| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 34.25 Billion |

| Market Size (2030) | USD 46.49 Billion |

| CAGR (2025 - 2030) | 6.30 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East Military Vehicles Market Analysis

The Middle East Military Vehicles Market size is estimated at USD 34.25 billion in 2025, and is expected to reach USD 46.49 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

The Middle East military vehicles market is experiencing a significant transformation as regional powers focus on developing indigenous military manufacturing capabilities and reducing dependence on foreign imports. Countries across the region are establishing strategic partnerships with international defense contractors to facilitate technology transfers and local production capabilities. This shift is exemplified by Turkey's domestic defense industry, which has demonstrated remarkable progress with companies like BMC delivering over 300,000 defense vehicles to customers across more than 80 countries, highlighting the growing manufacturing capabilities in the region.

The market is witnessing a strong emphasis on naval vessel modernization and fleet expansion programs. Several countries are investing in developing their naval capabilities through both domestic production and international procurement. For instance, Egypt has made significant strides in its naval modernization efforts, with the Alexandria Shipyard successfully manufacturing naval vessels under strategic partnerships with international shipbuilders. The country has also focused on developing its submarine capabilities, demonstrating the region's commitment to enhancing maritime defense capabilities.

Regional powers are increasingly focusing on developing advanced combat systems and integrating modern technologies into their armed forces vehicles. This trend is particularly evident in the aerospace sector, where countries are not only procuring advanced aircraft but also developing maintenance, repair, and overhaul (MRO) capabilities. Iran, for example, has significantly enhanced its manufacturing capability and now produces more than 500 different parts for various helicopters, showcasing the region's growing technical expertise in complex military systems.

The market dynamics are heavily influenced by regional security concerns and the need to modernize aging military fleets. Saudi Arabia, which maintains one of the region's largest defense budgets with spending of approximately USD 57.52 billion, exemplifies the significant investment in military modernization programs. Meanwhile, countries like Egypt are taking a more measured approach, with military spending accounting for 1.2% of GDP, focusing on strategic acquisitions and upgrades to maintain operational effectiveness while balancing economic considerations. This diverse approach to military spending and modernization reflects the varying priorities and capabilities across the region.

Middle East Military Vehicles Market Trends

Growing Regional Conflicts and Security Threats

The Middle East continues to face multiple security challenges and ongoing conflicts, particularly in regions like Yemen, Libya, Somalia, and the Sinai Peninsula, driving the demand for combat vehicles and armored vehicles. These persistent threats have compelled regional powers to strengthen their military capabilities through enhanced vehicle procurement and modernization programs. The evolving nature of these conflicts, combined with the emergence of sophisticated militant groups, has particularly emphasized the need for advanced armored vehicles and military transport capabilities that can operate effectively in diverse terrain conditions.

The increasing focus on protecting critical infrastructure and conducting humanitarian assistance operations has led to specific requirements for specialized military vehicles. For instance, in February 2023, the UAE's procurement strategy for MRAP vehicles was specifically oriented towards force protection, humanitarian assistance operations, and critical infrastructure protection. Similarly, Iran has maintained a large fleet of wheeled and sand-blasted armored vehicles that can be modified for various missions, including fire support, demonstrating the region's adaptation to evolving security challenges.

Understand The Key Trends Shaping This Market

Download PDF

Military Modernization Programs

Countries across the Middle East are implementing comprehensive military modernization programs to enhance their defense capabilities. A prime example is the UAE's initiative to modernize all units of its armed forces with new and advanced military equipment. In February 2023, this commitment was demonstrated through a significant agreement between Nexter and International Golden Group for the modernization of the UAE Army's Leclerc main battle tanks, showcasing the region's focus on upgrading existing capabilities while acquiring new platforms.

