Market Trends of Middle-East Paints and Coatings Industry

This section covers the major market trends shaping the Middle-East Paints & Coatings Market according to our research experts:

Increasing Demand from the Architectural Sector

- Paints and coatings are extensively used for interior and exterior applications in the architectural sector, domestic houses, and other construction projects. They are applied to the house's exterior to give it a new look and protect it from blistering summers, freezing winters, soaking rain, and daily exposure to UV radiation (without fading, peeling away, and cracking the exterior).

- The strong residential and non-residential construction activities, especially in Saudi Arabia, Qatar, and Kuwait, are expected to boost the consumption of paints and coatings across the region.

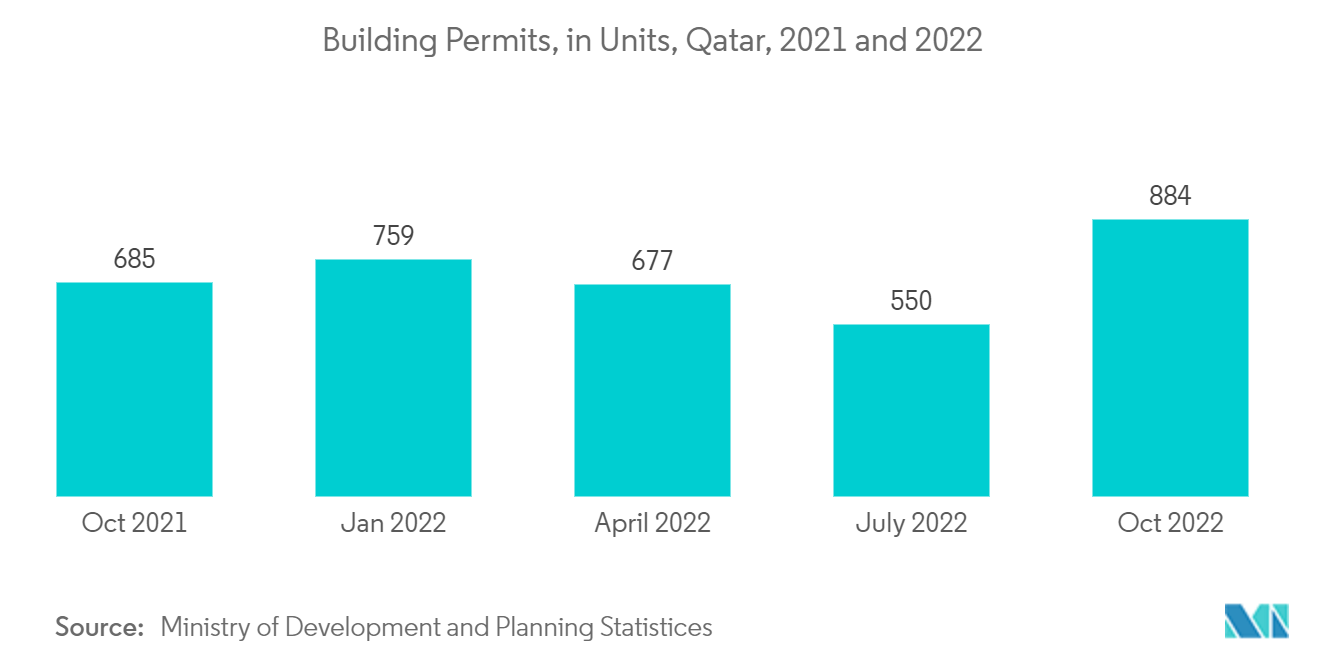

- According to the Planning and Statistics Authority (PSA), 884 building permits were issued in Qatar in September 2022. The new building permits (residential and non-residential) constituted 40% (356 permits) of the total building permits issued in September 2022. Of the new residential building permits, villas topped the list, accounting for 84% of the total, apartments 9%, and dwellings of housing loans 5%.

- Kuwait has some of the world's most beautiful structures, many of which have classical facades. With Kuwait Vision 2035 in mind, the necessity to develop environmentally friendly and sustainable buildings with high-performance and energy-efficient façades is becoming more apparent. There is a strong focus on cutting-edge façades that are structurally, aesthetically, thermally, technologically, and acoustically efficient, secure, and, most importantly, long-lasting.

Understand The Key Trends Shaping This Market

Download PDF

Saudi Arabia to Dominate the Market

- Saudi Arabia is the Middle-East's largest national market, accounting for roughly half of the region's total demand for paints and coatings. According to the International Monetary Fund (IMF), the country has declared a strong reform agenda as part of its Vision 2030, which is likely to result in robust growth over the medium term as structural changes are completed.

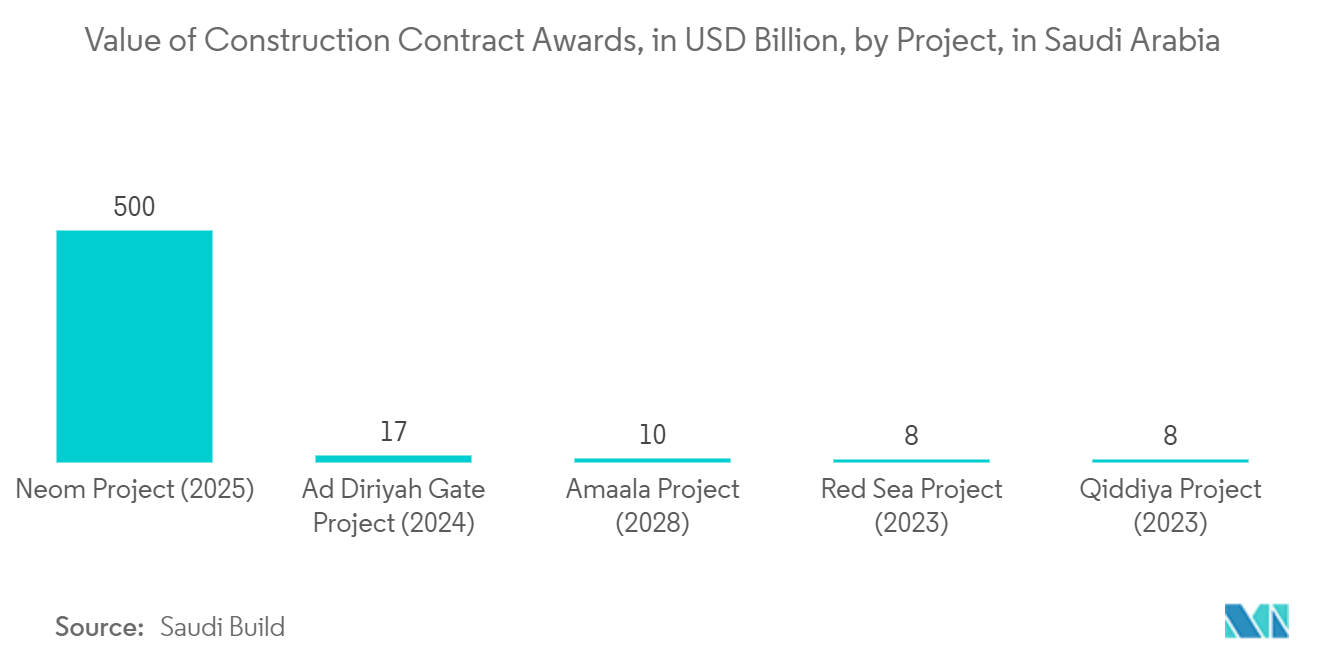

- The Kingdom offers the region's largest pipeline of future construction opportunities, driven by Riyadh's Vision 2030 national development agenda for the diversification and privatization of the giant Saudi economy, which includes a slew of massive megaprojects like the USD 500 billion Neom future cities, Qiddiya entertainment city, and the Red Sea Project.

- According to the Central Department of Statistics and Information, Saudi Arabia's GDP from construction grew to SAR 30,292 million (~USD 8,066.75 million) in the third quarter of 2022, up from SAR 28,544 million (~USD 7601.26 million) in the second quarter of 2022.

- Saudi Arabia motor vehicle sales recorded 556,559 units in Dec 2021, compared with 452,544 units in the previous year. Toyota controls 30% of the Saudi market followed by Hyundai and KIA at 26% and Renault-Nissan-Mitsubishi at 9%.

- According to the Kingdom's vision 2030 goals, the National Industrial Development Center (NIDC) aims to attract 3-4 Original Equipment Manufacturers (OEMs) across the ICE and EV value chain, to produce 300,000 vehicles yearly with a 40% local content by 2030.

Get Analysis on Important Geographic Markets

Download PDF