| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 5.73 Billion |

| Market Size (2030) | USD 7.01 Billion |

| CAGR (2025 - 2030) | 4.12 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle-East Oil and Gas Line Pipe Market Analysis

The Middle-East Oil And Gas Line Pipe Market size is estimated at USD 5.73 billion in 2025, and is expected to reach USD 7.01 billion by 2030, at a CAGR of 4.12% during the forecast period (2025-2030).

The Middle East line pipe industry continues to evolve amid significant pipeline infrastructure developments and technological advancements. The region's commitment to modernizing its oil and gas pipeline infrastructure is evident through major pipeline projects, with companies like TMK supplying over 5,000 tons of seamless steel pipes to the Sharjah National Oil Corporation (SNOC) in March 2021 for transporting high-sulfide content gas. This trend toward specialized pipeline system solutions reflects the industry's adaptation to increasingly complex extraction and transportation requirements. The integration of advanced materials and coating technologies has become paramount, particularly in addressing the challenges posed by corrosive substances and extreme environmental conditions.

Water infrastructure development has emerged as a crucial growth catalyst for the line pipe industry, with governments across the region implementing ambitious expansion plans. In January 2021, Saudi Arabia announced a substantial USD 16 billion investment in water transmission pipeline expansion projects, aiming to add approximately 3,500 kilometers of new transmission lines. The UAE has similarly demonstrated its commitment to water infrastructure development, with ADNOC announcing in March 2021 its participation in a large-scale seawater treatment and transmission pipeline project requiring approximately 450 kilometers of new pipeline infrastructure. These developments underscore the diversification of line pipe applications beyond traditional oil and gas sectors.

The industry is witnessing a significant shift toward sustainable and efficient pipeline solutions, particularly in water desalination and distribution networks. Major national initiatives, such as Kuwait's freshwater pipeline project connecting Mina Abdullah Distribution Complex to West Funaitees Complex, exemplify the region's focus on developing comprehensive water transmission systems. The implementation of advanced pipeline technologies, including sophisticated coating systems and monitoring capabilities, has become increasingly prevalent in ensuring long-term infrastructure reliability and operational efficiency.

The market is experiencing notable technological advancement in pipeline manufacturing and installation processes. Companies are increasingly adopting automated welding systems, advanced inspection technologies, and innovative materials to enhance pipeline performance and longevity. This evolution is particularly evident in projects like Perma-Pipe Egypt's recent USD 6.0 million contracts for thermally insulated pipe systems, incorporating sophisticated leak detection systems and anti-corrosion polyamide epoxy coatings. These technological improvements are reshaping industry standards and contributing to the development of more resilient and efficient pipeline infrastructure networks across the region.

Middle-East Oil and Gas Line Pipe Market Trends

Growing Natural Gas Infrastructure Development

The Middle East region is witnessing substantial growth in natural gas pipeline infrastructure development driven by increasing industrial demand from refining, petrochemical, specialty chemical, and fertilizer industries. The expansion of gas infrastructure is primarily motivated by countries' plans to increase gas exports and encourage domestic market usage. Major national oil companies are making significant investments in pipeline equipment expansion projects to support this growth. For instance, in September 2022, the Abu Dhabi National Oil Company (ADNOC) awarded a USD 548 million contract to the National Petroleum Construction Company (NPCC) for constructing a new natural gas pipeline at its Lower Zakum field offshore Abu Dhabi, demonstrating the region's commitment to expanding gas infrastructure.

The development of gas processing facilities and transportation networks continues to drive demand for line pipes across the region. A notable example is Saudi Arabia's Master Gas III project, for which Aramco issued a significant tender in November 2022 for 1.6 million metric tons of 56-inch non-sour surface pipelines. These pipelines will facilitate gas transportation from eastern to western Saudi Arabia, highlighting the scale of infrastructure development taking place. Additionally, the increasing focus on unconventional gas resources, particularly in Saudi Arabia, which holds the world's fifth-largest estimated shale gas reserves, is creating new demands for specialized process pipeline infrastructure designed to handle the unique characteristics of shale gas transportation.

Understand The Key Trends Shaping This Market

Download PDF

Expansion of Oil Production and Transportation Infrastructure

The Middle East continues to maintain its position as a global leader in oil production, with the region producing 1,315.8 million tons of crude oil in 2021, accounting for 31.2% of global production. This substantial production capacity necessitates continuous development and maintenance of transportation pipeline infrastructure to support transportation and processing operations. Saudi Arabia, as the world's second-largest crude oil producer with 10.95 million barrels per day in 2021, leads the regional demand for oil transportation pipeline infrastructure, driving significant investments in pipeline networks.

The expansion of refining and petrochemical capabilities across the region is creating additional demand for line pipes. Major projects such as Saudi Aramco and SABIC's joint oil-to-chemicals facility, designed to process 20 million tons of crude oil annually, exemplify the scale of infrastructure development underway. These projects require extensive petroleum pipeline networks for transporting raw materials and finished products, contributing to sustained demand for line pipes. Furthermore, the modernization and expansion of existing facilities, including upgrades at refineries like SASREF, Petro Rabigh, and Jubail, as well as the development of new facilities like the Jizan refinery, are creating additional requirements for pipeline equipment infrastructure.

Rising Water Infrastructure Development

The Middle East's status as one of the most water-scarce regions globally has prompted significant investments in water infrastructure development, particularly in desalination plants and water transmission systems. Countries across the region are implementing ambitious water security strategies, driving substantial demand for line pipes in water transportation networks. The UAE Water Security Strategy 2036 and Saudi Arabia's National Water Strategy 2030 are prime examples of comprehensive frameworks driving infrastructure development, with multiple projects requiring extensive pipeline networks for water transmission and distribution.

Major water infrastructure projects are being implemented across the region, creating sustained demand for line pipes. For instance, Abu Dhabi National Energy Company's subsidiary awarded projects worth AED 900 million for expanding its recycled water distribution program, which includes laying approximately 150 kilometers of pipelines. Similarly, ADNOC's large-scale seawater treatment and transportation project requires roughly 450 kilometers of new pipeline infrastructure, demonstrating the scale of water infrastructure development in the region. These initiatives, coupled with similar projects across other Middle Eastern countries, are creating significant opportunities for line pipe manufacturers and suppliers.

Segment Analysis: Type

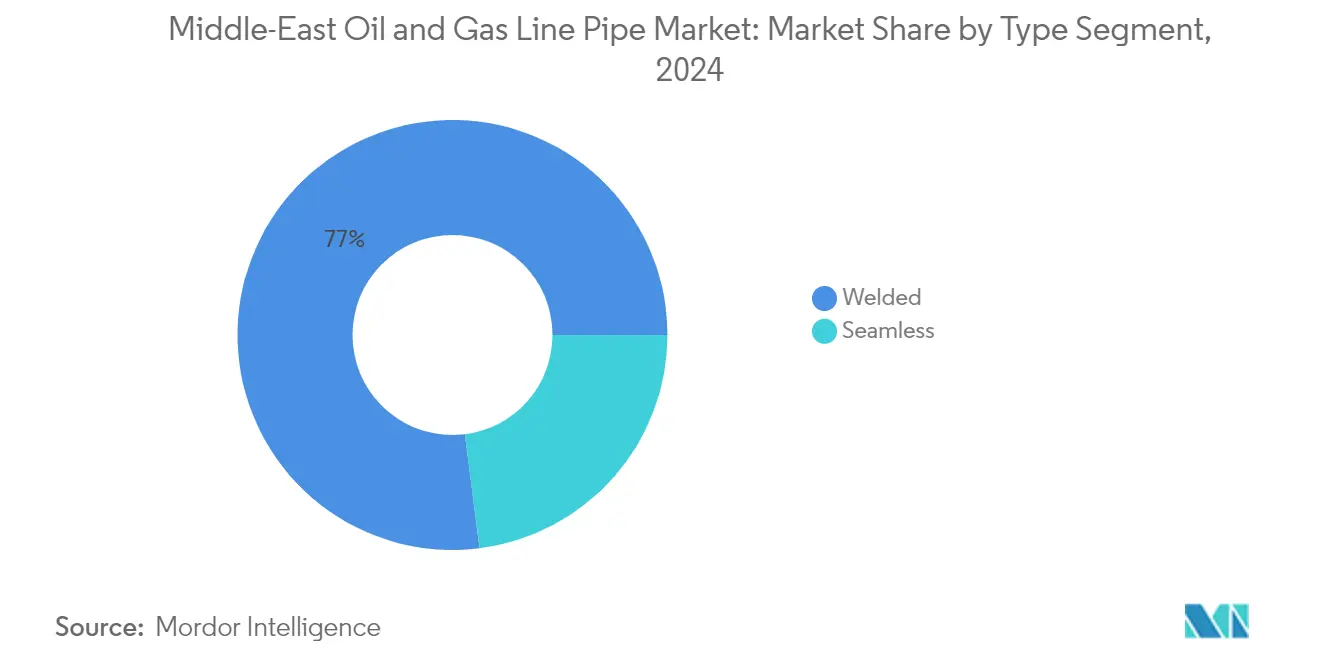

Welded Segment in Middle-East Oil and Gas Line Pipe Market

The welded pipe segment dominates the Middle-East oil and gas line pipe market, commanding approximately 77% of the total market share in 2024. This significant market position is attributed to welded pipes' widespread use in various applications, including gas lines, oil transportation, and water transmission systems. The segment encompasses three main types: Longitudinal Submerged Arc Welded (LSAW), Helical Submerged Arc Welded (HSAW), and Electric Resistance Welded (ERW) pipes, with LSAW holding the major share within the welded segment. These pipes are particularly preferred for their cost-effectiveness, large diameter availability, and suitability for high-pressure applications in refineries, desalination plants, water treatment facilities, LNG terminals, and petrochemical industries across the Middle East region. The welded segment's versatility in pipeline systems and industrial pipe applications further solidifies its market leadership.

Seamless Segment in Middle-East Oil and Gas Line Pipe Market

The seamless pipe segment is experiencing robust growth in the Middle-East oil and gas line pipe market during the forecast period 2024-2029. This growth is driven by seamless pipes' superior properties, including higher pressure resistance, uniform shape, and greater strength under load conditions. These pipes are particularly valued in high-pressure applications within the oil and gas midstream sector, refineries, and chemical industry. The increasing demand for corrosion-resistant pipes in water and oil and gas industries, where transported fluids are highly corrosive, is further accelerating the segment's growth. Major companies like TMK, ArcelorMittal Jubail, Jindal SAW Limited, and Vallourec SA are actively contributing to the segment's expansion through continuous product development and strategic investments in the region. The seamless segment's role in steel line pipe manufacturing is pivotal to meeting the region's growing demand.

Segment Analysis: Sector

Oil & Gas Segment in Middle-East Oil and Gas Line Pipe Market

The Oil & Gas segment dominates the Middle-East oil and gas line pipe market, accounting for approximately 74% of the total market share in 2024. This significant market share is driven by extensive pipeline system infrastructure requirements for transporting crude oil, natural gas, and petroleum products across the region. The segment's dominance is reinforced by major ongoing projects like the West Pipeline Expansion Project in Saudi Arabia and the Sharjah NOC pipeline project in the UAE. Additionally, the development of gas infrastructure and increasing investments in new oil and gas exploration activities, particularly in countries like Saudi Arabia, the UAE, and Qatar, continue to fuel the demand for line pipes in this segment. The segment's growth is further supported by the region's position as a global hub for oil and gas production, with countries making substantial investments in modernizing and expanding their upstream pipeline networks to enhance distribution capabilities.

Water Segment in Middle-East Oil and Gas Line Pipe Market

The Water segment in the Middle-East oil and gas line pipe market is experiencing steady growth, driven by increasing investments in water infrastructure projects across the region. This growth is primarily attributed to the rising number of desalination plants and water transmission projects, particularly in Saudi Arabia and the UAE. The segment's expansion is supported by major initiatives such as Saudi Arabia's "Saudi National Water Strategy 2030" and the UAE Water Security Strategy 2036, which focus on developing robust water infrastructure networks. Furthermore, significant projects like the ADNOC seawater treatment and transmission pipeline project in Abu Dhabi, requiring approximately 450 kilometers of new pipeline infrastructure, demonstrate the segment's growth potential. The increasing focus on water security and sustainable water management solutions continues to drive demand for line pipes in water transmission and distribution systems across the Middle East region. The use of pipeline components and process pipeline solutions is critical in ensuring the efficiency and reliability of these systems.

Middle-East Oil And Gas Line Pipe Market Geography Segment Analysis

Middle-East Oil and Gas Line Pipe Market in Rest of Middle East

The Rest of Middle East region dominates the Middle East oil and gas pipeline market, commanding approximately 49% of the total market value in 2024. The region's prominence is largely attributed to the presence of major oil and gas-producing nations with extensive pipeline infrastructure requirements. Countries in this region have been actively expanding their midstream infrastructure to support growing hydrocarbon production and transportation needs. The development of new gas fields and the expansion of existing facilities have created substantial demand for transmission pipeline and distribution pipeline systems. The region's focus on diversifying energy sources and modernizing existing pipeline networks has further strengthened market growth. Additionally, significant investments in water infrastructure projects, particularly in desalination plants and water transmission systems, have created parallel demand streams for line pipes.

Middle-East Oil and Gas Line Pipe Market in Saudi Arabia

Saudi Arabia represents a crucial market for oil and gas pipeline infrastructure, driven by its position as the world's second-largest crude oil producer and its extensive pipeline infrastructure. The kingdom's ongoing efforts to diversify its economy beyond oil, as outlined in its economic reform plans, continue to generate substantial demand for pipeline infrastructure. The country's upstream sector maintains robust activity levels, with Saudi Aramco operating over 90 pipelines spanning more than 12,000 miles. The nation's focus on developing its unconventional gas reserves, particularly its shale gas potential, has created additional demand for specialized gathering pipeline systems. The water sector also contributes significantly to line pipe demand, with major desalination projects and water transmission systems under development. The country's strategic location and well-established manufacturing base have attracted numerous international line pipe manufacturers to establish local production facilities.

Middle-East Oil and Gas Line Pipe Market in UAE

The United Arab Emirates maintains a strong position in the Middle East line pipe market, supported by its ambitious energy infrastructure development plans and growing focus on gas self-sufficiency. The country's strategic initiatives in expanding its oil and gas infrastructure, particularly in Abu Dhabi, have created sustained demand for distribution pipeline systems. The UAE's commitment to developing its gas infrastructure, including the construction of new processing facilities and pipeline networks, has been a key market driver. The nation's focus on water security, evidenced by significant investments in desalination plants and water transmission networks, has created additional demand streams. The presence of major line pipe manufacturers and the country's position as a regional trading hub have further strengthened its market position. The UAE's emphasis on quality standards and sustainable infrastructure development has influenced the types of line pipes being procured, with a growing preference for corrosion-resistant and high-performance materials.

Middle-East Oil and Gas Line Pipe Market in Qatar

Qatar's line pipe market demonstrates robust growth potential, with an expected CAGR of approximately 4% from 2024 to 2029. The country's position as the world's third-largest natural gas reserve holder and largest LNG supplier creates substantial demand for hydrocarbon pipeline infrastructure. Qatar's extensive gas transmission and distribution network, comprising approximately 3,000 km of interconnected pipelines, continues to expand with new projects. The country's ambitious plans to increase its LNG production capacity have necessitated significant investments in pipeline infrastructure. Qatar's water sector development, including the expansion of desalination facilities and water transmission networks, provides additional market opportunities. The country's strong focus on infrastructure development, backed by substantial financial resources, ensures sustained demand for line pipes across various applications.

Middle-East Oil and Gas Line Pipe Market in Other Countries

Other countries in the Middle East region, including Oman, Kuwait, Bahrain, and Iraq, collectively contribute significantly to the regional line pipe market. These nations are actively developing their oil and gas infrastructure, with numerous pipeline projects in various stages of implementation. The focus on diversifying energy sources and modernizing existing infrastructure drives demand across these markets. Water infrastructure development, particularly in addressing water scarcity through desalination projects, creates additional demand for line pipes. Each country's unique energy and infrastructure development priorities shape their specific requirements for line pipe specifications and applications. The presence of both established and emerging players in these markets ensures competitive pricing and technological advancement in line pipe solutions.

Get Analysis on Important Geographic Markets

Download PDF

Middle-East Oil and Gas Line Pipe Industry Overview

Top Companies in Middle-East Oil and Gas Line Pipe Market

The Middle East oil and gas line pipe market features prominent players like Arabian Pipes Company, Nippon Steel Corporation, Vallourec SA, SeAH Steel, TMK, Tenaris SA, Welspun Corp Ltd, and ArcelorMittal. These companies demonstrate strong product innovation capabilities, particularly in developing specialized coatings and high-pressure resistant pipes for extreme conditions. Operational agility is evidenced through strategic manufacturing facility placements near major oil and gas hubs, enabling quick responses to market demands. Companies are increasingly focusing on vertical integration to control costs and improve supply chain efficiency. Strategic moves include expanding local manufacturing presence through joint ventures and partnerships with regional players. The market also sees continuous investment in R&D for developing environmentally sustainable products and advanced manufacturing processes to meet evolving industry standards.

Dynamic Market with Strong Regional Players

The Middle East line pipe market exhibits a mix of global conglomerates and specialized regional manufacturers, with both types of players maintaining significant market presence. Global players like ArcelorMittal and Nippon Steel leverage their technological expertise and worldwide operations to serve the market, while regional players such as Arabian Pipes Company and Al Gharbia Pipe Company maintain competitive advantages through local market knowledge and established relationships with major oil and gas companies. The market shows moderate consolidation, with larger players continuously seeking to strengthen their positions through strategic acquisitions and joint ventures.

Recent market developments indicate a trend toward increased localization of manufacturing capabilities, with international players establishing production facilities in key Middle Eastern countries. Merger and acquisition activities focus on vertical integration and capability enhancement, particularly in specialized pipeline equipment manufacturing and coating technologies. Companies are also forming strategic alliances to combine complementary strengths, such as manufacturing expertise with local market access, creating more robust competitive positions in the market.

Innovation and Adaptability Drive Future Success

Success in the Middle East line pipe market increasingly depends on companies' ability to adapt to changing industry requirements and maintain technological leadership. Market players must focus on developing specialized products for emerging applications like shale gas transportation and high-pressure deep-water pipelines. The high concentration of major oil and gas companies in the region necessitates strong relationship management capabilities and the ability to meet stringent quality standards. Companies must also address the growing threat from substitute materials like PVC and fiberglass pipes, particularly in water transportation applications.

Future market success will require companies to maintain robust financial positions to support continuous investment in technology and capacity expansion. Local manufacturing presence is becoming increasingly crucial as regional governments implement policies favoring domestic production. Companies must also focus on developing environmentally sustainable products and processes to align with growing environmental concerns in the region. The ability to offer comprehensive solutions, including installation and maintenance services, will become increasingly important as customers seek integrated service providers rather than pure product suppliers. This includes the development of advanced pipeline infrastructure and pipeline systems to ensure seamless operations.

Middle-East Oil and Gas Line Pipe Market Leaders

-

Arabian Pipes Company

-

EEW Group

-

Rezayat Group

-

Vallourec S.A.

-

Sumitomo Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Middle-East Oil and Gas Line Pipe Market News

- August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023.

- March 2023: Gas Arabian Services Company has been granted a USD 13.58 million engineering, procurement, and construction (EPC) contract for a gas pipeline by Advanced Petrochemical Company (Advanced). The pipeline will connect Advanced's Propane Dehydrogenation (PDH) unit to Jubail United's cracking unit for upgrading the by-product gas stream to high-value chemicals.

Middle-East Oil and Gas Line Pipe Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Seamless

- 5.1.2 Welded

-

5.2 Geography

- 5.2.1 United Arab Emirates

- 5.2.2 Saudi Arabia

- 5.2.3 Rest of Middle East

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Arabian Pipes Company

- 6.3.2 Rezayat Group

- 6.3.3 EEW Group

- 6.3.4 Sumitomo Corporation

- 6.3.5 Vallourec SA

- 6.3.6 Abu Dhabi Metal Pipes & Profiles Industries Complex LLC

- 6.3.7 Jindal SAW Ltd

- 6.3.8 ArcelorMittal SA

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Middle-East Oil and Gas Line Pipe Industry Segmentation

Line pipe is a form of steel pipe that is used to move goods across the country via pipelines. Petroleum, natural gas, oil, and water can all be transported via line pipes. Line pipes are connected together to form a pipeline.

The market is segmented by type and geography. By type, the market is segmented into seamless and welded. The report also covers the market size and forecasts for the Middle-East Oil and Gas Line Pipe Market across the major countries in the region. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

| Type | Seamless |

| Welded | |

| Geography | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East |

Need A Different Region or Segment?

Customize Now

Middle-East Oil and Gas Line Pipe Market Research FAQs

How big is the Middle-East Oil And Gas Line Pipe Market?

The Middle-East Oil And Gas Line Pipe Market size is expected to reach USD 5.73 billion in 2025 and grow at a CAGR of 4.12% to reach USD 7.01 billion by 2030.

What is the current Middle-East Oil And Gas Line Pipe Market size?

In 2025, the Middle-East Oil And Gas Line Pipe Market size is expected to reach USD 5.73 billion.

Who are the key players in Middle-East Oil And Gas Line Pipe Market?

Arabian Pipes Company, EEW Group, Rezayat Group, Vallourec S.A. and Sumitomo Corporation are the major companies operating in the Middle-East Oil And Gas Line Pipe Market.

What years does this Middle-East Oil And Gas Line Pipe Market cover, and what was the market size in 2024?

In 2024, the Middle-East Oil And Gas Line Pipe Market size was estimated at USD 5.49 billion. The report covers the Middle-East Oil And Gas Line Pipe Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Middle-East Oil And Gas Line Pipe Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Middle-East Oil And Gas Line Pipe Market Research

Mordor Intelligence provides a comprehensive analysis of the oil and gas pipeline industry. With decades of expertise in energy pipeline research, our study covers the entire spectrum of pipeline infrastructure. This includes upstream pipeline operations, as well as midstream pipeline and downstream pipeline segments. The report, available as an easy-to-download PDF, offers detailed insights into natural gas pipeline networks, petroleum pipeline systems, and transportation pipeline developments across the Middle East region.

Our analysis benefits stakeholders throughout the pipeline system value chain. It offers a detailed examination of pipeline components and pipeline equipment. The report thoroughly investigates transmission pipeline networks, distribution pipeline systems, and gathering pipeline operations. It also addresses industrial pipeline applications. Stakeholders gain valuable insights into process pipeline developments, hydrocarbon pipeline innovations, and advances in steel line pipe technology. The comprehensive coverage includes an in-depth analysis of industrial pipe specifications and pipeline infrastructure developments. This ensures decision-makers have access to the most relevant market intelligence.