Military Radars Market Size

| Study Period | 2019 - 2029 |

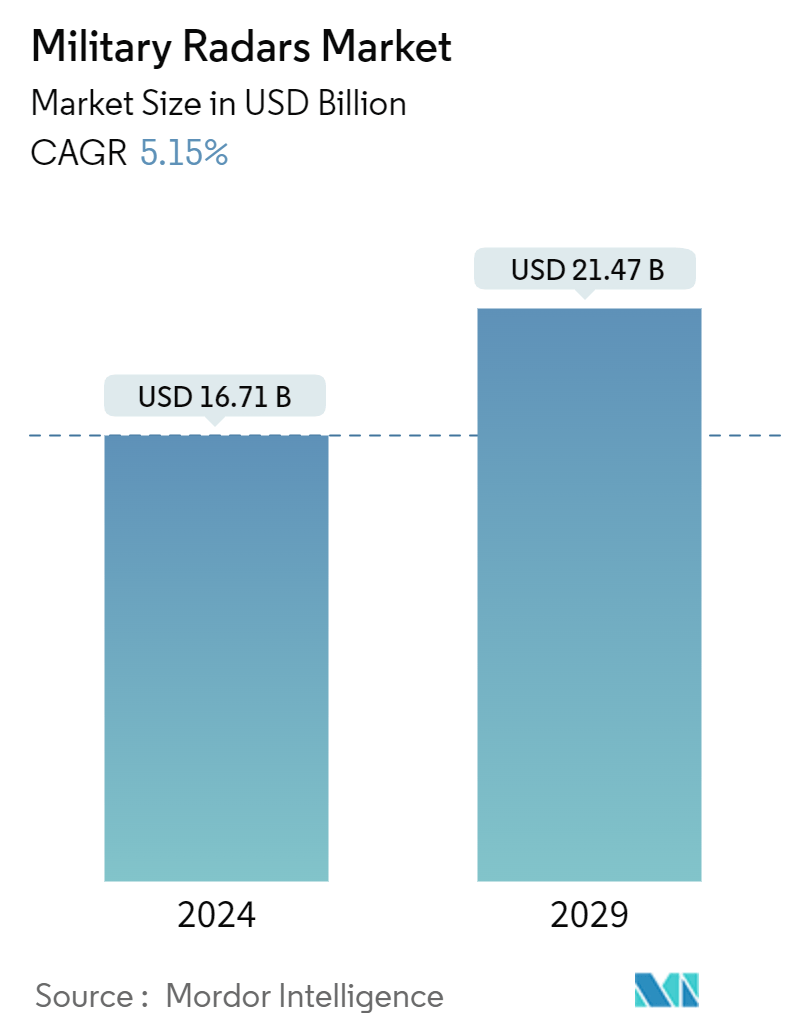

| Market Size (2024) | USD 16.71 Billion |

| Market Size (2029) | USD 21.47 Billion |

| CAGR (2024 - 2029) | 5.15 % |

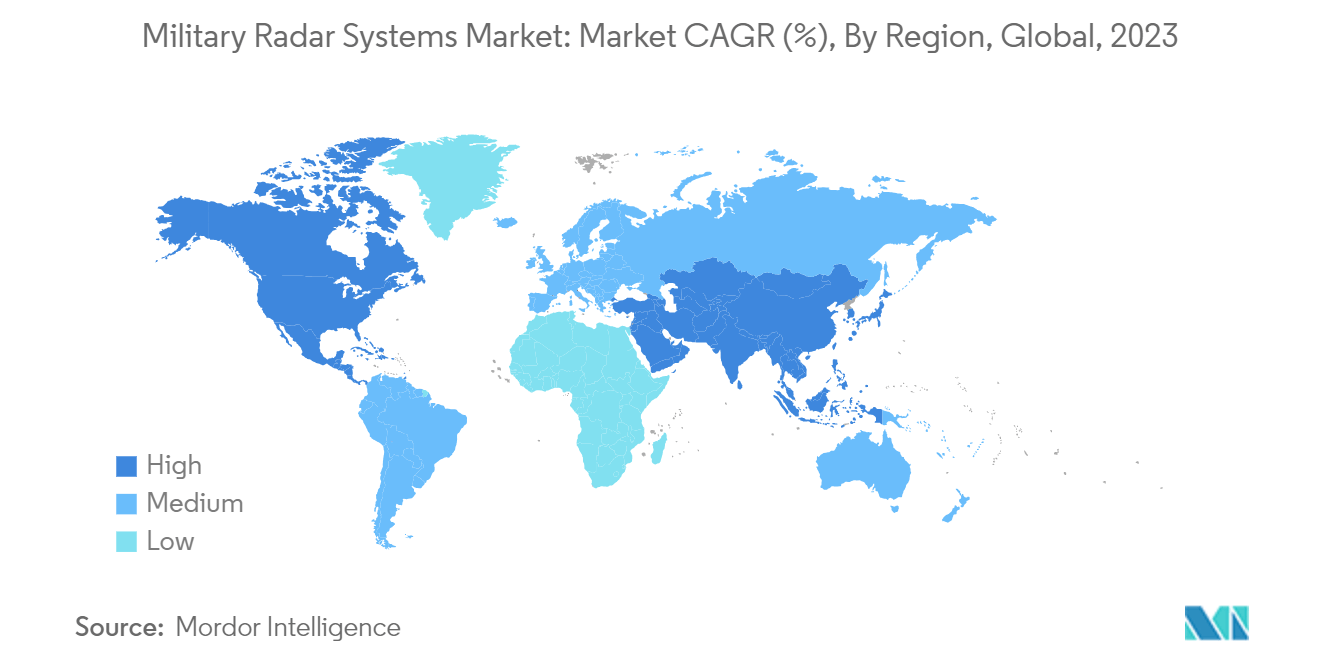

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Military Radars Market Analysis

The Military Radars Market size is estimated at USD 16.71 billion in 2024, and is expected to reach USD 21.47 billion by 2029, growing at a CAGR of 5.15% during the forecast period (2024-2029).

Radars are widely used in military applications for surveillance, navigation, weapon guidance, airspace monitoring, and other purposes. The demand for coherent radar in the military is expected to grow in the coming years due to the rise in terrorism and geopolitical tensions in certain geographies, such as the Middle East and Asia-Pacific.

A constant pursuit of technological superiority for defense and surveillance purposes characterizes radars for the military. The need for advanced threat detection, tracking, and target identification capabilities drives demand in this segment. With their rapid beam steering and high accuracy, phased array radars are increasingly prevalent in military applications. Trends in the military radar market include the integration of artificial intelligence (AI) for real-time threat analysis and decision-making. Stealth technology influences radar development, emphasizing reducing radar cross-sections to evade enemy detection.

However, the military radar systems market also faces some challenges, such as the high cost and complexity of radar systems, regulatory and environmental issues, vulnerability to jamming and spoofing, and competition from alternative technologies, such as lidar and sonar. Therefore, the market players must invest in research and development, innovation, and collaboration to overcome these challenges and gain a competitive edge.

Military Radars Market Trends

Airborne Segment Expected to Register the Highest CAGR During the Forecast Period

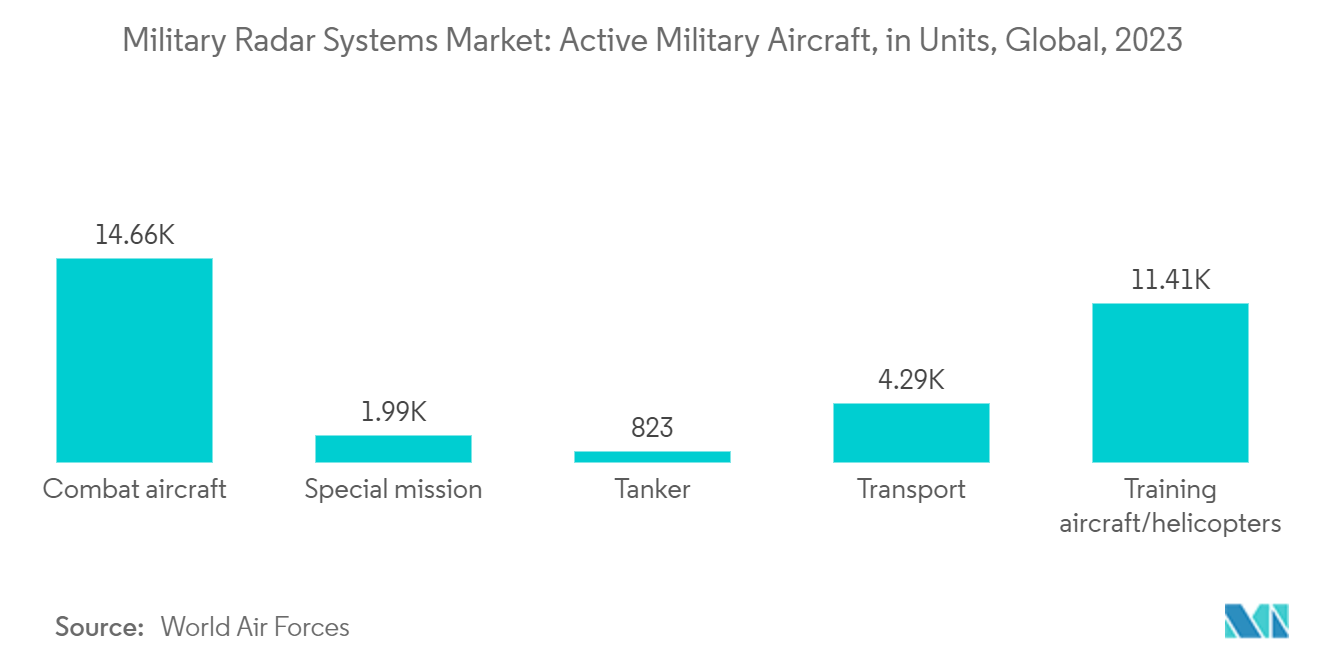

Modern military planes are made to do different kinds of missions. Hence, the radar systems on board must be able to do specific tasks that match the mission profiles. For example, radar is used in fighter planes to find enemy planes and control missiles, rockets, and other weapons on board. Similarly, in a bomber aircraft, radar is used to find surface targets, fix or move them, and navigate and avoid obstacles. An increase in the global aerial fleet has led to a rise in the demand for airborne radar.

Countries like the US, India, China, Iran, Israel, and Russia, among others, have invested in modernizing and upgrading their existing air fleets. China is using stealth technology in unmanned platforms and is unveiling more UAV variants. Furthermore, rising global expenditures and spending on enhancing defense capabilities drive market growth. For instance, in 2023, the global military expenditure reached USD 2,440 billion, a growth of 9% from the year 2022.

Additionally, various European countries, including the United States, France, Germany, Russia, the United Kingdom, and Japan, are collaborating on advancing stealth fighter jet technology. For example, in November 2022, France, Germany, and Spain agreed to commence the next phase of development for a new fighter jet under the Future Combat Air System program, with an estimated project cost surpassing USD 103.4 billion. As part of the program, these nations are expected to replace older fleets of fighter aircraft, such as the F-18 and Typhoon. Similarly, in December 2023, the United Kingdom partnered with Japan and Italy to develop a next-generation stealth fighter under the future combat air program. This fighter is anticipated to possess supersonic capabilities and be outfitted with cutting-edge technology, including airborne radars.

Furthermore, countries like India, Israel, and Turkey are investing in the development and acquisition of unmanned air vehicles to enhance their ISR capabilities. For instance, in November 2023, India awarded a contract to Israel Aerospace Industries Ltd to purchase an additional six Hermes 900 unarmed drones to bolster the country’s surveillance capabilities. Overall, the widespread adoption of stealth technology by the defense forces of multiple countries is expected to drive demand for military radar systems onboard aircraft, enabling silent target monitoring and the ability to penetrate enemy air defenses for neutralization, when necessary, during the forecast period.

North America to Occupy the Largest Market Share During the Forecast Period

In North America, the United States is a keen developer and user of various advanced military radar technologies. The market in the region is expected to be dominated by military radar systems, driven by the substantial military spending of the United States. For example, the US military defense expenditure increased to USD 916 billion in 2023, a 2.3% growth from 2022. The heightened investments in technologically advanced weaponry are a response to the increasing threat perception from China and Russia, propelling the demand for radar systems in the country.

Moreover, the increased defense spending in the United States is leading to active procurement of various military radar systems to bolster its defense capabilities, thus further fueling the demand for this market in the region. For instance, in October 2023, the US Air Force announced its intention to construct homeland-defense radars capable of detecting a new generation of Russian cruise missiles. As part of the Over-The-Horizon Radar program, the US plans to acquire four long-range radars from RTX Corporation, which can detect, track, and report airborne and surface targets. Canada also has plans to procure two of these radar systems under the same program.

In addition, North America is home to leading defense technology firms that consistently invest in developing advanced situational awareness enhancement systems. For example, in November 2023, the US Army revealed that RTX’s new missile defense radar, the Lower Tier Air and Missile Defense Sensor system, successfully intercepted a cruise missile in a development test. The LTAMDS is set to replace the original Patriot’s air and missile defense radar and will have the capability to neutralize ballistic missiles and other complex threats from all directions. Overall, these developments are anticipated to drive the demand for this market in North America during the forecast period.

Military Radars Industry Overview

The military radars systems market is consolidated and marked by many prominent players competing for a larger market share. Lockheed Martin Corporation, Northrop Grumman Corporation, Israel Aerospace Industries Ltd, Leonardo SpA, and RTX Corporation are some of the major players in the market.

The stringent safety and regulatory policies in the defense segment are expected to restrict the entry of new players. With the growing implementation of stealth technologies in adversary aerial platforms and weapons, market players are focusing on developing sophisticated radar systems that can effectively detect targets with lower radar cross-sections.

Also, players are investing in developing newer generation radars, like the active electronically scanned array (AESA) radar, passive radar, 3D radar, dual-band radar, etc., which offer several advantages compared to their conventional counterparts. With the growing focus on indigenization, several countries are investing in developing radar systems locally, which is expected to make the market more competitive during the forecast period.

Military Radars Market Leaders

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Leonardo S.p.A.

-

RTX Corporation

-

Israel Aerospace Industries Ltd.

*Disclaimer: Major Players sorted in no particular order

Military Radars Market News

March 2024: South Korea’s DAPA announced that it plans to invest USD 2.9 billion to enhance the radar systems and long-range mission capabilities of its F-15K Eagle fleet. Under the program, the aircraft is expected to be equipped with the AN/APG-82 electronic scanning radar, BAE Systems' AN/ALQ-250 Eagle Passive Active Warning Survivability System, and a new large-area display in the cockpit to enhance situational awareness.

December 2023: The Royal Malaysia Air Force (RMAF) awarded THALES a contract to deliver the new GM400α long-range radar. The GM400α allows Malaysia’s armed forces to detect all types of threats early for decision-making and action.

Military Radar Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Buyers/Consumers

4.4.2 Bargaining Power of Suppliers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Platform

5.1.1 Ground-based

5.1.2 Naval

5.1.3 Airborne

5.1.4 Space

5.2 Application

5.2.1 Air and Missile Defense

5.2.2 Intelligence, Surveillance, and Reconnaissance (ISR)

5.2.3 Navigation and Weapon Guidance

5.2.4 Space Situational Awareness

5.2.5 Other Applications

5.3 Component

5.3.1 Antennas

5.3.2 Transmitters

5.3.3 Receivers

5.3.4 Power Amplifiers

5.3.5 Duplexers

5.3.6 Digital Signal Processors

5.3.7 Stabilization Systems

5.3.8 Graphical User Interfaces

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.2 Europe

5.4.2.1 United Kingdom

5.4.2.2 Germany

5.4.2.3 France

5.4.2.4 Russia

5.4.2.5 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 India

5.4.3.3 Japan

5.4.3.4 South Korea

5.4.3.5 Rest of Asia-Pacific

5.4.4 Latin America

5.4.4.1 Brazil

5.4.4.2 Rest of Latin America

5.4.5 Middle East and Africa

5.4.5.1 United Arab Emirates

5.4.5.2 Saudi Arabia

5.4.5.3 Egypt

5.4.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 THALES

6.2.2 RTX Corporation

6.2.3 BAE Systems PLC

6.2.4 Lockheed Martin Corporation

6.2.5 Israel Aerospace Industries Ltd

6.2.6 Northrop Grumman Corporation

6.2.7 Saab AB

6.2.8 Leonardo SpA

6.2.9 Airbus SE

6.2.10 Teledyne Technologies Incorporated

6.2.11 HENSOLDT Holding Germany GmbH

6.2.12 QinetiQ Group PLC

7. MARKET OPPORTUNITIES

Military Radars Industry Segmentation

Armed forces use military radars for surveillance, locating targets, tracking their movements, and directing other weapons or countermeasures against them. Military radars are also used for navigation and tracking weather changes. The study includes radars used by the navy (coastal radars and ship-based radars), air force (weather navigation radar, airborne radar, and precision approach radar), and army (perimeter surveillance radars, long-range surveillance radars, and fixed and movable land radars), as well as in space applications. The other applications include IED detection, airspace monitoring, traffic management, and weather monitoring.

The military radar systems market is segmented by platform, application, components, and geography. By platform, it is segmented into ground-based, naval, airborne, and space. By application, the market is classified into air and missile defense, intelligence, surveillance, and reconnaissance (ISR), navigation and weapon guidance, space situational awareness, and other applications. Based on components, the market is segmented into antennas, transmitters, receivers, power amplifiers, duplexers, digital signal processors, stabilization systems, and graphical user interfaces. The report also covers the market sizes and forecasts for the military radar systems market in major countries across different regions. For each segment, the market size and forecast are provided in terms of value (USD).

| Platform | |

| Ground-based | |

| Naval | |

| Airborne | |

| Space |

| Application | |

| Air and Missile Defense | |

| Intelligence, Surveillance, and Reconnaissance (ISR) | |

| Navigation and Weapon Guidance | |

| Space Situational Awareness | |

| Other Applications |

| Component | |

| Antennas | |

| Transmitters | |

| Receivers | |

| Power Amplifiers | |

| Duplexers | |

| Digital Signal Processors | |

| Stabilization Systems | |

| Graphical User Interfaces |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Military Radar Market Research FAQs

How big is the Military Radars Market?

The Military Radars Market size is expected to reach USD 16.71 billion in 2024 and grow at a CAGR of 5.15% to reach USD 21.47 billion by 2029.

What is the current Military Radars Market size?

In 2024, the Military Radars Market size is expected to reach USD 16.71 billion.

Who are the key players in Military Radars Market?

Lockheed Martin Corporation, Northrop Grumman Corporation, Leonardo S.p.A., RTX Corporation and Israel Aerospace Industries Ltd. are the major companies operating in the Military Radars Market.

Which is the fastest growing region in Military Radars Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Military Radars Market?

In 2024, the North America accounts for the largest market share in Military Radars Market.

What years does this Military Radars Market cover, and what was the market size in 2023?

In 2023, the Military Radars Market size was estimated at USD 15.85 billion. The report covers the Military Radars Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Military Radars Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Military Radar Systems Industry Report

The Military Radar Systems Market Report is a comprehensive industry report segmented by platform, application, component, and geography. This market overview provides valuable industry analysis and industry information, offering insights into the market size and market share of various segments. The report includes a detailed market forecast, highlighting the market growth and market trends expected in the coming years.

The industry outlook indicates a significant growth rate driven by advancements in technology and increasing defense budgets. The report also covers market segmentation, providing a clear market review of different platforms such as ground-based, naval, airborne, and space. Additionally, it delves into various applications like air and missile defense, intelligence, surveillance, and reconnaissance (ISR), navigation and weapon guidance, and space situational awareness.

This industry research includes an analysis of key components such as antennas, transmitters, receivers, power amplifiers, duplexers, digital signal processors, stabilization systems, and graphic user interfaces. The report example and report PDF offer a detailed market analysis and market predictions, helping stakeholders understand the market value and industry sales potential.

The global market for military radar systems is analyzed across different regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. The report also identifies market leaders and provides industry statistics and market data to support strategic decision-making.

Overall, this market report is an essential resource for research companies and other stakeholders seeking to understand the current landscape and future prospects of the military radar systems market. The industry reports provide a thorough industry overview and market outlook, ensuring that readers are well-informed about the latest industry trends and market segmentation.

Military Radar Systems Market Report Snapshots