Turkey's military modernization efforts have been particularly noteworthy, with programs spanning across air, land, and naval domains. In May 2023, FNSS Defence Systems was contracted to enhance the capability of the Turkish Army's ACV-15 advanced armored personnel carriers, extending their service life by 20 years with modern subsystems. Additionally, the Turkish military's ambitious program to increase the structural life of F-16 Block 30 jets from 8,000 to 12,000 flight hours, involving modifications to up to 1,500 parts per aircraft, demonstrates the comprehensive nature of these modernization initiatives. These efforts also include advancements in military autonomous vehicles and military unmanned ground vehicles, reflecting the growing trend towards automation in military operations.

Focus on Indigenous Manufacturing Capabilities

Middle Eastern countries are increasingly prioritizing the development of domestic military vehicle manufacturing capabilities to reduce dependence on foreign suppliers and enhance strategic autonomy. Turkey has emerged as a leading example in this trend, having significantly advanced its armored vehicle manufacturing capabilities and establishing itself as a major producer of military vehicles. This focus on indigenous production has been accompanied by substantial investments in research and development, leading to the creation of advanced military platforms like the TCG Anadolu, Turkey's first landing platform dock received in April 2023.

The emphasis on local manufacturing is further supported by strategic partnerships and technology transfer agreements with international defense companies. These collaborations are enabling regional manufacturers to develop sophisticated military vehicles while building local expertise and supply chains. For instance, the UAE's partnership with Otokar for the Rabdan 8x8 infantry fighting vehicles, with the first batch of 400 vehicles delivered in February 2023, exemplifies how countries are combining technology transfer with local production capabilities to achieve their military industrialization objectives. Moreover, the focus on developing tactical vehicles and combat vehicles locally is a testament to the region's commitment to enhancing its defense manufacturing capabilities.

