Military Jet Fuel Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Growth Rate | 3.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

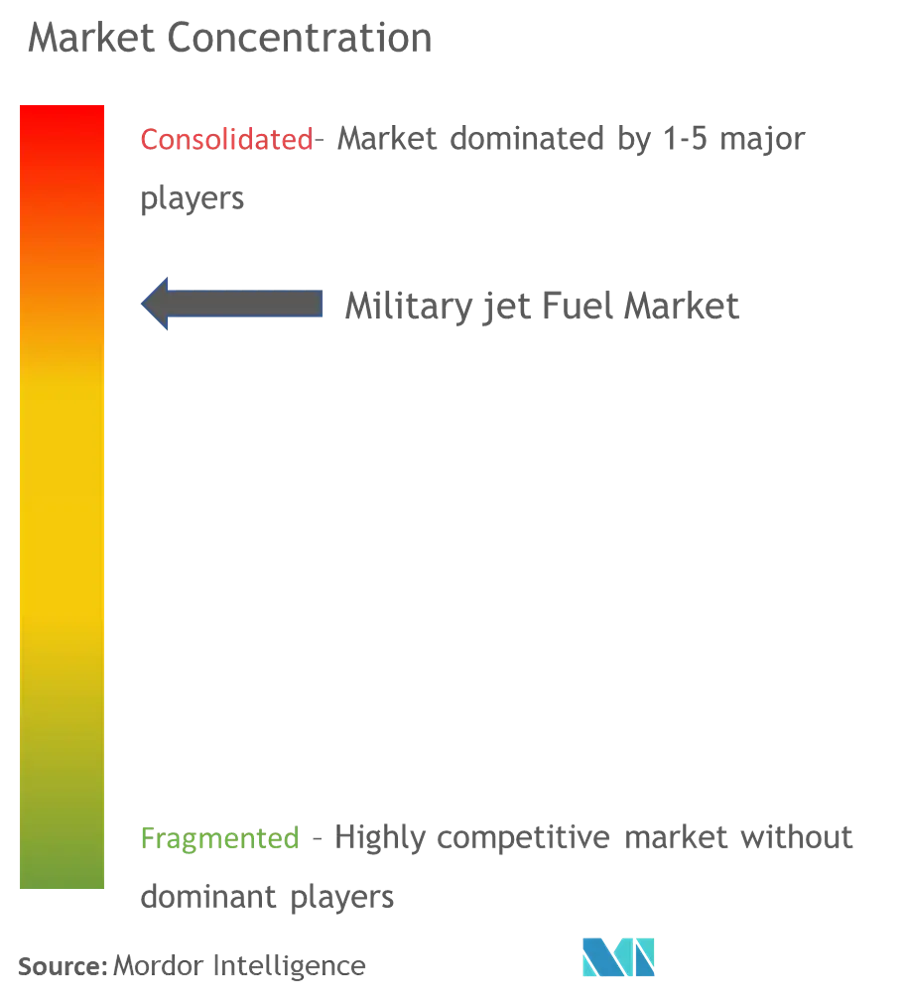

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Jet Fuel Market Analysis by Mordor Intelligence

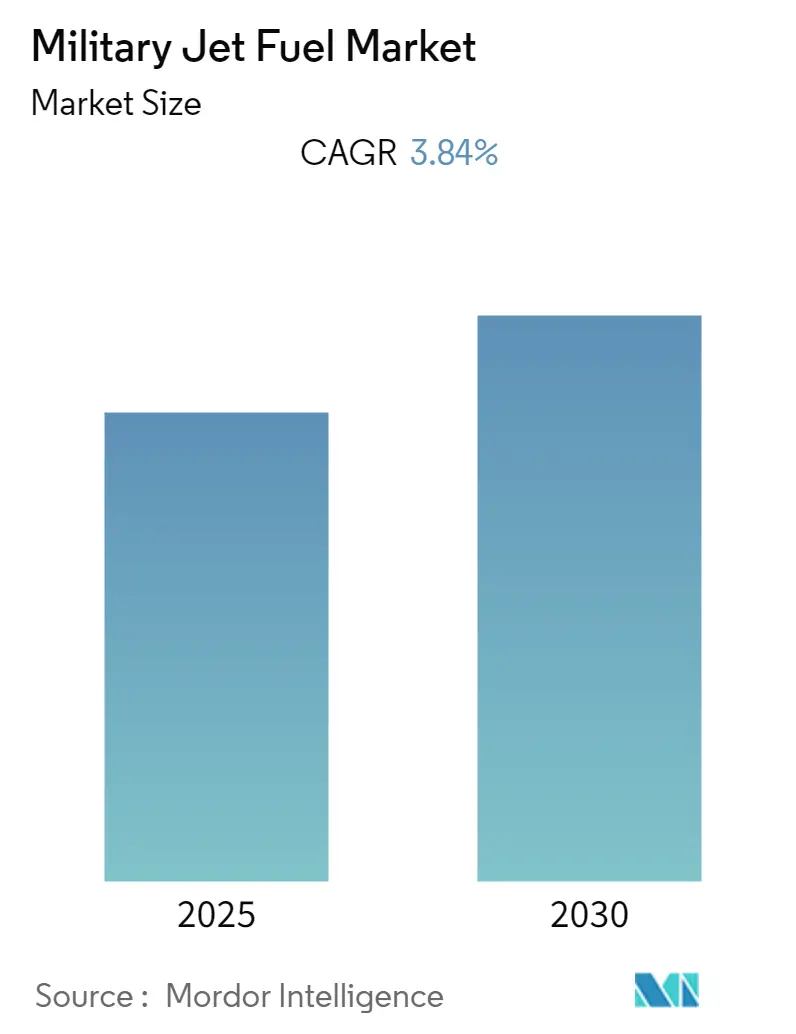

The Military Jet Fuel Market is expected to register a CAGR of 3.84% during the forecast period.

The military jet fuel landscape is experiencing significant transformation amid rising global defense expenditures, with worldwide military spending reaching USD 2,240 billion in 2022, marking the eighth consecutive year of growth. This surge in military activities has directly influenced military jet fuel consumption patterns, with military aircraft accounting for over 20% of total jet fuel consumption in major markets like the United States. The increasing frequency of military exercises, surveillance operations, and strategic deployments has necessitated reliable and efficient fuel supply chains, leading to new strategic partnerships between defense departments and fuel suppliers.

The industry is witnessing a dramatic shift toward sustainable aviation fuels (SAF) as environmental concerns take center stage. These alternative fuels have demonstrated the potential to reduce CO2 emissions by up to 85% compared to conventional fuels, driving significant investment in research and development. In February 2023, BP collaborated with the Royal Air Force for its groundbreaking first use of sustainable aviation fuel in Typhoon and Hercules military aircraft, marking a significant milestone in military aviation fuel's environmental initiatives. This transition is further supported by major policy developments, such as the December 2022 US Congress defense spending bill mandating the Department of Defense to establish SAF refineries and achieve a 10% SAF fuel blend by 2028.

Innovation in fuel production technologies is reshaping the industry's future trajectory. In March 2023, the United States Military announced Project SynCE (Synthetic Fuel for the Contested Environment), aimed at developing capabilities to produce military jet fuel synthetically and on-site. This initiative represents a significant advancement in addressing logistical challenges and reducing dependency on traditional supply chains. Similarly, sustainable aviation fuel startup Air Company secured a USD 65 million agreement with the Department of Defense in February 2023 to develop technology for producing fuel directly from atmospheric carbon dioxide on military bases worldwide.

Strategic partnerships and long-term supply agreements are becoming increasingly prevalent in the military aviation fuel sector. A notable example is the July 2023 contract between Viva Energy Refining Pty Ltd and the Australian Defense Force, spanning an initial six-year term with potential extension to 12 years, which includes the resumption of F-44 (Avcat) production at Geelong Refinery. These partnerships are crucial for ensuring fuel security and maintaining operational readiness while simultaneously advancing sustainable fuel initiatives. The industry is also witnessing increased collaboration between military organizations and private sector companies in developing and implementing new fuel technologies, particularly in the realm of sustainable aviation fuels, where over 370,000 flights have utilized renewable aviation fuel since 2016.

Global Military Jet Fuel Market Trends and Insights

Increasing Defense Budgets

The connection between the global military jet fuel market and nations' defense budgets is highly significant, with governments worldwide allocating substantial resources to support their armed forces. According to the Stockholm International Peace Research Institute (SIPRI), global military spending reached USD 2,240 billion in 2022, marking the eighth consecutive year of growth. The most significant surge in spending, amounting to a substantial increase of 13%, was observed in Europe, primarily attributed to increased military expenditures by Russia and Ukraine. This increased military spending directly impacts the demand for fighter jet fuel, as nations invest in advanced fighter jets and combat aircraft that have become integral assets to modern defense strategies, enabling governments to project power and execute crucial tactical missions.

The trend of increasing defense budgets is particularly evident in major military powers. The United States, maintaining its position as the world's largest defense spender, allocated USD 811.59 billion to its defense sector in 2022, while China, the second-largest spender, invested USD 297.99 billion. India has also significantly increased its defense spending, with the Ministry of Defence receiving a total allocation of INR 5,93,537 crore in the 2023-24 budget, representing a substantial increase of 13% compared to the previous year. These growing defense budgets have enabled countries to maintain and expand their military aircraft fleets, with the United States operating approximately 13,300 aircraft, while Russia, China, and India maintain fleets of 4,182, 3,166, and 2,210 aircraft respectively. This expansion in military aircraft fleets directly correlates with increased demand for fighter jet fuel consumption and military aircraft fuel.

Recent developments in 2023 further demonstrate the impact of defense budgets on military aviation capabilities. In July 2023, India's Defense Ministry granted preliminary approval to acquire 26 Rafale fighter jets for the Indian Navy, showcasing the ongoing investment in military aviation capabilities. Similarly, in February 2023, BP collaborated with the Royal Air Force (RAF) for its first use of sustainable aviation fuel (SAF) in Typhoon and Hercules military aircraft, while in March 2023, the United States Military announced Project SynCE, exploring new ways of producing military jet fuel synthetically and on-site. Additionally, sustainable aviation fuel startup Air Company secured a USD 65 million agreement with the Department of Defense in February 2023, highlighting the growing investment in alternative fuel technologies within the military aviation sector. The increasing focus on sustainable alternatives also influences the cost of fighter jet fuel, as these innovations aim to balance operational efficiency with environmental considerations.

Segment Analysis

Air Turbine Fuel Segment in Military Jet Fuel Market

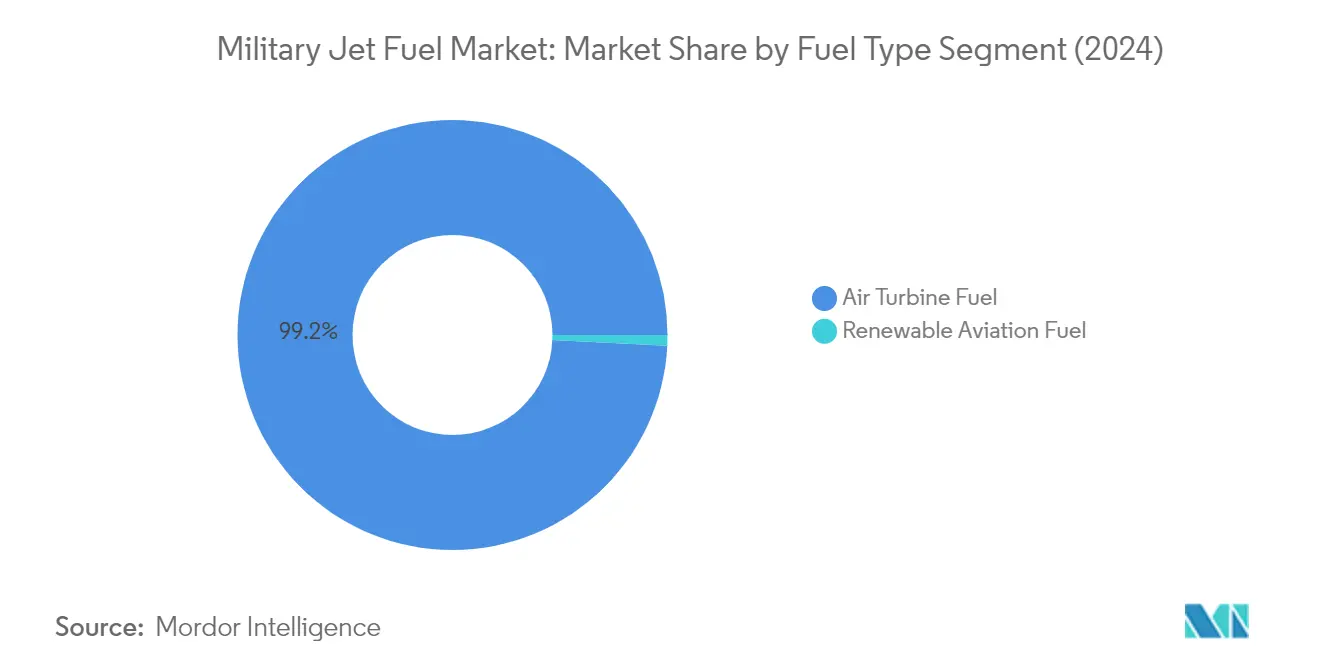

The Air Turbine Fuel segment dominates the global military jet fuel market, holding approximately 99% market share in 2024. This segment encompasses various military-grade fuels, including JP-8, which is the primary fuel used by NATO air forces, and JP-5, specifically designed for naval aviation applications. The segment's dominance is attributed to the extensive existing infrastructure supporting conventional jet fuel distribution, established supply chains, and the large fleet of military aircraft globally that are designed to operate on these fuels. Military organizations worldwide continue to rely heavily on air turbine fuel due to its proven performance characteristics, including high energy density, thermal stability, and reliable operation across diverse environmental conditions. The segment's robust market position is further strengthened by ongoing military modernization programs and increasing defense budgets across major economies, particularly in regions like North America, Europe, and Asia-Pacific. Additionally, understanding military jet fuel specifications is crucial for ensuring compatibility and performance in various military operations.

Renewable Aviation Fuel Segment in Military Jet Fuel Market

The Renewable Aviation Fuel segment is experiencing remarkable growth in the military jet fuel market, with a projected growth rate of approximately 43% during the forecast period 2024-2029. This exceptional growth is driven by increasing environmental regulations and military organizations' commitment to reducing their carbon footprint. The segment is witnessing substantial investments in research and development, particularly in sustainable aviation fuel (SAF) technologies. Notable developments include the United States Department of Defense's initiatives to establish SAF production facilities at military bases and the Royal Air Force's successful implementation of 100% sustainable aviation fuel flights. The segment's growth is further supported by various government policies and military directives aimed at incorporating renewable fuel blends into existing aircraft operations. Strategic partnerships between military organizations and renewable fuel producers are accelerating the development and deployment of sustainable aviation fuel solutions, marking a significant shift towards more environmentally conscious military aviation operations. The exploration of avcat fuel alternatives also highlights the military's dedication to innovative and sustainable fuel solutions.

Geography Analysis

Military Jet Fuel Market in North America

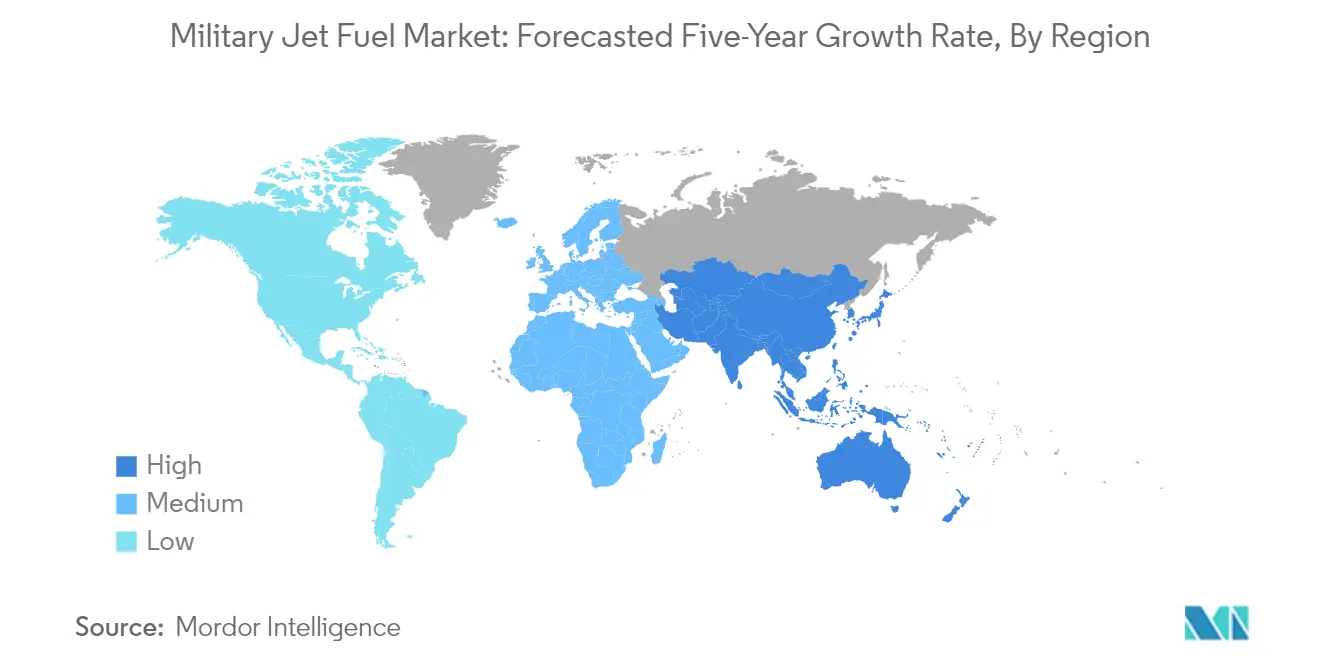

The North American military jet fuel market maintains its position as a dominant force in the global landscape, commanding approximately 28% of the global market share in 2024. The region's market is primarily driven by the United States, which possesses the world's most advanced air force technology and fleet. The extensive military infrastructure, combined with ongoing modernization efforts and strategic defense priorities, continues to fuel steady demand for military aircraft fuel. The market is characterized by significant investments in sustainable aviation fuel (SAF) development, with major initiatives underway to integrate renewable fuel options into military aircraft operations. The region's commitment to maintaining air superiority, coupled with an increasing focus on environmental sustainability, has led to a balanced approach in fuel procurement and usage. The presence of major defense contractors and fuel suppliers, along with robust supply chain networks, ensures reliable fuel availability for military operations. Furthermore, the strategic importance of North American military capabilities in global geopolitics continues to necessitate a consistent fuel supply for training, operations, and readiness maintenance.

Military Jet Fuel Market in Europe

The European military jet fuel market has demonstrated resilience and steady growth, registering an approximate 1% growth rate from 2019 to 2024. The market dynamics are significantly influenced by NATO requirements and regional security considerations, particularly in light of evolving geopolitical situations. The European market is characterized by a strong emphasis on fuel quality standards and increasing adoption of sustainable aviation fuel alternatives. Major countries, including Germany, France, and the United Kingdom, continue to drive market growth through their respective military modernization programs and operational requirements. The region's focus on reducing carbon emissions has led to increased investments in sustainable fuel technologies and infrastructure development. The market also benefits from strong collaboration between military organizations and fuel suppliers, ensuring efficient distribution networks across the continent. The presence of advanced military aircraft fleets and ongoing fleet modernization efforts continues to sustain demand for military aviation fuel, while investments in research and development support the evolution of fuel technologies.

Military Jet Fuel Market in Asia-Pacific

The Asia-Pacific military jet fuel market demonstrates robust growth potential, with projections indicating an approximate 4% growth rate from 2024 to 2029. The region's market is characterized by increasing military modernization efforts and expanding defense budgets across major economies. Countries such as China, India, Japan, and South Korea are driving significant market growth through their military aviation expansion programs and enhanced operational requirements. The market landscape is shaped by growing regional security concerns and the need for stronger air defense capabilities. Investments in military aviation infrastructure and the expansion of air force fleets continue to drive demand for military jet fuel across the region. The market also witnesses an increasing focus on fuel security and supply chain optimization, given the strategic importance of military aviation in regional defense strategies. The emergence of new military partnerships and defense agreements further strengthens the market's growth trajectory, while investments in fuel storage and distribution infrastructure support market expansion.

Military Jet Fuel Market in Rest of the World

The Rest of the World military jet fuel market encompasses diverse regions, including the Middle East, Africa, and South America, each with unique market characteristics and growth drivers. The market is primarily driven by increasing defense modernization efforts and expanding military aviation capabilities in key countries. The Middle East region, in particular, demonstrates strong market potential due to ongoing military modernization programs and strategic defense priorities. South American countries are focusing on enhancing their military aviation capabilities through fleet modernization and improved fuel management systems. The market benefits from increasing defense cooperation agreements and technology transfers, which support the development of military aviation infrastructure. Regional security considerations and the need for enhanced military readiness continue to drive market growth, while investments in fuel storage and distribution networks support market development. The increasing focus on military aviation capabilities and operational readiness ensures sustained demand for military jet fuel across these regions. Additionally, jet fuel consumption by country varies significantly, reflecting diverse military needs and strategic priorities.

Competitive Landscape

Top Companies in Military Jet Fuel Market

The military jet fuel market is characterized by the strong presence of major oil and gas conglomerates, including Shell PLC, BP PLC, ExxonMobil Corporation, Chevron Corporation, TotalEnergies SE, and other significant players like Honeywell UOP and Repsol SA. These companies are actively investing in sustainable aviation fuel (SAF) development and production capabilities, demonstrating their commitment to environmental sustainability and future market demands. Strategic collaborations with military organizations and research institutions have become increasingly common as companies seek to enhance their technological capabilities and market position. The industry has witnessed a notable shift towards expanding production facilities and distribution networks to ensure reliable supply chains for military customers. Companies are also focusing on developing specialized fuel formulations that meet stringent military specifications while incorporating innovative additives and performance-enhancing components.

Consolidated Market with High Entry Barriers

The military aviation fuel market exhibits a moderately consolidated structure dominated by large multinational energy corporations with extensive refining and distribution capabilities. These established players leverage their integrated operations, spanning from crude oil extraction to final fuel production and distribution, creating significant barriers for new entrants. The market's competitive dynamics are shaped by long-term supply agreements with defense organizations, requiring suppliers to maintain stringent quality standards and demonstrate reliable delivery capabilities. The industry has witnessed selective strategic partnerships and joint ventures, particularly in developing sustainable aviation fuel technologies and expanding geographical presence.

The competitive landscape is further characterized by high capital requirements, complex regulatory compliance needs, and the necessity for sophisticated technical expertise. Regional players maintain their presence through specialized knowledge of local defense requirements and established relationships with military establishments in their respective territories. Market consolidation activities are primarily driven by the need to acquire technological capabilities, expand geographical footprint, and strengthen supply chain networks, rather than purely market share considerations. The industry's high fixed costs and specialized infrastructure requirements contribute to maintaining the existing competitive structure.

Innovation and Sustainability Drive Future Success

Success in the military aircraft fuel market increasingly depends on companies' ability to balance traditional fuel production with sustainable alternatives while maintaining strict performance standards. Market leaders are investing heavily in research and development to develop advanced fuel formulations that offer enhanced performance characteristics while reducing environmental impact. The ability to scale up sustainable aviation fuel production while maintaining cost competitiveness has become a critical differentiator. Companies are also focusing on developing robust supply chain networks and establishing strategic partnerships with military organizations to ensure long-term market presence.

For new entrants and smaller players, success lies in identifying specialized market niches and developing innovative fuel solutions that address specific military requirements. The increasing focus on environmental regulations and sustainability goals presents opportunities for companies with advanced clean fuel technologies. Building strong relationships with military procurement agencies and demonstrating reliable supply capabilities remain crucial for market success. The industry's future competitive dynamics will be significantly influenced by technological advancements in aircraft design, evolving military requirements, and increasingly stringent environmental regulations, requiring companies to maintain high levels of operational flexibility and innovation capabilities.

Military Jet Fuel Industry Leaders

BP PLC

Honeywell International Inc

Repsol SA

GS Caltex Corporation

Shell PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2023: Viva Energy Refining Pty Ltd (Viva Energy) secured a contract with the Department of Defense to supply aviation, marine, and ground fuel to the Australian Defense Force (ADF). The Fuel Supply Contract is for an initial six-year term which may be extended to 12 years. As part of the deal and an essential Australian Industry Capability activity, Viva Energy is expected to resume production at Geelong Refinery of F-44 (Avcat) or JP-5, a military specification aviation turbine fuel used on aircraft carriers.

- March 2023: The Jet fuel supply for Myanmar's armed forces was affected by the latest sanctions imposed by the United States on the country's military regime and crony businesses. The United States Treasury Department imposed sanctions on two people and six entities connected to Myanmar's military, who had enabled the regime's continuing atrocities. Three sanctioned entities work in Myanmar's defense sector, specifically importing, storing, and distributing aviation fuel for the country's armed forces.

Global Military Jet Fuel Market Report Scope

Jet fuel, or aviation fuel, is a type of highly volatile fuel used in aircraft gas turbine engines. The airline and defense industries are the world's largest consumers of jet fuel.

The military jet fuel market is segmented by fuel type and geography. By fuel type, the market is segmented into air turbine fuel and renewable aviation fuel. The report also covers the size and forecasts of the military jet fuel market across the regions. For each segment, market sizing and forecasts have been done based on revenue (USD).

| Air Turbine Fuel |

| Renewable Avaition Fuel |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of North America | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Algeria |

| Fuel Type | Air Turbine Fuel | |

| Renewable Avaition Fuel | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of North America | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Algeria | ||

Key Questions Answered in the Report

What is the current Military Jet Fuel Market size?

The Military Jet Fuel Market is projected to register a CAGR of 3.84% during the forecast period (2025-2030)

Who are the key players in Military Jet Fuel Market?

BP PLC, Honeywell International Inc, Repsol SA, GS Caltex Corporation and Shell PLC are the major companies operating in the Military Jet Fuel Market.

Which is the fastest growing region in Military Jet Fuel Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Military Jet Fuel Market?

In 2025, the Asia Pacific accounts for the largest market share in Military Jet Fuel Market.

What years does this Military Jet Fuel Market cover?

The report covers the Military Jet Fuel Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Military Jet Fuel Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: