Military Transport Aircraft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

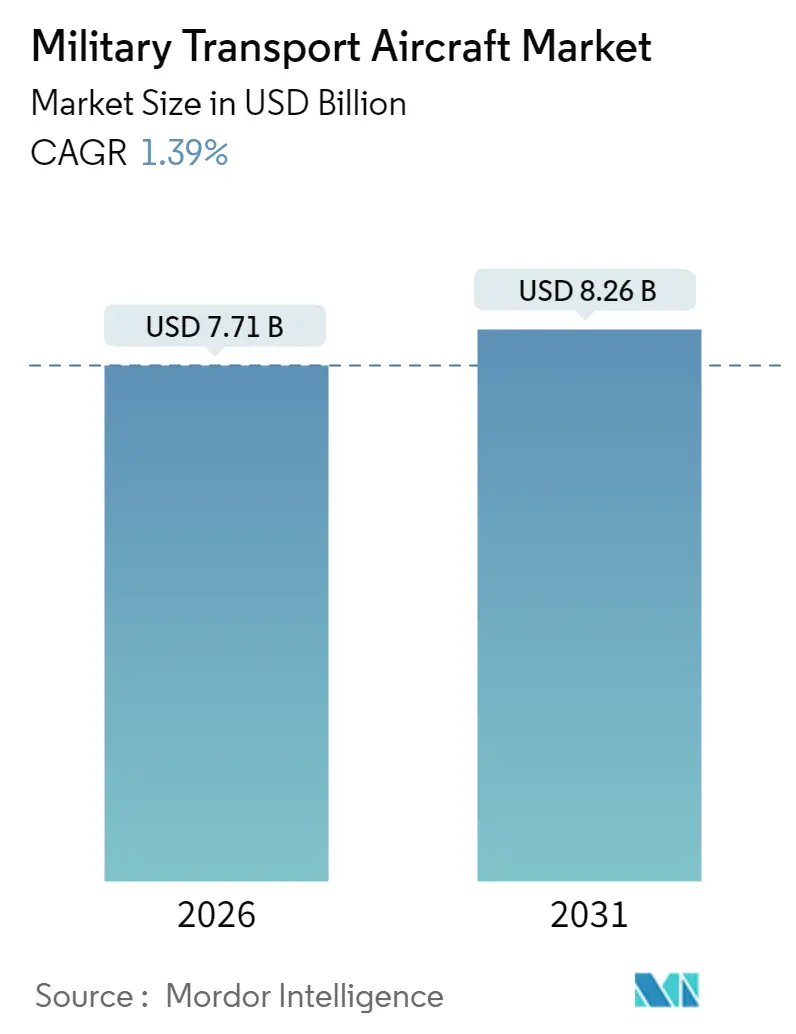

| Market Size (2026) | USD 7.71 Billion |

| Market Size (2031) | USD 8.26 Billion |

| Growth Rate (2026 - 2031) | 1.39% CAGR |

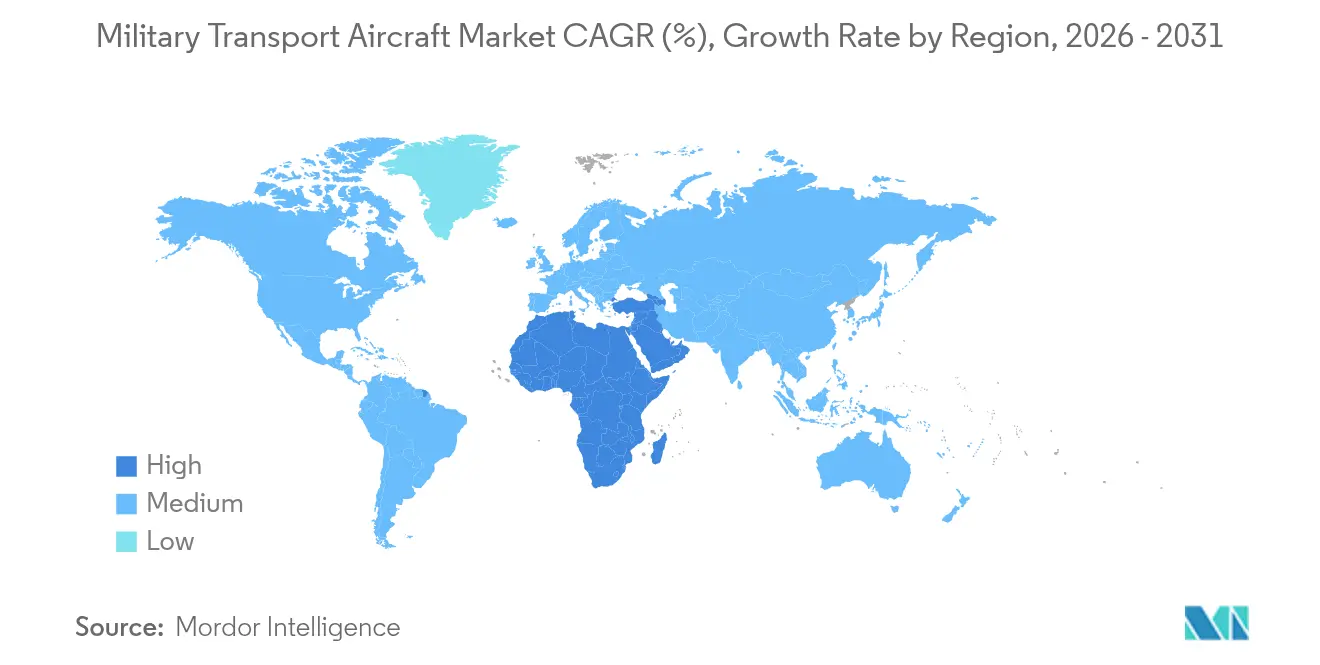

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

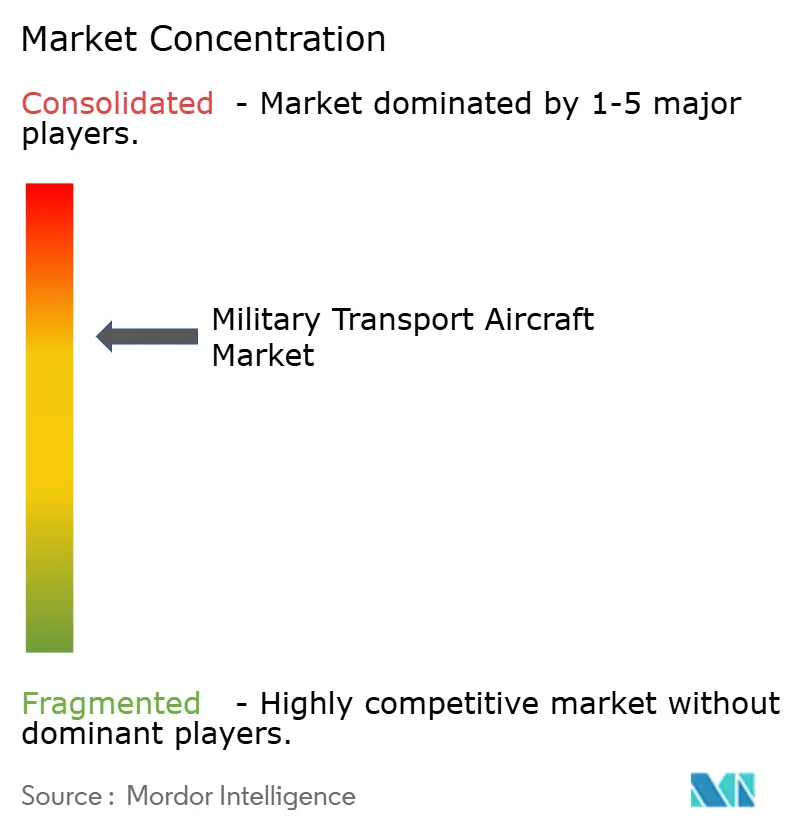

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Transport Aircraft Market Analysis by Mordor Intelligence

The military transport aircraft market was valued at USD 7.60 billion in 2025 and estimated to grow from USD 7.71 billion in 2026 to reach USD 8.26 billion by 2031, at a CAGR of 1.39% during the forecast period (2026-2031). Current expansion stems from heightened geopolitical tensions, urgent humanitarian operations, and programmed fleet renewal cycles. Asia‐Pacific defense ministries continue to order heavy strategic platforms while smaller nations favor light and medium airlifters that require lower infrastructure investment. Modernization programs increasingly specify open-architecture avionics, digital-thread maintenance suites, and multi-role reconfigurability, enabling operators to reduce downtime and expand mission sets. Although procurement budgets remain sound, supply-chain bottlenecks for composite structures and aero-engines restrain annual deliveries, causing manufacturers to negotiate longer lead times and activate additional Tier-2 suppliers. Competitive dynamics now feature indigenous entrants from China, India, and South Korea contesting the traditional dominance of Airbus, Boeing, and Lockheed Martin, an evolution likely to reshape export patterns through 2030.

Key Report Takeaways

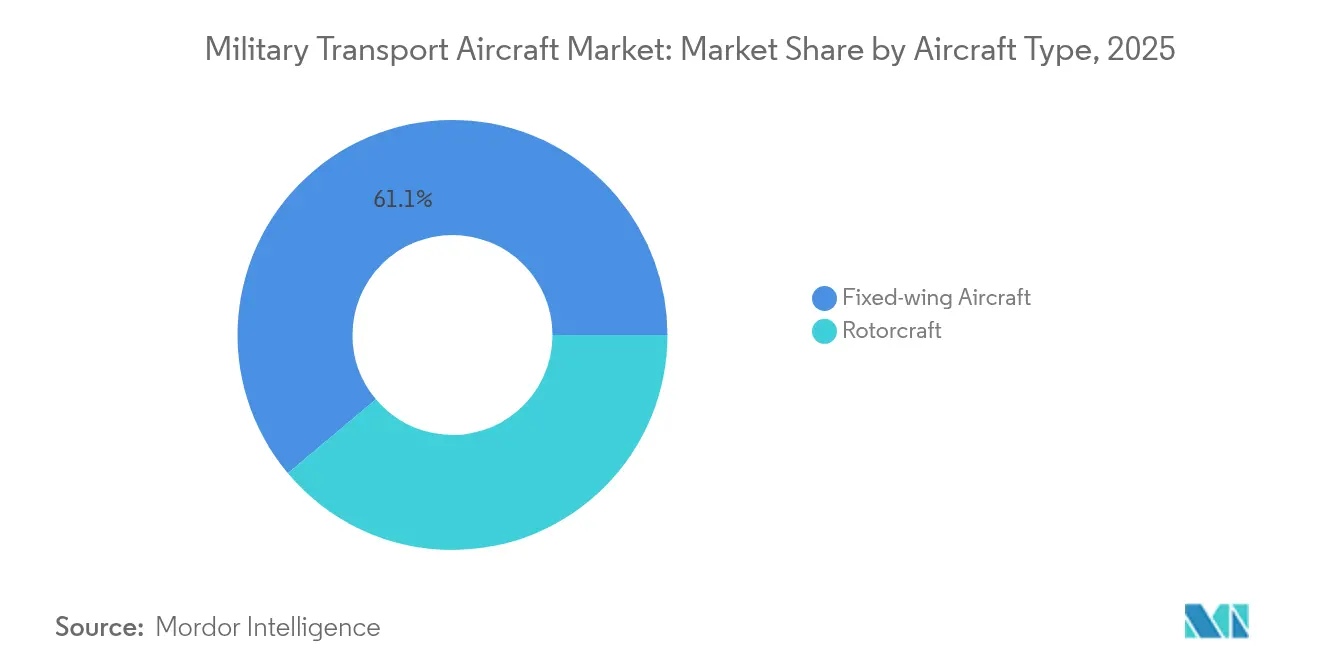

- By aircraft type, fixed-wing platforms led the military transport aircraft market with 61.12% of the market share in 2025; rotorcraft are forecasted to advance at a 4.20% CAGR through 2031.

- By application, troop and cargo airlifting led the military transport aircraft market with a 44.85% revenue share in 2025; humanitarian and disaster relief is projected to expand at a 5.45% CAGR through 2031.

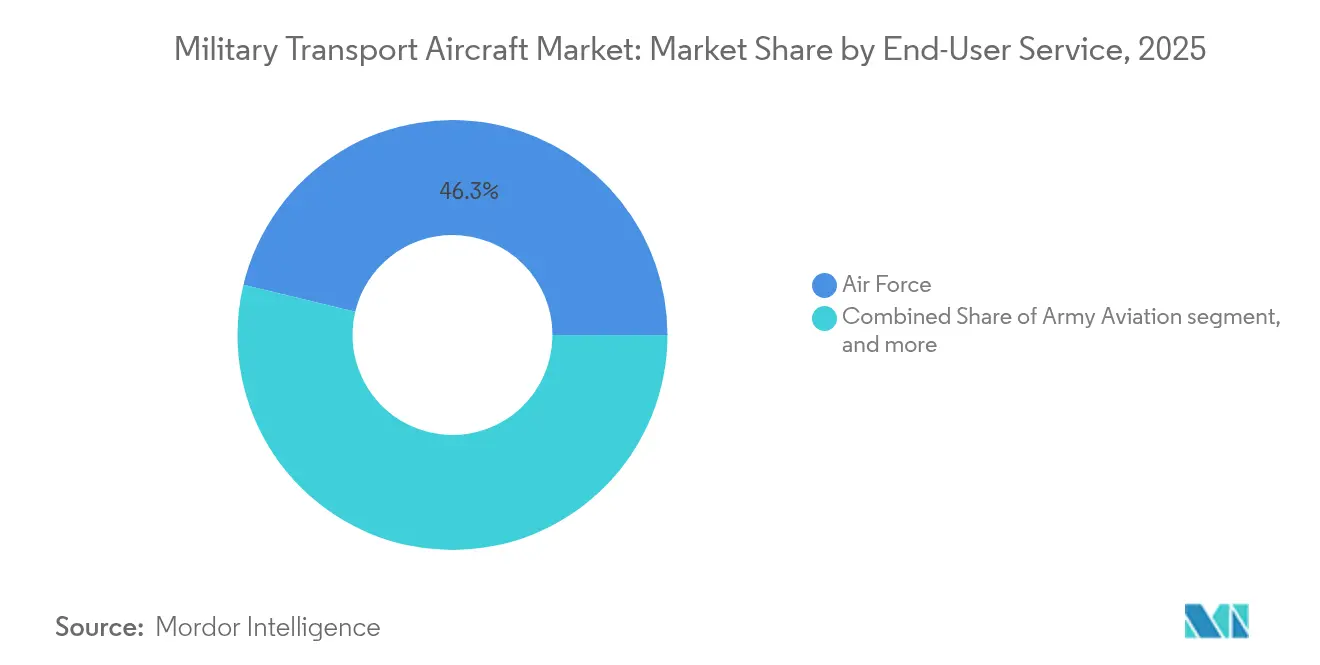

- By end-user service, the Air Force segment held 46.25% of the military transport aircraft market size in 2025, while the paramilitary and coast guard segments are projected to expand at a 3.86% CAGR through 2031.

- By propulsion, turbofan-powered models accounted for a 52.05% share of the military transport aircraft market size in 2025; turboshaft-equipped airframes are expected to post a 5.15% CAGR between 2026 and 2031.

- By geography, the Asia-Pacific region commanded 39.05% of the military transport aircraft market share in 2025, whereas the Middle East and Africa are anticipated to register the fastest growth, with a 3.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Transport Aircraft Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating defense budgets in Asia-Pacific and the Middle East | +0.4% | Asia-Pacific core, Middle East expansion | Medium term (2-4 years) |

| Fleet-modernization programs replacing aging C-130/L-100 and An-26 classes | +0.3% | Global, concentrated in NATO and allied nations | Long term (≥ 4 years) |

| Geopolitical flashpoints spurring urgent lift capability | +0.5% | Europe, Asia-Pacific, spillover to allied nations | Short term (≤ 2 years) |

| Expansion of humanitarian and disaster-relief missions requiring dual-role airlifters | +0.2% | Global, emphasis on disaster-prone regions | Medium term (2-4 years) |

| Digital-thread MRO reducing downtime and enlarging aftermarket revenue pools | +0.2% | Global, concentrated in advanced military operators | Medium term (2-4 years) |

| Emerging eVTOL logistics aircraft for agile last-mile resupply | +0.1% | North America, Europe, early-adopter markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Defense Budgets in Asia-Pacific and the Middle East

Defense outlays rose sharply in 2024, with China allocating USD 296 billion and the United Arab Emirates lifting aviation procurement by 18%. These higher budgets are funneled into new heavy airlift programs, life-extension packages, and local industrial partnerships that include technology transfer clauses.[1]Stockholm International Peace Research Institute, “Global Military Spending Reaches Record USD 2.7 Trillion in 2024,” sipri.org Sustained spending also underpins research into digital logistics suites that cut lifecycle costs and speed mission readiness. Countries in the Gulf Cooperation Council continue to diversify their fleets toward modular A400M and C-130J variants, ensuring interoperability with coalition partners for coalition operations.

Fleet-modernization Programs Replacing Aging C-130/L-100 and AN-26 Classes

Over 60% of legacy C-130A/B and An-26 airframes have exceeded 40 years in service, prompting operators to fast-track competitive tenders that favor new-build C-390, C-295, and KC-390 Millennium models.[2]Lockheed Martin Corporation, “C-130J Super Hercules Fact Sheet,” lockheedmartin.com Sweden’s 2024 order for four C-390 aircraft marks a shift toward higher-throughput airframes with fly-by-wire controls and lower fuel consumption. Eastern European users are simultaneously retiring Soviet-era transport systems to reduce their dependence on Russian supply chains, creating a steady replacement funnel through 2035.

Geopolitical Flashpoints Spurring Urgent Lift Capability

NATO registered a 340% surge in transport sorties during 2024 humanitarian and resupply missions into Eastern Europe.[3]NATO, “Strategic Airlift Capability Factsheet,” nato.int The resulting operational tempo accelerated procurement decisions, reducing traditional five-year evaluations to less than three years. In the Indo-Pacific, Japan boosted C-2 production and Australia advanced C-130J options by 18 months. Such flashpoints place a premium on proven, rapidly available designs, giving incumbents a short-term edge while stressing production capacity.

Expansion of Humanitarian and Disaster-relief Missions Requiring Dual-role Airlifters

Climate-related disasters increased by 23% in 2024, prompting militaries to deploy cargo aircraft for relief, medical evacuation, and food distribution in addition to their combat duties.[4]United Nations Office for Disaster Risk Reduction, “2024 Disasters in Numbers,” undrr.org The A400M and C-130J fleets now feature quick-change medical modules, with certification conducted under the guidance of the International Civil Aviation Organization's Annex 12. Modular interiors maximize utilization rates and help justify investment outlays to finance ministries.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain constraints for widebody composite structures and aero-engines | −0.3% | Global, concentrated in Western manufacturing hubs | Medium term (2-4 years) |

| High total-ownership cost versus potential leased cargo conversions | −0.2% | North America, Europe, cost-sensitive markets | Long term (≥ 4 years) |

| Export-control and ITAR barriers limiting platform addressable markets | −0.2% | Global, affecting non-allied nations | Long term (≥ 4 years) |

| Runway-availability risk in dispersed operations limiting heavy-lift utility | −0.1% | Global, concentrated in contested environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-chain Constraints for Widebody Composite Structures and Aero-engines

Pratt & Whitney’s TP400 line and Toray’s carbon-fiber feedstocks reached 18-month backlogs in 2024, delaying A400M handovers and forcing original equipment manufacturers to resequence production slots. The scarcity raises unit pricing and compels air forces to accept interim capability gaps or pay premium “surge” fees for supplemental charter lift.

High Total-ownership Cost Versus Potential Leased Cargo Conversions

Fully burdened military airlift flight hours average USD 35,000-50,000, double that of commercial B767-300ER freighters in troop-seat configuration. Mid-tier nations, therefore, charter Il-76 or An-124 aircraft for peace-time missions, delaying or reducing outright purchases. Budget agencies request cost-benefit studies comparing life-cycle ownership against ad-hoc leasing, introducing procurement uncertainty through 2028.

Segment Analysis

By Aircraft Type: Fixed-wing Dominance Drives Market Leadership

Fixed-wing transports captured 61.12% of the 2025 military transport aircraft market size, anchored by dependable performers such as the C-130J Super Hercules and A400M Atlas. Continuous block upgrades raise payload-range productivity while preserving interoperability certifications. At the same time, rotorcraft benefit from doctrinal shifts toward point-to-point lift in denied environments, driving a 4.20% CAGR that outpaces the broader military transport aircraft market. The widespread use of composite blades and improved transmission designs raises lift-to-weight ratios, expanding external-sling capacities for the Chinook and CH-53K fleets.

Rotorcraft share gains also reflect special-operations demand for low-signature infiltration, where tilt-rotor platforms like the CV-22 offer jet-class speed combined with vertical takeoff and landing (VTOL) capabilities. However, fixed-wing aircraft remain irreplaceable for inter-theater moves; the C-390 Millennium’s fly-by-wire controls provide civil-certified Category IIIb autoland, allowing entry to fog-prone forward locations. Through 2030, fixed-wing deliveries are expected to stabilize at around 95 aircraft annually, whereas rotary procurement could peak at 140 units as new FLRAA entrants mature.

Note: Segment shares of all individual segments available upon report purchase

By Application: Troop and Cargo Airlifting Dominance Challenged by Humanitarian Growth

Troop and cargo airlifting generated the largest slice of the 2025 military transport aircraft market size, at USD 3.41 billion, equivalent to 44.85% of the total value, and is forecasted to track closely to the overall 1.39% CAGR as nations sustain their strategic lift requirements. The sub-segment benefits from fixed-wing workhorses such as the C-130J and A400M, which together accounted for more than 60% of troop-movement sorties in 2024. Fleet planners prioritize payload-range improvements and rapid re-role configurations, ensuring the segment defends its scale even as growth plateaus. Procurement pipelines in the Asia-Pacific and Europe remain steady. At the same time, North American operators focus on avionics refreshes and service-life extensions, which anchor aftermarket spending within the military transport aircraft market.

By End-User Service: Air Force Share Challenged by Paramilitary Expansion

Air Force branches accounted for 46.25% of global deliveries in 2025, maintaining the largest share of the military transport aircraft market. Strategic commands rely on established fleets of C-17s and Y-20s for long-haul sustainment, with mission-capable rates restored above 80% after recent avionics retrofits. Paramilitary and coast-guard authorities, including homeland security agencies, are now the fastest risers at a 3.86% CAGR, owning missions such as maritime interdiction and disaster relief.

These services are funding light transports with modular roll-on, roll-off sensor pallets, enabling quick shifts between patrol, medevac, or cargo operations. Joint-service procurement boards increasingly favor standard airframes across departments to simplify spares and pilot conversion courses. Such convergence nudges traditional Air Force buyers to accept multi-agency budgeting structures, potentially blurring historical boundaries among service segments.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion Type: Turbofan Stability Contrasts Turboshaft Acceleration

Turbofan-powered airlifters, led by the C-17 Globemaster III, accounted for 52.05% of 2025 revenue in the military transport aircraft market. Their high cruise speed and 4,000 nautical miles unrefueled range satisfy strategic lift mandates. Incremental upgrades focus on FADEC refinements and ceramic matrix composite hot sections that reduce specific fuel consumption by 2%. In contrast, turboshaft propulsion is expected to build momentum with a 5.15% CAGR as helicopter transport continues to escalate.

Next-generation engines, such as the GE Catalyst with a 16:1 overall pressure ratio, promise 20% more power at equal weight, directly boosting sling capacities for future tilt-rotors. Concurrently, turboprop stalwarts like the AE2100D3 sustain their tactical lift roles thanks to proven fuel economy and robustness on rough fields, ensuring a balanced propulsion mix throughout the decade.

Geography Analysis

The Asia-Pacific region accounted for 39.05% of 2025 revenue, solidifying its regional leadership in the military transport aircraft market. Volume comes from continuous Y-20 production, India’s indigenous C-295 line, and Japan’s expanded C-2 build rate. The regional CAGR is forecasted at 1.75%, driven by annual defense budget growth averaging 8.5% across major economies. Capability cooperatives, such as the Quad-spur interoperability requirements, further stimulate joint crew-training contracts.

North America held a 28.50% share, primarily through US Air Force programs, which saw a 12% increase in C-130J flight hours in 2024. Canada’s CC-330 Husky tanker-transport initiative and Mexico’s CN-235 expansion underscore the growing continental demand. Across the Atlantic, Europe accounted for 22.05%, though supply-chain snarls limited A400M outputs to eight units. NATO’s Strategic Airlift Capability rotates C-17s from Pápa Air Base, underscoring the alliance’s reliance on pooled assets.

The Middle East and Africa emerge as the fastest-growing slice with a 3.60% CAGR. Nigeria’s four-unit C-295 order and South Africa’s C-130BZ modernization illustrate how peacekeeping and humanitarian mandates override tight budgets. Gulf states blend Middle East and Africa statistics; the UAE’s fresh C-130J-30s and Qatar’s pending A400M purchase underpin a 2.32% regional CAGR. Shared infrastructure under the African Union mobilizes cross-border airlift operations, easing regulatory hurdles and encouraging cooperative maintenance depots.

Competitive Landscape

The military transport aircraft market exhibits moderate concentration, with Airbus, Lockheed Martin, and Boeing accounting for the majority of fixed-wing revenues. Each firm advances digital twin toolsets to secure post-sale support contracts that can double the program value over the fleet's life. Airbus embeds its predictive maintenance e-Suite on every new A400M, while Lockheed Martin bundles Immersive Crew Training labs with C-130J orders.

Indigenous challengers climb the ladder. China's AVIC plans to deliver 24 Y-20 units in 2024, aiming for 36 units per year by 2026. Tata Advanced Systems delivered the first Indian-built C-295, marking the inauguration of a regional C-295 main assembly line for Embraer. Embraer's KC-390 Millennium won Sweden's four-aircraft deal, demonstrating competitive pricing and multi-mission versatility.

Supply resiliency now determines whether commercial wins are as significant as payload or range. OEMs are diversifying their single-source composite vendors and co-locating line-replaceable-unit stockpiles near their operating bases to achieve 80% availability targets. Meanwhile, export-control constraints continue to filter customer options: China markets the Y-9E to non-aligned states, whereas Western OEMs must navigate ITAR licensing for sensitive subsystems.

Military Transport Aircraft Industry Leaders

Airbus SE

Lockheed Martin Corporation

The Boeing Company

Leonardo S.p.A.

Embraer S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Embraer, the Brazilian aerospace company, inaugurated its office in India. To mark the occasion, the company signed a strategic cooperation agreement with the Mahindra Group to enhance the C-390 Millennium military transport aircraft for the Indian Air Force.

- September 2025: Portugal signed a contract with Embraer, acquiring a sixth KC-390 Millennium transport aircraft and establishing 10 new purchase options for potential acquisitions by allied nations. The Portuguese Air Force, which introduced the KC-390 in 2023, is the first operator globally to expand its initial order.

- September 2025: Sweden agreed to procure four C-390 Millennium military transport aircraft from Embraer. These aircraft will replace the Swedish Hercules planes, which have been in service for over 60 years. The first delivery is scheduled for 2027.

Global Military Transport Aircraft Market Report Scope

| Fixed-wing Transport Aircraft |

| Rotary-wing Transport Aircraft |

| Troop and Cargo Airlifting |

| Humanitarian and Disaster Relief |

| Special Missions (MEDEVAC, SAR, VIP) |

| Air Force |

| Army Aviation |

| Naval/Marine Corps Aviation |

| Joint/Special Operations |

| Paramilitary and Coast Guard |

| Turboprop |

| Turboshaft |

| Turbofan |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Aircraft Type | Fixed-wing Transport Aircraft | ||

| Rotary-wing Transport Aircraft | |||

| By Application | Troop and Cargo Airlifting | ||

| Humanitarian and Disaster Relief | |||

| Special Missions (MEDEVAC, SAR, VIP) | |||

| By End-User Service | Air Force | ||

| Army Aviation | |||

| Naval/Marine Corps Aviation | |||

| Joint/Special Operations | |||

| Paramilitary and Coast Guard | |||

| By Propulsion Type | Turboprop | ||

| Turboshaft | |||

| Turbofan | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Market Definition

- Aircraft Type - All the military aircraft which are used for various applications are included under military aviation market.

- Sub-Aircraft Type - For this study, all the military fixed-wing transport aircraft which are used for troops and cargo carrying are considered.

- Body Type - Various models of fixed-wing transport aircraft are considered in this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms