| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 15.57 Billion |

| Market Size (2030) | USD 19.57 Billion |

| CAGR (2025 - 2030) | 4.67 % |

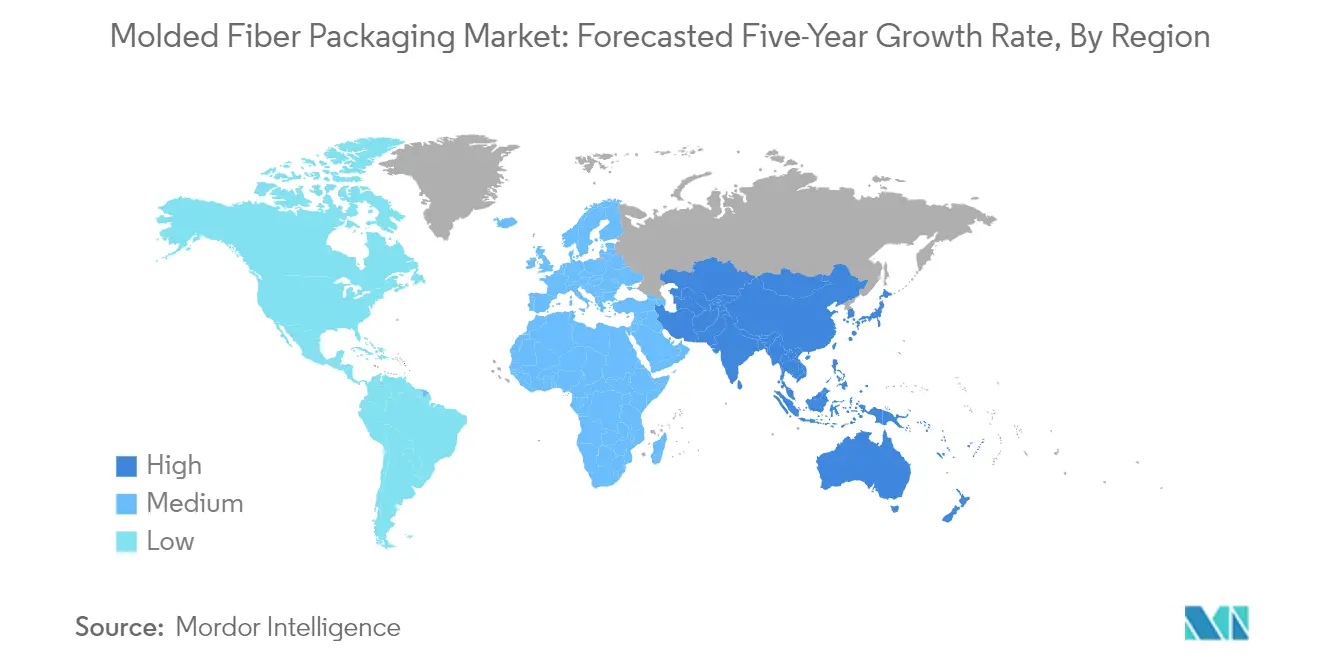

| Fastest Growing Market | Europe |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Molded Fiber Packaging Market Analysis

The Molded Fiber Packaging Market size is worth USD 15.57 Billion in 2025, growing at an 4.67% CAGR and is forecast to hit USD 19.57 Billion by 2030.

The molded fiber packaging industry is experiencing significant transformation driven by technological advancements and manufacturing innovations. Companies are increasingly adopting advanced manufacturing technologies like Dry Molded Fiber Technology (DMF) to enhance production efficiency and product quality. This trend is evidenced by several major developments in 2023, including Matrix Pack's launch of innovative hot and cold beverage closure solutions using DMF technology, and TekniPlex's announcement of a new 200,000 square foot specialty molded fiber manufacturing facility in Ohio. The integration of automation and digital technologies in production processes has enabled manufacturers to achieve higher precision, consistency, and scalability in their operations.