Segment Analysis: Military Aircraft

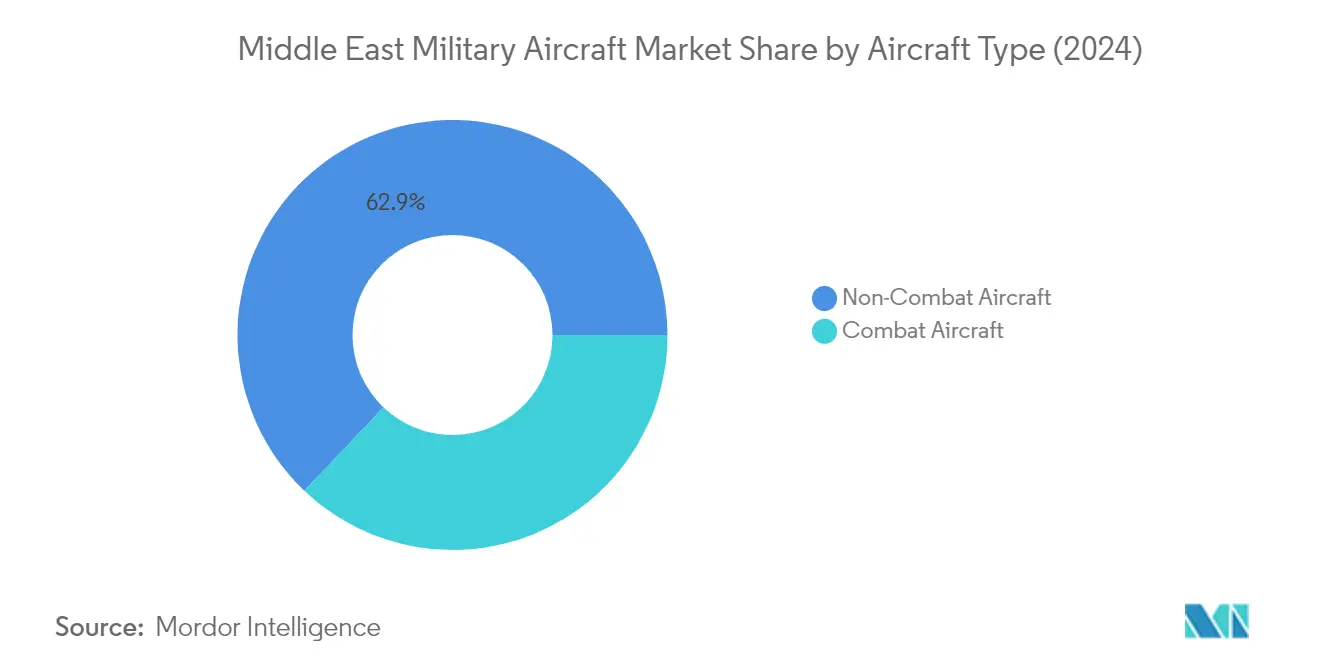

Non-Combat Aircraft Segment in Middle East Military Aircraft Market

The non-combat aircraft segment dominates the Middle East military aircraft market, accounting for approximately 63% of the total market share in 2024. This significant market share can be attributed to the increasing demand for reconnaissance and surveillance aircraft, transport aircraft, and trainer aircraft across the region. Countries like Saudi Arabia, the UAE, and Israel have been actively expanding their non-combat aircraft fleets to enhance their military logistics, training capabilities, and intelligence-gathering operations. The segment's dominance is further strengthened by the growing focus on maritime patrol aircraft and airborne early warning systems to monitor vast territorial waters and maintain regional security.

Combat Aircraft Segment in Middle East Military Aircraft Market

The combat aircraft segment is projected to witness the highest growth rate of approximately 4% during the forecast period 2024-2029. This growth is primarily driven by ongoing military modernization programs across Middle Eastern countries and increasing defense budgets allocated for fighter aircraft procurement. The segment's growth is further supported by rising regional tensions and the need to maintain air superiority. Countries in the region are actively pursuing advanced fighter aircraft acquisitions and upgrading existing fleets with modern combat capabilities. The increasing focus on indigenous combat aircraft development programs and technology transfer agreements with global aerospace manufacturers is also contributing to the segment's rapid growth.

Segment Analysis: Naval Vessels

Frigates Segment in Middle East Military Vehicles Market

The frigates segment dominates the Middle East military vehicles market's naval vessels category, commanding approximately 54% market share in 2024. This significant market position is driven by several major procurement programs across the region. The segment's growth is supported by countries like Saudi Arabia, which has awarded contracts for Multi-Mission Surface Combatant ships based on the Freedom-Class Littoral Combat Ship design. The UAE's naval modernization initiatives and Egypt's acquisition of FREMM frigates have further strengthened this segment's market position. These vessels are being equipped with advanced weapon systems, including surface-to-air missiles, anti-ship missiles, torpedoes, and sophisticated radar systems, making them crucial assets for maritime security operations in the region.

Submarines Segment in Middle East Military Vehicles Market

The submarines segment is experiencing rapid growth in the Middle East military vehicles market, with a projected growth rate of approximately 15% during 2024-2029. This growth is primarily driven by increasing investments in underwater warfare capabilities by regional naval forces. Countries like Egypt are expanding their submarine fleet with Type-209/1400 class submarines, while Iran continues to develop its indigenous submarine manufacturing capabilities. The segment's growth is further supported by technology transfer agreements and partnerships with established submarine manufacturers, enabling local production capabilities. Advanced features such as Air Independent Propulsion (AIP) systems, modern combat management systems, and enhanced stealth capabilities are becoming standard requirements for new submarine acquisitions in the region.

Remaining Segments in Naval Vessels

The other segments in the naval vessels category, including corvettes, destroyers, and other support vessels, collectively play vital roles in the Middle East's maritime defense infrastructure. Corvettes are gaining prominence as versatile platforms for coastal defense and patrol missions, with several countries investing in modern corvette programs. The destroyer segment, while smaller, represents an important capability for air defense and long-range operations. Other vessels, including patrol boats, mine countermeasure vessels, and amphibious transport ships, provide essential support capabilities for naval operations. These segments are witnessing steady modernization efforts as regional navies focus on developing comprehensive maritime capabilities to address evolving security challenges in the Persian Gulf and Red Sea regions.

