantifiable benefits of digital starters. As skilled labor shortages intensify, factories are prioritizing compact, digitally connected motor starters that reduce unplanned downtime, accelerate commissioning, and integrate with cloud-based MES platforms.

Global Energy-Efficiency Mandates for Motors

Regulations now demand premium-efficiency drive systems. The European Union’s Regulation 2019/1781 made IE4 ratings mandatory for motors with a power rating of 75-200 kW, starting in July 2023, affecting approximately 380 million installed units and targeting 110 TWh of annual savings by 2030. Singapore, Vietnam, and other ASEAN economies follow with IE3 or higher thresholds, creating an even broader base for retrofits. Siemens’ fully electronic e-Starter utilizes silicon-carbide MOSFETs to deliver 1,000 times faster short-circuit protection and minimal conduction losses. Premium efficiency skews the product mix toward electronically controlled soft starters, which enable smooth acceleration without inrush current spikes. Suppliers that align their portfolios with super-premium classes capture higher margins, while legacy electromechanical designs tend toward commoditization.

Expansion of Water & Wastewater Infrastructure

Governments are modernizing legacy treatment plants to meet population growth and climate-resilience goals. Brazilian utility Saneago achieved 25% energy savings by replacing mechanical starters with ABB integrated drive-starter packages across four pumping stations. Smart-city blueprints include real-time flow monitoring, which demands starters capable of variable torque optimization and remote diagnostics. Rockwell Automation’s Connected Enterprise reference architecture for water treatment combines IEC 61800-9 compliance, SIL-rated safety, and seamless SCADA integration. As utilities adopt predictive maintenance, sensor-rich soft starters that collect vibration and temperature data and feed it to cloud analytics are gaining traction.

Ageing Power-Plant Modernisation Programs

Thermal and hydroelectric plants require advanced motor control when repowered for grid stabilization roles. Eaton converts idle steam-turbine alternators into synchronous condensers, while ABB upgrades hydro units with digital speed-regulation and excitation packages. Such projects bring 20-year life-cycle contracts for high-reliability starters that withstand frequent cycling and fault-ride-through demands. Cleveland-Cliffs’ USD 150 million transformer plant underlines the downstream demand ripple in electrical balance-of-plant equipment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid substitution by variable-frequency drives | -1.40% | Global, particularly in developed markets | Short term (≤ 2 years) |

| Raw-material & semiconductor price volatility | -0.80% | Global supply chain impact | Medium term (2-4 years) |

| Cyber-security risks in connected MCCs | -0.60% | Developed markets with high IIoT adoption | Short term (≤ 2 years) |

| THD-limit regulations on electromechanical starters | -0.40% | North America & EU primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Substitution by Variable-Frequency Drives

VFD penetration erodes demand for traditional starters whenever variable speed and energy efficiency outweigh the simplicity of starters. Danfoss reports 60% energy savings in centrifugal pumps after VFD retrofits.[2] Danfoss A/S, “Energy Savings with VFDs in Pump Applications,” danfoss.com Natural Resources Canada concludes that drives outperform mechanical dampers, advancing torque control while slashing maintenance. Starter vendors respond by integrating soft-starter modes into hybrid drive-starter platforms, but pure speed-regulation applications still migrate to VFDs.

Cyber-Security Risks in Connected MCCs

Increased OT-IT convergence exposes motor control centers to ransomware and network-intrusion events. ARC Advisory Group warns that an average cyber-incident costs USD 1.1 million in immediate downtime and remedial expenses.[3]ARC Advisory Group, “OT Cybersecurity Incident Cost Analysis,” arcweb.com Compliance with IEC 62443 and NIST frameworks can increase product-development budgets and lengthen certification cycles.

Segment Analysis

By Starter Type: Soft Starters Drive Innovation

Soft starters contributed USD 2.12 billion to the motor starter market size in 2024 and are expected to outpace the overall 6.67% industry CAGR with 8.7% growth through 2030. Growth stems from IIoT functionality, torque control accuracy, and thermal management advantages that extend motor lifespan. Direct-on-line units still dominate constant-speed conveyors and HVAC blowers due to their low upfront cost and simple maintenance routines. Siemens’ November 2024 SIMATIC ET 200SP e-Starter validates the premium segment’s direction toward silicon-carbide power devices, offering a 1 µs short-circuit response and opening service windows for predictive analytics. Star-delta, autotransformer, and slip-ring starters remain relevant in heavy-torque lifts, though their combined share gradually declines as electronic soft starters add customizable ramp profiles. Across retrofit projects, soft-starter control modules integrate seamlessly with OPC UA gateways, providing machine builders with a single firmware environment—an attribute that drives procurement preference. By 2030, soft starters are projected to secure more than 40% of the motor starter market share as OEMs standardize on electronic solutions for modular production floors.

The mid-term engineering roadmap focuses on heat-dissipation materials, cybersecurity-hardened firmware, and embedded metrology that feeds real-time power-factor data to plant dashboards. Component obsolescence mitigation is also crucial; several vendors now guarantee 15-year product availability, aligning with typical machine replacement cycles. Bundled warranty services, including remote firmware updates, differentiate suppliers, especially in life-science packaging lines where validation downtimes are punitive. Such service-centric models enhance brand stickiness and annuity revenue streams, ensuring long-term dominance for innovators in the electronic-starter class.

Note: Segment shares of all individual segments available upon report purchase

By Power Rating: Mid-Range Motors Accelerate Growth

Motors with a capacity of up to 5 kW retained the largest 47.5% share of the motor starter market in 2024, generating USD 2.96 billion in revenue. Compact agricultural pumps, textile spindles, and refrigeration compressors constitute the bulk of installations. However, the 5-50 kW tier is forecast to expand at a 7.3% CAGR, elevating its contribution to nearly USD 3.1 billion by 2030. This tier dominates packaging machinery, intralogistics conveyors, and pharmaceutical granulators, where mid-range torque pairs with moderate current draw are utilized. Modular I/O cabinets have standardized slot heights around this range, facilitating faster field-retrofit swapping and encouraging OEM standardization.

Above 50 kW, high-torque applications, such as crusher mills and marine propulsion, form a niche but critical segment. Mitsubishi Electric’s XB-series HVIGBT module, rated 3.3 kV/1,500 A, lowers switching losses by 15% and improves inverter MTBF, underlining the technical push toward higher voltage build-outs. Vendors focusing here bundle condition-monitoring analytics that forecast bearing wear and torque ripple in real time. Custom busbar design, high-speed fuses, and arc-flash containment become key differentiators, driving premium ASPs and higher margins than the commoditized low-power range.

By Voltage Class: Medium Voltage Gains Momentum

Low-voltage equipment, defined as equipment with a voltage below 1 kV, accounted for 70.8% of 2024 revenue, primarily due to its widespread adoption in commercial buildings, food processing, and light assembly. Yet, the medium-voltage band (1-35 kV) is expected to drive growth, projected to contribute an incremental USD 1.1 billion to the motor starter market size by 2030. Mining electrification and utility-scale water pumping drive the uplift, necessitating starters with redundant SCR paths, synchronous detection, and arc-proof switchgear. ABB’s trolley-assist at Boliden’s Aitik mine highlights the robust duty cycle and energy-saving synergy achievable when pairing medium-voltage starters with regenerative braking.

High-voltage starters above 35 kV remain primarily limited to steel mills, oil-sands upgraders, and pumped-storage hydro facilities, but they deliver higher unit margins. IEC 60076-11 dry-type transformer compatibility, real-time partial-discharge monitoring, and forced-air ventilation packages define winning specifications. Suppliers focusing on medium- to high-voltage systems adopt modular shipping units, simplifying site erection and commissioning in remote geographies, such as Andean copper mines.

Note: Segment shares of all individual segments available upon report purchase

By End-user: Water Treatment Leads Growth

Manufacturing facilities drew USD 1.51 billion in initial purchases during 2024, but water and wastewater operations, representing USD 970 million, are expected to grow the fastest, surpassing USD 1.6 billion by 2030. The segment’s 8.4% CAGR is supported by stimulus-funded pipe replacement in North America and desalination in the Middle East. ABB’s success with Saneago’s Brazil project, delivering 25% energy savings, illustrates ROI-driven adoption cases. Meanwhile, mining operators are introducing ruggedized medium-voltage starters to power all-electric haul trucks, which dovetail with their corporate decarbonization pledges.

Food and beverage producers prioritize hygienic stainless-steel enclosures and IP69K wash-down starters. Oil and gas downstream installations require explosion-proof housings and SIL 2 or higher certification. Building services contractors specify starters with BACnet/IP capability to integrate directly into BMS dashboards, while pulp-and-paper mills favor units that can handle high inertia during thick-stock pump startup. Vendors who localize firmware language packs, offer modular cooling choices, and implement fieldbus protocols tailored to specific industries have captured higher customer lifetime values and reduced attrition.

Geography Analysis

The Asia-Pacific region sustained 43.6% of global revenue in 2024 and is expected to remain the largest region, thanks to its concentrated electronics, EV, and process-industry footprints. China’s policy to lift capital-equipment investment by 25% through 2027 supports continued soft-starter penetration in high-throughput production lines. India aims for manufacturing to contribute 25% of GDP by 2025, prompting accelerated greenfield factory construction that specifies IE3/IE4 compliant starters. ASEAN’s focus on EV clusters attracts Chinese OEMs, creating localized demand for motion-control systems throughout the stamping, painting, and final assembly processes.

North America embeds modern starters in data center cooling skids, modular switchgear for utility-scale battery farms, and ammonia compressors used in cold storage logistics. Aging thermal plants across the United States undergo synchronous-condenser repowering, driving medium-voltage starter replacement cycles with enhanced inertia-ride-through capability. Europe’s mandatory IE4 rules shift procurement toward premium-efficiency soft starters and hybrid drive-starter packages. Retrofit programs in Germany, France, and Scandinavia enhance digital monitoring requirements to offset skilled labor gaps and maintain OEE levels above 80%.

South America’s surge in copper and lithium mining in Chile and Peru underpins medium-voltage starter demand for pit-haul conveyors and gearless mills. Brazil’s water-utility upgrades pipeline booster stations with soft starters that integrate leakage-detection analytics, reducing non-revenue water loss. Middle East megaprojects, such as Saudi Arabia’s NEOM development and the UAE's desalination plants, necessitate stainless-steel starters capable of operating at 55 °C ambient temperatures and providing extreme dust ingress protection. Africa’s mining electrification in Botswana and Zambia promotes trolley-assist schemes, requiring robust starter cabinets resistant to vibration and abrasive dust.

Competitive Landscape

The motor starter market exhibits moderate concentration, with the top five vendors accounting for roughly 45-50% of the combined revenue. ABB, Schneider Electric, and Siemens rely on integrated portfolios, global service footprints, and aggressive R&D allocations topping 5% of sales to maintain a technological edge. Eaton and Rockwell Automation augment their portfolios through targeted acquisitions, such as Resilient Power Systems and solid-state transformer developers, which strengthen their digital power competencies.

KPS Capital’s EUR 3.5 billion takeover of Siemens’ Innomotics division reshapes the competitive map by spinning off a 15,000-employee motor-and-drive specialist able to allocate capex nimbly across emerging niches without the constraints of a large conglomerate. Meanwhile, ABB expanded its NEMA motor capability through the acquisition of Aurora Motors, cementing supply-chain resilience in vertical pump segments.

Strategic moves center on cloud-connected starter modules, cybersecurity certification, and silicon carbide adoption. Vendors now position themselves as lifecycle partners, bundling start-up commissioning, remote firmware updates, and vibration analytics subscriptions into equipment leases. Hybrid drive-starter platforms blur the line with low-voltage VFDs, allowing incumbents to hedge against substitution risk. The top players leverage manufacturing expansions—such as Schneider’s Tennessee switchgear plant or Mitsubishi Electric’s Kentucky compressor factory—to shorten lead times and localize designs for infrastructure-bill-funded projects. Partnerships with software analytics firms emerge as a tactic to inject AI-driven predictive maintenance, providing differentiation beyond hardware features.

Motor Starter Industry Leaders

-

Schneider Electric SE

-

Seimens AG

-

ABB Ltd

-

Rockwell Automation Inc.

-

Eaton Corp plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Standard Motor Products bought Kade Trading GmbH to enhance its European EV-compressor footprint.

- June 2025: Standard Motor Products completed its USD 108 million purchase of Trombetta, bringing power-switching solutions for off-highway EVs.

- April 2025: Rockwell Automation introduced the M100 electronic motor starter, featuring SIL3 point-on-wave switching, for food and beverage lines.

- January 2025: Hitachi acquired Joliet Electric Motors to expand maintenance services across North America.

Global Motor Starter Market Report Scope

A motor starter is an electrical device designed to start, control, and stop an electric motor safely. It regulates the initial current to the motor, preventing high inrush currents that can cause damage. In addition to starting the motor, it provides overload protection by automatically stopping the motor if it overheats or experiences other electrical issues.

The study tracks the revenue generated from the sale of motor starters by various manufacturers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates during the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The motor starter market is segmented by type (direct-on-line starter, stator resistance starter, slip ring starter, auto transformer starter, star delta starter, and soft starter), power rating (up to 5 kW, 5 - 50 kW, above 50 kW), end-user vertical (manufacturing, oil and gas, mining, water and wastewater treatment, automotive, food and beverage, and building and construction), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Direct-on-Line (DOL) Starter |

| Stator-Resistance Starter |

| Slip-Ring Starter |

| Autotransformer Starter |

| Star-Delta Starter |

| Soft Starter |

| Combination Starter |

| Up to 5 kW |

| 5 to 50 kW |

| Above 50 kW |

| Low Voltage (Below 1 kV) |

| Medium Voltage (1 to 35 kV) |

| High Voltage (Above 35 kV) |

| Manufacturing |

| Oil and Gas |

| Mining |

| Water and Wastewater Treatment |

| Automotive |

| Food and Beverage |

| Building and Construction |

| Power Generation and Utilities |

| HVAC and Refrigeration |

| Pulp and Paper |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia & New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Starter Type | Direct-on-Line (DOL) Starter | |

| Stator-Resistance Starter | ||

| Slip-Ring Starter | ||

| Autotransformer Starter | ||

| Star-Delta Starter | ||

| Soft Starter | ||

| Combination Starter | ||

| By Power Rating | Up to 5 kW | |

| 5 to 50 kW | ||

| Above 50 kW | ||

| By Voltage Class | Low Voltage (Below 1 kV) | |

| Medium Voltage (1 to 35 kV) | ||

| High Voltage (Above 35 kV) | ||

| By End-user | Manufacturing | |

| Oil and Gas | ||

| Mining | ||

| Water and Wastewater Treatment | ||

| Automotive | ||

| Food and Beverage | ||

| Building and Construction | ||

| Power Generation and Utilities | ||

| HVAC and Refrigeration | ||

| Pulp and Paper | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the motor starter market?

The motor starter market size stood at USD 6.67 billion in 2025 and is projected to reach USD 9.20 billion by 2030.

Which starter type is growing fastest?

Soft starters are expanding at an 8.7% CAGR due to IIoT integration and energy-efficiency benefits, outpacing other starter categories.

Why is Asia-Pacific the largest regional market?

Asia-Pacific benefits from concentrated manufacturing bases in China and India, automation incentives, and accelerated EV production, giving it 43.6% revenue share in 2024.

What challenges do manufacturers face?

Key headwinds include variable-frequency drive substitution, raw-material price swings, semiconductor shortages, and rising cybersecurity costs in connected motor control centers.

How are energy-efficiency regulations shaping demand?

Mandatory IE4 standards in the EU and rising IE3 norms in Asia push demand toward electronic soft starters that support premium-efficiency motors.

What is the outlook for medium-voltage starters?

Medium-voltage units are forecast to post a 7.9% CAGR as mining electrification and power-generation upgrades require advanced protection and digital monitoring capabilities.

Page last updated on: