| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 9.16 Billion |

| Market Size (2030) | USD 10.52 Billion |

| CAGR (2025 - 2030) | 2.80 % |

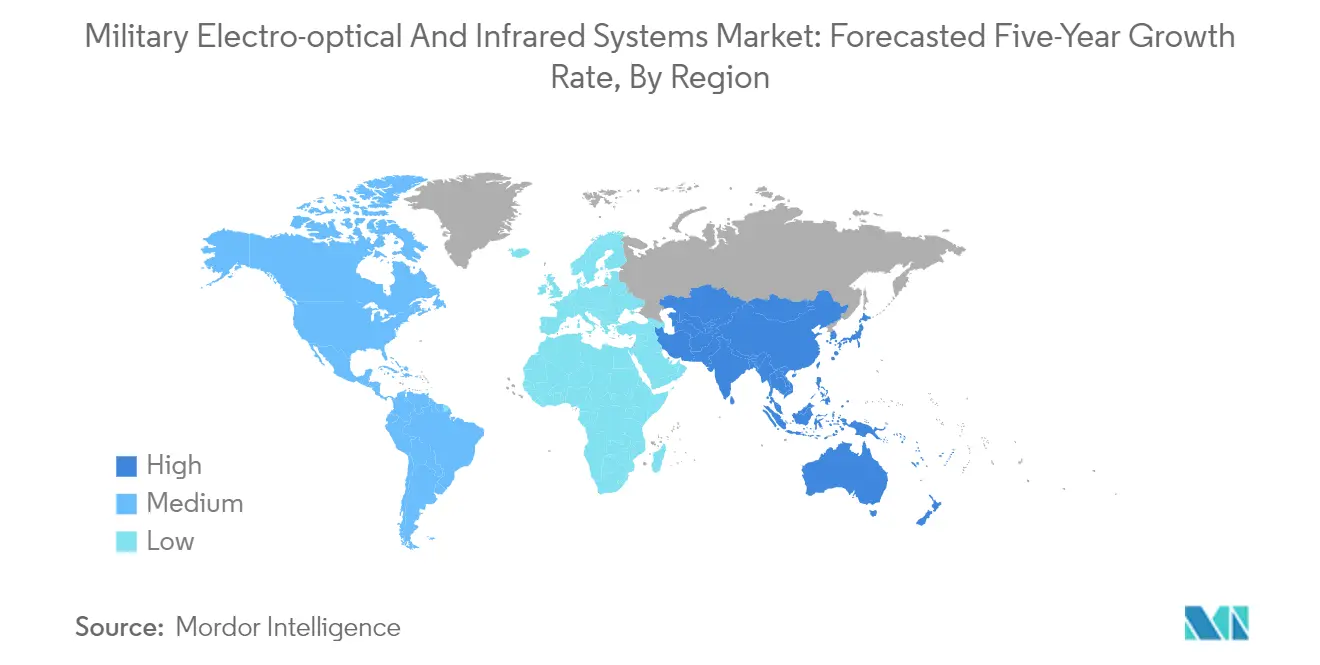

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

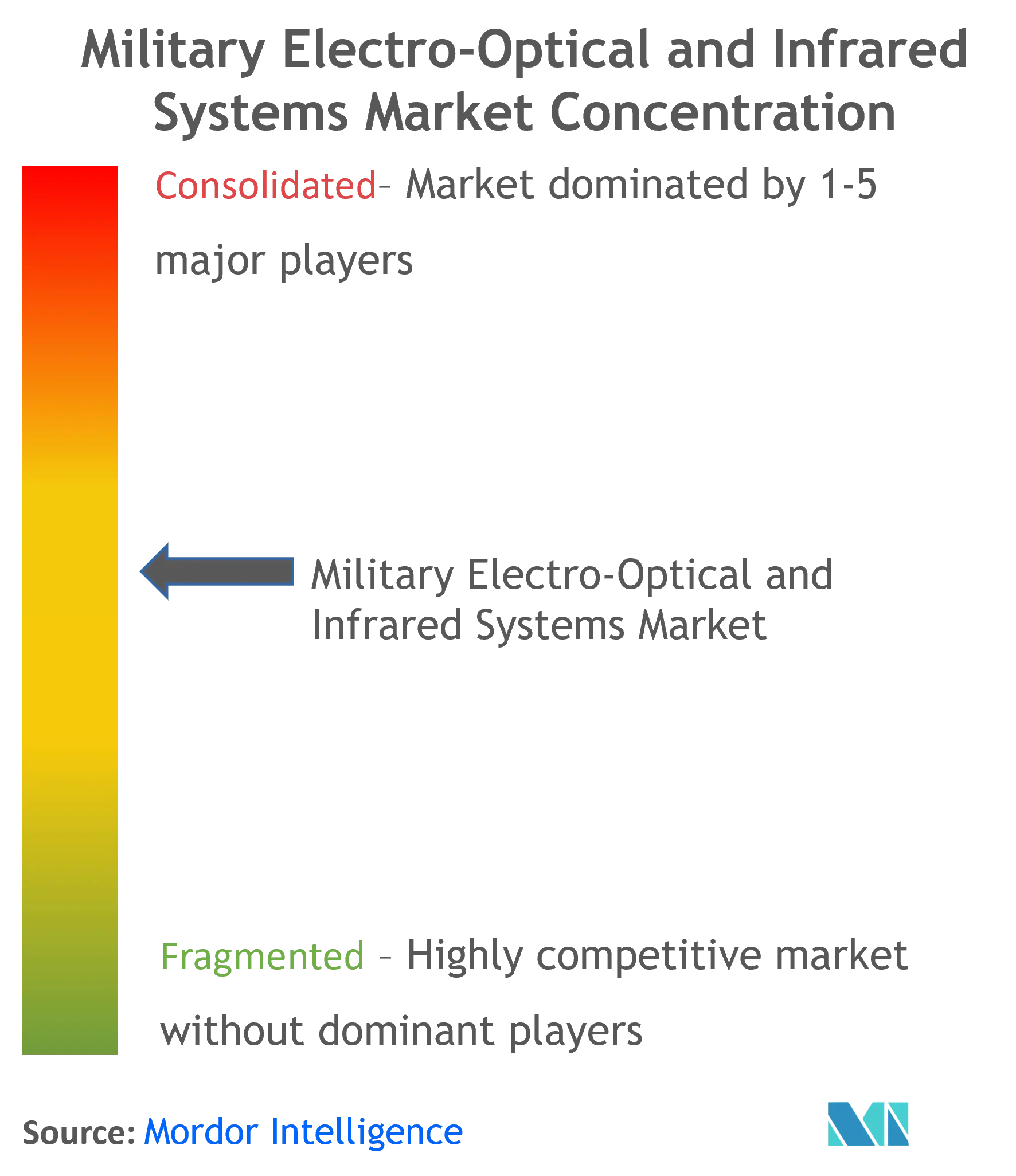

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Military Electro-optical and Infrared Systems Market Analysis

The Military Electro-optical And Infrared Systems Market size is estimated at USD 9.16 billion in 2025, and is expected to reach USD 10.52 billion by 2030, at a CAGR of 2.8% during the forecast period (2025-2030).

The military electro-optical and infrared systems market is experiencing significant transformation driven by technological advancements and changing defense priorities. Major defense powers are increasingly focusing on developing indigenous manufacturing capabilities to reduce dependency on foreign suppliers, with several countries establishing local production facilities and research centers. This shift is exemplified by recent developments like the March 2022 announcement by Saudi Arabia's General Authority for Military Industries regarding the localization of their new multi-use monitoring system, Zarqa Al-Yamama-Zali, representing a significant step in developing domestic electro-optic sensor capabilities.

The industry is witnessing a strong trend toward system integration and multi-sensor fusion technologies. Companies are actively working on merging multiple sensors into single devices, focusing on raw data fusion and on-platform processing capabilities to deliver real-time information sharing across military platforms. This evolution is evidenced by recent contracts such as L3Harris Technologies' June 2022 agreement worth USD 205 million to deliver a Shipboard Panoramic Electro-Optic/Infrared system for enhanced fleet protection, demonstrating the growing demand for integrated surveillance solutions in military surveillance systems.

Strategic partnerships and industry consolidation are reshaping the competitive landscape, as companies seek to combine complementary capabilities and expand their market reach. For instance, in November 2021, Abu Dhabi-based EDGE Group and L3Harris Technologies announced a partnership to establish a WESCAM MX-Series electro-optical and infrared systems service center in the UAE, highlighting the industry's move toward localized service capabilities and technology transfer arrangements. These collaborations are particularly focused on developing next-generation sensors with enhanced capabilities in areas such as wide field-of-view distributed-aperture sensors and persistent 360-degree surveillance.

The market is seeing increased emphasis on size reduction and power optimization in EO/IR systems, driven by the growing demand for man-portable equipment and unmanned platforms. Manufacturers are investing in research and development to create smaller, lighter sensors without compromising performance capabilities. This trend is reflected in recent technological developments, such as the introduction of new carbon-based materials, nano-materials, and metamaterials that are fundamentally changing how EO/IR systems are designed and built. The US Defense Department's January 2022 contract worth USD 49.6 million for advanced targeting sight systems demonstrates the ongoing investment in compact, high-performance optical systems, including military infrared cameras and military thermal imaging technologies.

Military Electro-optical and Infrared Systems Market Trends

Rising Defense Expenditures

The profound changes in the international strategic landscape have led to significant increases in defense spending globally, driven by growing hegemonism, unilateralism, and power politics that have fueled several ongoing global conflicts. Military powerhouses have been focusing on augmenting their military firepower and defensive capabilities through increased defense budgets. For instance, the US House of Representatives recently approved a USD 840 billion defense budget for the next fiscal year beginning October 2023, with a USD 37 billion increase in the Pentagon budget focusing on providing funds to Ukraine's military and competing with China. This increased spending has enabled several major procurement programs for advanced electro-optical and infrared systems across different military platforms.

The emphasis on capability upgrades encompasses several technical aspects, leading to the phase-out of legacy military assets and their replacement with advanced systems featuring sophisticated EO/IR capabilities. This is evidenced by several recent high-value contracts, such as the US Special Operations Command's USD 96 million contract with L3Harris Technologies for WESCAM MX electro-optical, infrared, and laser designator sensor suites. These modernization initiatives are being implemented across various military branches to ensure combat readiness and enhance operational capabilities. The growing defense budgets have particularly benefited the development and procurement of advanced sensor systems that provide enhanced situational awareness and target acquisition capabilities.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Necessity to Enhance the Military ISR Capabilities and Battlefield Situational Awareness

Growing asymmetric threat environments globally are necessitating the need for more advanced Intelligence, Surveillance, and Reconnaissance (ISR) capabilities for militaries. There is an increasing focus on integrating different systems to work together to create enterprise-like systems that provide a broader view of the entire ISR spectrum. Military forces worldwide are shifting their focus toward real-time intelligence gathering and enhanced situational awareness, leading to the incorporation of advanced technologies in different modalities like EO/IR systems, RADAR systems, and signals intelligence systems into ISR payloads to obtain multi-mission data gathering capabilities.

In the current battlefield scenario, militaries are required to operate during days, nights, and under adverse weather and limited visibility conditions, where human vision is insufficient. This has led to increased adoption of advanced EO/IR sensors that can be mounted on aerial, land, and sea-based vehicles or made man-portable to identify and track moving targets and assess threats from a distance in challenging environmental conditions. For instance, the US Navy's recent USD 205 million contract for the Shipboard Panoramic Electro-Optic/Infrared (SPEIR) system represents a generational leap in using 360-degree EO/IR imagery for enhanced situational awareness. The system provides improved passive mission solution capability, marking a significant advancement in battlefield awareness capabilities. This advancement is complemented by the integration of night vision for military and thermal imaging for military technologies, which are crucial for operations in low-light and adverse conditions.

Growing Procurement of Unmanned Systems

The growing adoption of unmanned systems for ISR purposes has increased the demand for better motion imagery capabilities of EO/IR sensors to provide day-night, long-range surveillance capabilities, thus enhancing the militaries' ability to identify targets and perform threat assessment. This is complementary to the situational awareness obtained through their manned counterparts. Unmanned systems are being deployed for a wide variety of missions, primarily focusing on ISR and long-duration missions where data collection is essential. However, their role is expected to expand to cargo transportation and more manned-unmanned teaming operations, where they can act as extensions for manned aircraft.

