| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.43 Billion |

| Market Size (2030) | USD 1.89 Billion |

| CAGR (2025 - 2030) | 5.79 % |

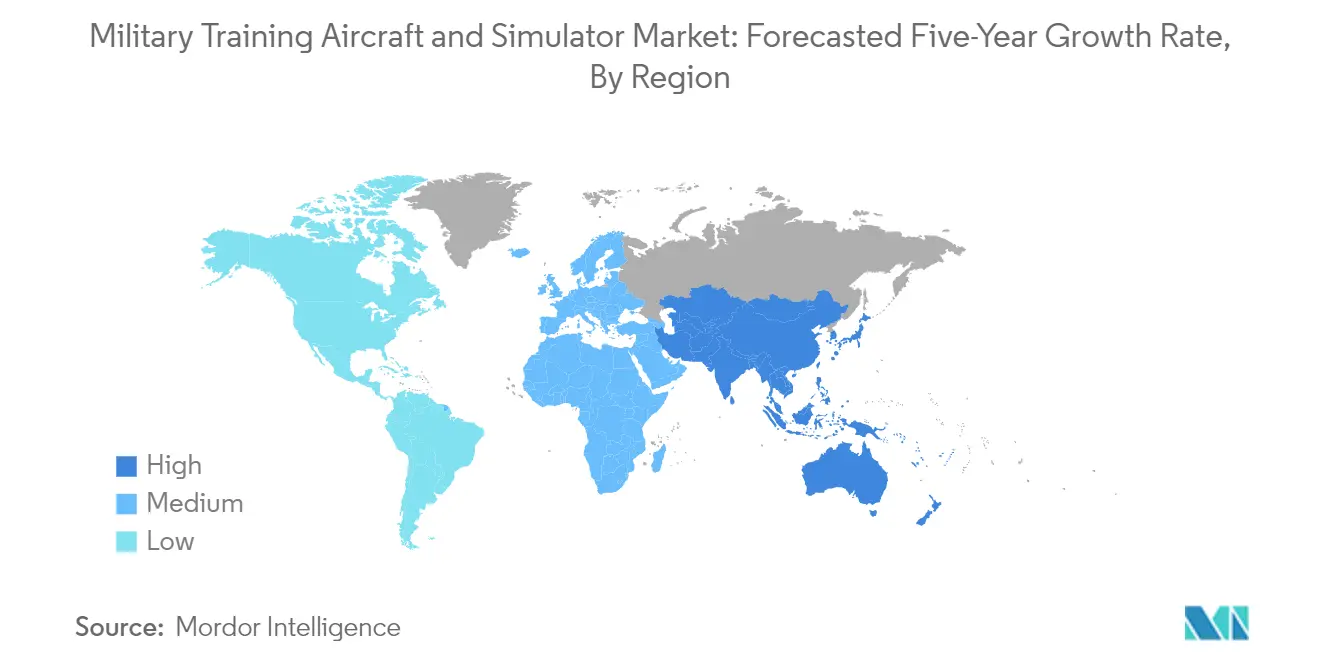

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Military Aircraft Simulation & Training Market Analysis

The Military Aerospace Simulation And Training Market size is estimated at USD 1.43 billion in 2025, and is expected to reach USD 1.89 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030).

The military aerospace simulation and training landscape is experiencing significant technological transformation, driven by the integration of advanced technologies and changing training requirements. The United States, being the largest military aviation force globally, maintains a substantial fleet of 14,061 aircraft as of 2019, with 2,634 dedicated trainer aircraft in 2023, highlighting the massive scale of military aviation training infrastructure. The evolution of training methodologies has led to the development of sophisticated flight simulators that combine virtual reality, artificial intelligence, and advanced graphics to create highly realistic training environments.

The industry is witnessing a strong push towards the modernization of training fleets and simulation systems across major military powers. This is evidenced by significant procurement activities, such as the US Navy's USD 677.2 million contract with Textron Aviation in January 2023 for up to 64 T-54A multi-engine training system aircraft, and the Indian Defense Ministry's USD 825.67 million agreement with Hindustan Aeronautics Limited in March 2023 for 70 HTT-40 basic trainer aircraft. These investments reflect the growing emphasis on developing comprehensive military training systems capabilities to meet evolving military aviation requirements.

The simulation technology sector is undergoing rapid advancement with the introduction of innovative solutions. In December 2022, Leonardo unveiled its groundbreaking Smart Chair simulation technology, capable of replicating next-generation fighter jet cockpits with minimal physical components. This trend towards more compact, versatile simulation systems is reshaping the training landscape, with companies like Diamond Aircraft Industries supporting over 5,500 training aircraft globally for various training operations, demonstrating the substantial scale of the training infrastructure.

The market is characterized by increasing adoption of integrated training solutions that combine both live aircraft training and advanced simulation systems. This is exemplified by the United Arab Emirates Air Force's comprehensive approach to training, maintaining 47% of its 335-unit fleet as training aircraft, while simultaneously investing in advanced military simulation technologies. The trend towards such balanced training approaches is gaining traction globally, as military forces seek to optimize training effectiveness while managing operational costs and maintaining readiness levels. The use of military flight simulators is becoming increasingly prevalent, enhancing the realism and effectiveness of aerospace training programs.

Military Aircraft Simulation & Training Market Trends

Geopolitical Tensions Across the World and Changing Battlefield Scenario

The ever-evolving nature of global conflicts and increasing geopolitical tensions have fundamentally transformed the requirements for military pilot training. In recent years, the battlefield scenario has become increasingly complex, with modern combat aircraft becoming more avionics-intensive and featuring sophisticated all-glass cockpits based on waypoint navigation and advanced software systems. This technological evolution has made it imperative for defense forces to train their pilots using ground-based full mission simulators (FMS) for both routine flights and advanced combat simulation missions. The changing nature of warfare, coupled with the rise in unresolved regional tensions, breakdown in rule of law, and scarcity of resources, has led to a significant increase in the demand for advanced military aircraft simulators and military training software systems globally.

The defense forces worldwide are responding to these challenges by investing heavily in sophisticated training infrastructure. For instance, in March 2023, Leonardo introduced its Smart Chair simulation-based pilot training technology, which allows for advanced pilot training in multi-domain scenarios and can potentially replicate a sixth-generation fighter jet cockpit. Similarly, in April 2023, VRgineers announced the development of a mobile cockpit simulator for virtual reality flight training that fits into a compact suitcase, developed in cooperation with the US Marine Corps. These advancements in simulator technology are directly addressing the need to prepare pilots for modern battlefield scenarios, where the integration of artificial intelligence, advanced avionics, and complex mission parameters requires extensive training in realistic, simulated environments.

Understand The Key Trends Shaping This Market

Download PDF

Acquisitions of Military Trainer Aircraft

The global defense landscape has witnessed a surge in the acquisition of military trainer aircraft, driven by the increasing need for advanced pilot training systems and the modernization of existing training fleets. In March 2023, the Indian Defense Ministry sealed a significant deal with Hindustan Aeronautics Limited (HAL) for the procurement of 70 HTT-40 basic trainer aircraft at a cost of over USD 825.67 million for the Indian Air Force. Similarly, in March 2023, the Spanish Air Force ordered 16 additional PC-21 next-generation trainer aircraft from Swiss aerospace manufacturer Pilatus Aircraft, making Spain the largest operator of trainer aircraft in Europe. These acquisitions demonstrate the growing emphasis on developing robust pilot training capabilities across major military powers.

The trend of military trainer aircraft acquisition is further exemplified by recent developments in the Middle East and Asia-Pacific regions. In February 2023, China's National Aero-Technology Import & Export Corporation (CATIC) secured a contract to export domestically developed L-15 advanced trainer jets to the United Arab Emirates, with the initial order comprising 12 aircraft and options for an additional 36 units. Additionally, in February 2023, BAE Systems and FSTC announced plans to design, build, and supply simulators to train pilots of the Indian Armed Forces, including the development of a twin-dome full mission simulator for the BAE Systems Hawk 132 jet trainer aircraft. These developments highlight the growing recognition among defense forces worldwide of the need to enhance their training capabilities through modern trainer aircraft and advanced aviation training devices and military virtual reality training systems.

Segment Analysis: Aircraft Type

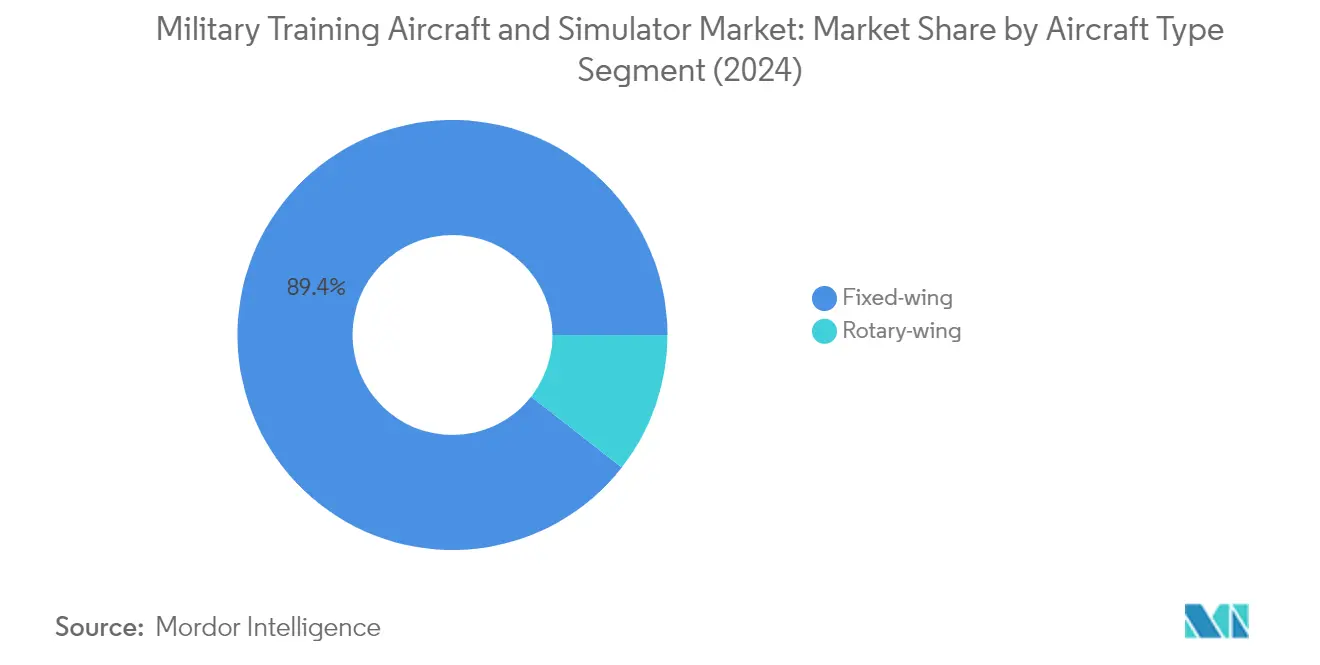

Fixed-wing Segment in Military Training Aircraft and Simulator Market

The fixed-wing segment dominates the military training aircraft and simulator market, commanding approximately 89% market share in 2024. This substantial market position is driven by the extensive use of fixed-wing aircraft in military pilot training programs worldwide. Fixed-wing trainers offer versatile and transferable skill sets, making them ideal for preparing pilots for various operational roles. These aircraft provide extended endurance, higher speeds, superior maneuverability, and cost-effectiveness compared to other training platforms. The segment's dominance is further strengthened by the existing infrastructure at military bases globally, which is primarily designed to support fixed-wing operations. The demand for fixed-wing trainer aircraft has grown significantly with the induction of new multi-mission and combat aircraft models into active service, as militaries worldwide focus on modernizing their training fleets to align with advanced operational requirements.

Rotary-wing Segment in Military Training Aircraft and Simulator Market

The rotary-wing segment is projected to experience the fastest growth in the military training aircraft and simulator market between 2024 and 2029, with an estimated growth rate of around 6%. This accelerated growth is attributed to the increasing importance of helicopter operations in modern military missions. The segment's expansion is driven by the specialized nature of rotary-wing training, which requires pilots to master unique flight characteristics including hover capabilities, vertical takeoff and landing, autorotation, and low-speed maneuvering. Military forces are increasingly investing in advanced rotary-wing training platforms to support special operations forces in missions requiring rapid insertion, extraction, and close air support. The growing emphasis on night vision operations, fast roping, rappelling, and other specialized helicopter tactics is driving the demand for sophisticated rotary-wing training solutions.

Segment Analysis: Engine Type

Turbofan Segment in Military Training Aircraft and Simulator Market

The turbofan segment dominates the military training aircraft and simulator market, commanding approximately 48% of the total market share in 2024. This significant market position is driven by the superior capabilities of turbofan engines in advanced military trainer aircraft. Most turbofan aircraft feature modern avionics systems, including digital cockpits, advanced flight controls, navigation systems, and integrated sensor packages. These aircraft offer superior speed, climb rates, and maneuverability compared to other engine types, making them ideal for preparing pilots for operational military aircraft powered by similar or more advanced turbofan engines. The segment's growth is further bolstered by the advent of supersonic flight capabilities in new-generation combat aircraft, which has necessitated the adoption of similar versions of trainer aircraft. Additionally, with hypersonic weaponry being developed, the speed and agility requirements of new combat aircraft are expected to increase, thereby creating sustained demand for new generation advanced trainer aircraft powered by high-performance turbofan engines.

Turboprop Segment in Military Training Aircraft and Simulator Market

The turboprop segment represents a significant portion of the military training aircraft market, serving as a crucial stepping stone in pilot training programs. This segment is experiencing robust growth as many military aircraft, including transport planes and surveillance aircraft, are turboprop-powered. Training pilots on turboprops allows for a smoother transition to these turbine-powered platforms as trainees become familiar with the principles of turbine engines, managing engine power, and operating more complex systems. The segment's growth is supported by the fact that turboprop aircraft are typically equipped with multiple engines, providing an opportunity for trainee pilots to gain experience in multi-engine operations. Some models of turboprop aircraft used in military training can be equipped with simulated weapon systems, allowing pilots to practice tactical maneuvers, weapons delivery, and engagement procedures, which enhances their combat readiness and prepares them for the integration of weapons and sensor systems on operational military aircraft.

Remaining Segments in Engine Type

The piston and turboshaft engine segments play vital complementary roles in military aviation training. Piston aircraft are predominantly used for basic flight training, particularly for ab-initio training of new pilots, providing a cost-effective platform for trainees to master fundamental flying skills. The turboshaft segment primarily serves the rotary-wing training sector, where helicopters are essential for specialized missions such as search and rescue, close air support, and special operations. These segments are crucial in providing a comprehensive training ecosystem that caters to different stages of pilot development and various mission requirements. Both engine types continue to evolve with technological advancements, focusing on improved fuel efficiency, reduced maintenance requirements, and enhanced training capabilities to meet modern military aviation training needs.

Segment Analysis: By Engine Count

Single Engine Segment in Military Training Aircraft and Simulator Market

The single engine segment continues to dominate the military training aircraft and simulator market, commanding approximately 62% of the total market share in 2024. This significant market position is primarily driven by the widespread use of single-engine aircraft for primary training phases in military aviation programs worldwide. Single engine trainer aircraft are particularly valued for their simplified construction and minimal complicated equipment, making them ideal for basic flight training and familiarization. These aircraft provide an optimal platform for trainee pilots to master fundamental flying skills, including takeoffs, landings, climbs, descents, and basic maneuvering. The segment's dominance is further reinforced by the cost-effectiveness and operational efficiency of single-engine platforms compared to their multi-engine counterparts, making them the preferred choice for initial pilot training programs across global defense forces.

Multi Engine Segment in Military Training Aircraft and Simulator Market

The multi-engine segment is emerging as the fastest-growing category in the market, projected to expand at approximately 6% through 2024-2029. This growth trajectory is driven by the increasing complexity of modern military aircraft operations and the growing need for advanced training capabilities. Multi-engine trainers play a crucial role in preparing pilots for transition to more sophisticated aircraft platforms, particularly for those who will operate transport aircraft, tankers, and other multi-engine military aircraft. The segment's growth is further supported by the rising demand for comprehensive training solutions that can effectively bridge the gap between basic flight training and advanced operational requirements. Military organizations worldwide are increasingly investing in multi-engine training platforms to ensure their pilots are well-prepared for the complexities of modern military aviation, including mission-specific training and advanced tactical operations.

Segment Analysis: By Seat Count

Dual Seat Segment in Military Training Aircraft and Simulator Market

The dual seat configuration dominates the military training aircraft and simulator market, commanding approximately 73% market share in 2024. This configuration has emerged as the preferred choice for military training applications due to its inherent advantages in pilot instruction. The side-by-side or tandem seating arrangements in dual-seat aircraft enable direct interaction between the instructor and trainee pilot, facilitating real-time guidance and correction during flight operations. This setup is particularly valuable for both elementary and advanced training phases, allowing instructors to demonstrate complex maneuvers and monitor trainee performance closely. The dual-seat configuration also proves essential for long-range combat missions, where one pilot can focus on aircraft control while the other manages mission-critical tasks. Major aircraft manufacturers have recognized this demand, incorporating dual-seat configurations across their trainer aircraft portfolios to meet the evolving requirements of global defense forces.

Single Seat Segment in Military Training Aircraft and Simulator Market

The single-seat configuration segment is projected to exhibit the highest growth rate of approximately 6% during the forecast period 2024-2029. This growth trajectory is primarily driven by the increasing adoption of retired fighter aircraft being repurposed as single-seat trainers, offering a cost-effective solution for advanced pilot training programs. The segment's expansion is further supported by technological advancements in autonomous systems and enhanced flight control technologies, which are making single-seat configurations more viable for specific training scenarios. Military organizations are increasingly incorporating single-seat trainers into their advanced training phases, particularly for specialized combat training where pilots need to develop independent decision-making capabilities. The integration of advanced avionics and sophisticated simulation systems in single-seat platforms is enabling more comprehensive training experiences, contributing to the segment's accelerated growth rate.

Segment Analysis: By Simulator Type

Full Flight Simulators Segment in Military Training Aircraft and Simulator Market

Full Flight Simulators (FFS) maintain their dominant position in the military training aircraft and simulator market, commanding approximately 48% market share in 2024. These high-fidelity simulation systems provide the most realistic and comprehensive training experience for military pilots, replicating actual aircraft behavior and operational scenarios with exceptional accuracy. The segment's leadership is driven by increasing demands for ultra-realistic training experiences that safely expose pilots-in-training to challenging real-world scenarios. Military organizations worldwide are investing heavily in FFS technology to enhance pilot proficiency while reducing operational costs and risks associated with live aircraft training. The growing complexity of modern military aircraft and mission requirements has further cemented the importance of FFS in military pilot training programs. These simulators offer advanced features like high-resolution visual systems, motion platforms, and sophisticated aerodynamic modeling that closely mirror actual aircraft performance.

Flight Training Devices Segment in Military Training Aircraft and Simulator Market

Flight Training Devices (FTD) represent the fastest-growing segment in the military training aircraft and simulator market, driven by their cost-effectiveness and versatility in pilot training programs. These devices offer a more accessible yet effective training solution compared to full flight simulators, making them increasingly popular among military organizations looking to expand their training capabilities. The segment's growth is fueled by technological advancements in visual systems, computing power, and software capabilities that have significantly enhanced the training experience. Military forces are increasingly adopting FTDs for procedural training, instrument flight rules (IFR) training, and basic flight operations practice. The integration of advanced features like augmented reality and artificial intelligence in modern FTDs has further boosted their appeal. Additionally, the compact footprint and lower maintenance requirements of FTDs make them an attractive option for military training facilities with space or budget constraints.

Remaining Segments in Military Training Aircraft Simulator Types

Other simulator types in the military training market encompass a range of specialized training devices, including Advanced Aviation Training Devices (AATDs) and Basic Aviation Training Devices (BATDs). These systems play a crucial complementary role in military pilot training programs by providing focused training for specific skills and procedures. They serve as essential tools in the early stages of pilot training, helping cadets familiarize themselves with basic flight concepts and procedures before progressing to more advanced simulators. These devices are particularly valuable for familiarization training, procedure practice, and basic instrument training. The integration of these various simulator types creates a comprehensive training ecosystem that allows military organizations to develop pilot proficiency through a structured and progressive approach. Their continued evolution and integration with newer technologies ensure they remain relevant in modern military training programs.

Segment Analysis: By Training Purpose

Combat Training Segment in Military Training Aircraft and Simulator Market

Combat training emerged as the dominant segment in the military training aircraft and simulator market, accounting for approximately 43% market share in 2024. This significant market position is attributed to the growing demand for military aircraft and rising spending on pilot training for combat missions. The segment's growth is driven by increasing adoption of advanced military simulators and growing expenditure on research and development of sophisticated combat training solutions. Military organizations worldwide are investing heavily in combat training infrastructure to prepare pilots for modern warfare scenarios. The rise in geopolitical tensions and evolving battlefield requirements have further accelerated the demand for advanced combat training systems. Leading manufacturers in the market are developing numerous solutions such as weapon system analysis software, threat environment simulation, weapon system trainers, and air combat training ranges with highly adaptable low-cost flight simulator options and integrated Instructor Operating Systems.

Weapons Training Segment in Military Training Aircraft and Simulator Market

The weapons training segment is projected to demonstrate remarkable growth in the market during the forecast period 2024-2029, with an expected growth rate of approximately 3%. This growth trajectory is primarily driven by increasing expenditure from defense forces on military aircraft pilots and growing procurement of military training aircraft. The segment's expansion is supported by the development of sophisticated weapons training simulators that provide realistic combat scenarios. Military organizations are increasingly focusing on weapons training to enhance their operational readiness and combat effectiveness. The integration of advanced technologies like virtual reality and augmented reality in weapons training simulators is further propelling segment growth. Leading companies are continuously innovating to develop more sophisticated weapons training systems that can simulate various mission scenarios and weapons systems, enabling pilots to gain proficiency in different combat situations.

Remaining Segments in Training Purpose Market Segmentation

The flight training segment represents another crucial component of the military training aircraft and simulator market. This segment focuses on fundamental aspects of aircraft handling, including low-level missions, instrument flying, air-to-air combat, and air-to-air refueling. Flight training encompasses all aspects of basic and advanced flight instruction, providing essential foundational skills for military pilots. The segment is characterized by comprehensive training programs that combine simulation, academic instruction, and actual flight experience. Military organizations worldwide recognize the importance of robust flight training programs in developing skilled pilots capable of operating advanced aircraft systems. The segment continues to evolve with the integration of new technologies and training methodologies, ensuring pilots receive thorough preparation for various operational scenarios.

Military Aerospace Simulation and Training Market Geography Segment Analysis

Military Training Aircraft and Simulator Market in North America

The North American military training aircraft and simulator market demonstrates significant strength driven by extensive military aviation programs and substantial defense investments across the United States and Canada. The region maintains sophisticated pilot training infrastructure with numerous dedicated facilities and advanced simulation centers. Both countries have well-established networks of airports and fixed-base operators supporting military aviation activities, including training exercises, aircraft maintenance, and logistical support. The presence of major aircraft manufacturers and simulator providers further strengthens the regional market ecosystem through continuous technological innovations and enhanced training capabilities, including the use of military simulation technologies.

Military Training Aircraft and Simulator Market in United States

The United States dominates the North American market with approximately 95% market share in 2024. The country maintains the world's largest fleet of military aircraft and the highest defense budget globally. The U.S. armed forces operate numerous dedicated training facilities and ranges for military aviation, including Air Force Bases, Naval Air Stations, and Army Airfields primarily used for training purposes. The Joint Base San Antonio-Randolph in Texas serves as a prime example, being home to the 12th Flying Training Wing and functioning as the primary training center for U.S. Air Force pilots. The country's robust training infrastructure includes a comprehensive network of simulation centers equipped with state-of-the-art full flight simulators and advanced training devices.

Military Training Aircraft and Simulator Market in Canada

Canada exhibits strong growth potential with an expected CAGR of approximately 4% during 2024-2029. The Royal Canadian Air Force (RCAF) is actively modernizing its training capabilities through various initiatives and partnerships. The country's pilot training infrastructure includes the Canadian Forces Flying Training School in Portage la Prairie and the NATO Flight Training Centre in Moose Jaw, providing comprehensive training from basic to advanced levels. Canada's commitment to enhancing its military aviation capabilities is evident through its Future Aircrew Training (FAcT) program, which aims to revolutionize pilot training over the next two decades. The country's focus on adopting advanced pilot training simulator technologies and modernizing its training aircraft fleet positions it for sustained growth in the market.

Military Training Aircraft and Simulator Market in Europe

The European military training aircraft and simulator market showcases strong development through collaborative defense initiatives and modernization programs across multiple countries. The region benefits from advanced aerospace capabilities in the United Kingdom, Germany, France, and Italy, each contributing unique strengths to the overall market landscape. These nations maintain sophisticated military training infrastructures and regularly participate in joint training exercises, fostering interoperability and shared expertise. The European market is characterized by strong domestic manufacturing capabilities and ongoing investments in next-generation military training systems.

Military Training Aircraft and Simulator Market in United Kingdom

The United Kingdom leads the European market with approximately 24% market share in 2024. The country's military aviation training infrastructure is anchored by the Royal Air Force College Cranwell, the world's first Air Academy, which provides comprehensive training for all RAF officers. The UK's Military Flying Training System (MFTS), operated through a partnership between industry leaders and the Ministry of Defence, delivers advanced flight training solutions for the British Royal Air Force, Army Air Corps, and Royal Navy. The nation maintains multiple active military airfields and training facilities, supported by a robust network of simulation centers and training devices, including pilot training simulators.

Military Training Aircraft and Simulator Market in France

France demonstrates strong market momentum with an anticipated CAGR of approximately 4% during 2024-2029. The French Air Force Academy (FAFA) serves as the cornerstone of the country's military aviation training, providing comprehensive instruction for various specializations including fighter pilots, helicopter pilots, and transport aircraft pilots. The country's commitment to military aviation excellence is reflected in its advanced training infrastructure and continuous investment in modern simulation technologies. France's strategic focus on developing next-generation training capabilities and maintaining a modern fleet of trainer aircraft positions it as a key growth driver in the European market.

Military Training Aircraft and Simulator Market in Asia-Pacific

The Asia-Pacific military training aircraft and simulator market demonstrates robust development driven by increasing defense modernization initiatives across China, India, Japan, and South Korea. The region witnesses substantial investments in military aviation training infrastructure, with countries focusing on developing indigenous capabilities while maintaining strategic partnerships with global aerospace leaders. The market is characterized by a growing emphasis on advanced simulation technologies and the modernization of trainer aircraft fleets to meet evolving military requirements, including the integration of aerospace training solutions.

Military Training Aircraft and Simulator Market in China

China leads the Asia-Pacific market through its comprehensive military aviation training programs and substantial investments in training infrastructure. The People's Liberation Army Air Force maintains extensive training facilities and has implemented new training curricula to enhance pilot proficiency. The country's focus on developing indigenous training capabilities, coupled with its strategic partnerships with international aerospace companies, strengthens its position in the regional market. China's commitment to military aviation excellence is reflected in its continuous efforts to modernize training methodologies and equipment, including the adoption of advanced military simulation technologies.

Military Training Aircraft and Simulator Market in India

India exhibits remarkable growth potential in the military training aircraft and simulator market. The Indian Air Force maintains multiple training establishments, with the Air Force Academy at Dundigal serving as the primary institution for pilot training. The country's indigenous aerospace capabilities, coupled with strategic international partnerships, contribute to its expanding military aviation training infrastructure. India's focus on modernizing its trainer aircraft fleet and enhancing simulation-based training capabilities positions it for sustained growth in the regional market.