Segment Analysis: Armored Vehicles

Main Battle Tank Segment in Middle East Military Vehicles Market

The main battle tank (MBT) segment dominates the Middle East military vehicles market, accounting for approximately 33% of the total market value in 2024. This significant market share can be attributed to the increasing focus on modernizing tank fleets across Middle Eastern countries and the growing need for enhanced battlefield capabilities. The segment is witnessing substantial growth due to several ongoing tank modernization programs, particularly in countries like Saudi Arabia, the UAE, and Egypt. The development of advanced MBTs with improved protection systems, enhanced firepower, and sophisticated electronics is driving market growth. Countries in the region are increasingly investing in next-generation tanks that offer better survivability, mobility, and combat effectiveness. The integration of modern technologies like advanced fire control systems, improved armor protection, and enhanced situational awareness capabilities has made MBTs more crucial than ever in modern warfare scenarios.

MRAP Segment in Middle East Military Vehicles Market

The Mine-Resistant Ambush Protected (MRAP) vehicle segment is experiencing significant growth in the Middle East military vehicles market, with a projected growth rate of approximately 5% from 2024 to 2029. The increasing focus on soldier survivability and protection against improvised explosive devices (IEDs) is driving the demand for MRAP vehicles. These vehicles are becoming increasingly important in asymmetric warfare scenarios common in the region. The growth is further supported by technological advancements in MRAP design, including improved blast protection, enhanced mobility features, and integration of modern communication systems. Regional manufacturers are developing indigenous MRAP capabilities, with several countries establishing local production facilities. The segment is also benefiting from the increasing adoption of MRAPs for various missions beyond traditional combat roles, including reconnaissance, command and control, and medical evacuation operations.

Remaining Segments in Armored Vehicles Market

The other segments in the Middle East military vehicles market include military personnel carriers (APCs), Infantry Fighting Vehicles (IFVs), and other specialized armored vehicles. APCs continue to play a crucial role in troop transport and battlefield mobility, with many countries in the region upgrading their APC fleets with modern variants featuring improved protection and mobility capabilities. The IFV segment is witnessing increased adoption due to its versatility in providing both troop transport and fire support capabilities. These vehicles are being equipped with advanced weapon systems and electronic warfare capabilities to enhance their battlefield effectiveness. The other specialized vehicles segment, though smaller in market share, serves specific military requirements such as engineering support, recovery operations, and specialized combat roles, contributing to the overall military capability of forces in the region.

Middle East Military Vehicles Market Geography Segment Analysis

Middle East Military Vehicles Market in Saudi Arabia

Saudi Arabia continues to dominate the Middle East military vehicles market, commanding approximately 36% of the total market share in 2024. The country's robust military modernization program, coupled with its strategic position in the region, has driven significant investments in military vehicles procurement. The Saudi Arabian Military Industries (SAMI), established as part of Vision 2030, plays a crucial role in developing indigenous manufacturing capabilities for military vehicles. The country's focus on localizing defense production has led to numerous partnerships with international defense contractors for technology transfer and local manufacturing. Saudi Arabia's comprehensive military vehicle portfolio spans across land, air, and naval domains, with particular emphasis on advanced fighter aircraft, naval vessels, and armored vehicles. The country's commitment to maintaining regional security and protecting its strategic assets has resulted in continued investments in military vehicle modernization and expansion programs.

Middle East Military Vehicles Market in Turkey

Turkey's military vehicles market is projected to grow at approximately 8% annually from 2024 to 2029, establishing itself as the fastest-growing market in the region. The country has made remarkable strides in developing its indigenous defense manufacturing capabilities, particularly in armored vehicles and naval vessels. Turkey's defense industry has evolved from being primarily an importer to becoming a significant exporter of military vehicles, with companies like Turkish Aerospace Industries (TAI) and BMC leading the charge. The country's focus on self-sufficiency in defense production has resulted in the development of numerous indigenous platforms, including the Altay main battle tank and various armored combat vehicles. Turkey's strategic location and its role in regional security affairs continue to drive investments in military vehicle capabilities. The country's emphasis on research and development, coupled with its growing expertise in unmanned systems and modern warfare technologies, has positioned it as a significant player in the regional military vehicles market.

Middle East Military Vehicles Market in Qatar

Qatar has emerged as a significant player in the Middle East military vehicles market, driven by its ambitious military modernization program. The country's strategic focus on building a modern and capable military force has led to substantial investments across all military vehicle segments. Qatar's procurement strategy emphasizes acquiring advanced technology platforms, including state-of-the-art fighter aircraft, naval vessels, and armored vehicles. The country has established strategic partnerships with various international defense contractors to ensure access to cutting-edge military vehicle technologies. Qatar's emphasis on developing its naval capabilities has resulted in significant investments in maritime platforms, including corvettes and patrol vessels. The country's commitment to maintaining regional security and protecting its maritime interests continues to drive investments in military vehicle capabilities. Additionally, Qatar's focus on building a comprehensive air defense capability has led to investments in advanced aircraft and associated support systems.

Middle East Military Vehicles Market in Israel

Israel maintains its position as a technological leader in the Middle East military vehicles market, driven by its strong domestic defense industry and focus on innovation. The country's emphasis on maintaining a qualitative military edge has resulted in the development of advanced military vehicles across all domains. Israel's defense industry, led by companies like Israel Aerospace Industries and Rafael, continues to develop cutting-edge military vehicles and associated technologies. The country's focus on autonomous systems and artificial intelligence integration in military vehicles has positioned it at the forefront of military technology innovation. Israel's unique security challenges have driven the development of specialized military vehicles designed for specific operational requirements. The country's expertise in unmanned systems and combat-proven platforms has made it a significant player in the global military vehicles market. Additionally, Israel's focus on developing advanced protection systems for military vehicles has resulted in numerous technological breakthroughs.

Middle East Military Vehicles Market in Other Countries

The military vehicles market in other Middle Eastern countries, including the United Arab Emirates, Iran, Egypt, and smaller Gulf states, continues to evolve with varying degrees of investment and technological advancement. These countries are focusing on modernizing their military vehicle fleets while developing indigenous manufacturing capabilities. The United Arab Emirates has made significant strides in developing its domestic defense industry, while Egypt continues to diversify its military vehicle suppliers. Iran's focus on self-reliance has driven domestic development of military vehicles, despite international restrictions. The smaller Gulf states are investing in modern military vehicles to enhance their defense capabilities and contribute to regional security efforts. These countries are increasingly emphasizing local production and maintenance capabilities through partnerships with international defense contractors. The focus on protecting maritime interests has driven investments in naval vessels, while land border security concerns continue to influence armored vehicle procurement decisions.

Get Analysis on Important Geographic Markets

Download PDF

Middle East Military Vehicles Industry Overview

Top Companies in Middle East Military Vehicles Market

The Middle East military vehicles market features prominent players like Lockheed Martin, Boeing, BAE Systems, Israel Aerospace Industries, and Rostec State Corporation leading the competitive landscape. Companies are heavily investing in research and development to create next-generation military engineering vehicles incorporating advanced technologies like AI, data fusion, and composite materials. Strategic partnerships and joint ventures with local companies have become increasingly common to establish manufacturing capabilities within the region, as evidenced by collaborations between global OEMs and entities in Saudi Arabia, UAE, and Turkey. Market leaders are focusing on expanding their product portfolios across air, land, and naval domains while simultaneously developing indigenous capabilities through technology transfer agreements. The competitive dynamics are further shaped by companies investing in modernization programs, offering comprehensive lifecycle support services, and developing specialized solutions for regional requirements.

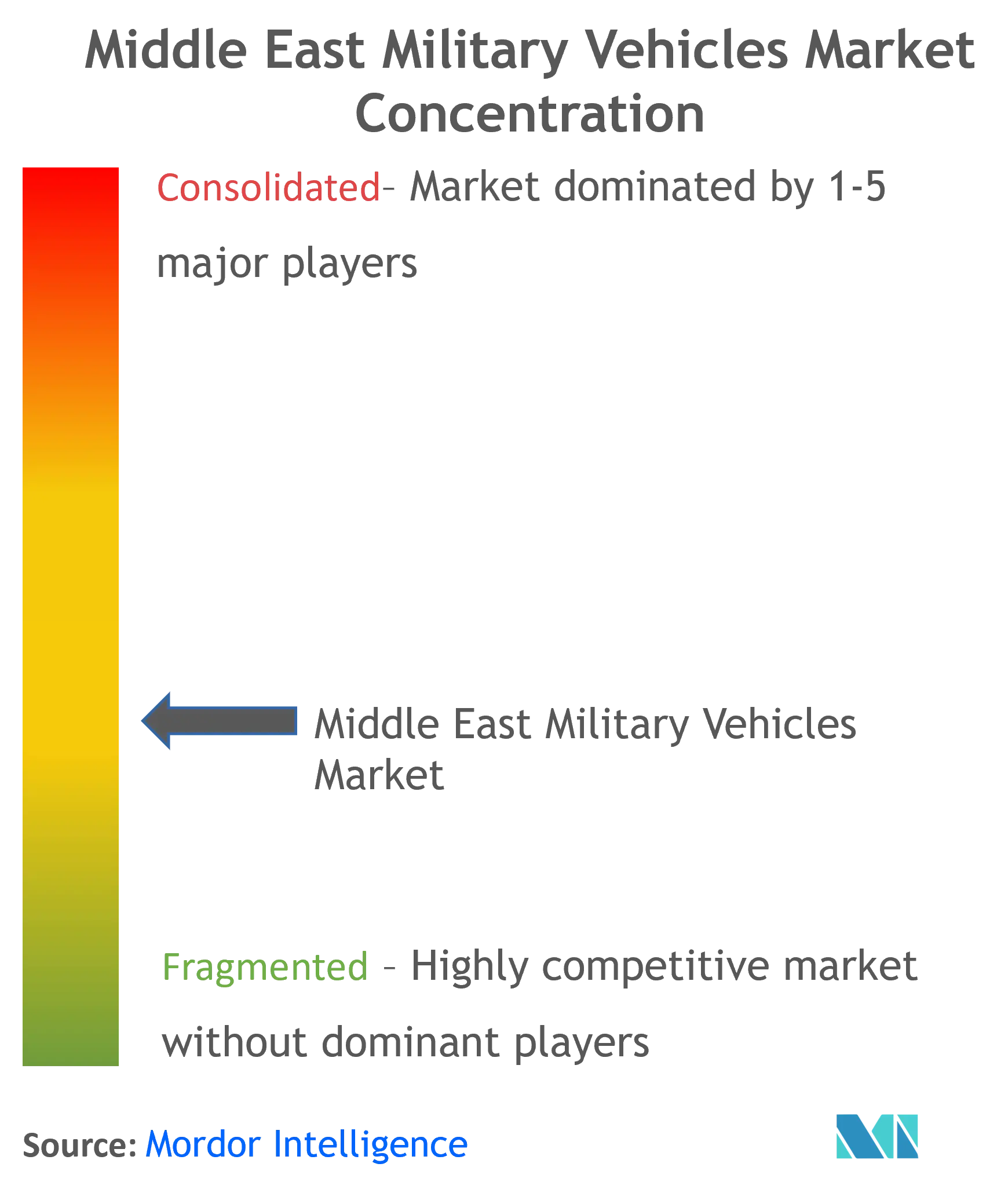

Market Structure Reflects Regional Defense Priorities

The market structure is characterized by a mix of established global defense contractors and emerging regional players developing indigenous capabilities. Traditional Western defense companies maintain strong positions through long-standing relationships and advanced technological offerings, while regional players like Israel Aerospace Industries, Turkish defense companies, and UAE's EDGE Group are rapidly expanding their capabilities. The market shows moderate consolidation with high barriers to entry due to significant capital requirements, stringent regulatory frameworks, and the need for proven technological expertise. Joint ventures and strategic partnerships between global and local players have become increasingly prevalent as countries push for local manufacturing and technology transfer.

The competitive landscape is evolving with an increased focus on developing domestic defense industrial bases in key markets like Saudi Arabia, UAE, and Turkey. These countries are actively promoting local defense companies through initiatives like Saudi Vision 2030 and UAE's EDGE Group formation, leading to new competitive dynamics. Market participants are adapting by establishing a local presence, forming industrial partnerships, and investing in regional manufacturing facilities. The emphasis on indigenous capabilities has led to the emergence of new players in specific segments, though they typically start with less complex systems before moving up the value chain through strategic collaborations and technology acquisition.

Innovation and Localization Drive Future Success

Success in the market increasingly depends on companies' ability to balance technological innovation with local industrial participation. Established players must focus on developing cutting-edge solutions while simultaneously building strong local partnerships and manufacturing capabilities. The ability to offer comprehensive solutions across multiple domains, provide technology transfer, and support the development of local supply chains has become crucial. Companies need to demonstrate long-term commitment to regional industrial development while maintaining their technological edge through continuous innovation and adaptation to evolving battlefield requirements.

Market contenders can gain ground by focusing on niche capabilities, particularly in emerging technology areas like unmanned systems, cyber defense, and advanced electronics. Building strong relationships with local defense establishments, understanding regional security requirements, and participating in offset programs are essential strategies for market entry and growth. The regulatory environment continues to emphasize local content and technology transfer, making it crucial for companies to develop flexible business models that can adapt to different national requirements. Success also depends on the ability to navigate complex procurement processes, build local talent pools, and establish sustainable supply chain networks within the region. Furthermore, the rise of military electric vehicles is becoming a significant trend, with companies exploring sustainable options to meet future defense needs.

Middle East Military Vehicles Market Leaders

-

Lockheed Martin Corporation

-

The Boeing Company

-

Saudi Arabian Military Industries (SAMI)

-

Leonardo S.p.A.

-

Rostec

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Middle East Military Vehicles Market News

- In October 2023, the Estonian Centre for Defence Investments awarded contracts to Turkish manufacturers Otokar and Nurol Makina to purchase roughly 230 armored vehicles for a total of about USD 211 million.

- In June 2022, Israel awarded a USD 28 million contract to IAI for the purchase of hundreds of combat vehicles for the country’s special forces.

Middle East Military Vehicles Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Military Aircraft

- 5.1.1 Combat Aircraft

- 5.1.1.1 Fighter Aircraft

- 5.1.1.2 Combat Helicopters

- 5.1.2 Non-combat Aircraft

- 5.1.2.1 Reconnaissance and Surveillance Aircraft

- 5.1.2.2 Trainer Aircraft

- 5.1.2.3 Transport Aircraft

- 5.1.2.4 Other Non-combat Aircraft

-

5.2 Naval Vessels

- 5.2.1 Destroyers

- 5.2.2 Frigates

- 5.2.3 Corvettes

- 5.2.4 Submarines

- 5.2.5 Other Naval Vessels

-

5.3 Armored Vehicles

- 5.3.1 Armored Personnel Carriers

- 5.3.2 Infantry Fighting Vehicles

- 5.3.3 Mine-Resistant Ambush Protected

- 5.3.4 Main Battle Tanks

- 5.3.5 Other Armored Vehicles

-

5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Turkey

- 5.4.5 Israel

- 5.4.6 Rest of the Middle East

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Rostec

- 6.2.2 Lockheed Martin Corporation

- 6.2.3 The Boeing Company

- 6.2.4 Abu Dhabi Ship Building Co.

- 6.2.5 IAI

- 6.2.6 BMC Otomotiv Sanayi ve Ticaret A.Ş.

- 6.2.7 Fincantieri S.p.A.

- 6.2.8 Saudi Arabian Military Industries (SAMI)

- 6.2.9 Dassault Aviation SA

- 6.2.10 Naval Group

- 6.2.11 Denel SOC Ltd.

- 6.2.12 BAE Systems plc

- 6.2.13 Oshkosh Corporation

- 6.2.14 Airbus SE

- 6.2.15 Leonardo S.p.A.

- 6.2.16 Patria Group

- 6.2.17 FNSS Savunma Sistemleri A.Ş.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Middle East Military Vehicles Industry Segmentation

The study provides insights into the procurement, indigenous manufacturing, upgrade activities, and development of military vehicles in the Middle Eastern region. Military vehicles include military aircraft, naval vessels, and armored vehicles.

The Middle East military vehicles market is segmented by military aircraft, naval vessels, armored vehicles, and geography. By military aircraft, the market is segmented into combat aircraft and non-combat aircraft. By naval vessels the market is segmented into destroyers, frigates, corvettes, submarines, and other naval vessels. The other naval vessels include patrol boats, support vehicles, etc. By armored vehicles the market is segmented into armored personnel carriers, infantry fighting vehicles, mine-resistant ambush protected, main battle tanks, and other armored vehicles. The report also offers the market size and forecasts for five countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD).

| Military Aircraft | Combat Aircraft | Fighter Aircraft | |

| Combat Helicopters | |||

| Non-combat Aircraft | Reconnaissance and Surveillance Aircraft | ||

| Trainer Aircraft | |||

| Transport Aircraft | |||

| Other Non-combat Aircraft | |||

| Naval Vessels | Destroyers | ||

| Frigates | |||

| Corvettes | |||

| Submarines | |||

| Other Naval Vessels | |||

| Armored Vehicles | Armored Personnel Carriers | ||

| Infantry Fighting Vehicles | |||

| Mine-Resistant Ambush Protected | |||

| Main Battle Tanks | |||

| Other Armored Vehicles | |||

| Geography | Saudi Arabia | ||

| United Arab Emirates | |||

| Qatar | |||

| Turkey | |||

| Israel | |||

| Rest of the Middle East | |||

Need A Different Region or Segment?

Customize Now

Middle East Military Vehicles Market Research FAQs

How big is the Middle East Military Vehicles Market?

The Middle East Military Vehicles Market size is expected to reach USD 34.25 billion in 2025 and grow at a CAGR of 6.30% to reach USD 46.49 billion by 2030.

What is the current Middle East Military Vehicles Market size?

In 2025, the Middle East Military Vehicles Market size is expected to reach USD 34.25 billion.

Who are the key players in Middle East Military Vehicles Market?

Lockheed Martin Corporation, The Boeing Company, Saudi Arabian Military Industries (SAMI), Leonardo S.p.A. and Rostec are the major companies operating in the Middle East Military Vehicles Market.

What years does this Middle East Military Vehicles Market cover, and what was the market size in 2024?

In 2024, the Middle East Military Vehicles Market size was estimated at USD 32.09 billion. The report covers the Middle East Military Vehicles Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Middle East Military Vehicles Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Middle East Military Vehicles Market Research

Mordor Intelligence offers a comprehensive analysis of the military vehicles and armed forces vehicles sector. We leverage decades of defense industry expertise to deliver this analysis. Our detailed report covers the full spectrum of defense vehicles, including main battle tanks, armoured vehicles, and combat vehicles. The research encompasses military automotive technologies, ranging from tactical vehicles to military amphibious vehicles. Stakeholders can access crucial insights in an easy-to-download report PDF format.

The analysis extensively covers military truck variants, military utility vehicles, and infantry fighting vehicles. It also examines emerging technologies such as military autonomous vehicles and military unmanned ground vehicles. Our research details various categories, including military transport vehicles, military engineering vehicles, military recovery vehicles, and military ambulance units. The report provides valuable insights into military logistics vehicles, military personnel carrier systems, and specialized categories like military tracked vehicles, military wheeled vehicles, and military patrol vehicles. This enables stakeholders to make informed decisions in this dynamic sector.