Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

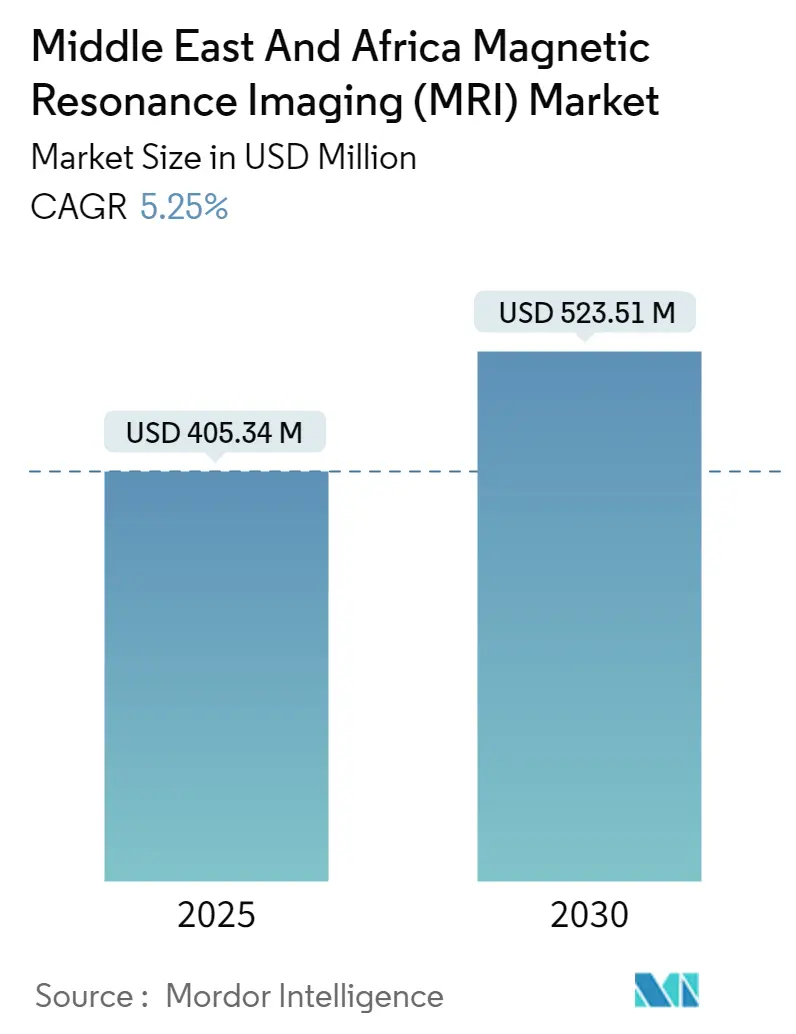

| Market Size (2025) | USD 405.34 Million |

| Market Size (2030) | USD 523.51 Million |

| Growth Rate (2025 - 2030) | 5.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

The Middle East and Africa MRI market size reached USD 405.34 million in 2025 and is projected to expand to USD 523.51 million by 2030, reflecting a 5.25% CAGR. Rising chronic-disease incidence, government-funded screening mandates, and a pivot toward precision diagnostics anchor the growth trajectory. Large sovereign wealth funds in Saudi Arabia, the UAE, and Qatar are deploying multi-billion-dollar capital programs that bundle high-field scanners with AI-ready digital platforms, while portable low-field solutions widen access in resource-constrained settings. Vendor competition has shifted from raw magnet performance to workflow automation, helium-saving sustainability, and service contracting flexibility. Hospitals remain the primary buyers, yet independent imaging centers are expanding faster as systems decentralize care delivery and pursue higher scanner utilization efficiency.

Key Report Takeaways

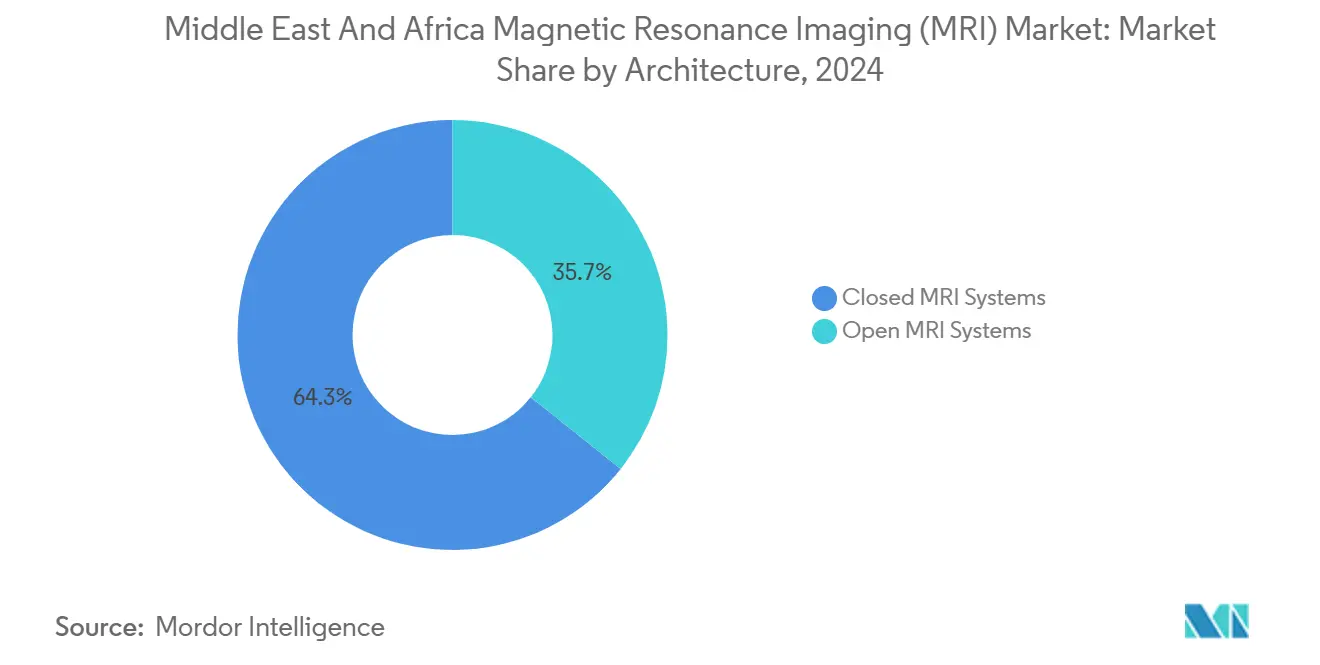

- By architecture, closed systems led with 64.35% revenue share in 2024, while open units are forecast to advance at 5.82% CAGR through 2030.

- By field strength, high-field 1.5 T platforms captured 54.70% share of the Middle East and Africa MRI market size in 2024, whereas very-high 3 T and ultra-high ≥7 T installations are poised for 5.86% CAGR growth to 2030.

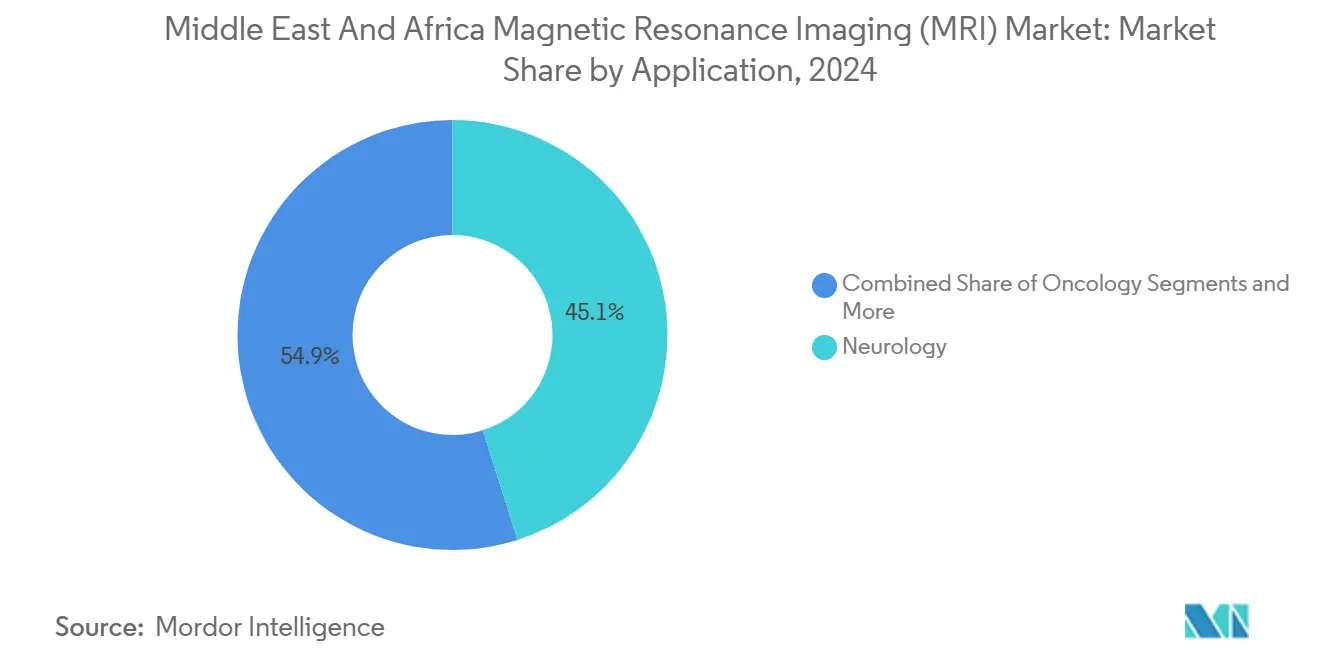

- By application, neurology retained 45.14% share in 2024; oncology is set to accelerate at 6.17% CAGR to 2030.

- By end user, hospitals accounted for 48.17% of 2024 revenue, yet diagnostic imaging centers are expanding at 6.23% CAGR through 2030.

- By geography, GCC economies commanded 48.24% of 2024 spending, while South Africa is projected to post a 6.31% CAGR through 2030.

Middle East And Africa Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Chronic-Disease & Ageing Burden | +1.2% | Global, with concentration in GCC and South Africa | Long term (≥ 4 years) |

| National Insurance Reforms And Cancer/Cardiac Screening Programmes In Saudi Arabia, UAE And South Africa | +0.9% | GCC core, South Africa | Medium term (2-4 years) |

| Expansion Of Public-Sector Healthcare Projects | +0.8% | GCC, Egypt, Nigeria | Medium term (2-4 years) |

| AI-Enhanced 3T Imaging & Workflow Automation | +0.7% | GCC, South Africa, urban centers across MEA | Short term (≤ 2 years) |

| Rise Of Portable Low-Field POC MRI Units | +0.6% | Sub-Saharan Africa, rural MEA regions | Medium term (2-4 years) |

| Gulf Sovereign-Fund PPP Diagnostic Clusters | + 0.5% | GCC countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Chronic-Disease & Aging Burden

Chronic illnesses such as diabetes, cardiovascular disease, and prostate cancer continue to climb, driving demand for stroke, cardiac, and whole-body MRI protocols across the Middle East and Africa MRI market. GCC governments finance prevention campaigns that make advanced imaging a front-line tool for population health management. Egypt’s universal insurance expansion alone targets 12.8 million new beneficiaries by 2030, guaranteeing reimbursement for medically necessary scans. MRI vendors benefit from predictable throughput and the associated service revenue tied to long-term disease monitoring.

National Insurance Reforms and Screening Programs

Mandatory screening frameworks in Saudi Arabia, the UAE, and South Africa embed MRI volumes directly into reimbursement schedules, stabilizing cash flow for providers and creating scale economies for equipment suppliers. Cloud-based health-information exchanges unify scheduling, reporting, and archival, ensuring that scanners reach higher utilization thresholds. Volume-based reimbursement negotiations tighten per-scan margins yet reward manufacturers that market uptime-focused service contracts and AI engines that shorten acquisition times.

AI-Enhanced 3 T Imaging & Workflow Automation

AI reconstruction and triage engines reduce scan times by up to 80% and sharpen image quality by 80%, enabling 24/7 operations even where radiologist density is below one per million population [1]Philips, “Philips collaborates with NVIDIA to improve patient care in MR with latest AI advances,” PHILIPS.COM . Vendors emphasize subscription-style software licensing and cloud inference to bring premium performance to mid-tier hospitals without costly on-prem servers.

Rise of Portable Low-Field POC MRI Units

Point-of-care 0.05 T scanners eliminate the need for specialized shielding, plug into standard wall power, and travel to rural clinics. Clinical studies confirm their utility in emergent neuroimaging. Distribution agreements in Turkey, Israel, and Saudi Arabia accelerate reach, and humanitarian deployments in Malawi validate resilience in low-resource environments [2]AJNR, “Implementation of a Low-Field Portable MRI Scanner in a Resource-Constrained Environment,” AJNR.ORG .

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition & Lifecycle Cost | -1.1% | Global, particularly Sub-Saharan Africa | Long term (≥ 4 years) |

| Radiologist / Technologist Shortage | -0.8% | Sub-Saharan Africa, rural MEA regions | Medium term (2-4 years) |

| Power-Grid & Cooling-Water Instability | -0.6% | Sub-Saharan Africa, rural and semi-urban MEA | Medium term (2-4 years) |

| Limited Reimbursement For Advanced Sequences | -0.4% | Global MEA, with acute impact in low-income countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Lifecycle Cost

Conventional 1.5 T installations range from USD 1-3 million plus 8-12% annual maintenance, stretching limited capital in low-income economies. Cooling, shielding, and helium demands add 30-50% to project budgets, forcing many hospitals to opt for refurbished systems or vendor-financed leasing that extends payback horizons. Helium-free magnet designs now reduce running expenses, but sticker prices remain a hurdle until bulk-purchase consortia mature.

Radiologist / Technologist Shortage

Radiologist density across several Sub-Saharan states is below 1 per million inhabitants, limiting MRI throughput despite rising scanner counts. AI-guided acquisition and teleradiology alleviate bottlenecks, but inconsistent broadband and regulatory silos delay full adoption. Workforce migration to higher-income nations sustains the deficit, underscoring the value of automation, remote supervision, and accelerated upskilling programs.

Segment Analysis

By Architecture: Closed Systems Dominate Yet Open Designs Gain Momentum

Closed scanners generated 64.35% of 2024 revenue in the Middle East and Africa MRI market. High signal-to-noise ratio and compatibility with advanced neurological protocols sustain their primacy. Hospitals favor these systems for stroke and oncology pathways that require sub-millimeter resolution. Open designs, meanwhile, are advancing at 5.82% CAGR as claustrophobia-sensitive patient groups and interventional teams demand lateral access and comfort.

Fujifilm’s 0.4 T platform couples wide bores with motion-compensated RADAR sequences, narrowing the image-quality gap to closed units and satisfying ISO 13485 compliance. Independent imaging centers leverage lower purchase prices and faster room turnover to reach breakeven sooner, pushing additional closed-to-open mix shifts in outpatient settings.

By Field Strength: High-Field Leadership Meets Ultra-High Expansion

High-field 1.5 T systems accounted for 54.70% of 2024 scanner installations because they balance diagnostic versatility with manageable siting requirements. The Middle East and Africa MRI market share for ultra-high 3 T and ≥7 T units is rising quickly as research hospitals and cancer centers seek superior tissue contrast. Virtually helium-free 1.5 T and 3 T magnets from Philips have already conserved 5 million L of helium worldwide.

Canon Medical’s 3 T Supreme Edition integrates deep-learning reconstruction to shorten protocols and minimize operator steps. Portable low-field models below 1.5 T cater to emergency neurology and neonatal wards that lack the infrastructure for superconducting magnets. Collectively, these tiers expand the accessible customer base without cannibalizing core high-field demand.

By Application: Neurology Remains Core as Oncology Overtakes Growth

Neurology delivered 45.14% of 2024 revenue, anchored in stroke detection protocols and diabetes-linked neuropathies prevalent across GCC states. Rapid-access brain MRI pathways reduce door-to-needle time for thrombolysis and drive scanner placement in emergency departments. Oncology scans, however, will post the fastest CAGR at 6.17% through 2030 as Saudi and Emirati screening programs extend coverage to breast, prostate, and colorectal cancers.

Cardiology uptake accelerates with 4D flow imaging that maps intracardiac hemodynamics. Musculoskeletal and gastroenterology sub-segments benefit from sports-medicine growth and fatty-liver monitoring, respectively. Across modalities, AI-enabled post-processing standardizes reporting and reduces turnaround, strengthening clinician confidence and payer reimbursement alignment.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Anchors with Clinic-Driven Outperformance

Hospitals contributed 48.17% of 2024 scanner revenue thanks to multi-disciplinary service lines and 24/7 emergency imaging. Their capital budgets absorb high-field purchases and advanced coils. Yet independent imaging centers and specialist clinics will expand fastest at 6.23% CAGR as health systems decentralize. Dedicated MRI sites achieve higher utilization and patient convenience, attracting private insurance referrals.

Burjeel Holdings illustrates the hybrid model: its 19 hospitals integrate acute care imaging, while 97 satellite clinics handle scheduled scans, boosting fleet productivity. Mobile services employing low-field units further broaden outreach to rural communities, aligning with national equity objectives.

Geography Analysis

GCC nations accounted for 48.24% of 2024 spending as sovereign wealth funds financed AI-ready diagnostic clusters linked to Vision 2030 roadmaps. Saudi Arabia’s plan to privatize 290 hospitals pushes private participation from 25% to 35%, yet universal coverage guarantees scan volumes and smooth cash flows. The UAE, investing more than USD 7.9 billion in digital platforms, deploys region-wide image-exchange networks that lift scanner utilization and inform risk-stratified screening. Qatar’s preparation for population expansion and medical-tourism inflows sustains high-field demand, while harmonized registration rules expedite foreign OEM launches.

South Africa represents the fastest growing sub-market with a 6.31% CAGR projected through 2030. Universal Health Insurance shifts 15% of citizens from private to public cover, forecasting larger pooled procurements that favor vendors offering helium-free life-cycle savings. The new Artificial Intelligence Institute of South Africa accelerates research partnerships that rely on 3 T functional imaging. SAHPRA’s regulatory rigor obliges clinical-quality sourcing, benefiting premium manufacturers.

The rest of Middle East and Africa presents a heterogeneous outlook. Egypt’s medical-city projects and universal insurance rollout demand mid-range 1.5 T systems, yet currency swings and power-grid instability force flexible financing. Nigeria’s USD 5 billion initiative to unlock diagnostic value chains promises volume but contends with logistics complexity. Morocco, where 30% of hospitals use AI-assisted diagnosis, showcases the region’s innovation potential, driving interest in cloud-connected scanners that sidestep local compute shortages.

Competitive Landscape

The Middle East and Africa MRI market favors global conglomerates that couple magnet engineering with AI ecosystems. Siemens Healthineers is investing USD 314 million in new manufacturing capacity while rolling out helium-light MAGNETOM Flow models, emphasizing lower operating costs. GE HealthCare reinforces platform stickiness via smart-technology collaborations with major imaging chains and the acquisition of advanced visualization firm MIM Software [3]GE HealthCare, “GE HealthCare announces agreement to acquire MIM Software,” INVESTOR.GEHEALTHCARE.COM . Philips differentiates through BlueSeal sealed magnets and cloud-hosted AI reconstruction, citing 40 MWh annual energy savings per 1.5 T unit.