Several manufacturers are developing and launching EO/IR systems specifically designed for the evolving requirements of unmanned systems. These systems are being integrated into various platforms, from small tactical drones to large unmanned aerial vehicles, providing enhanced reconnaissance and surveillance capabilities for deployed military forces. Additionally, unmanned ground vehicles are utilizing a variety of electro-optical and radar sensors to provide unprecedented reconnaissance and surveillance capabilities, while also being used to increase ground troops and land vehicles' safety by detecting and averting threats like IEDs. This growing integration of EO/IR systems in unmanned platforms is driving significant technological advancements in sensor capabilities and miniaturization. The inclusion of thermal cameras for military technology in these systems further enhances their capability to operate effectively in diverse environments, ensuring comprehensive surveillance systems for military support.

Segment Analysis: By Platform

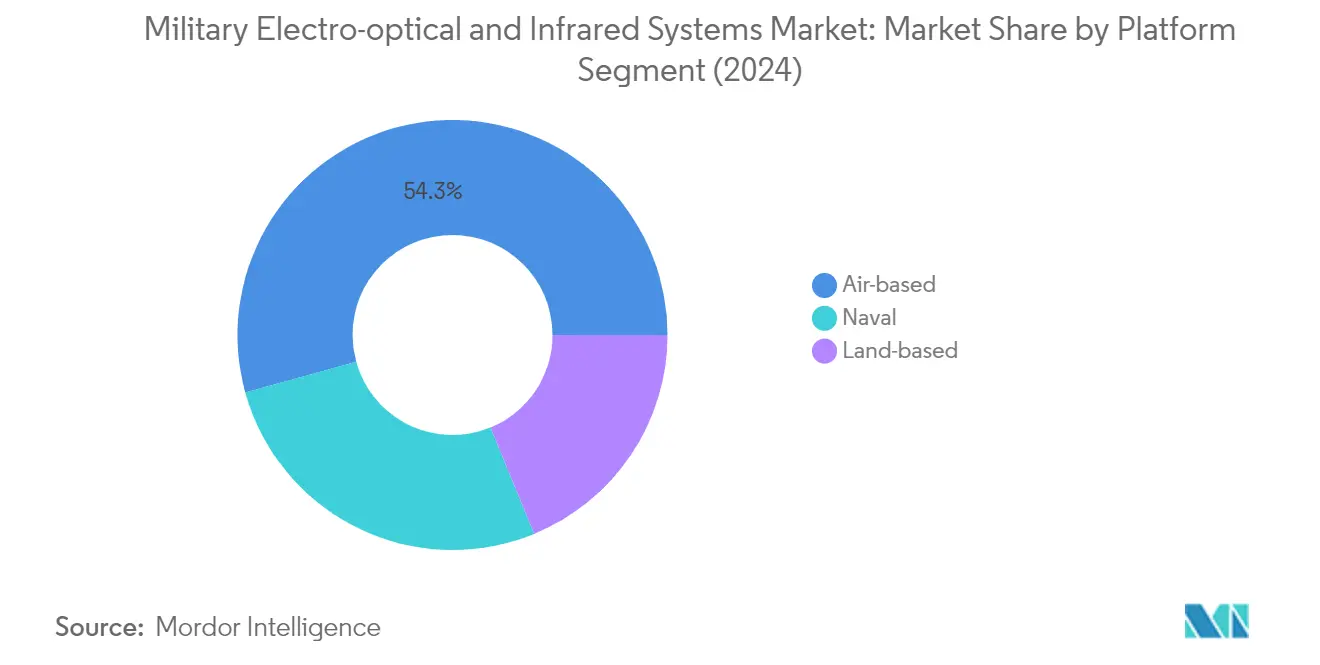

Air-based Segment in Military Electro-optical and Infrared Systems Market

The air-based segment dominates the military electro-optical and infrared systems market, accounting for approximately 54% of the total market share in 2024. This significant market position is driven by the increasing integration of advanced EO/IR systems in various aerial platforms, including fighter aircraft, military helicopters, and unmanned aerial vehicles (UAVs). The growing emphasis on enhancing aerial surveillance, reconnaissance, and combat capabilities has led to substantial investments in airborne EO/IR technologies. Modern military aircraft are increasingly being equipped with sophisticated electro-optical targeting systems, infrared search and track (IRST) capabilities, and multi-spectral imaging systems to provide superior situational awareness and targeting precision. The segment's dominance is further reinforced by the rising procurement of military aircraft and the continuous modernization of existing aerial fleets across major military powers.

Land-based Segment in Military Electro-optical and Infrared Systems Market

The land-based segment is experiencing the fastest growth in the military electro-optical and infrared systems market, driven by increasing investments in ground force modernization programs worldwide. This growth is fueled by the rising demand for advanced night vision for military devices, thermal imaging systems, and electro-optical sights for infantry weapons. The segment is witnessing rapid technological advancements in areas such as man-portable EO/IR systems, vehicle-mounted observation systems, and ground-based surveillance equipment. Military forces are increasingly focusing on enhancing their ground forces' capabilities through the integration of sophisticated EO/IR systems in armored vehicles, combat vehicles, and infantry equipment. The growing emphasis on improving situational awareness and combat effectiveness in urban warfare scenarios has led to increased adoption of thermal sights for military and night vision technologies in land-based platforms.

Naval Segment in Military Electro-optical and Infrared Systems Market

The naval segment plays a crucial role in the military electro-optical and infrared systems market, offering specialized solutions for maritime operations and naval warfare. This segment focuses on providing advanced surveillance and targeting capabilities for various naval platforms, including frigates, destroyers, and patrol vessels. Naval EO/IR systems are particularly important for maritime patrol, coastal surveillance, and anti-submarine warfare operations. These systems are designed to operate effectively in challenging maritime environments, providing critical capabilities such as long-range target identification, maritime surveillance, and threat detection. The segment continues to evolve with the integration of advanced technologies like panoramic infrared search and track systems and multi-sensor electro-optical systems for naval applications. The inclusion of surveillance systems for military enhances the effectiveness of these naval platforms.

Military Electro-optical And Infrared Systems Market Geography Segment Analysis

Military Electro-Optical and Infrared Systems Market in North America

North America represents a dominant force in the military electro-optical and infrared systems market, driven by substantial defense budgets and continuous technological advancements. The region's market is characterized by significant investments in research and development, particularly in advanced sensor technologies and integrated systems. Both the United States and Canada maintain robust defense modernization programs, with a strong focus on enhancing their surveillance and reconnaissance capabilities, including the deployment of military surveillance systems. The presence of major defense contractors and technological innovators further strengthens the region's position in the global market.

Military Electro-Optical and Infrared Systems Market in the United States

The United States maintains its position as the largest market in North America, holding approximately 86% of the regional market share in 2024. The country's dominance is supported by its extensive military modernization initiatives and substantial defense budget allocations. The U.S. military's focus on maintaining technological superiority has led to significant investments in advanced EO/IR systems across all platforms—air, land, and naval. This includes the integration of military thermal cameras and military infrared cameras, which are pivotal in enhancing operational capabilities. The country's robust defense industrial base, including major contractors and specialized technology firms, continues to drive innovation in EO/IR technologies. The emphasis on developing next-generation capabilities, particularly in areas such as multi-spectral imaging and integrated sensor systems, further reinforces the United States' market leadership.

Military Electro-Optical and Infrared Systems Market Growth in the United States

The United States is also experiencing the highest growth rate in North America, with a projected CAGR of approximately 3% from 2024 to 2029. This growth is driven by increasing investments in advanced military technologies and the ongoing modernization of existing platforms. The U.S. military's focus on enhancing its ISR capabilities across all domains has led to sustained demand for sophisticated EO/IR systems, including military imaging systems. The country's commitment to maintaining technological superiority through programs like the F-35 Joint Strike Fighter and various unmanned system initiatives continues to drive market expansion. Additionally, the integration of artificial intelligence and machine learning with EO/IR systems is creating new opportunities for market growth.

Get Analysis on Important Geographic Markets

Download PDF

Military Electro-optical and Infrared Systems Industry Overview

Top Companies in Military Electro-Optical and Infrared Systems Market

The military electro-optical and infrared systems market is characterized by continuous product innovation focused on enhancing sensor capabilities, reducing size-weight-power requirements, and improving integration with various platforms. Companies are investing heavily in research and development to develop advanced technologies like multi-sensor fusion, wide field-of-view distributed aperture sensors, and enhanced image processing capabilities. Strategic partnerships and collaborations with defense organizations and research institutions have become crucial for maintaining a competitive advantage. Market leaders are expanding their geographical presence through local manufacturing facilities and partnerships, particularly in emerging defense markets. Operational agility is demonstrated through rapid prototyping and customization capabilities to meet specific military requirements, while vertical integration of manufacturing processes ensures control over key component technologies and supply chains.

Consolidated Market Led by Defense Specialists

The market structure is dominated by large defense conglomerates with established relationships with military organizations and extensive experience in developing complex defense systems. These major players possess significant technological capabilities, established supply chains, and a deep understanding of military requirements across different regions. The market shows moderate consolidation with a mix of global defense giants and specialized electro-optical system manufacturers, each bringing unique capabilities and market focus.

The industry has witnessed strategic mergers and acquisitions aimed at expanding technological capabilities and market reach. Companies are acquiring specialized firms to gain access to specific technologies or regional markets, while also focusing on vertical integration to secure critical component supply chains. Local players in key defense markets are strengthening their positions through technology transfers and joint ventures with global leaders, creating a more diverse competitive landscape while maintaining high entry barriers for new entrants.

Innovation and Integration Drive Market Success

Success in this market increasingly depends on the ability to develop integrated solutions that combine multiple sensing capabilities while ensuring interoperability with existing military systems. Companies need to maintain strong relationships with military customers, understand evolving battlefield requirements, and demonstrate the ability to deliver reliable, high-performance systems under strict military specifications. Investment in next-generation technologies like artificial intelligence for image processing, advanced materials for improved sensor performance, and enhanced cybersecurity features will be crucial for maintaining a competitive advantage.

Market contenders can gain ground by focusing on specialized niches where they can offer superior technology or cost advantages. Building a strong local presence in key defense markets, developing partnerships with established players, and investing in research and development capabilities are essential strategies. The high concentration of military customers and stringent certification requirements create significant barriers to entry, while the critical nature of these systems in modern military operations reduces substitution risks. Regulatory compliance, particularly regarding export controls and technology transfer restrictions, remains a crucial factor affecting market participation and growth strategies. Additionally, advancements in military imaging systems and military thermal imaging are becoming increasingly important as they enhance the operational capabilities of modern defense forces.

Military Electro-optical and Infrared Systems Market Leaders

-

Lockheed Martin Corporation

-

BAE Systems plc

-

Ultra Electronics Holdings

-

THALES

-

Leonardo S.p.A

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Military Electro-optical and Infrared Systems Market News

- October 2023: The US Defense Advanced Research Projects Agency (DARPA) released a broad agency announcement for the Intensity-Squeezed Photonic Integration for Revolutionary Detectors (INSPIRED) project. The goal is to develop small size, weight, and power consumption (SWaP) optical sensors with sensitivity below the quantum-shot noise limit by using so-called squeezed light.

- June 2022: Excelitas Technologies Corp., a leading industrial technology manufacturer focusing on innovative photonic solutions, showcased its latest thermal imaging and camera technologies for military applications at the Close Combat Symposium. The exhibited DRAGON-S12 Non-Cooled Thermal Attachment Sniper Sight featured a 60Hz uncooled thermal sensor coupled with a near-silent aperture, providing exceptional sensitivity and uniformity. The PHOENIX-S product, designed for demanding ground-based sniper missions, demonstrated field-proven capabilities for early detection, recognition, and identification of targets at longer ranges, even in extremely poor light conditions. Its attachment configuration enables easy integration into a variety of firearm systems and optical riflescopes with a magnification of up to 25x.

- May 2022: Israel Aerospace Industries (IAI) secured a contract to supply its MiniPOP electro-optical/infrared (EO/IR) systems for the Philippine Navy's patrol vessels. As per company specifications and Janes C4ISR & Mission Systems: Air, the MiniPOP is an EO/IR system that can integrate four sensors into a single optical payload. It features a gyrostabilized single line-replaceable unit (LRU) housing a medium-wave infrared (MWIR) thermal imager with an XBn detector, a high-definition complementary metal oxide semiconductor (HD-CMOS) day color camera with continuous zoom, a laser rangefinder, and an IR laser pointer.

Military Electro Optical and Infrared Systems Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Platform

- 5.1.1 Air-based

- 5.1.2 Land-based

- 5.1.3 Sea-based

-

5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Mexico

- 5.2.4.2 Brazil

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Elbit Systems Ltd.

- 6.2.3 Teledyne FLIR LLC

- 6.2.4 Israel Aerospace Industries Ltd.

- 6.2.5 L3Harris Technologies Inc.

- 6.2.6 Leonardo S.p.A

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Raytheon Technologies Corporation

- 6.2.9 Rheinmetall AG

- 6.2.10 Saab AB

- 6.2.11 THALES

- 6.2.12 Ultra Electronics Holdings

- *List Not Exhaustive

-

6.3 Other Players

- 6.3.1 Danbury Mission Technologies

- 6.3.2 System Controls

- 6.3.3 Zygo Corporation

- 6.3.4 Navitar

- 6.3.5 Optikos

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Military Electro-optical and Infrared Systems Industry Segmentation

Electro-optical and infrared systems, referred to as EO/IR systems, cover various distinct technologies based on targets and their missions. These sensors include visible spectrum and infrared sensors, due to which electro-optical/infrared (EO/IR) systems provide total situational awareness during both day and night, even in low light conditions. EO/IR sensors can be deployed in many ways. They are usually mounted on aircraft or vehicles used at sea or are hand-carried and can identify targets, track moving targets, and assess threats from a distance. Their applications include but are not limited to, airborne security, combat, patrol, surveillance, reconnaissance, and search and rescue operations.

The market has been segmented by platform and geography. By platform, the market is segmented into land-based, air-based, and sea-based. The report also covers the market sizes and forecasts for the military electro-optical and infrared systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Platform | Air-based | ||

| Land-based | |||

| Sea-based | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Mexico | ||

| Brazil | |||

| Rest of Latin America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Military Electro Optical and Infrared Systems Market Research FAQs

How big is the Military Electro-optical and Infrared Systems Market?

The Military Electro-optical and Infrared Systems Market size is expected to reach USD 9.16 billion in 2025 and grow at a CAGR of 2.80% to reach USD 10.52 billion by 2030.

What is the current Military Electro-optical and Infrared Systems Market size?

In 2025, the Military Electro-optical and Infrared Systems Market size is expected to reach USD 9.16 billion.

Who are the key players in Military Electro-optical and Infrared Systems Market?

Lockheed Martin Corporation, BAE Systems plc, Ultra Electronics Holdings, THALES and Leonardo S.p.A are the major companies operating in the Military Electro-optical and Infrared Systems Market.

Which is the fastest growing region in Military Electro-optical and Infrared Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Military Electro-optical and Infrared Systems Market?

In 2025, the North America accounts for the largest market share in Military Electro-optical and Infrared Systems Market.

What years does this Military Electro-optical and Infrared Systems Market cover, and what was the market size in 2024?

In 2024, the Military Electro-optical and Infrared Systems Market size was estimated at USD 8.90 billion. The report covers the Military Electro-optical and Infrared Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Military Electro-optical and Infrared Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Military Electro-optical And Infrared Systems Market Research

Mordor Intelligence offers a comprehensive analysis of the military electro-optical and infrared systems market, drawing on decades of expertise in defense technology research. Our extensive report examines advanced military surveillance systems and cutting-edge military imaging systems. It provides detailed insights into technological developments and operational capabilities. The analysis covers the latest innovations in military night vision technology and military thermal imaging applications. This offers stakeholders a thorough understanding of current market dynamics and future opportunities.

Our detailed research report, available as an easy-to-download PDF, provides an in-depth analysis of military thermal camera and military infrared camera technologies. It includes their integration into modern defense platforms. The study examines various applications of military thermal sight systems, offering valuable insights for manufacturers, suppliers, and defense contractors. Stakeholders gain access to comprehensive data on procurement trends, technological advancements, and strategic developments across major defense markets. This is supported by expert analysis and forecasting methodologies that ensure informed decision-making.