Consumer Goods and Services

29th JulyUnlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

The Mobile Protective Cases Market Report is Segmented by Case Type (Back Plate Cases, and More), Material Type (Silicon, Genuine and PU Leather, and More), Price Range (Mass, Premium), Distribution Channel (Online Retail Stores, Offline Retail Stores), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

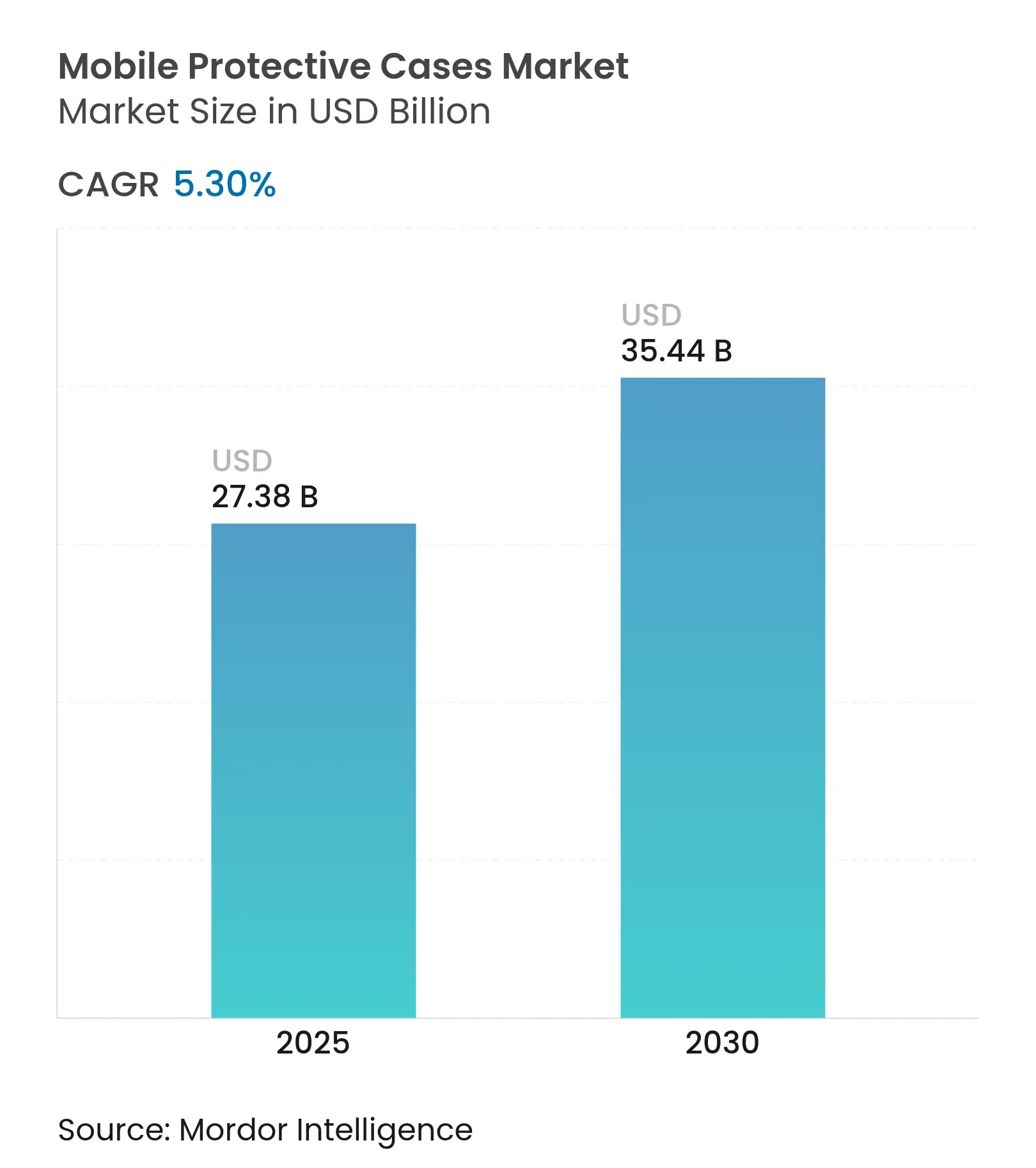

| Market Size (2025) | USD 27.38 Billion |

| Market Size (2030) | USD 35.44 Billion |

| Growth Rate (2025 - 2030) | 5.30 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The mobile protective cases market was valued at USD 27.38 million in 2025 and is forecast to reach USD 35.44 million by 2030, advancing at a 5.30% CAGR during 2025-2030. Rising premium-smartphone adoption, continuous material innovation, and omnichannel retail strategies sustain the growth momentum despite price competition. Silicon remains the dominant material, yet leather and next-generation biodegradable thermoplastic polyurethane gain ground as environmental regulations tighten. With the rise in e-commerce sales, online channels are steadily surpassing offline formats. The Asia-Pacific region continues to lead, driven by strong integrated supply chains and a growing middle-income population. In this dynamic market, competitive differentiation now relies on features such as wireless-charging compatibility, antimicrobial finishes, and sustainable sourcing, aligning with stricter PFAS and plastics regulations.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in premium-smartphone sales

Surge in premium-smartphone sales

| +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:Global, with concentration in North America and Asia-Pacific |

Impact Timeline

:

Medium term (2-4 years)

|

Customization and personalization trend

Customization and personalization trend

| +0.8% | Global, led by North America and Europe | Long term (≥ 4 years) | |||

Material and design innovation

Material and design innovation

| +0.9% | Global, with research centers in North America and Europe | Medium term (2-4 years) | |||

Fashion and lifestyle influence

Fashion and lifestyle influence

| +0.7% | Global, strongest in developed markets | Long term (≥ 4 years) | |||

Growth of e-commerce and digital retail

Growth of e-commerce and digital retail

| +1.1% | Global, accelerated in North America | Short term (≤ 2 years) | |||

Consumer focus on multifunctionality

Consumer focus on multifunctionality

| +0.6% | Global, early adoption in tech-savvy markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in premium-smartphone sales

The proliferation of flagship smartphones is transforming the demand for protective cases. In India, smartphone exports are expected to reach USD 21 billion by 2025. Apple is a key contributor, with iPhone exports accounting for nearly 70% of the total and generating USD 14.39 billion in 2024, according to the India Brand Equity Foundation[1]Source: India Brand Equity Foundation, "Smartphone exports beat estimates", ibef.org. Premium smartphone users focus on protecting their investments, driving demand for cases that offer superior protection against drops, scratches, and wear. As premium smartphone sales grow, consumers are increasingly spending USD 30-80 on protective solutions for devices priced between USD 800-1,200. This trend is particularly prominent in developed markets, where extended device replacement cycles, often exceeding three years, highlight the need for durable protection. Additionally, advanced features in flagship smartphones, such as wireless charging and sophisticated camera systems, are driving demand for specialized case designs that integrate these technologies without compromising functionality.

Material and design innovation

Breakthroughs in sustainable materials are redefining industry standards by addressing environmental concerns while maintaining performance capabilities. Algenesis Corporation has developed a biodegradable thermoplastic polyurethane (TPU) that decomposes rapidly through composting. Soil microorganisms break down this TPU into harmless nutrients, effectively mitigating the issue of microplastics. This advancement is particularly relevant given the concerns over toxic substances in mobile phone protective cases, where studies have detected polybrominated diphenyl ethers (PBDEs) and heavy metals in traditional materials. Additionally, advanced manufacturing techniques are enabling precise engineering of thermal management properties, which are critical for wireless charging. This is especially important as the Federal Communications Commission (FCC) enforces a specific absorption rate (SAR) limit of 1.6 W/kg for general population exposure. Beyond sustainability, material innovations now include antimicrobial properties, enhanced drop protection, and smart feature integration, transforming protective cases into advanced technology platforms. For instance, in September 2024, Apple introduced the iPhone 16 Plus Clear Case, a Silicone Case with MagSafe technology.

Growth of e-commerce and digital retail

Digital retail transformation is accelerating consumers' access to and customization of products. These online platforms enable direct-to-consumer models, eliminating traditional retail markups and delivering personalization services that were previously unavailable through conventional channels. E-commerce platforms provide a wide range of phone case styles, materials (spanning from plastic to eco-friendly options), and price points. This variety is challenging to replicate in traditional retail, attracting consumers who prioritize both functionality and unique designs. The impact of digital retail extends beyond sales, enhancing supply chain efficiency and enabling manufacturers to quickly respond to design trends and consumer preferences. However, the shift to online shopping has also increased the prevalence of counterfeit products. Small parcel shipments often evade regulatory oversight, creating both challenges and opportunities for legitimate manufacturers. As internet usage grows, so does the reach and effectiveness of e-commerce platforms for phone cases and accessories. For instance, in 2024, the International Telecommunication Union (ITU) reported 5.5 billion global internet users[2]Source: International Telecommunication Union (ITU), "Internet Use", itu.int. This increased internet adoption supports features like customer reviews, virtual try-ons, and hassle-free returns, significantly enhancing consumer confidence in purchasing phone cases online.

Fashion and lifestyle influence

As consumer perceptions evolve, protective cases have transitioned from mere utilitarian accessories to sought-after fashion statements. This shift is not only driving the expansion of the premium segment but also diversifying designs. Today's consumers are increasingly inclined to buy multiple cases tailored for various occasions, broadening the market beyond the traditional one-case-per-device mindset. Younger demographics, in particular, are heavily influenced by fashion, viewing smartphone accessories as extensions of their personal expression. Pop culture references such as TV shows, movies, music, and celebrities help consumers express their fandom and connect with like-minded individuals. Furthermore, designs can reflect emotions, make social or political statements, or showcase national or cultural pride. The growing lifestyle integration of protective cases mirrors a broader trend in consumer electronics, emphasizing personalization and aesthetic customization. This trend is further bolstered by manufacturing technologies that facilitate cost-effective, small-batch production of unique designs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Counterfeit and look-alike products

Counterfeit and look-alike products

| -0.9% | Global, concentrated in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

Global, concentrated in emerging markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Plastics regulations and PFAS restrictions Plastics regulations and PFAS restrictions | -0.6% | North America and Europe, expanding globally | Medium term (2-4 years) | |||

Thermal-management risk with reverse charging

Thermal-management risk with reverse charging

| -0.4% | Global, acute in premium segments | Medium term (2-4 years) | |||

Price commoditization and margin squeeze Price commoditization and margin squeeze | -0.8% | Global, most severe in mass market segments | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Counterfeit and look-alike products

Counterfeit products are stifling the growth of legitimate markets. Mobile phone accessories, with their straightforward manufacturing processes and lucrative profit margins, are especially susceptible. This allows counterfeiters to churn out convincing replicas at a fraction of the cost. E-commerce platforms, often lacking robust verification mechanisms, unintentionally aid in the spread of counterfeits. The challenge is further compounded for customs authorities, who grapple with enforcement due to the nature of small parcel shipments. In Italy, the "Ministry of the Interior" reported 509 cases of e-commerce counterfeits in 2023[3]Source: Ministry of the Interior, "Criminal Analysis Service, governo.it. Beyond the economic ramifications, the safety concerns are alarming: many counterfeit products bypass rigorous material testing, potentially harboring hazardous substances that endanger consumer health. Enforcing intellectual property rights is a daunting task, especially in areas where lax regulatory oversight and minimal international collaboration embolden counterfeiting operations.

Plastics regulations and PFAS restrictions

Manufacturers face rising compliance costs and challenges in material sourcing due to tightening regulations on per- and polyfluoroalkyl substances (PFAS) and plastic waste management. Washington State's Safer Products for Washington program has flagged organohalogen flame retardants as priority chemicals, pushing for safer alternatives in plastic device casings. While PFAS restrictions differ across jurisdictions, Maine and Minnesota have set comprehensive laws mandating disclosure and eventual removal from all products. This creates a compliance maze for manufacturers catering to diverse markets. The European Commission's 2030 roadmap aims to phase out harmful chemicals, further complicating matters for manufacturers. They now face the dual challenge of investing in alternative material development and restructuring their supply chains. Smaller manufacturers, with limited resources for rigorous material testing and certification, feel the brunt of these compliance costs. This scenario could lead to a market consolidation, favoring larger players better equipped to navigate regulatory challenges.

By Case Type: Back Plate Cases Balance Protection and Access

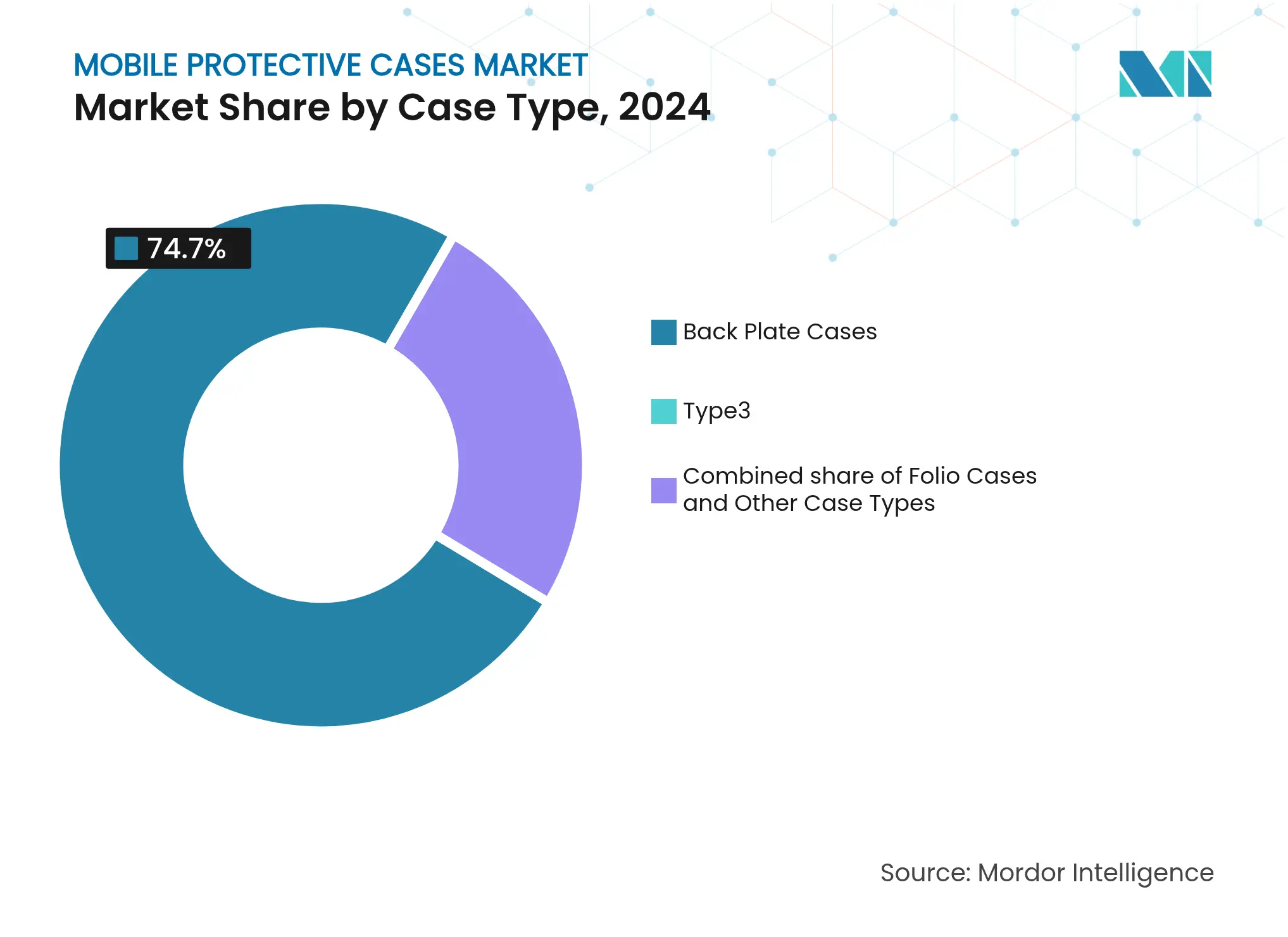

Back plate designs dominated the mobile protective cases market in 2024 with a 74.70% revenue share and are projected to grow at a 5.64% CAGR (2025-2030), supported by their slim profile and manufacturing cost advantages. Device makers recommend these single-piece shells because they leave displays unhindered while covering glass backs that are prone to shattering. The launch of the Qi2 magnetic profile, which elevates wireless-charging efficiencies to as high as 90%, positions compatible back plate cases for enhanced demand as consumers perceive tangible charging speed improvements. Over the forecast period, folio and rugged variants will remain niche, serving professional or outdoor users who require card slots or dustproof sealing.

Recent flagship smartphone models, featuring reverse-wireless-charging capabilities, have driven a significant shift in design priorities toward improved heat dissipation. To address this, manufacturers are increasingly integrating materials such as graphite sheets or aluminum inserts, which effectively diffuse localized hotspots and ensure optimal device performance. Suppliers capable of developing back plates that combine thermal conductivity with RF transparency are well-positioned to establish strategic partnerships with OEMs. This development highlights the critical role of the back plate segment in the evolving mobile protective cases market, as it becomes a key component in meeting both functional and performance demands.

Note: Segment shares of all individual segments available upon report purchase

By Material Type: Silicon Dominance Faces Environmental Crosswinds

Silicon accounted for 56.64% of 2024 revenue, reflecting its elasticity, scratch resistance, and labor-efficient molding. Silicone cases are becoming more functional as they increasingly incorporate features like antimicrobial coatings, MagSafe compatibility, and support for wireless charging. Yet anticipated PFAS legislation and growing consumer eco-consciousness bolster demand for leather and plant-based polymers that post a 6.68% CAGR through 2030. Luxury handset owners gravitate toward full-grain leather, while sustainability-minded buyers choose biodegradable TPU lines.

Amid growing public health concerns during 2024-2025, material developers are actively incorporating silver-ion and zinc additives into products to inhibit microbial growth on high-touch surfaces. This innovation aims to address hygiene demands in various applications. Meanwhile, silicon continues to hold a dominant position in the mobile protective cases market. However, its leadership is increasingly being contested, as evidenced by a notable rise in patent filings for hybrid silicone-textile lattices. These advanced materials offer enhanced durability, including the ability to withstand drops from heights of up to 2 meters, signaling a shift in market dynamics.

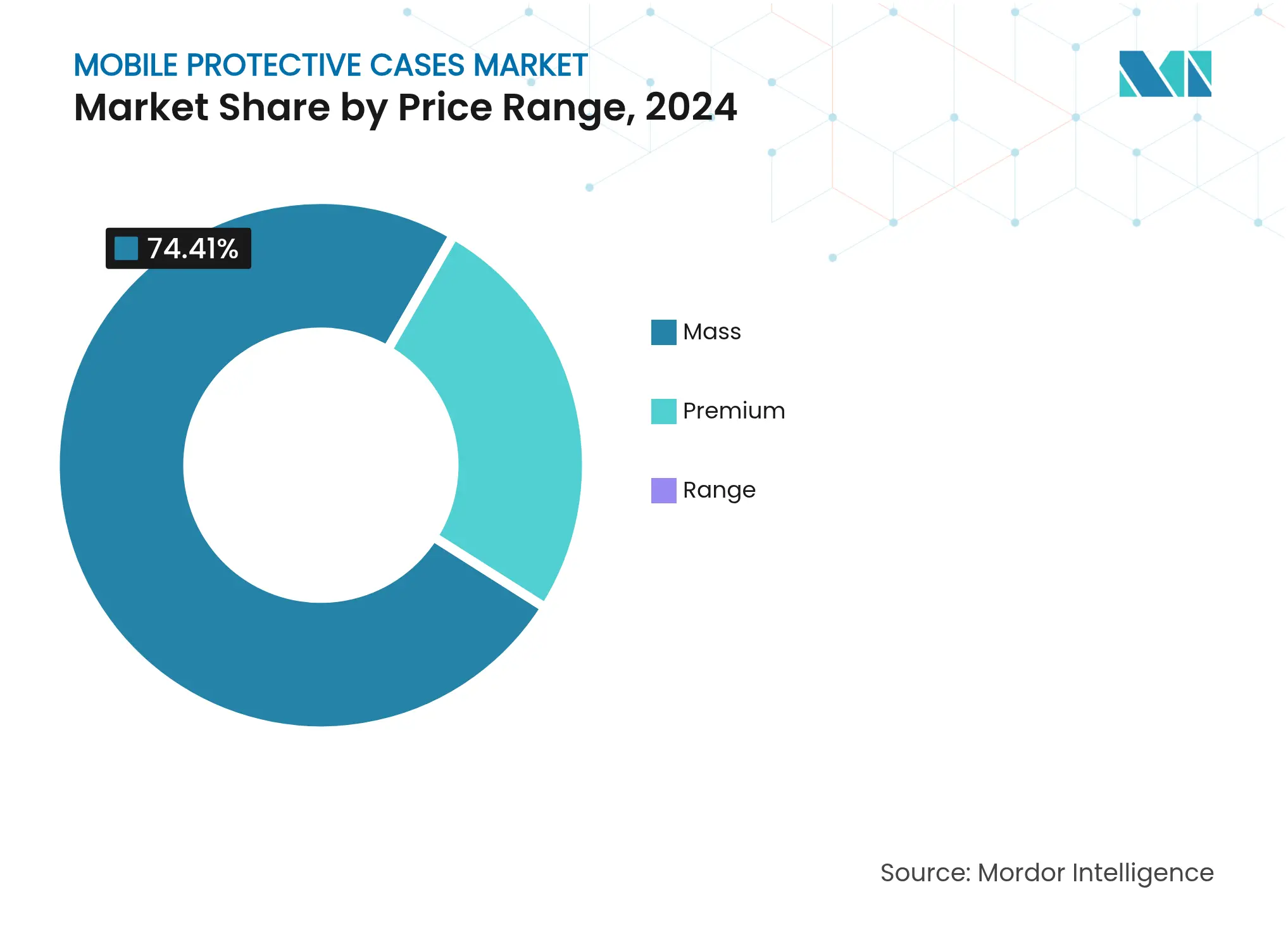

By Price Range: Mass Market Stability Meets Premium Upswing

Mass-market SKUs retained 74.41% of global revenue in 2024. Robust availability at hypermarkets and convenience stores ensures their continued prevalence among first-time smartphone owners, particularly in emerging economies where cost sensitivity shapes accessory purchases. Premium models, sporting genuine leather, MagSafe magnets, or antimicrobial surfaces, capture incremental upgrades as aging devices need style refreshes. The premium cohort’s 6.57% CAGR demonstrates that buyers increasingly regard phone cases as lifestyle accents and status signals rather than pure protective gear.

Brands in the mobile protective cases market are shifting their focus. Rather than just prioritizing protection levels, they're now spotlighting elements like the origin of materials, carbon footprint certifications, and ergonomic touches like chamfered edges to minimize pinkie fatigue. These features cater to environmentally conscious consumers and those seeking enhanced usability. Furthermore, to safeguard profit margins and bolster customer loyalty, brands are tapping into direct-to-consumer online platforms. By offering personalized options, such as complimentary engraving services, they aim to create a more engaging and tailored customer experience.

By Distribution Channel: Digital Acceleration Reshapes Reach

Offline channels maintained a 67.10% share of global revenue in 2024 as consumers value instant gratification and tactile inspection. Retailers showcase drop tests and mock handsets to illustrate fit, crucial for higher-priced lines. Online marketplaces, recording a 7.21% CAGR through 2030, extend catalog depth beyond store shelving limits. The surge is reinforced by mobile-first shopping interfaces and frictionless returns policies that lower perceived risk. Features such as customer reviews, virtual try-ons, and hassle-free returns on e-commerce platforms build trust and enhance the purchasing experience.

Hybrid click-and-collect programs are gaining traction, allowing buyers to reserve exclusive designs online and conveniently pick them up the same day from malls. These omnichannel strategies enable established retailers to bridge the gap between online and offline shopping experiences. By leveraging physical service desks for additional offerings such as repairs and recycling take-back programs, retailers not only enhance customer convenience but also promote sustainability. This integrated approach plays a crucial role in reinforcing brand trust and loyalty within the mobile protective cases market.

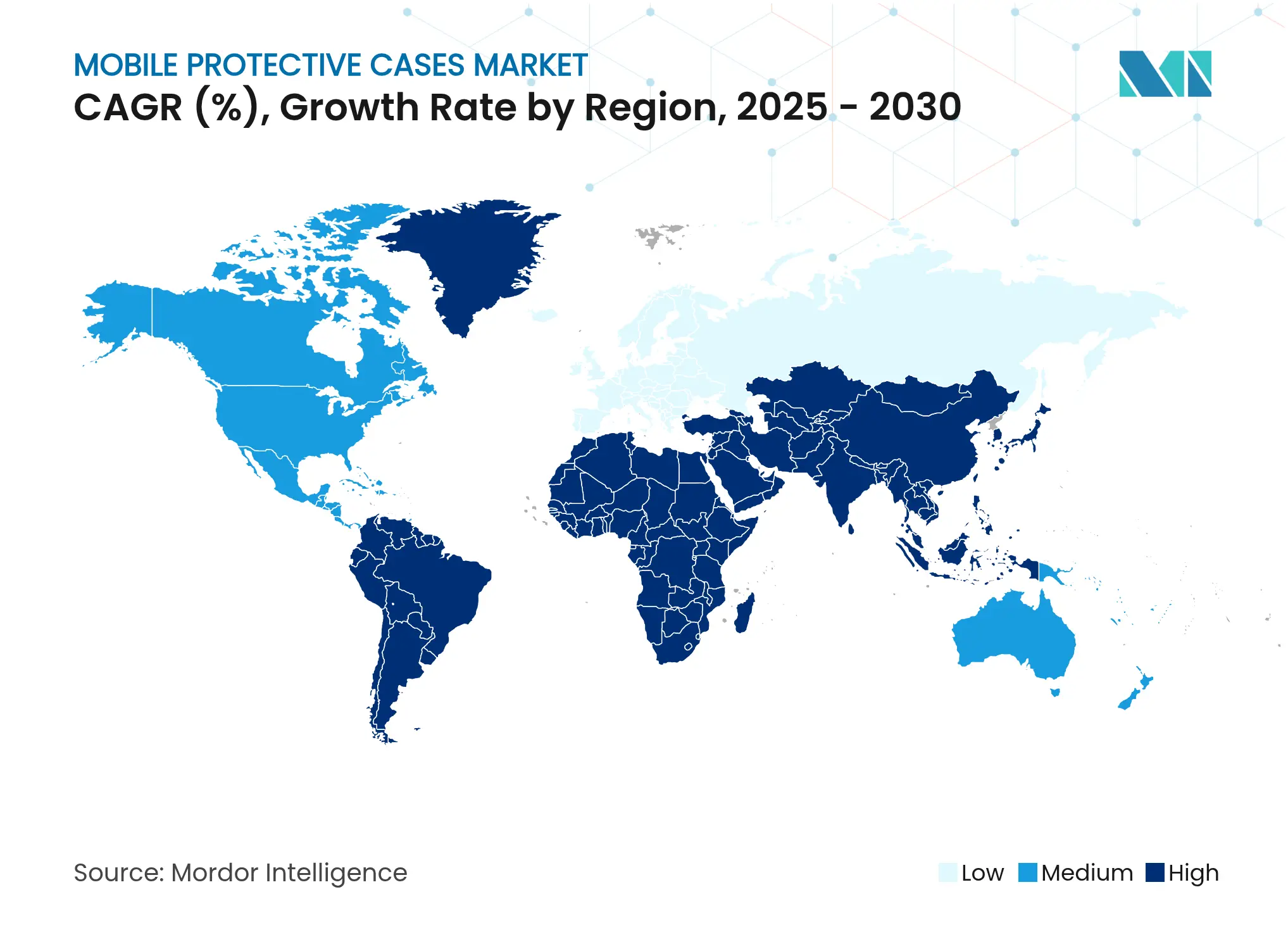

Asia-Pacific led the mobile protective cases market in 2024 with 43.73% revenue share, anchored by integrated handset manufacturing clusters in China, South Korea, and Vietnam. Local suppliers benefit from just-in-time logistics that shorten concept-to-launch cycles to under 60 days. Rising disposable incomes in India and Indonesia spur mid-tier smartphone upgrades, expanding the addressable base for entry-level cases. Government broadband initiatives further increase smartphone penetration, widening accessory demand.

In North America, the market presents a mature yet profitable environment where flagship handsets gain widespread adoption, supported by handset subsidies. Premium smartphone cases, featuring advanced attributes such as MagSafe rings for enhanced compatibility, antimicrobial coatings for improved hygiene, and warranty-backed drop protection claims, are increasingly appealing to consumers. Additionally, stringent chemical regulations enforced by the FCC and state-level authorities are driving material innovation. These regulations introduce additional compliance costs, which tend to favor well-established brands with the resources to adapt. In Europe, the market reflects similar trends observed in North America but is further shaped by stronger consumer activism. European consumers place greater emphasis on product recyclability and carbon labeling, pushing sustainability to the forefront. This shift has prompted retailers to prioritize and promote eco-scored product assortments, aligning with the growing demand for environmentally responsible options.

The Middle East and Africa market grows the fastest, posting a projected 7.65% CAGR through 2030. Youthful demographics and rapid 5G rollouts in Gulf economies boost high-spec handset uptake. E-commerce infrastructure improves through cross-border logistics hubs in the United Arab Emirates, widening product availability. Conversely, currency volatility in parts of Africa sustains demand for mass-market cases, yet growing urban centers such as Lagos and Nairobi provide footholds for premium lines.

Market Concentration

The mobile protective cases market demonstrates moderate fragmentation, with established players leveraging their brand recognition and distribution networks, while emerging competitors focus on niche opportunities through specialized materials and direct-to-consumer strategies. Prominent players in the market include Otter Products LLC, Spigen Inc., Casetagram Limited, Incipio LLC, and Belkin International inc, among others. The market remains relatively unconcentrated, as low manufacturing barriers allow new entrants to compete effectively in specific segments. However, larger players benefit from scale advantages in mass-market categories. Technology integration increasingly defines competitive positioning, with features like wireless charging compatibility, antimicrobial treatments, and sustainable materials becoming critical differentiators over basic protection capabilities.

Companies are prioritizing vertical integration and supply chain optimization to control material sourcing and manufacturing quality while minimizing reliance on third-party suppliers. Patent portfolios related to wireless charging integration and advanced materials create competitive advantages. For example, ENORCOM Corporation holds patents for mobile device security systems and intelligent connection mechanisms.

Innovative manufacturers find opportunities in sustainable materials and multifunctional designs, as regulatory compliance and shifting consumer preferences set entry barriers. These barriers not only limit market entry for new players but also encourage existing participants to invest in research and development to stay competitive. Competitive dynamics are swayed by industry standards, notably the certification requirements set by the Wireless Power Consortium. Notably, Qi certification has emerged as a prerequisite for those aiming to tap into the premium market segment, ensuring product compatibility and quality assurance for consumers.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Mobile phone protective cases are designed to attach to or grip a mobile phone and are well-accepted and fashionable accessories for various phones (including smartphones). The mobile protective cases market is segmented by product type into black plate cases, folio cases, and other case types; by category into mass and premium; by distribution channel into online retail and offline retail; and by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

Unlocking Opportunities in the Headwear Market

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.