Challenger brands such as Hyperfine and United Imaging target white-space opportunities. Hyperfine’s portable platform signed new distributors across Turkey, Israel, and Saudi Arabia to capture emergency-room and rural demand. United Imaging’s 5 T head-only scanner, cleared by the FDA, appeals to neuroscientific centers seeking ultra-high resolution without complete MRI suite renovation.

Sustainability and total cost of ownership trump raw Gauss races. Hospital groups now benchmark energy draw, helium consumption, uptime, and AI-workflow additions when scoring tenders. Vendors that bundle scanner, service, and software in outcome-linked contracts gain the inside track, especially where sovereign-fund buyers seek 10-year life-cycle guarantees that align with national health-care masterplans.

Middle East And Africa Magnetic Resonance Imaging (MRI) Industry Leaders

-

Canon Medical Systems Corporation

-

Koninklijke Philips N.V

-

General Electric Company (GE Healthcare)

-

Siemens Healthineers

-

FUJIFILM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Prime Minister Mostafa Madbouly inspected the first factory in Africa and the Middle East for ultrasound and MRI production in Egypt’s 6th of October City.

- September 2023: Philips and Burjeel Hospital launched a diagnostic-imaging Center of Excellence in Dubai, coupled with an MRI technologist development program.

- February 2023: GE HealthCare agreed to supply precision-diagnostic equipment, including MRI, to Saudi Arabia’s My Clinic facility in Riyadh.

Middle East And Africa Magnetic Resonance Imaging (MRI) Market Report Scope

Magnetic resonance imaging is a medical imaging technique used in radiology to produce pictures of the anatomy and physiological processes of the body. These pictures are then used to diagnose and detect abnormalities in the body.

The Middle East and Africa MRI market is segmented by architecture, field strength, application, and geography. By architecture, the market is segmented into closed MRI systems and open MRI systems. By field strength, the market is segmented into low-field MRI systems, high-field MRI systems, and very high-field MRI systems and ultra-high MRI systems. By application, the market is segmented into oncology, neurology, cardiology, and other applications. By geography, the market is segmented into GCC, South Africa, and Rest of Middle East and Africa.

The report offers market sizes and forecasts in terms of value (USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (< 1.5 T) |

| High-Field (1.5 T) |

| Very-High (3 T) & Ultra-High (≥ 7 T) |

By Application

| Oncology |

| Neurology |

| Cardiology |

| Gastroenterology |

| Musculoskeletal |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Others |

By Geography

| GCC |

| South Africa |

| Rest of Middle East and Africa |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (< 1.5 T) |

| High-Field (1.5 T) | |

| Very-High (3 T) & Ultra-High (≥ 7 T) | |

| By Application | Oncology |

| Neurology | |

| Cardiology | |

| Gastroenterology | |

| Musculoskeletal | |

| Other Applications | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Others | |

| By Geography | GCC |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How big is the Middle East And Africa Magnetic Resonance Imaging Market?

The Middle East And Africa Magnetic Resonance Imaging Market size is expected to reach USD 405.34 million in 2025 and grow at a CAGR of 5.25% to reach USD 523.51 million by 2030.

Which MRI architecture currently leads revenues?

Closed systems hold 64.35% of 2024 revenue, reflecting their superior image quality for complex diagnostics.

Who are the key players in Middle East And Africa Magnetic Resonance Imaging Market?

Canon Medical Systems Corporation, Koninklijke Philips N.V, General Electric Company (GE Healthcare), Siemens Healthineers and FUJIFILM Corporation are the major companies operating in the Middle East And Africa Magnetic Resonance Imaging Market.

How are AI advances influencing MRI purchasing decisions?

Providers prioritize scanners with AI reconstruction because they cut scan times by up to 80% and mitigate radiologist shortages.

Page last updated on: