| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 7.61 Billion |

| Market Size (2030) | USD 23.61 Billion |

| CAGR (2025 - 2030) | 25.41 % |

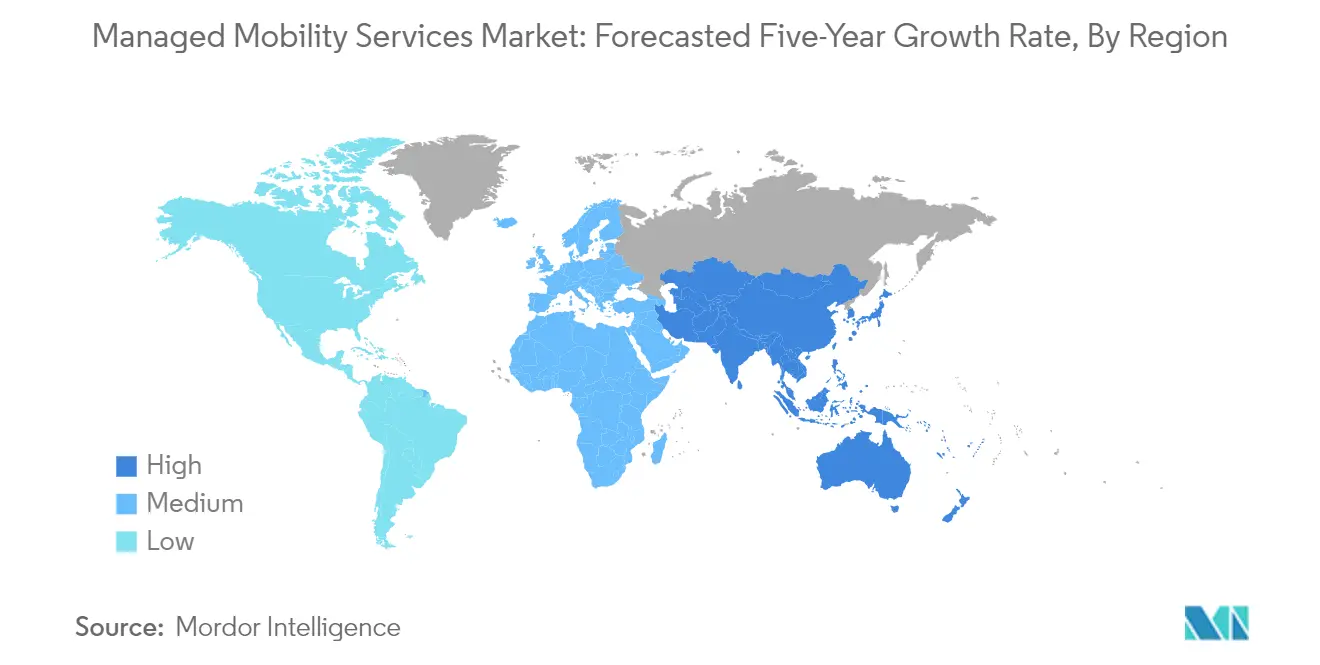

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

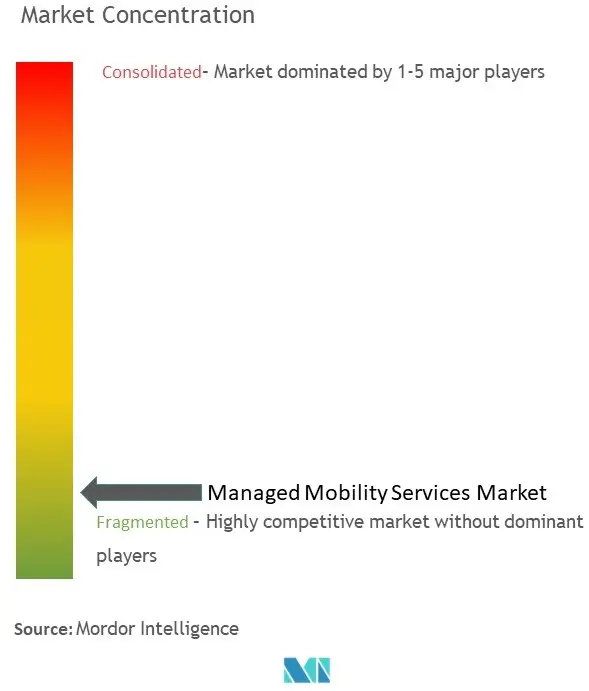

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Managed Mobility Services Market Analysis

The Global Managed Mobility Services Market size is estimated at USD 7.61 billion in 2025, and is expected to reach USD 23.61 billion by 2030, at a CAGR of 25.41% during the forecast period (2025-2030).

The managed mobility services landscape is experiencing unprecedented growth driven by the rapid evolution of digital connectivity and mobile technology adoption. According to recent industry data, there are over 10.47 billion mobile connections worldwide in 2022, significantly surpassing the global population of 7.932 billion, indicating the massive scale of device management requirements across enterprises. This exponential growth in connected devices has created complex ecosystems within organizations, requiring sophisticated mobility management services that can handle diverse device types, operating systems, and security protocols. The convergence of multiple devices per user, coupled with the need for seamless integration across platforms, has made centralized mobility management an essential component of modern enterprise operations.

The financial services sector has emerged as a significant catalyst for managed mobility services adoption, with real-time payment systems driving digital transformation initiatives. According to FIS, several countries have witnessed remarkable growth in real-time payment transaction values, with the Philippines experiencing a 482% increase, followed by Bahrain at 311%, and Australia at 231%. This surge in digital financial transactions has necessitated robust mobile security protocols and device management systems, particularly as financial institutions expand their digital service offerings. The integration of mobile banking platforms, digital wallets, and payment systems has created a complex web of security and management requirements that mobility service providers are uniquely positioned to address.

Enterprise mobility managed services have evolved beyond simple device control to encompass comprehensive lifecycle management, application security, and data protection. Organizations are increasingly seeking solutions that can provide end-to-end visibility and control over their mobile assets while ensuring compliance with industry regulations and security standards. The integration of artificial intelligence and machine learning capabilities into managed mobility solutions has enabled predictive maintenance, automated security responses, and enhanced user experience management, fundamentally transforming how enterprises approach mobile device administration and security.

The telecommunications and healthcare sectors are witnessing significant transformations in their mobility management approaches, driven by the need for specialized solutions that can handle sector-specific requirements. Healthcare organizations, in particular, are adopting mobility managed services to ensure compliance with data protection regulations while enabling seamless communication among healthcare professionals. The integration of mobile devices in clinical workflows, patient care, and administrative processes has created a complex ecosystem that requires sophisticated management solutions to ensure both efficiency and security. This trend is particularly evident in the adoption of secure messaging platforms, mobile health applications, and remote patient monitoring systems, all of which require robust device management and security protocols.

Managed Mobility Services Market Trends

Increasing Adoption of BYOD in Multiple Industries

The enterprise mobility trend has emerged as a significant driver for managed mobility services, with companies increasingly focusing on core business strategies while embracing bring-your-own-device (BYOD) policies. According to Cisco's analysis, enterprises implementing BYOD policies achieve substantial cost benefits, saving approximately USD 350 per employee annually, with potential increases to USD 1,300 per employee through reactive programs. This financial advantage has become particularly compelling for small and medium enterprises (SMBs), enabling them to protect their bottom line while simultaneously improving employee productivity and operational flexibility. The trend is further supported by the increasing sophistication of managed mobility solutions, which allow organizations to maintain security protocols while providing employees the flexibility to use their preferred devices.

The proliferation of connected devices is accelerating the adoption of BYOD policies across industries. According to Cisco's annual internet report, the average number of devices and connections per capita worldwide is projected to reach 3.6 by 2023, with the United States leading at an expected 13.6 devices per capita. This surge in device usage has prompted organizations to implement comprehensive mobility managed solutions that can secure corporate data across multiple platforms while maintaining operational efficiency. The integration of 5G technology is further amplifying this trend, with GSMA predicting that 5G will reach 100 million mobile connections by early 2023 and establish itself as the dominant mobile network technology by 2025, with over 190 million connections in the United States alone.

Understand The Key Trends Shaping This Market

Download PDF

Companies Outsourcing IT Activities

The increasing complexity of IT infrastructure and the need for specialized expertise have driven organizations to outsource their IT activities, particularly in mobile device and application management. With digital transformation initiatives becoming more sophisticated, organizations are finding it more efficient to partner with managed mobility service providers who can offer comprehensive mobility solutions. These providers bring expertise in areas such as mobile security, device management, and application lifecycle management, allowing companies to focus on their core business operations while ensuring their mobile infrastructure remains secure and efficient. The trend is particularly evident in the integration of cloud-based services, where organizations can leverage specialized knowledge without maintaining extensive in-house IT teams.

The rising costs associated with data breaches and security incidents have further accelerated the trend toward IT outsourcing. According to the Ponemon Institute's study, the global average cost of a data breach stands at USD 3.83 million, with some regions experiencing significantly higher costs. This financial risk has prompted organizations to seek specialized managed mobility service providers who can implement robust security measures and maintain compliance with evolving regulatory requirements. The trend is particularly pronounced in industries handling sensitive data, where the combination of mobility management and security expertise has become crucial for maintaining operational integrity while meeting compliance standards. Service providers are responding by offering integrated solutions that encompass device management, application security, and compliance monitoring, providing organizations with comprehensive protection against evolving security threats. The managed mobility services market is poised for growth as these solutions become increasingly essential.