The industry is witnessing a remarkable shift in consumer behavior and preferences regarding sustainable packaging solutions. According to Hanchett Paper Company's Sustainable Packaging Consumer Report 2022, 76% of surveyed shoppers in the United States made a conscious effort to buy more sustainable products in the previous year. This changing consumer mindset has prompted manufacturers to innovate and expand their product portfolios. The trend is particularly evident in the food service sector, where companies are developing new solutions for disposable items like cups, plates, and food containers that maintain functionality while meeting sustainability requirements.

Global expansion and strategic partnerships are reshaping the competitive landscape of the molded fiber packaging market. In 2023, significant developments included HZ Green Pulp becoming Malaysia's first DMF manufacturer and Nippon Molding securing its position as Japan's first DMF licensee. These expansions reflect the industry's growing geographical footprint and the increasing adoption of sustainable packaging solutions across different regions. Companies are forming strategic alliances to combine technological expertise with local market knowledge, creating more efficient and sustainable fiber packaging solutions.

The market is experiencing substantial growth in various end-user industries, particularly in the electronics and food retail sectors. According to the Consumer Technology Association, retail sales of consumer electronics in the United States are projected to reach USD 485 billion in 2023, indicating a strong demand for protective packaging solutions. In the food retail sector, the Gulf Cooperation Council countries are expected to see sales grow to USD 216.3 billion by 2026, highlighting the increasing need for sustainable food packaging solutions. This growth in end-user industries is driving innovation in molded fiber packaging design and functionality, particularly in areas requiring specialized protection and preservation capabilities.

Molded Fiber Packaging Market Trends

Shift in Consumer Preference Toward Recyclable and Eco-friendly Materials

The growing environmental consciousness among consumers has fundamentally transformed packaging preferences, with over 83% of younger consumers (aged 44 and under) expressing a willingness to pay premium prices for products utilizing sustainable packaging solutions in 2022. This shift in consumer behavior has prompted manufacturers to reimagine their packaging strategies, particularly in the food service sector where molded fiber products are increasingly replacing traditional plastic materials in applications such as clamshell containers, takeout meal containers, egg cartons, and fruit trays. The enhanced barrier properties of modern molded fiber packaging, which effectively regulate gas and water vapor exchange to preserve food quality, have further accelerated this transition toward eco-friendly alternatives.

According to a 2022 sustainable packaging consumer report by Hanchett Paper Company, 76% of surveyed shoppers made conscious efforts to purchase more sustainable products in the previous year, while 77% expect brands and retailers to transition to 100% sustainable packaging solutions in the near future. This consumer-driven transformation has catalyzed innovation in the industry, with manufacturers developing advanced molded fiber products that not only meet environmental objectives but also deliver superior performance in terms of strength, thermal properties, and barrier protection. The industry's commitment to sustainability is further evidenced by the increasing utilization of diverse raw materials, including non-wood sources such as bamboo, sugarcane, wheat straw, and other agricultural residues, which contribute to a more circular and environmentally responsible packaging ecosystem.

Understand The Key Trends Shaping This Market

Download PDF

Growing Disposable Income

The correlation between rising disposable income and sustainable packaging adoption has become increasingly evident, as consumers with greater purchasing power demonstrate a stronger inclination toward environmentally responsible products. According to an Ipsos survey conducted in August 2022, while 40% of global consumers anticipated a decline in disposable income, 25% expected an increase, indicating a significant segment of consumers maintaining or improving their purchasing capacity. This economic dynamic has enabled consumers to prioritize environmental considerations in their purchasing decisions, particularly in the packaging sector where premium sustainable solutions are gaining traction.

The impact of disposable income on packaging choices is further reinforced by the substantial growth in retail sales, with the United States recording retail sales of USD 7,096.88 billion in 2022, representing a significant increase from USD 5,040.21 billion in 2017. This growth in retail spending has been accompanied by a heightened emphasis on sustainable packaging solutions, as consumers increasingly leverage their spending power to support environmentally responsible practices. The trend is particularly pronounced in the food and beverage sector, where molded fiber food packaging has emerged as a preferred alternative for applications ranging from egg cartons to wine bottle protection, reflecting consumers' willingness to invest in sustainable packaging solutions that align with their environmental values.

Augmented Demand for Reusable and Sustainable Packaging from End-Users

The escalating demand for sustainable packaging solutions from end-users has catalyzed significant innovations in the fiber-based packaging market, particularly in sectors such as food service, electronics, and healthcare. Organizations such as the European Organization for Packaging and the Environment (EUROPEN) and the UK-based Industry Council for Packaging and the Environment (INCPEN) have been instrumental in establishing effective practices for recyclable and reusable materials manufacturing, driving the industry toward more sustainable solutions. This institutional support, combined with technological advancements in manufacturing processes, has enabled the development of more robust, smoother products that effectively compete with traditional plastic packaging in terms of both functionality and aesthetic appeal.

The transformation in end-user preferences is particularly evident in the food packaging sector, where barrier properties and sustainability requirements have driven significant innovations. Modern fiber packaging solutions now offer enhanced flexibility, rigidity, water and oil resistance, air permeability, and hygroscopic capabilities, making them excellent alternatives to plastic food packaging. This evolution has been further supported by major brands' commitment to sustainability, with companies developing various types of green and sustainable packaging solutions to meet the growing demand from environmentally conscious end-users. The industry's response to this demand is exemplified by recent innovations in manufacturing processes that have improved the quality and versatility of molded fiber packaging products while maintaining their fundamental environmental benefits.

Segment Analysis: By Type

Transfer Segment in Molded Fiber Packaging Market

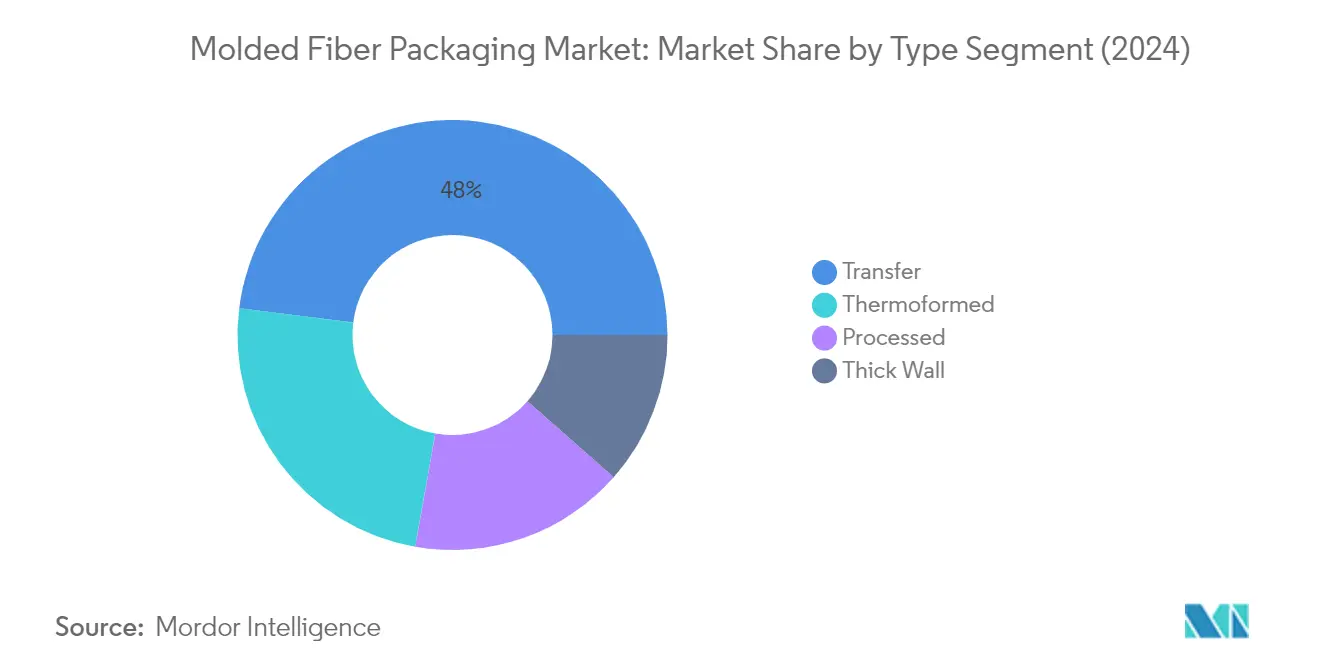

The transfer segment dominates the molded fiber packaging market, commanding approximately 48% market share in 2024, driven by its extensive application in various consumer goods and food & beverage packaging. Transfer molding, similar to precision molding, offers finished surfaces on both sides as the pulp transfers between molds, making it ideal for egg cartons, electronics packaging, and hospital disposables. The segment's popularity stems from its ability to provide neat product presentation, well-structured protection, and enhanced shelf life. The material's wall thickness of around 1/8 to 3/16 inches (3mm to 5mm) offers strong cushioning properties that prevent surface scratches and abrasions, particularly beneficial for electronic appliances during transportation. The segment's growth is further propelled by increasing adoption in food service disposables, appliances, office equipment, and tableware applications.

Transfer Segment Growth Trajectory in Molded Fiber Packaging Market

The transfer segment is projected to maintain its market leadership position with the highest growth rate of approximately 5% during 2024-2029. This accelerated growth is attributed to the increasing demand for sustainable molded fiber packaging solutions across various industries. The segment's growth is particularly driven by the rising adoption of transfer molded fiber trays in electronics packaging, where protection against changing weather, humidity, and dust is crucial. Organizations worldwide are embracing transfer molded fiber packaging to maintain sustainability, with many manufacturers investing in advanced manufacturing technologies and innovative solutions. The segment's expansion is further supported by its versatility in creating various designs for electronic products such as cell phones and DVD players, along with its applications in hospital disposables and appliance packaging.

Remaining Segments in Molded Fiber Packaging Market by Type

The thermoformed, processed, and thick wall segments complete the molded fiber packaging market landscape, each serving distinct applications and industries. Thermoformed fiber, produced using multiple heated molds, offers smooth surfaces and detailed shapes with minimal draft, making it particularly suitable for luxury packaging applications. The processed segment undergoes additional treatments such as dyeing, coating, and hot pressing, providing customization options for various end-use applications. Thick wall molded fiber, with its robust construction and superior strength, serves heavy-duty packaging needs, particularly in industrial applications and for protecting heavier items during transportation. These segments collectively contribute to the market's diversity and ability to meet varied packaging requirements across different industries.

Segment Analysis: By Format Type

Wet Segment in Molded Fiber Packaging Market

The wet format type segment dominates the global molded fiber packaging market, commanding approximately 89% market share in 2024. This substantial market presence is attributed to its widespread adoption in luxury goods and brand-name products due to its superior quality and finish. The wet molding process, which involves adding suitable additives to fiber of certain consistency to form wet fiber through adsorption, offers high production efficiency particularly for eco-friendly cutlery and tableware manufacturing. Products manufactured through wet processing demonstrate smooth, delicate, and attractive surfaces, with thinner walls and higher density that save space. The segment's prominence is further reinforced by its versatility in food packaging, delicate industrial packaging, and various other paper-molded products, making it the preferred choice for manufacturers seeking sustainable packaging solutions.

Dry Segment in Molded Fiber Packaging Market

The dry format type segment is emerging as the fastest-growing segment in the molded fiber packaging market, projected to grow at approximately 6% CAGR from 2024 to 2029. This growth is driven by the segment's innovative dry-forming technology that enables sustainable transition from single-use plastics to fiber-based alternatives. The dry molded fiber (DMF) technology stands out for its water-saving capabilities, requiring minimal water for production while maintaining high efficiency in terms of both time and cost. The segment's growth is further accelerated by its expanding applications across various industries including food service, beauty and cosmetics, refrigerated foods, coffee, frozen foods, personal care, and medical devices. The increasing adoption of DMF technology by major manufacturers and the development of standardized and commercially approved products are expected to sustain this growth trajectory over the forecast period.

Segment Analysis: By End-User Industry

Food and Beverages Segment in Molded Fiber Packaging Market

The Food and Beverages segment continues to dominate the global molded fiber packaging market, commanding approximately 66% market share in 2024. This significant market position is driven by the extensive adoption of molded fiber products in various food service applications, including clam-shell containers, takeout meal containers, egg trays and cartons, and fruit, vegetable, and mushroom trays. The segment's prominence is further strengthened by the increasing consumer preference for sustainable and eco-friendly packaging solutions in the food industry. The production process has evolved significantly, resulting in new coatings and molded fiber products with enhanced flexibility, rigidity, water and oil resistance, air permeability, and hygroscopic ability, making them excellent alternatives to plastic food packaging. Customers now recognize molded pulp packaging as an indicator that restaurants are concerned about the environment, establishing it as the preferred food packaging option for health-conscious businesses, including fast-casual eateries, farm-to-table restaurants, and healthcare facilities.

Healthcare Segment in Molded Fiber Packaging Market

The Healthcare segment is emerging as the fastest-growing sector in the molded fiber packaging market, projected to grow at approximately 6% from 2024 to 2029. This growth is primarily driven by the increasing adoption of sustainable and biodegradable packaging solutions in the healthcare industry. The segment's expansion is fueled by the rising demand for clinical packaging that offers protection against cross-contamination in inpatient care settings. Molded fiber products have gained significant traction in the disposable goods industry due to their affordability, biodegradability, and disposability characteristics. The healthcare sector increasingly utilizes these sustainable solutions for various applications, including urine bottles, bedpans, kidney plates, and bowls, demonstrating an expanding application beyond traditional packaging needs. The segment's growth is further supported by the superior benefits of single-use disposables, which are more practical, cost-effective, and significantly reduce the risk of infection and cross-contamination.

Remaining Segments in End-User Industry

The Electronics and Other End-user Industries segments continue to play vital roles in shaping the molded fiber packaging market landscape. The Electronics segment is particularly noteworthy for its adoption of molded fiber packaging in protecting sensitive electronic components during shipping and storage, offering excellent shock absorption and compression resistance capabilities. The Other End-user Industries segment, which encompasses personal care, cosmetics, and industrial applications, demonstrates the versatility of molded fiber packaging across various sectors. These segments are increasingly embracing molded fiber solutions due to their sustainable characteristics, customization possibilities, and ability to provide superior protection for diverse products. The growing emphasis on environmental sustainability across these industries continues to drive innovation in molded fiber packaging solutions, leading to expanded applications and improved product offerings.

Molded Fiber Packaging Market Geography Segment Analysis

Molded Fiber Packaging Market in North America

The North American molded fiber packaging market demonstrates strong growth potential driven by increasing environmental awareness and stringent regulations against single-use plastics. The United States and Canada represent the key markets in this region, with both countries showing significant adoption of sustainable packaging solutions. The region's growth is primarily fueled by the expanding food service industry, rising e-commerce activities, and increasing demand from electronics manufacturers. The presence of major market players and advanced manufacturing capabilities further strengthens North America's position in the global molded fiber packaging market.

Molded Fiber Packaging Market in the United States

The United States dominates the North American market, holding approximately 85% market share in 2024. The country's market is driven by robust demand from online food service delivery and increasing adoption of transfer molded products. Several manufacturers are expanding their production capabilities across the country, particularly focusing on sustainable and innovative solutions. The growing rate of urbanization has resulted in a higher focus on sustainability and recyclability in food packaging. The healthy growth of end-users, such as quick-service restaurants, full-service restaurants, coffee and snack outlets, and retail establishments, continues to drive the demand for convenient and sustainable fiber packaging solutions.

Molded Fiber Packaging Market in Canada

Canada emerges as the fastest-growing market in North America with a projected growth rate of approximately 6% during 2024-2029. The country's market is experiencing high demand from manufacturers of perishable fresh food products primarily sold at retail outlets such as supermarkets, hypermarkets, and department stores. The government's strong focus on sustainable packaging initiatives and investments in promoting eco-friendly alternatives is driving market growth. Canadian manufacturers are increasingly adopting innovative technologies and sustainable practices to meet the rising demand for environmentally conscious molded fiber packaging solutions.

Molded Fiber Packaging Market in Europe

Europe represents a mature market for molded fiber packaging, with a strong presence across multiple countries including Germany, France, the United Kingdom, Italy, and Spain. The region's market is characterized by stringent environmental regulations and high consumer awareness regarding sustainable packaging solutions. The European market benefits from advanced manufacturing capabilities, strong research and development activities, and continuous technological innovations in molded fiber production.

Molded Fiber Packaging Market in Germany

Germany leads the European market, commanding approximately 26% market share in 2024. The country's dominant position is supported by its robust manufacturing infrastructure and strong presence of key industry players. German manufacturers are at the forefront of technological innovations in molded fiber packaging, particularly in developing solutions for the food and beverage industry. The country's strict recycling regulations and growing consumer preference for sustainable packaging solutions continue to drive market growth.

Molded Fiber Packaging Market in the United Kingdom

The United Kingdom demonstrates the highest growth potential in Europe with a projected growth rate of approximately 5% during 2024-2029. The country's market is driven by increasing adoption of sustainable packaging solutions across various industries, particularly in the food service and healthcare sectors. British manufacturers are actively investing in research and development to create innovative molded fiber packaging solutions. The government's initiatives to reduce plastic waste and promote recyclable packaging materials further support market growth.

Molded Fiber Packaging Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for molded fiber packaging, with China, Japan, and India emerging as key contributors. The region's market is driven by rapid industrialization, growing environmental awareness, and increasing adoption of sustainable packaging solutions across various industries. The presence of abundant raw material resources and lower manufacturing costs make APAC an attractive market for both domestic and international players.

Molded Fiber Packaging Market in China

China maintains its position as the largest market in the Asia-Pacific region, supported by its extensive manufacturing capabilities and growing demand from various end-user industries. The country's robust electronics manufacturing sector and expanding food delivery services contribute significantly to market growth. Chinese manufacturers are increasingly focusing on technological advancements and product innovations to meet the evolving demands of both domestic and international markets.

Molded Fiber Packaging Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by increasing environmental awareness and government initiatives to reduce plastic usage. The country's market benefits from the availability of various non-wood raw materials for pulp production, including bagasse, jute fiber, and wheat straw. Indian manufacturers are actively investing in modern production facilities and innovative technologies to meet the growing demand for sustainable packaging solutions.

Molded Fiber Packaging Market in Latin America

The Latin American market for molded fiber packaging shows promising growth potential, with Brazil and Mexico emerging as key markets. The region's growth is driven by increasing awareness about sustainable packaging and stringent regulations against plastic usage. Brazil leads the market size in the region, while Mexico demonstrates the fastest growth rate, supported by its robust manufacturing sector and increasing adoption of eco-friendly packaging solutions across various industries.

Molded Fiber Packaging Market in the Middle East & Africa

The Middle East & Africa region presents emerging opportunities in the molded fiber packaging market, with the United Arab Emirates, Saudi Arabia, and South Africa as key markets. The region's growth is primarily driven by increasing environmental awareness and government initiatives to reduce plastic waste. Saudi Arabia leads the market size in the region, while the United Arab Emirates shows the fastest growth rate, supported by its growing food service industry and increasing adoption of sustainable packaging solutions.

Get Analysis on Important Geographic Markets

Download PDF

Molded Fiber Packaging Industry Overview

Top Companies in Molded Fiber Packaging Market

The molded fiber packaging companies market features established players like Huhtamaki Oyj, Henry Molded Products, Omni-Pac Group, Cullen Packaging, and Brødrene Hartmann leading the industry through continuous innovation and strategic expansion. Companies are increasingly focusing on developing sustainable molded fiber packaging solutions, particularly in thermoformed fiber and precision molding technologies, to meet growing environmental concerns. Market leaders are investing heavily in research and development to improve product quality, enhance manufacturing efficiency, and develop new applications across various industries. Strategic partnerships and collaborations with technology providers, particularly in dry molded fiber solutions, have become a key trend to accelerate innovation and market penetration. Operational agility is being achieved through investments in automated manufacturing processes, digitalization of operations, and establishment of regional production facilities to serve local markets more effectively.

Market Structure Shows Dynamic Competitive Environment

The molded fiber packaging market exhibits a mix of global conglomerates and specialized regional players, creating a moderately fragmented competitive landscape. Global players like Huhtamaki and Brødrene Hartmann leverage their extensive manufacturing networks, technological capabilities, and strong customer relationships to maintain market leadership, while regional specialists focus on serving specific geographic markets or industry segments with customized solutions. The market is characterized by increasing consolidation through mergers and acquisitions, as larger players seek to expand their geographic presence, enhance technological capabilities, and strengthen their product portfolios.

The competitive dynamics are shaped by the presence of both vertically integrated manufacturers who control their supply chain from raw material to finished products, and specialized producers focusing on specific market segments. Market participants are increasingly pursuing strategic partnerships with raw material suppliers, technology providers, and end-users to strengthen their market position and ensure sustainable growth. The industry is witnessing a trend towards consolidation, particularly in mature markets, as companies seek economies of scale and broader market access through strategic acquisitions and joint ventures.

Innovation and Sustainability Drive Future Success

Success in the molded fiber packaging market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and meeting sustainability requirements. Incumbent players are focusing on developing proprietary technologies, expanding their sustainable product portfolios, and strengthening their manufacturing capabilities to maintain their market position. Companies are also investing in research and development to create differentiated products with enhanced performance characteristics, while simultaneously optimizing their production processes to improve cost efficiency and reduce environmental impact.

For contenders looking to gain market share, the focus needs to be on developing specialized molded fiber packaging solutions for specific industry segments, building strong relationships with key customers, and leveraging technological innovations to create competitive advantages. The market's future success factors include the ability to address increasing end-user demands for sustainable packaging solutions, navigate potential regulatory changes regarding environmental protection and recycling, and manage the risk of substitution from alternative packaging materials. Companies must also consider the concentration of end-users in key industries such as food and beverages, electronics, and healthcare, while developing strategies to expand their customer base and reduce dependency on specific market segments.

Molded Fiber Packaging Market Leaders

-

Huhtamaki OYJ

-

Henry Moulded Products Inc.

-

Cullen Packaging

-

Pulpac AB

-

Sabert Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Molded Fiber Packaging Market News

- September 2024: Dart Container Corporation, a seasoned player in food service packaging specializing in paper, plastic, and wet molding technologies, has forged a strategic alliance with PulPac. With backing from PulPac’s North American sales agent, Seismic Solutions, Dart has secured a license from PulPac and is setting up the inaugural Dry Molded Fiber production line in North America, known as the PulPac Scala. In collaboration with their turnkey partner, Huarong Group from Taiwan, PulPac unveiled a versatile and compact Dry Molded Fiber machine platform.

- August 2024: In a notable milestone underscoring its enduring dedication to sustainability, Sabert Corporation revealed a significant achievement. Products crafted at the Greenville, Texas facility, utilizing the company's Pulp Plus and Pulp Ultra molded formulations, have garnered certification from the Biodegradable Products Institute (BPI). These products also align with ASTM standards for compostable items in North America. This validation from an independent entity cements Sabert's position as a premier BPI-certified domestic producer of molded pulp food service packaging in the U.S.

Molded Fiber Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

-

4.4 Import Export Analysis of Molded Fiber for Listed Countries

- 4.4.1 United States - Import and Export Analysis

- 4.4.2 United Kingdom - Import And Export Analysis

- 4.4.3 France - Import and Export Analysis

- 4.4.4 Germany - Import and Export Analysis

- 4.4.5 Italy - Import and Export Analysis

- 4.4.6 Spain - Import and Export Analysis

- 4.4.7 China - Import and Export Analysis

- 4.4.8 Japan - Import and Export Analysis

- 4.4.9 India - Import and Export Analysis

- 4.4.10 Brazil - Import and Export Analysis

- 4.4.11 Mexico - Import and Export Analysis

- 4.4.12 United Arab Emirates - Import and Export Analysis

- 4.4.13 Saudi Arabia - Import and Export Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Shift in Consumer Preferences Toward Recyclable and Eco-friendly Materials

- 5.1.2 Growing Disposable Income

- 5.1.3 Augmented Demand For Reusable and Sustainable Packaging From End-users

-

5.2 Market Challenges

- 5.2.1 Strict Government Rules and Regulations

- 5.2.2 Fluctuations in the Cost of Raw Materials

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Thick wall

- 6.1.2 Transfer

- 6.1.3 Thermoformed

- 6.1.4 Processed

-

6.2 By Formal Type

- 6.2.1 Wet

- 6.2.2 Dry

-

6.3 By End-user Industry

- 6.3.1 Food and Beverages

- 6.3.2 Electronics

- 6.3.3 Healthcare

- 6.3.4 Other End-user Industries

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 France

- 6.4.2.3 Germany

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 United Arab Emirates

- 6.4.6.2 Saudi Arabia

- 6.4.6.3 South Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Huhtamaki Oyj

- 7.1.2 Henry Molded Products Inc.

- 7.1.3 Omni-PAC Group UK

- 7.1.4 Cullen Packaging

- 7.1.5 Brodrene Hartmann A/S

- 7.1.6 Enviropak Corporation

- 7.1.7 Heracles Packaging Company SA

- 7.1.8 Sabert Corporation

- 7.1.9 Keiding, Inc.

- 7.1.10 International Paper

- 7.1.11 PulPac AB

- *List Not Exhaustive

8. INVESTMENT OUTLOOK

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and the Geography section will also include Rest of Europe, Asia Pacific, Latin America and Middle East and Africa.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Molded Fiber Packaging Industry Segmentation

The study covers the molded fiber packaging market tracked in terms of consumption and the sales of molded fiber packaging products offered by various vendors operating across the geographies. The consumption value of molded fiber packaging is considered in (USD) for the market size and forecasts.

The molded fiber packaging market is segmented by type (thick wall, transfer, thermoformed, and processed), formal type (wet and dry), end-user industry (food and beverages, electronics, healthcare, and other end-user industries), and geography (North America [United States and Canada], Europe [United Kingdom, France, Germany, Italy, Spain, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific), Latin America [Brazil, Mexico, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are in terms of value (USD) for all the above segments.

| By Type | Thick wall | ||

| Transfer | |||

| Thermoformed | |||

| Processed | |||

| By Formal Type | Wet | ||

| Dry | |||

| By End-user Industry | Food and Beverages | ||

| Electronics | |||

| Healthcare | |||

| Other End-user Industries | |||

| By Geography*** | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Asia | China | ||

| Japan | |||

| India | |||

| Australia and New Zealand | |||

| Latin America | Brazil | ||

| Mexico | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

Need A Different Region or Segment?

Customize Now

Molded Fiber Packaging Market Research FAQs

How big is the Molded Fiber Packaging Market?

The Molded Fiber Packaging Market size is worth USD 15.57 billion in 2025, growing at an 4.67% CAGR and is forecast to hit USD 19.57 billion by 2030.

What is the current Molded Fiber Packaging Market size?

In 2025, the Molded Fiber Packaging Market size is expected to reach USD 15.57 billion.

Which is the fastest growing region in Molded Fiber Packaging Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Molded Fiber Packaging Market?

In 2025, the Europe accounts for the largest market share in Molded Fiber Packaging Market.

What years does this Molded Fiber Packaging Market cover, and what was the market size in 2024?

In 2024, the Molded Fiber Packaging Market size was estimated at USD 14.84 billion. The report covers the Molded Fiber Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Molded Fiber Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Molded Fiber Packaging Market Research

Mordor Intelligence provides a comprehensive analysis of the molded fiber packaging market, utilizing our extensive expertise in fiber-based packaging research and consulting. Our latest report examines the evolving landscape of molded fiber technology and molded pulp packaging. It covers crucial developments across global molded fiber packaging segments. The detailed report PDF, available for download, offers in-depth insights into fiber packaging trends, molded fiber food packaging innovations, and emerging packaging solutions across various regions, including North America and Europe.

Our analysis benefits stakeholders by offering detailed profiles of leading molded fiber packaging manufacturers and molded fiber packaging companies. It also includes a comprehensive evaluation of fiber packaging suppliers. The report examines various aspects, including molded fibre packaging applications, moulded pulp packaging developments, and fiber molded packaging innovations. Stakeholders gain valuable insights into molded fiber products advancement, regional market dynamics, and emerging opportunities in the molded fiber pulp packaging sector, supported by robust data analysis and industry expert perspectives.