Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

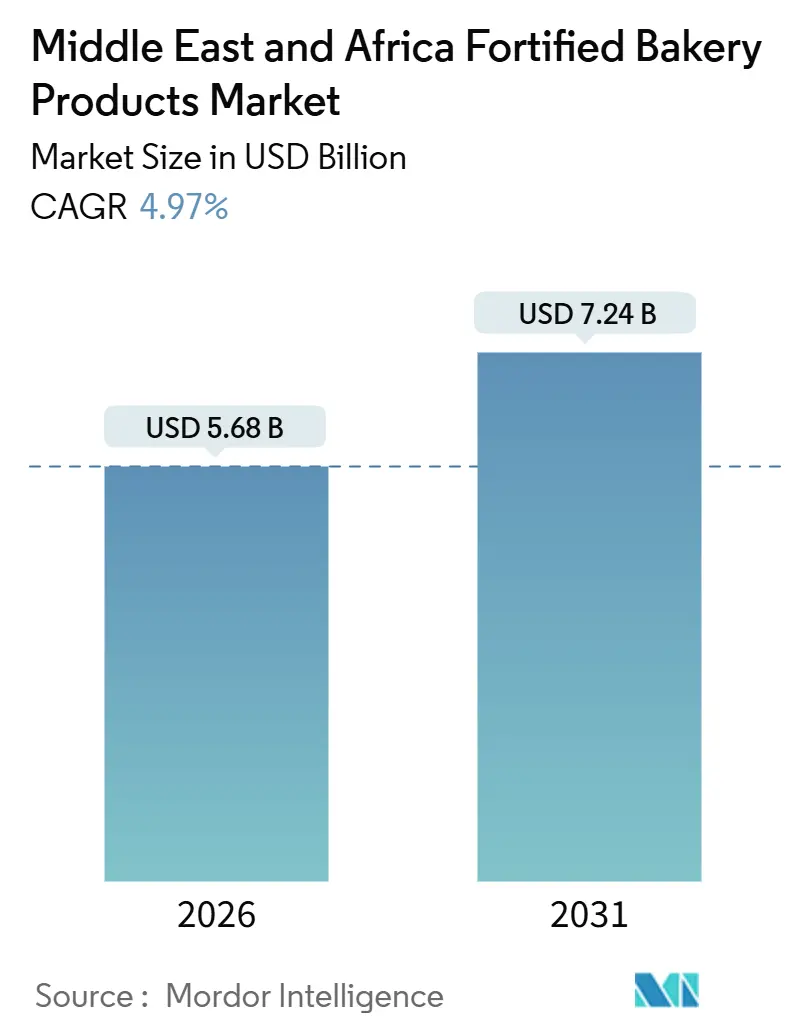

| Market Size (2026) | USD 5.68 Billion |

| Market Size (2031) | USD 7.24 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Fortified Bakery Products Market Analysis by Mordor Intelligence

The fortified bakery products market in the Middle East and Africa is projected to grow from USD 5.68 billion in 2026 to USD 7.24 billion by 2031, registering a CAGR of 4.97%. Significant structural changes are occurring as eleven Middle Eastern governments have transitioned from voluntary micronutrient guidelines to mandatory flour-fortification regulations. Additionally, Egypt reinstated its previously suspended program in 2025, establishing iron and folic acid fortification as a compulsory standard for all mills. Factors such as Saudi Arabia's SFDA standards, Turkey's bread-focused dietary habits, increasing e-commerce penetration, and a growing consumer preference for clean-label functional foods are driving steady mid-single-digit growth. However, challenges such as raw material price volatility, complex regulatory labeling requirements, and high dependency on imported premixes continue to impact profit margins and increase operational risks.

Key Report Takeaways

- By product type, fortified bread led with a 52.09% revenue share in 2025, while fortified biscuits and cookies are the fastest-growing category at a 4.36% CAGR over the same horizon.

- By fortified micronutrient, minerals-fortified products captured 46.10% share in 2025; fiber/protein enriched variants record the highest projected CAGR at 5.79% to 2030.