Segment Analysis: By Function

Mobile Device Management Segment in Global Managed Mobility Services Market

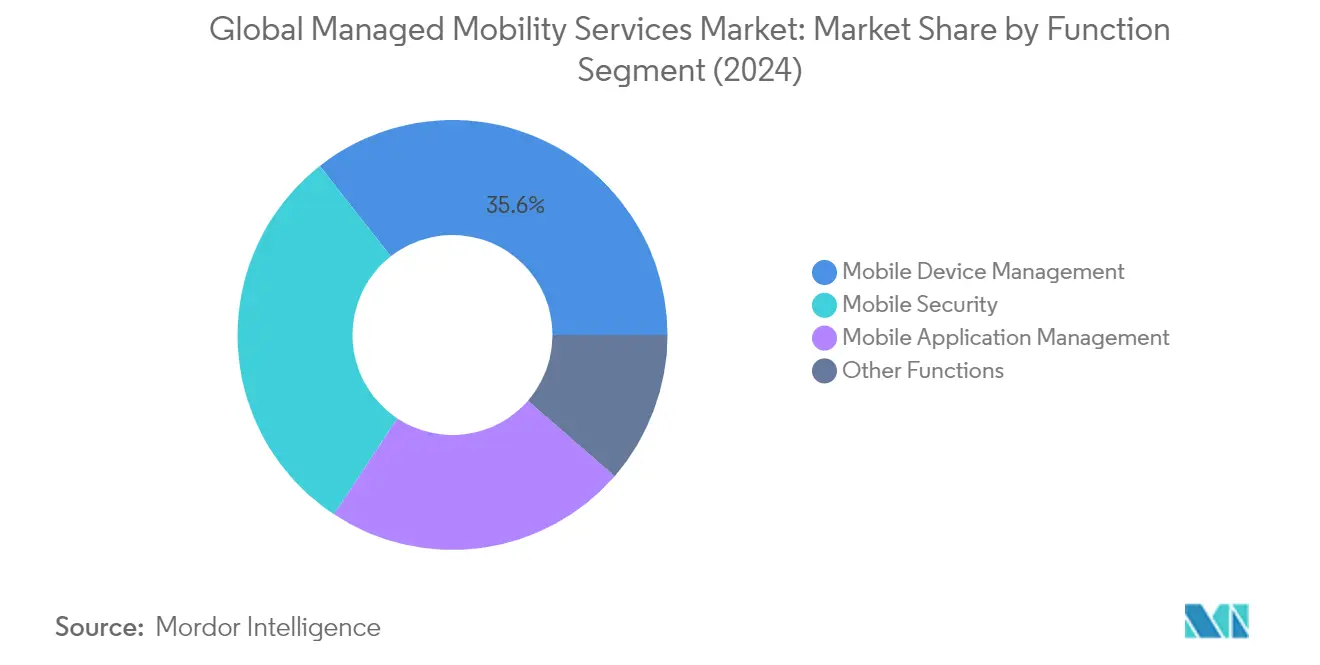

Mobile Device Management (MDM) holds the dominant position in the global managed mobility services market, accounting for approximately 36% market share in 2024. This segment's leadership is driven by the increasing adoption of BYOD policies across enterprises and the growing need for centralized device management solutions. MDM solutions enable organizations to efficiently manage and secure their mobile device fleet through features like over-the-air distribution of applications, remote configuration management, and comprehensive device lifecycle management. The segment's strong performance is further bolstered by the rising demand for solutions that can handle diverse device ecosystems, including smartphones, tablets, laptops, and IoT devices, while ensuring compliance with corporate security policies.

Mobile Application Management Segment in Global Managed Mobility Services Market

The Mobile Application Management (MAM) segment is experiencing the most rapid growth in the managed mobility services market, projected to grow at approximately 26% during 2024-2029. This exceptional growth is driven by the increasing complexity of enterprise mobile applications and the need for sophisticated application-level security controls. Organizations are increasingly adopting MAM solutions to manage the complete lifecycle of mobile applications, including installation, configuration, updates, and security policies. The segment's growth is further accelerated by the rising demand for granular control over application data, secure app deployment capabilities, and the need to separate personal and corporate applications on employee devices.

Remaining Segments in Managed Mobility Services Market by Function

The Mobile Security segment represents a crucial component of the managed mobility services market, focusing on comprehensive threat protection and secure access management for mobile devices and applications. This segment addresses critical security challenges, including malware protection, data loss prevention, and secure network access. The Other Functions segment encompasses various specialized services such as Mobile Content Management (MCM) and Mobile Information Management (MIM), which provide secure access to corporate resources and help organizations maintain control over their mobile content distribution and access policies.

Segment Analysis: By Deployment

Cloud Segment in Global Managed Mobility Services Market

The cloud segment has emerged as the dominant force in the global managed mobility services market, commanding approximately 50% of the total market share in 2024. This segment's leadership position is driven by several key factors, including the increasing adoption of cloud-based mobile device management solutions across enterprises of all sizes. Organizations are increasingly preferring cloud deployment due to its inherent benefits of flexibility, scalability, and reduced upfront costs. The segment's growth is further accelerated by the rising trend of remote work environments, which has made cloud-based mobility management services essential for maintaining business continuity and operational efficiency. Additionally, the cloud segment is experiencing rapid expansion with an expected growth rate of around 28% during 2024-2029, primarily driven by the increasing demand for real-time data access, improved collaboration capabilities, and the need for seamless integration with existing enterprise systems.

On-Premise Segment in Global Managed Mobility Services Market

The on-premise segment continues to maintain a significant presence in the managed mobility services market, particularly among organizations with stringent data security requirements and regulatory compliance needs. This deployment model remains crucial for enterprises that prefer complete control over their mobility management infrastructure and data security protocols. The segment's resilience is supported by industries such as banking, healthcare, and government sectors, where data sovereignty and privacy concerns often necessitate on-premise solutions. Despite the growing cloud adoption, on-premise deployments continue to be relevant for organizations that require customized managed mobility solutions aligned with their existing IT infrastructure and security frameworks.

Segment Analysis: By End-User Industry

IT and Telecom Segment in Managed Mobility Services Market

The IT and Telecom sector continues to dominate the managed mobility services market, holding approximately 21% market share in 2024. This significant market position is driven by the sector's high rate of technological adoption and the widespread implementation of bring-your-own-device (BYOD) policies across organizations. The increasing complexity of managing multiple device platforms, interpreted content for specialized mobile applications, and the need for seamless communication between mobile office workers and management systems have made mobile managed services essential for IT and telecom companies. These organizations are leveraging managed mobility services to overcome traditional communication challenges, enabling efficient access to business emails, databases, and other corporate content across various devices. The sector's leadership is further strengthened by the growing shift towards digital connectivity, with at least half of the employees using multiple devices for work, necessitating centralized management solutions.

Education Segment in Managed Mobility Services Market

The education sector is emerging as the fastest-growing segment in the managed mobility services market, with a projected growth rate of approximately 28% during 2024-2029. This remarkable growth is primarily driven by the increasing adoption of virtual learning environments and device-loan programs across educational institutions. Higher education institutions are implementing bring-your-own-device (BYOD) programs as a smarter way for students and faculty to work, collaborate, and access technology resources. The sector faces unique challenges in implementing successful virtual learning environments, including the need for rapid deployment of devices at scale, maintaining cost control while ensuring visibility, addressing safety and security concerns in virtual environments, and establishing sustainable long-term device management programs. These challenges are compelling educational institutions to turn to managed mobility services for ensuring productive mobile device usage while minimizing distractions and reducing disruptions.

Remaining Segments in End-User Industry

The managed mobility services market encompasses several other significant segments, including BFSI, Healthcare, Manufacturing, Retail, and other industries. The BFSI sector is particularly notable for its increasing focus on digital transformation and the need for robust security measures in mobile banking applications. The healthcare sector is driven by the growing adoption of mobile devices among medical professionals and the need to comply with healthcare data regulations. Manufacturing companies are leveraging managed mobility services to support their digital transformation initiatives and Industry 4.0 implementations. The retail sector is utilizing these services to enhance customer experience through mobile point-of-sale systems and inventory management. Each of these segments contributes uniquely to the market's growth by addressing sector-specific mobility challenges and requirements.

Global Managed Mobility Services Market Geography Segment Analysis

Managed Mobility Services Market in North America

North America represents a mature managed mobility services market, driven by widespread adoption of digital transformation initiatives and enterprise mobility solutions. The United States and Canada form the key markets in this region, with organizations increasingly focusing on mobile security, device management, and application management services. The region's growth is supported by the presence of major technology vendors, strong IT infrastructure, and increasing adoption of BYOD policies across various industries.

Managed Mobility Services Market in the United States

The United States dominates the North American managed mobility services landscape as the largest market. With approximately 84% share of the regional market in 2024, the country's leadership position is driven by extensive cloud adoption, digital transformation initiatives, and an increasing focus on mobile security. The market is characterized by a strong presence of major service providers, growing adoption of BYOD policies, and increasing demand from sectors like healthcare, BFSI, and manufacturing. Organizations in the United States are particularly focused on securing mobile environments and managing diverse device ecosystems, while government organizations, including the defense sector, are increasingly adopting BYOD approaches.

Managed Mobility Services Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected CAGR of approximately 24% from 2024-2029. The country's growth is driven by increasing adoption of IoT technologies across different industries, particularly in the manufacturing and healthcare sectors. Canadian enterprises are increasingly focusing on digital transformation initiatives and cloud adoption, creating significant opportunities for managed mobility service providers. The market is also influenced by growing cybersecurity concerns and the need for comprehensive mobile device management solutions across various industry verticals.

Managed Mobility Services Market in Europe

The European managed mobility services market demonstrates strong growth potential, characterized by increasing adoption of digital transformation initiatives across various industries. The region encompasses key markets including Germany, the United Kingdom, and France, each contributing significantly to the overall market dynamics. The market is driven by strong regulatory frameworks, increasing cloud adoption, and a growing focus on mobile security across enterprises.

Managed Mobility Services Market in Germany

Germany leads the European managed mobility services market, commanding approximately 25% of the regional market share in 2024. The country's market leadership is supported by a strong industrial base, government initiatives promoting digital transformation, and increasing adoption of Industry 4.0 practices. German organizations are particularly focused on mobile security solutions and device management services, driven by stringent data protection regulations and increasing cybersecurity concerns.

Managed Mobility Services Market in Germany

Germany also emerges as the fastest-growing market in Europe, with an expected CAGR of approximately 23% from 2024-2029. The growth is driven by increasing adoption of cloud services, rising demand for mobile security solutions, and government initiatives supporting digital transformation. The country's focus on industrial digitization, coupled with a strong emphasis on data protection and security, creates significant opportunities for mobility service providers.

Managed Mobility Services Market in Asia-Pacific

The Asia-Pacific region represents a dynamic mobility technology market for managed mobility services, characterized by rapid digital transformation across various industries. Key markets include China, India, and Japan, each contributing uniquely to the regional market landscape. The region's growth is driven by increasing smartphone penetration, rising adoption of BYOD policies, and a growing focus on enterprise mobility solutions.

Managed Mobility Services Market in China

China dominates the Asia-Pacific mobility managed services market as the largest country market. The country's leadership position is supported by extensive digital transformation initiatives, growing adoption of cloud computing, and an increasing focus on mobile security solutions. Chinese enterprises are particularly focused on implementing comprehensive device management solutions and securing their mobile environments, driven by the rapid growth in connected devices and an expanding mobile workforce.

Managed Mobility Services Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's growth is driven by rapid digitalization across industries, increasing adoption of BYOD policies, and a growing focus on mobile security solutions. Indian organizations are increasingly investing in managed mobility services to enhance operational efficiency and secure their mobile environments, particularly in sectors like IT, BFSI, and manufacturing.

Managed Mobility Services Market in Latin America

The Latin American managed mobility services market shows promising growth potential, with Brazil, Argentina, and Mexico as key contributing countries. The region's market is characterized by increasing digital transformation initiatives, growing adoption of cloud services, and a rising focus on mobile security solutions. Brazil emerges as the largest market in the region, while Argentina demonstrates the fastest growth rate, driven by government initiatives supporting digital infrastructure development and increasing enterprise mobility adoption.

Managed Mobility Services Market in Middle East & Africa

The Middle East & Africa region presents significant opportunities in the managed mobility services market, with the United Arab Emirates, Saudi Arabia, and South Africa as key markets. The region's growth is driven by digital transformation initiatives, increasing cloud adoption, and a growing focus on mobile security solutions. Saudi Arabia represents the largest market in the region, while South Africa shows the fastest growth rate, supported by increasing enterprise mobility adoption and rising demand for managed security services.

Get Analysis on Important Geographic Markets

Download PDF

Managed Mobility Services Industry Overview

Top Companies in Managed Mobility Services Market

The managed mobility services market features prominent players including AT&T, IBM (Kyndryl), Fujitsu, Wipro, Orange SA, Telefónica, Samsung Electronics, Hewlett-Packard, Vodafone Group, Microsoft Corporation, and Tech Mahindra. These managed mobility service companies are actively pursuing product innovation through enhanced mobile device management solutions, security features, and cloud integration capabilities. Operational agility is demonstrated through the development of comprehensive end-to-end mobility solutions and flexible deployment models spanning on-premise and cloud environments. Strategic moves include significant investments in research and development, particularly in areas like artificial intelligence, machine learning, and IoT integration for mobility management. Market expansion efforts are characterized by strategic partnerships, regional market penetration initiatives, and the development of industry-specific solutions targeting sectors like healthcare, retail, and manufacturing.

High Competition Drives Market Consolidation Trends

The managed mobility services market exhibits a mix of global technology conglomerates and specialized mobility service providers competing for market share. Global players leverage their extensive infrastructure, established client relationships, and comprehensive service portfolios to maintain market dominance, while specialized providers focus on niche solutions and superior customer service to carve out their market positions. The market structure is characterized by moderate consolidation, with larger players actively pursuing strategic acquisitions to enhance their technological capabilities and expand their geographical presence.

The industry has witnessed significant merger and acquisition activity, particularly focused on strengthening managed security services capabilities and expanding regional footprints. Companies are increasingly acquiring smaller, specialized firms to gain access to innovative technologies, skilled talent pools, and established customer bases in specific regions or industries. This consolidation trend is driven by the need to offer comprehensive mobility solutions that encompass device management, security, application management, and support services under a single umbrella, allowing providers to better serve the evolving needs of enterprise customers.

Innovation and Adaptability Drive Future Success

Success in the managed mobility services market increasingly depends on providers' ability to deliver comprehensive, secure, and scalable solutions while maintaining operational efficiency. Incumbent players must focus on continuous innovation in areas such as artificial intelligence-driven management tools, advanced security features, and seamless integration capabilities across different platforms and devices. Additionally, providers need to develop strong partnerships with device manufacturers, software providers, and cloud service providers to create comprehensive ecosystem solutions that address the complex needs of enterprise customers.

For contenders looking to gain market share, differentiation through specialized services, industry-specific solutions, and superior customer support becomes crucial. The market presents moderate substitution risk, primarily from in-house mobility management solutions, though the complexity of managing diverse mobile environments continues to favor managed mobility service providers. Regulatory compliance, particularly regarding data privacy and security, remains a critical factor shaping service offerings and market dynamics. Success also depends on providers' ability to address the high concentration of enterprise customers by offering flexible, customizable solutions that can scale according to client needs while maintaining cost-effectiveness.

Managed Mobility Services Market Leaders

-

AT&T Intellectual Property

-

Fujitsu

-

Kyndryl Inc.

-

Wipro

-

Orange S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Managed Mobility Services Market News

- February 2023: Kyndryland Microsoft established its first Latin American Center of Excellence with multidisciplinary teams in Brazil, Colombia, Mexico, and Peru. The center combines Kyndryl'sexpertise and understanding of mission-critical IT systems with the Microsoft Cloud to assist companies in the region in accelerating their digital transformation journeys. Organizations throughout Latin America have identified the need to modernize their IT structures and legacy systems by migrating to cloud environments. This will allow them to increase hybrid cloud speed and agility. According to IDC, the cloud market in the region will grow by more than 30% by 2023. Furthermore, the Kyndryland Microsoft Center of Excellence will be a central hub of information, resources, and skills related to Microsoft technologies to support enterprise customers throughout Latin America. Kyndryl's experts in solutions, consulting, and managed services, will collaborate with Microsoft architects and technical staff to co-create replicable assets, conduct proof of concepts (POCs), and scale innovation best practices.

- February 2023: Spanish company Telefonica SA and US-based SkydwellerAero Inc., which develop solar-powered aircraft for defense and commercial industries, announced an official partnership to explore developing connectivity solutions to accelerate the expansion of cellular coverage, delivering reliable and affordable broadband access in unserved and underserved regions.

Managed Mobility Services Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of COVID-19 Impact on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Adoption of BYOD in Multiple Industries

- 5.1.2 Companies Outsourcing IT Activities

-

5.2 Market Restraints

- 5.2.1 Lack of Control over Operations and Cost Visibility

6. MARKET SEGMENTATION

-

6.1 By Function

- 6.1.1 Mobile Device Management

- 6.1.2 Mobile Application Management

- 6.1.3 Mobile Security

- 6.1.4 Other Functions

-

6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

-

6.3 By End-user Industry

- 6.3.1 IT and Telecom

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 Education

- 6.3.7 Other End-user Industries

-

6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 AT&T Intellectual Property

- 7.1.2 Fujitsu

- 7.1.3 Kyndryl Inc.

- 7.1.4 Wipro

- 7.1.5 Orange SA

- 7.1.6 Telefónica SA

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 Hewlett Packard Enterprise

- 7.1.9 Vodafone Group PLC

- 7.1.10 Microsoft Corporation

- 7.1.11 Tech Mahindra

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Managed Mobility Services Industry Segmentation

Managed mobility services (MMS) are defined as the procurement, deployment, and management of mobile devices and apps and PC software and services, connecting out-of-office workers to the enterprise environment. The options for allied services range from short-term post-go-live assistance to long-term application operations. Managed mobility services (MMS) market for the study defines the revenues generated from functions such as mobile device management, mobile application management, mobile security, and other functions that are being used in various end-user industries worldwide. The scope of the study is limited only to the services offered in the market for mobility management. The study also analyses the overall impact of COVID-19 on the ecosystem. The study includes qualitative coverage of the most adopted strategies and an analysis of the key base indicators in emerging markets.

The managed mobility services market is segmented by function (mobile device management, mobile application management, mobile security), deployment (cloud and on-premise), end-user industry (IT and telecom, BFSI, healthcare, manufacturing, retail, education), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Rest of Europe), Asia-Pacific (China, India, Japan, and the rest of Asia-Pacific), Latin America (Brazil, Argentina, Mexico, and the rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and the rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

| By Function | Mobile Device Management | ||

| Mobile Application Management | |||

| Mobile Security | |||

| Other Functions | |||

| By Deployment | Cloud | ||

| On-premise | |||

| By End-user Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare | |||

| Manufacturing | |||

| Retail | |||

| Education | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Argentina | |||

| Mexico | |||

| Rest of Latin America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Managed Mobility Services Market Research FAQs

How big is the Global Managed Mobility Services Market?

The Global Managed Mobility Services Market size is expected to reach USD 7.61 billion in 2025 and grow at a CAGR of 25.41% to reach USD 23.61 billion by 2030.

What is the current Global Managed Mobility Services Market size?

In 2025, the Global Managed Mobility Services Market size is expected to reach USD 7.61 billion.

Who are the key players in Global Managed Mobility Services Market?

AT&T Intellectual Property, Fujitsu, Kyndryl Inc., Wipro and Orange S.A. are the major companies operating in the Global Managed Mobility Services Market.

Which is the fastest growing region in Global Managed Mobility Services Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Managed Mobility Services Market?

In 2025, the North America accounts for the largest market share in Global Managed Mobility Services Market.

What years does this Global Managed Mobility Services Market cover, and what was the market size in 2024?

In 2024, the Global Managed Mobility Services Market size was estimated at USD 5.68 billion. The report covers the Global Managed Mobility Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Managed Mobility Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Global Managed Mobility Services Market Research

Mordor Intelligence provides a comprehensive analysis of the managed mobility services (MMS) industry. We leverage our extensive expertise in the mobility technology market to deliver insightful research. Our detailed report examines the evolving landscape of enterprise mobility managed services, managed mobility solutions, and mobile managed services. The analysis covers leading managed mobility service providers and their innovative approaches to mobility managed solutions. Additionally, it evaluates emerging trends in managed mobility and collaboration services.

Stakeholders gain valuable insights through our thorough examination of mobility management services across global markets. We focus particularly on mobility service providers and their strategic initiatives. The report, available as an easy-to-download PDF, offers an in-depth analysis of managed mobility consulting practices and managed mobility support providers. Our research thoroughly covers managed mobility services companies and leading MMS vendors. It offers stakeholders a comprehensive understanding of mobility managed services implementation strategies and industry best practices. The analysis includes a detailed evaluation of managed mobile services adoption patterns and emerging opportunities in the managed mobility services market.