Military Training Aircraft and Simulator Market in Latin America

The Latin American military training aircraft and simulator market shows steady development, with Brazil emerging as both the largest and fastest-growing market in the region. The market benefits from established aerospace manufacturing capabilities and growing investments in military aviation training infrastructure across various countries. Brazil's leadership is supported by its robust domestic aerospace industry and comprehensive military pilot training programs, while other countries in the region continue to modernize their training capabilities through strategic partnerships and technology acquisitions. The region's focus on enhancing military aviation capabilities drives continued investment in advanced training platforms and simulation technologies.

Military Training Aircraft and Simulator Market in Middle East & Africa

The Middle East & Africa military training aircraft and simulator market demonstrates strong potential, driven by substantial defense investments and modernization initiatives across multiple countries. The United Arab Emirates emerges as the largest market in the region, while Saudi Arabia shows the fastest growth trajectory. The region benefits from significant defense spending and strategic partnerships with global aerospace leaders, leading to the establishment of advanced training facilities and the adoption of modern simulation technologies. Countries across the region are actively expanding their military aviation training capabilities through investments in new training aircraft and advanced simulation systems, supported by growing domestic aerospace capabilities and international collaborations.

Get Analysis on Important Geographic Markets

Download PDF

Military Aircraft Simulation & Training Industry Overview

Top Companies in Military Aerospace Simulation and Training Market

The military aerospace simulation and training market features prominent players like CAE Inc., Raytheon Technologies, Boeing, Northrop Grumman, and Textron leading the innovation landscape. These companies are increasingly focusing on developing advanced simulation technologies incorporating artificial intelligence, virtual reality, and mixed reality capabilities to enhance training effectiveness. Strategic partnerships with defense organizations and continuous investment in research and development remain key priorities across the industry. Companies are expanding their product portfolios through the development of portable training solutions and cloud-based platforms to provide flexible training options. The industry is witnessing a shift towards more sustainable and cost-effective training solutions, with manufacturers emphasizing electric propulsion technologies and lightweight trainer aircraft development. Market leaders are also strengthening their positions through strategic acquisitions and collaborations to enhance their technological capabilities and expand their global footprint in the flight simulator market.

Consolidated Market with Strong Defense Ties

The military aerospace simulation and training market exhibits a highly consolidated structure dominated by large defense contractors and specialized simulation technology providers. These established players leverage their long-standing relationships with military organizations, extensive intellectual property portfolios, and significant technological expertise to maintain their market positions. The market demonstrates high barriers to entry due to substantial capital requirements, stringent regulatory standards, and the need for specialized knowledge in both aerospace and simulation technologies. The industry has witnessed strategic acquisitions aimed at expanding capabilities and geographic reach, with companies like Leonardo and BAE Systems actively pursuing inorganic growth opportunities.

The competitive landscape is characterized by a mix of global defense conglomerates and specialized simulation providers, each bringing unique strengths to the market. Global players like Boeing and Northrop Grumman leverage their extensive aerospace expertise and established defense relationships, while specialists like CAE Inc. focus on developing cutting-edge simulation technologies. The market shows regional variations in competitive dynamics, with different players holding strong positions in specific geographic markets based on local defense relationships and manufacturing capabilities. Companies are increasingly focusing on developing comprehensive training solutions that combine both hardware and software components to provide end-to-end training capabilities. This approach is particularly relevant in the military simulation market, where integrated solutions are essential.

Innovation and Adaptability Drive Market Success

Success in the military aerospace simulation and training market increasingly depends on companies' ability to innovate and adapt to evolving military training requirements. Market leaders are investing heavily in next-generation technologies such as high-fidelity graphics, portable simulation devices, and integrated training systems that can seamlessly connect live, virtual, and constructive training environments. Companies are also focusing on developing cost-effective solutions that can address the growing demand for military pilot training while maintaining high training standards. The ability to provide customizable solutions that can be rapidly adapted to different aircraft types and training scenarios has become a crucial differentiator in the market.

For new entrants and emerging players, success lies in identifying and exploiting specific market niches while building strong relationships with defense organizations. Companies must navigate complex regulatory requirements while demonstrating clear value propositions in terms of training effectiveness and cost efficiency. The concentration of buyers in the defense sector necessitates long-term relationship building and proven track records of reliability and performance. Future market success will increasingly depend on companies' ability to integrate emerging technologies, adapt to changing training requirements, and provide sustainable solutions that align with military modernization initiatives. The growing emphasis on environmental sustainability and cost reduction in military training programs will also shape competitive strategies moving forward, particularly in the context of the military synthetic training environment and aerospace modeling and simulation. Additionally, the role of defense simulation in enhancing training effectiveness cannot be overstated.

Military Aircraft Simulation & Training Market Leaders

-

TRU Simulation + Training Inc.

-

FlightSafety International Inc.

-

CAE Inc.

-

THALES

-

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Military Aircraft Simulation & Training Market News

- July 2024: Romania planned to finalize a government-to-government deal with the United States. Romania aims to procure 32 F-35 aircraft from Lockheed Martin Corporation at USD 6.5 billion. This agreement covers the aircraft and includes logistics, training services, flight simulators, and ammunition.

- October 2023: Fidelity secured a USD 18 million contract to design and procure a UH-60M flight simulator. The project will be carried out in Slovakia and is expected to be completed in 2027.

Military Aerospace Simulation And Training Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Simulator Type

- 5.1.1 Full Flight Simulator (FFS)

- 5.1.2 Flight Training Devices (FTD)

- 5.1.3 Other Simulator Types

-

5.2 By Aircraft Type

- 5.2.1 Rotorcraft

- 5.2.2 Fixed-Wing

- 5.2.3

-

5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 L3Harris Technologies, Inc.

- 6.2.2 RTX Corporation

- 6.2.3 BAE Systems plc

- 6.2.4 The Boeing Company

- 6.2.5 CACI International Inc.

- 6.2.6 CAE Inc.

- 6.2.7 Merlin Simulation Inc.

- 6.2.8 Lockheed Martin Corporation

- 6.2.9 THALES

- 6.2.10 TRU Simulation + Training Inc.

- 6.2.11 Rheinmetall AG

- 6.2.12 Northrop Grumman Corporation

- 6.2.13 Flight Safety International Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Military Aircraft Simulation & Training Industry Segmentation

Flight simulators artificially recreate the environment for pilot training purposes. They not only deliver knowledge about flying but also provide pilots with experience in reacting to emergencies.

The military aircraft simulation and training market is segmented by simulator type, aircraft type, and geography. Based on the simulator type, the market is segmented into full-flight simulators (FFS), flight training devices (FTD), and other simulator types. The other simulator types include fixed-base simulators, computer-based simulators, cockpit procedures trainers (CPT), and part-task trainers (PTT). Based on Aircraft Type, the market is segmented into Rotorcraft and Fixed-Wing. The report also covers the market sizes and forecasts for the military aircraft simulator & training market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Simulator Type | Full Flight Simulator (FFS) | ||

| Flight Training Devices (FTD) | |||

| Other Simulator Types | |||

| By Aircraft Type | Rotorcraft | ||

| Fixed-Wing | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Military Aerospace Simulation And Training Market Research Faqs

How big is the Military Aerospace Simulation And Training Market?

The Military Aerospace Simulation And Training Market size is expected to reach USD 1.43 billion in 2025 and grow at a CAGR of 5.79% to reach USD 1.89 billion by 2030.

What is the current Military Aerospace Simulation And Training Market size?

In 2025, the Military Aerospace Simulation And Training Market size is expected to reach USD 1.43 billion.

Who are the key players in Military Aerospace Simulation And Training Market?

TRU Simulation + Training Inc., FlightSafety International Inc., CAE Inc., THALES and RTX Corporation are the major companies operating in the Military Aerospace Simulation And Training Market.

Which is the fastest growing region in Military Aerospace Simulation And Training Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Military Aerospace Simulation And Training Market?

In 2025, the North America accounts for the largest market share in Military Aerospace Simulation And Training Market.

What years does this Military Aerospace Simulation And Training Market cover, and what was the market size in 2024?

In 2024, the Military Aerospace Simulation And Training Market size was estimated at USD 1.35 billion. The report covers the Military Aerospace Simulation And Training Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Military Aerospace Simulation And Training Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Military Aerospace Simulation And Training Market Research

Mordor Intelligence provides comprehensive expertise in analyzing the military simulation market. We offer deep insights into aerospace training and advanced simulation technologies. Our extensive research covers the evolution of flight simulator technology. This includes sophisticated cockpit simulator systems and air combat simulation platforms. The report offers a detailed analysis of military training systems and aviation training devices. We focus particularly on emerging technologies like aerospace digital twin applications and military virtual reality training solutions. Available as an easy-to-download report PDF, our research encompasses both traditional pilot training simulator approaches and cutting-edge defense simulation methodologies.

Stakeholders in the flight simulator industry benefit from our thorough examination of military training software and combat simulation trends. The report delivers actionable insights into military serious games development and the implementation of military synthetic training environment solutions. Our analysis covers the latest advances in aerospace modeling and simulation, including military virtual training applications and specialized military flight simulator technologies. The comprehensive coverage ensures decision-makers stay informed about innovations in military simulation and training. This supports strategic planning and investment decisions in this rapidly evolving sector.