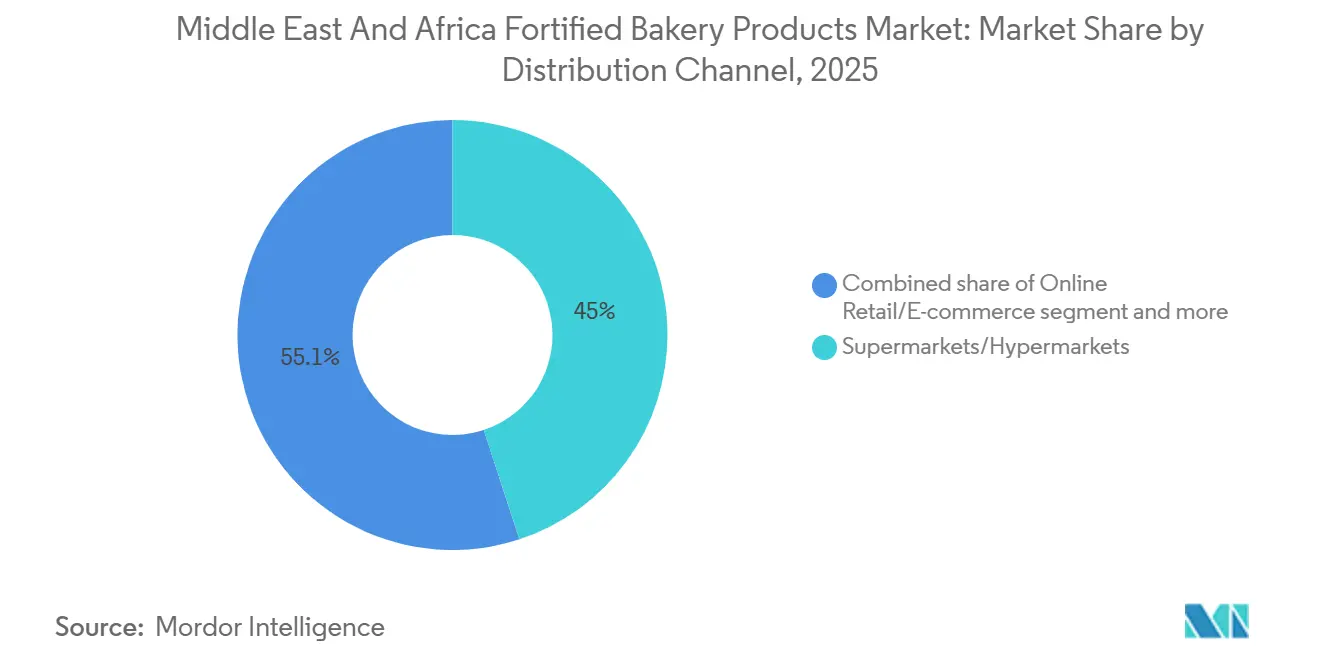

- By distribution channel, supermarkets/hypermarkets held a 44.95% share in 2025, yet Online Retail /E-commerce is advancing at a 6.14% CAGR through 2030.

- By geography, Saudi Arabia commanded a 29.58% share in 2025, whereas Turkey shows the fastest trajectory at a 5.88% CAGR out to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Fortified Bakery Products Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed food security and nutritional resilience objectives | +1.2% | Middle East (11 of 22 countries), Egypt, Morocco, Nigeria, South Africa | Medium term (2-4 years) |

| Growing consumer health-consciousness and functional-food demand | +1.0% | Saudi Arabia, United Arab Emirates, Turkey, and urban centers across the Middle East and Africa | Short term (≤ 2 years) |

| Cultural integration of bread and bakery staples | +0.9% | Turkey, Saudi Arabia, Egypt, Morocco, broader Middle East | Long term (≥ 4 years) |

| Rising consumer awareness of micronutrient deficiencies | +1.1% | Nigeria, Egypt, Saudi Arabia, broader EMRO region | Medium term (2-4 years) |

| Rising interest in pediatric and family nutrition | +0.8% | Nigeria, United Arab Emirates, Saudi Arabia, Egypt | Short term (≤ 2 years) |

| Clean-label and natural fortification preference | +0.7% | Turkey, United Arab Emirates, Saudi Arabia, urban Middle East and Africa markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed food security and nutritional resilience objectives

Government-supported food security and nutritional resilience initiatives are key drivers of growth in the Middle East and Africa fortified bakery products market. National and regional authorities across the region are implementing strategies aimed at improving population health, reducing micronutrient deficiencies, and enhancing food system stability. As of 2024, there were 1,502 active initiatives, with 674 completed and 596 progressing as planned, demonstrating a strong commitment to long-term food security goals under frameworks such as Vision 2030 and similar national development agendas [1]Source: Vision 2030, "Vision 2030 2024 Annual Report", vision2030.gov.sa. These policies increasingly require or encourage the fortification of staple foods, including bakery products, to address prevalent nutritional deficiencies (e.g., iron, folate, vitamin A) and reduce health issues such as anemia and micronutrient malnutrition. Government support includes mandatory fortification standards, subsidies for fortified flour and grains, public-private partnerships, and nutrition education campaigns to increase consumer awareness of the benefits of fortified products.

Growing consumer health-consciousness and functional-food demand

The increasing prevalence of lifestyle-related diseases in the Middle East and Africa is driving demand for fortified bakery products focused on preventive health and functional nutrition. Consumers are becoming more proactive in managing long-term health risks through daily diets, leading to a growing preference for bakery products fortified with omega-3 fatty acids, probiotics, prebiotics, fiber, and essential micronutrients. These products are recognized for their potential benefits in supporting heart health, digestive wellness, immunity, and metabolic balance. This trend is particularly significant given the high prevalence of cardiovascular health issues, with coronary heart disease accounting for 32.4% of total deaths in Egypt in 2024, highlighting the need for dietary solutions to mitigate chronic disease risk factors [2]Source: National Library of Medicine, "Cardiovascular Disease and Stroke Risk Among Egyptian Resident Physicians: A Cross-Sectional Multicenter Study", pmc.ncbi.nlm.nih.gov. Fortified breads, biscuits, and other functional bakery staples provide an accessible and culturally accepted means of delivering health-enhancing ingredients without requiring significant dietary changes. Additionally, with rising urbanization, sedentary lifestyles, and increased consumption of processed foods in the region, functional fortified bakery products are increasingly seen as practical options to address nutritional deficiencies and promote healthier lifestyles. This trend is a key growth driver for the fortified bakery products market in the Middle East and Africa.

Cultural integration of bread and bakery staples

The cultural importance of bread and bakery staples is a key factor driving the growth of the Middle East and Africa bakery products market. Bread serves as a daily dietary essential and plays a significant role in traditional meals, social events, and religious practices, leading to consistent and substantial consumption across the region. This cultural connection encompasses a diverse range of bakery products, such as flatbreads, loaves, pastries, and snack breads, which align with local eating habits and consumer preferences. Bread is often used in various forms, such as a base for meals, an accompaniment to dishes, or as a standalone snack, further emphasizing its versatility and significance. Manufacturers capitalize on this cultural relevance by offering products tailored to regional tastes, textures, and formats, while also innovating with fortified, functional, and convenient options to address changing lifestyle and health needs. Additionally, the growing demand for premium and artisanal bakery products reflects a shift in consumer preferences toward higher-quality and unique offerings, further driving market growth.

Rising consumer awareness of micronutrient deficiencies

Increasing consumer awareness of micronutrient deficiencies is a key factor driving the demand for fortified bakery products in the Middle East and Africa. Nutritional issues, such as Vitamin D deficiency, affecting 49.3% of adults aged 18 and above and 69.1% of children aged 6 to 17 in 2024–2025, underscore the need for dietary solutions to enhance overall health and immunity [3]Source: Emirates News Agency-WAM, "MoHAP releases National Health and Nutrition Survey 2024-2025", wam.ae. Consumers are progressively opting for everyday food products that deliver essential vitamins and minerals, prompting bakery manufacturers to develop fortified breads, biscuits, and other convenience bakery items enriched with micronutrients such as Vitamin D, iron, folate, and calcium. This trend is further supported by public health campaigns, media coverage, and educational initiatives that highlight the role of nutrient intake in preventing deficiencies, improving bone health, and supporting immunity. Consequently, fortified bakery products are increasingly viewed not only as convenient food staples but also as functional options addressing specific nutritional needs, driving market growth and encouraging manufacturers and retailers to expand their health-focused product offerings across the region.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material and premix price volatility | -0.3% | Global, with acute impact on import-dependent Middle East and Africa markets | Short term (≤ 2 years) |

| High product development costs | -0.2% | United Arab Emirates, Saudi Arabia, Turkey, multinational research and develpoment hubs | Medium term (2-4 years) |

| Labeling and regulatory compliance complexity | -0.2% | Saudi Arabia, United Arab Emirates, Gulf Cooperation Council states, Egypt, Nigeria | Medium term (2-4 years) |

| High import dependency for fortification ingredients | -0.1% | Nigeria, Egypt, Morocco, smaller Middle East and Africa economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-material and premix price volatility

Fluctuations in raw material and premix prices present a significant challenge to the growth of the Middle East and Africa bakery products market. Essential inputs such as wheat, flour, sugar, oils, and vitamin- and mineral-based premixes are influenced by global supply variations, currency exchange rate changes, geopolitical tensions, and climate-related disruptions. These price instabilities can lead to higher production costs, reduced profit margins, and increased uncertainty for manufacturers, particularly those producing fortified or functional bakery products that depend on premium-quality premixes. Small and medium-sized bakeries, which often operate with constrained budgets and limited hedging options, are particularly at risk.

Labeling and regulatory compliance complexity

Complex and evolving labeling and regulatory requirements present a significant challenge for the Middle East and Africa bakery products market. Governments in the region have implemented strict regulations for fortified and functional bakery products, addressing areas such as micronutrient content, health claims, allergen disclosure, halal certification, and packaging standards. Compliance with these regulations necessitates investments in dedicated compliance teams, testing procedures, and regular updates to product labels, leading to increased operational costs and delays in bringing new products to market. Furthermore, variations in regulatory frameworks across countries within the region create additional cross-border challenges for companies aiming to expand their products regionally.

Segment Analysis

By Product Type: Bread Anchors, Biscuits Accelerate

Fortified bread accounted for 52.09% of product-type revenue in 2025, driven by its status as a daily staple in Middle Eastern and North African households. Egypt's subsidized baladi bread program, which benefits 60 million citizens, requires iron and folic acid fortification. Similarly, Saudi Arabia's SFDA enforces standards under GSO 2362, ensuring that even unbranded bread meets minimum micronutrient requirements. Fortified biscuits and cookies are projected to grow at a CAGR of 4.36% through 2031, marking the fastest growth among product categories. This growth is attributed to manufacturers focusing on pediatric nutrition with iron-enriched options and convenient, on-the-go formats.

Regulatory frameworks significantly influence product innovation cycles. The Gulf Cooperation Council's GSO 2271 standard for bread improvers and GSO 2394 for bran-enriched bread specify allowable enzyme blends, emulsifiers, and fortificant carriers. These regulations guide research and development efforts at companies like Puratos Group and Corbion, which are developing natural ferments and mold-inhibition solutions to extend shelf life without synthetic preservatives. The combination of mandatory fortification in bread, premiumization in cakes and pastries, and functional innovation in biscuits and bars creates a tiered product hierarchy that addresses both mass-market and aspirational consumer demands.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fortified Micronutrient: Minerals Lead, Protein Surges

Mineral-fortified products, including iron, zinc, and calcium, accounted for 46.10% of the segment's turnover in 2025, reflecting a public health emphasis on addressing anemia and iodine deficiencies. Meanwhile, fiber/protein enriched baked goods are growing at a CAGR of 5.79% through 2030. Agthia’s specialty wheat mixes and dairy premixes enable bakers to achieve 7–9 grams of protein per serving without compromising dough elasticity. The vitamin segment is experiencing commoditization as synthetic B-complex premixes become more affordable. Experimental fortificants, such as omega-3 and probiotics, remain niche due to challenges with thermal stability.

The "Others" category includes omega-3 fatty acids, probiotics, and botanical extracts, which remain experimental in bakery applications due to heat-stability issues during baking. Reis Gıda, a Turkish flour manufacturer, exports gluten-free flours made from red lentil, chickpea, and buckwheat to 26 countries, including the UAE and Saudi Arabia, positioning these as high-protein, high-fiber alternatives to wheat flour.

By Distribution Channel: Supermarkets Dominate, E-Commerce Sprints

Supermarkets/hypermarkets accounted for 44.95% of distribution channel revenue in 2025, benefiting from extensive shelf space, promotional capabilities, and private-label fortified bread and biscuit offerings. Online retail/e-commerce channels are growing at a compound annual growth rate (CAGR) of 6.14% through 2031, representing the fastest expansion among distribution modes. Quick-commerce platforms such as Talabat, Noon, Careem, and Jumia have integrated bakery stock-keeping units (SKUs) into 15-minute delivery windows, transforming impulse purchases into recurring subscriptions.

Convenience stores cater to on-the-go consumption, particularly for fortified biscuits and bars, while specialist and artisanal bakeries target premium segments, with consumers willing to pay approximately 15-20% more for organic or specialty products. "Other Distribution Channels," including institutional sales to schools, hospitals, and corporate cafeterias, benefit from government procurement mandates. For instance, Egypt's subsidized baladi bread program and Nigeria's school feeding initiatives drive consistent demand for fortified loaves and biscuits. The combination of hypermarket scale, e-commerce convenience, and artisanal premiumization creates a multi-channel ecosystem where fortified bakery brands must maintain a presence to engage diverse consumer groups.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Saudi Arabia is projected to dominate the Middle East and Africa bakery products market, contributing 29.58% of regional revenue by 2025, while Turkey is forecasted to record fastest CAGR of 5.88% through 2031. This position is bolstered by robust regulatory frameworks, such as the Saudi Food and Drug Authority’s (SFDA) mandatory iron and folic acid fortification standards for wheat flour (SFDA.FD 2483:2018) and the National Nutrition Strategy 2030, which targets a 25% reduction in anemia prevalence by the end of the decade. These measures have driven demand for fortified bakery products while fostering a structured environment that prioritizes product quality and safety compliance.

Requirements like halal certification under SFDA.FD 05:2022 and Arabic labeling mandates, while increasing compliance costs for manufacturers, serve as barriers to entry, protecting established players and promoting market stability. These regulations ensure that manufacturers adhere to high standards, creating a competitive yet controlled market environment. Additionally, these measures support the long-term sustainability of the bakery products market in Saudi Arabia.

Other countries in the Middle East and Africa are increasingly implementing fortification programs, nutritional policies, and halal certification requirements, contributing to the regional growth of fortified bakery products. Markets with expanding urban populations, higher disposable incomes, and growing health awareness are witnessing increased consumption of breads, biscuits, and snack bakery items enriched with vitamins, minerals, and functional ingredients. However, inconsistent regulatory standards and varying enforcement levels across countries pose challenges for manufacturers aiming to scale fortified bakery products regionally. This highlights the strategic importance of local compliance expertise and the need for market-specific product adaptation.

Competitive Landscape

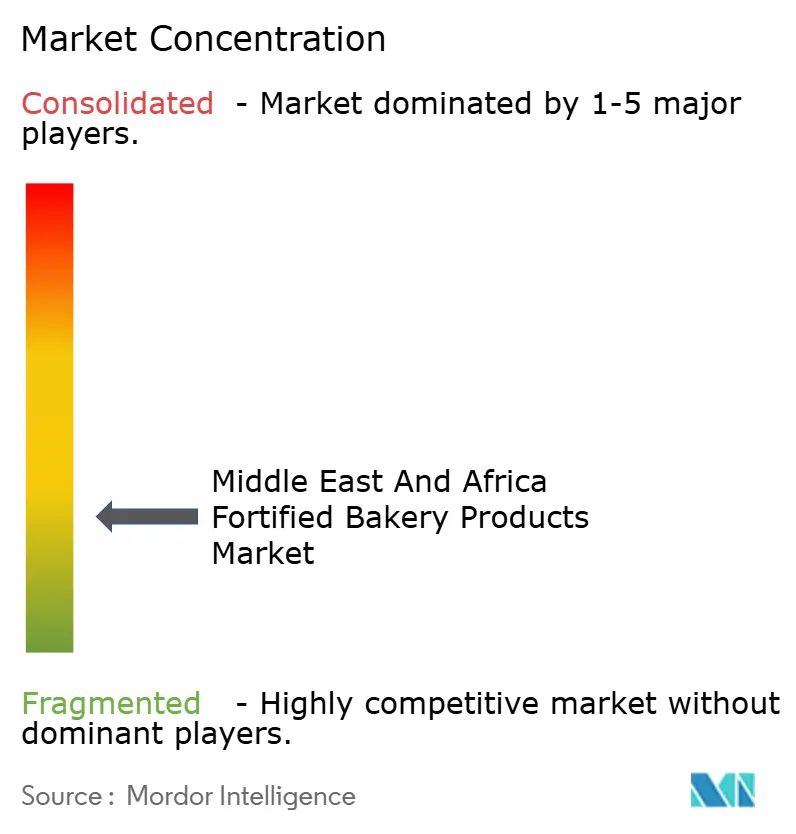

The fortified bakery market in the Middle East and Africa is highly fragmented, with regional players competing alongside multinational companies like Grupo Bimbo, Mondelēz, and Nestlé. Competitive strategies in the market focus on three key areas, adherence to mandatory fortification regulations, exploring opportunities in biofortified flour sourcing, utilizing iron- and zinc-rich crop varieties to reduce dependence on imported premixes, and the adoption of halal-certified enzyme blends to extend shelf life without synthetic preservatives. Ingredient suppliers such as Corbion and Puratos are addressing this need through natural ferments and functional enzyme solutions. These strategies are critical for meeting consumer demand for healthier and longer-lasting bakery products while ensuring compliance with regional standards.

Regulatory frameworks play a significant role in shaping competition within the fortified bakery market. The European Union’s Regulation 1333/2008 on food additives serves as a reference for Gulf Cooperation Council (GCC) states in defining permitted fortificant carriers and enzyme blends. Additionally, GCC standards GSO 2362 and GSO 2394 establish composition limits, creating a regulatory environment that benefits companies with strong in-house compliance capabilities. These regulations not only ensure product safety and quality but also create barriers to entry for smaller players, favoring established companies with the resources to navigate complex compliance requirements. As a result, regulatory expertise has become a key differentiator in the market.

Overall, the fortified bakery market in the Middle East and Africa region is highly dynamic, driven by evolving consumer preferences and regulatory demands. Competitive advantage is determined by scale, expertise in regulatory compliance, speed-to-market, and innovation. Opportunities for growth include natural fortification, enzyme-based shelf-life solutions, and the development of localized functional bakery products. Companies that can effectively balance innovation with compliance and leverage regional consumer insights are well-positioned to capitalize on the growing demand for fortified bakery products in the region.

Middle East And Africa Fortified Bakery Products Industry Leaders

-

Associated British Foods plc

-

Britannia Industries Limited

-

Grupo Bimbo, S.A.B. de C.V.

-

Mondelēz International, Inc.

-

General Mills, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Mondelēz Egypt has inaugurated a Biscuit and Baked Snacks research and development Laboratory at its Biscuits plant in the Tenth of Ramadan (BTOR). This facility represents a significant step in the company’s innovation strategy. It is designed to facilitate the development of new recipes, enhance existing products, and adapt to evolving consumer preferences, while promoting collaboration and experimentation among research and development teams.

- September 2024: Nestlé is establishing its first food manufacturing plant in Saudi Arabia, marking a notable expansion of its local production capabilities. The company has signed an agreement with the Saudi Authority for Industrial Cities and Technology Zones (MODON) to construct the facility on a 117,000-square-meter site in Jeddah’s Third Industrial City. Operations are scheduled to commence in 2025, following an initial investment of SAR 270 million (approximately USD 72 million).

Middle East And Africa Fortified Bakery Products Market Report Scope

Bakery food includes food products such as biscuits, bread, muffins, and cupcakes. A fortified bakery product is bread or other baked goods enriched with vitamins and minerals. This type of product is important because it helps to ensure that people get the nutrients they need, especially those who may not be able to consume a varied diet. The fortified bakery products market is segmented by product type and distribution channel. By type, the market is segmented into cake, biscuits, bread, morning goods, and others. Distribution channel, the market is divided into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into Saudi Arabia, South Africa, and the rest of the Middle East & Africa. It provides an analysis of emerging and established countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Fortified Bread |

| Fortified Biscuits and Cookies |

| Fortified Cakes and Pastries |

| Fortified Morning Goods (Muffins, Croissants) |

| Others (Bars, Wraps, Crackers etc) |

By Fortified Micronutrient

| Vitamins Fortified |

| Minerals Fortified |

| Fibre/Protein Enriched |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialist and Artisanal Bakeries |

| Online Retail / E-commerce |

| Other Distribution Channels |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Fortified Bread |

| Fortified Biscuits and Cookies | |

| Fortified Cakes and Pastries | |

| Fortified Morning Goods (Muffins, Croissants) | |

| Others (Bars, Wraps, Crackers etc) | |

| By Fortified Micronutrient | Vitamins Fortified |

| Minerals Fortified | |

| Fibre/Protein Enriched | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist and Artisanal Bakeries | |

| Online Retail / E-commerce | |

| Other Distribution Channels | |

| By Geography | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the fortified bakery products market in the Middle East and Africa?

The fortified bakery products market size stands at USD 5.68 billion in 2026 with a forecast to reach USD 7.24 billion by 2031.

Which product category holds the largest share?

Fortified bread accounts for 52.09% of 2025 sales thanks to mandatory flour-fortification programs in Egypt and Saudi Arabia.

Which country is the fastest-growing market?

Turkey leads growth at a projected 5.88% CAGR through 2031, supported by high per-capita bread consumption and health-focused shoppers.

How important is online retail for fortified bakery sales?

Online retail is the fastest-expanding channel, advancing at a 6.14% CAGR to 2031 as platforms like Talabat and Noon offer 15-minute delivery.