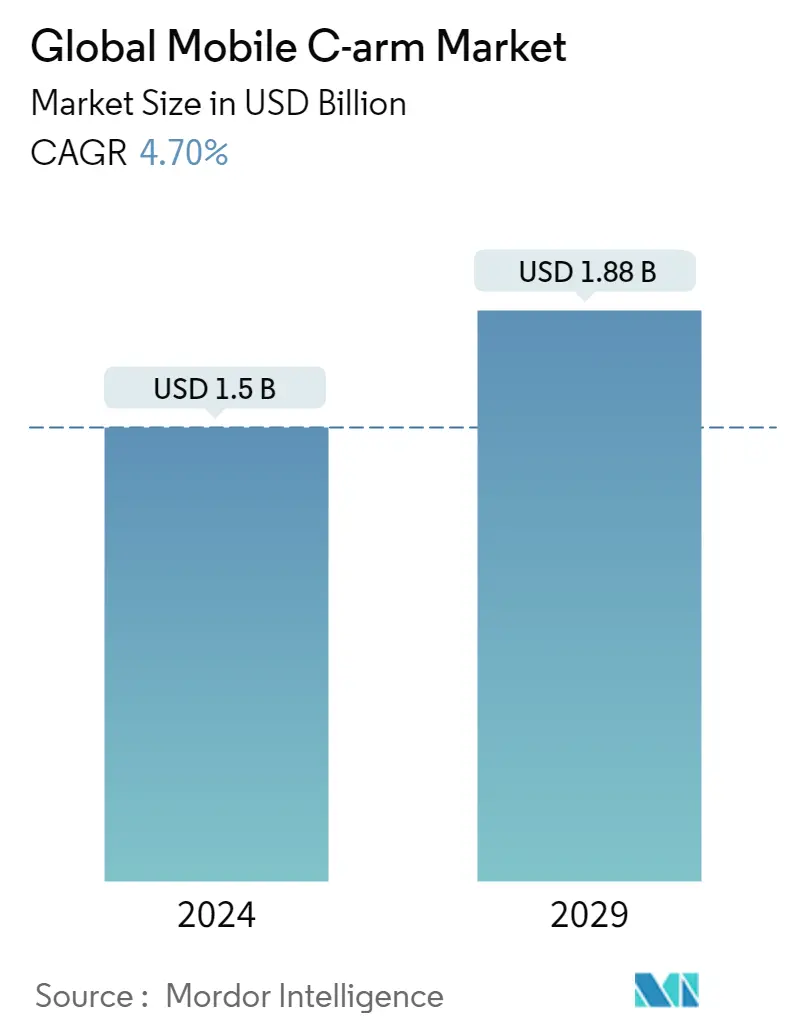

Market Size of Global Mobile C-arm Industry

| Study Period | 2019 - 2029 |

| Market Size (2024) | USD 1.50 Billion |

| Market Size (2029) | USD 1.88 Billion |

| CAGR (2024 - 2029) | 4.70 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Mobile C-arms Market Analysis

The Global Mobile C-arm Market size is estimated at USD 1.5 billion in 2024, and is expected to reach USD 1.88 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

COVID-19 has had an unprecedented impact on the growth of the mobile c-arms market. As with the upsurge in COVID-19 cases, many elective surgeries were halted or postponed for the time being. For instance, the PLOS ONE Journal article titled "The Impact of the COVID-19 pandemic on waiting times for elective surgery patients: A Multicenter Study" published in July 2021 reported that elective procedure incidence decreased rapidly at the onset of the first COVID-19 wave in March 2020. It was also reported that in May 2020 and thereafter until November, waiting times were longer, with monthly increases varying between 7% and 34% in elective surgeries. Further, the waiting times were longer in 2020 for gastrointestinal and genitourinary diseases and neoplasm surgeries. Since C-arms are used in image-guided procedures that are mostly elective and were postponed due to COVID-19, such a delay in elective surgeries has impacted the growth of the market.

Factors such as the growing burden of chronic diseases, technological advancement in imaging capabilities, and the launch of new products in the market are propelling the growth of the market. The growing burden of chronic disease and surgeries is also propelling the growth of the market. For instance, Thoracic Cardiovascular Surgery Journal article titled "German Heart Surgery Report 2020: The Annual Updated Registry of the German Society for Thoracic and Cardiovascular Surgery", published in June 2021, there was a total of 92,809 operations classified as heart surgery procedures in the classical sense, of which 29,444 were isolated coronary artery bypass grafting procedures, 35,469 were isolated heart valve procedures. Thus, a high number of heart procedures and operations are being performed around the world, which is expected to drive the growth of the mobile C-arms market.

Additionally, the increasing focus of market players on improving the efficiency and workflow of the system through the advancements in the products is also propelling the growth of the market. For instance, in July 2020, Philips Healthcare reported two major innovations to its Zenition mobile C-arm platform, which now includes a new Table Side User Interface and an extension integrating intravascular ultrasound (IVUS). With the change to the Table Side User Interface, clinicians will be able to operate the C-arm inside a sterile field and IVUS for peripheral vascular procedures, potentially streamlining activity and workflow in the operating room. Such advancements are also boosting the growth of the market.

However, the high procedural and equipment costs and a lack of skilled professionals may hinder the growth of the market over the forecast period.

Mobile C-arms Industry Segmentation

As per the scope of the report, a mobile C-arm is a medical imaging device that is based on X-ray technology and can be used flexibly. Hence it is also known as a portable c-arm. It is called a C-arm as a C-shaped arm is used to connect the X-ray source and X-ray detector to one another. These are used for a range of diagnostic imaging and minimally invasive surgical procedures. These fluoroscopy devices are also referred to as image intensifiers. The mobile C-arm market is segmented by Product Type (Mini C-arms, Full-Size C-arms, and Others), Application (Cardiology, Gastroenterology, Neurology, Orthopedics and Trauma, Oncology, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD billion) for the above segments.

| By Product Type | |

| Mini C-arms | |

| Full Size C-arms | |

| Others (Compact C-arms, Super C-arms) |

| By Application | |

| Cardiology | |

| Gastroenterology | |

| Neurology | |

| Orthopedics and Trauma | |

| Oncology | |

| Other Applications |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Global Mobile C-arm Market Size Summary

The mobile C-arm market is poised for steady growth over the forecast period, driven by factors such as the increasing prevalence of chronic diseases and advancements in imaging technology. The market has experienced disruptions due to the COVID-19 pandemic, which led to delays in elective surgeries, thereby impacting the demand for mobile C-arms used in these procedures. However, the introduction of innovative products and enhancements in system efficiency and workflow by key players is expected to propel market growth. The mini C-arms segment, in particular, is anticipated to witness significant expansion due to their advantages in fluoroscopy of extremities and the rising incidence of road injuries and orthopedic conditions. Regulatory approvals and strategic distribution agreements further bolster the market's expansion, especially in regions like North America, where a well-developed healthcare infrastructure and a high burden of chronic diseases drive demand.

The North American region holds a significant share of the mobile C-arm market, supported by technological advancements and a robust healthcare system. The approval of advanced medical imaging products by regulatory bodies such as the FDA and Health Canada contributes to market growth in this region. Strategic initiatives, including collaborations and distribution agreements, enhance the geographical presence of market players, further driving growth. The market is moderately fragmented, with multinational companies like Siemens Healthineers, GE Healthcare, and Philips leading in market share. These players are actively engaged in product development and strategic partnerships to increase market penetration and improve surgical outcomes. Overall, the mobile C-arm market is expected to experience robust growth, with key players continuing to innovate and expand their offerings.

Global Mobile C-arm Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Growing Burden of Chronic Diseases, Road Injuries Coupled With Rising Geriatric Population

-

1.2.2 Technological Advancements in the Imaging Capabilities

-

-

1.3 Market Restraints

-

1.3.1 High Procedural and Equipment Cost

-

1.3.2 Lack of Skilled Professionals

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD million)

-

2.1 By Product Type

-

2.1.1 Mini C-arms

-

2.1.2 Full Size C-arms

-

2.1.3 Others (Compact C-arms, Super C-arms)

-

-

2.2 By Application

-

2.2.1 Cardiology

-

2.2.2 Gastroenterology

-

2.2.3 Neurology

-

2.2.4 Orthopedics and Trauma

-

2.2.5 Oncology

-

2.2.6 Other Applications

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

2.3.2.4 Italy

-

2.3.2.5 Spain

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 Australia

-

2.3.3.5 South Korea

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Middle-East and Africa

-

2.3.4.1 GCC

-

2.3.4.2 South Africa

-

2.3.4.3 Rest of Middle-East and Africa

-

-

2.3.5 South America

-

2.3.5.1 Brazil

-

2.3.5.2 Argentina

-

2.3.5.3 Rest of South America

-

-

-

Global Mobile C-arm Market Size FAQs

How big is the Global Mobile C-arm Market?

The Global Mobile C-arm Market size is expected to reach USD 1.50 billion in 2024 and grow at a CAGR of 4.70% to reach USD 1.88 billion by 2029.

What is the current Global Mobile C-arm Market size?

In 2024, the Global Mobile C-arm Market size is expected to reach USD 1.50 billion.